19 ASC 320 INVESTMENTS—DEBT AND EQUITY SECURITIES

Debt Securities and Equity Securities with Readily Determinable Fair Values

Classification of investment securities

Fair Value Readily Determinable

Held-to-Maturity Debt Securities

Sales within three months of maturity date

Example of held-to-maturity debt securities

Example of accounting for trading securities

Example of accounting for a realized gain on trading securities

Example of available-for-sale equity securities

Example of available-for-sale debt securities

Example of a transfer between trading and available-for-sale portfolios

Example of a transfer between available-for-sale and trading portfolios

Other-than-Temporary Impairment (OTTI)

Step 1—Determine whether the investment is impaired

Step 2—Evaluate whether the impairment is other than temporary

Recognition of an other-than-temporary impairment

Example of other-than-temporary impairment of an available-for-sale security

Example of temporary impairment

Subsequent measurement after recognition of an OTTI

Example of income statement presentation of OTTI

Subsequent accounting for debt securities after recognition of OTTI

Change in Fair Value Measurements After Yearend, Disclosures, and Elections

Changes in fair value after the date of the statement of financial position

PERSPECTIVE AND ISSUES

Subtopics

The Codification contains several Topics dealing with investments, including:

- ASC 320 - Investments—Debt and Equity Securities

- ASC 323, Investments—Equity Method and Joint Ventures

- ASC 325, Investments—Other.

ASC 320, Investments–Debt and Equity Securities contains one subtopic:

- ASC 320-10, Overall, that contains guidance for

- Passive investments in all debt securities and

- Those equity securities that have a readily determinable fair value.

Scope and Scope Exceptions

ASC 320 applies to all entities that do not belong to specialized industries for purposes of ASC 320. The entities to which it applies include

- Cooperatives,

- Mutual entities and

- Trusts that do not report substantially all their securities at fair value.

ASC 320 does not apply to “entities whose specialized accounting practices include accounting for substantially all investments in debt securities and equity securities at fair value, with changes in value recognized in earnings (income) or in the change in net assets,” such as brokers and dealers in securities, defined benefit and other portretirement plans, and investment companies. (ASC 320-15-3)

ASC 320 does not apply to

- Derivative instruments

- Cost method investments accounted for under ASC 325-20, except with respect to the impairment guidance in ASC 320-10-35

- Equity method investments absent the election of the fair value option under ASC 825-10-25-1

- Investments in consolidated subsidiaries.

(ASC 320-10-15-7)

In the case of an investment subject to ASC 320 with an embedded derivative, the host instrument is accounted for under ASC 320, and the embedded derivative is accounted for under ASC 815.

Overview

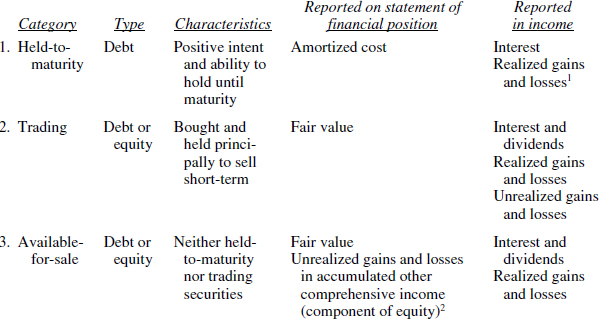

ASC 320 classifies these securities into one of three categories:

- Held-to-maturity,

- Trading, or

- Available-for-sale.

Because equity securities have no maturity date, the held-to-maturity category can only be applied to debt securities, which are then reported at amortized cost. The trading category can include both debt and equity securities, which are reported at fair value, via charges or credits included in current earnings. The available-for-sale category is used for those investments that do not fit in either of the other two classifications. Available-for-sale securities are also reported at fair value in the statement of financial position, however, changes in fair value are not reflected in current earnings.

Practice Alert

While SEC rules only apply to public entities, preparers of financial statements can benefit from the findings of SEC reviewers. Investments are a frequent topic of SEC comment letters. Determining when an investment is other-than-temporarily-impaired requires significant judgment. Neither the SEC nor the ASC offer definitive guidelines. The SEC commonly requests:

- Support for the preparer's conclusion that unrealized losses are temporary

- Information on how the preparer determined which period to report the impairment

- More transparent disclosures

- Basis for determining unrealized losses are recoverable

- How entities separate their OTTI losses on debt securities between credit and noncredit components.

With the worldwide economy continuing to experience volatility, the SEC recently has focused on disclosures related to holdings of sovereign debt issued by Eurozone member countries experiencing financial difficulty. Entities need to determine whether those debt securities will recover their entire amortized cost basis. Equity and privately debt securities issued in those areas also need a careful evaluation.

DEFINITIONS OF TERMS

Source: ASC 320-10-20 Glossary.

Amortized cost basis. The amount at which an investment is acquired, adjusted for accretion, amortization, collection of cash, previous other-than-temporary impairments recognized in earnings (less any cumulative-effect adjustments), foreign exchange, and fair value hedge accounting adjustments.

Asset group. An asset group is the unit of accounting for a long-lived asset or assets to be held and used that represents the lowest level for which identifiable cash flows are largely independent of the cash flows of other groups of assets and liabilities.

Available-for-sale-securities. Investments not classified as either trading securities or as held-to-maturity securities.

Component of an entity. A component of an entity comprises operations and cash flows that can be clearly distinguished, operationally and for financial reporting purposes, from the rest of the entity. A component of an entity may be a reportable segment or an operating segment, a reporting unit, a subsidiary, or an asset group.

Debt security. Any security representing a creditor relationship with an entity. The term debt security also includes all of the following:

- Preferred stock that by its terms either must be redeemed by the issuing entity or is redeemable at the option of the investor

- A collateralized mortgage obligation (or other instrument) that is issued in equity form but is required to be accounted for as a nonequity instrument regardless of how that instrument is classified (that is, whether equity or debt) in the issuer's statement of financial position

- US Treasury securities

- US government agency securities

- Municipal securities

- Corporate bonds

- Convertible debt

- Commercial paper

- All securitized debt instruments, such as collateralized mortgage obligations and real estate mortgage investment conduits

- Interest-only and principal-only strips.

The term debt security excludes all of the following:

- Option contracts

- Financial futures contracts

- Forward contracts

- Lease contracts

- Receivables that do not meet the definition of security and so are not debt securities (unless they have been securitized, in which case they would meet the definition of a security), for example:

- Trade accounts receivable arising from sales on credit by industrial or commercial entities

- Loans receivable arising from consumer, commercial, and real estate lending activities of financial institutions.

Equity security. Any security representing an ownership interest in an entity (for example, common, preferred, or other capital stock) or the right to acquire (for example, warrants, rights, and call options) or dispose of (for example, put options) an ownership interest in an entity at fixed or determinable prices. The term equity security does not include any of the following:

- Written equity options (because they represent obligations of the writer, not investments)

- Cash-settled options on equity securities or options on equity-based indexes (because those instruments do not represent ownership interests in an entity)

- Convertible debt or preferred stock that by its terms either must be redeemed by the issuing entity or is redeemable at the option of the investor.

Fair value. The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Holding gain or loss. The net change in fair value of a security. The holding gain or loss does not include dividend or interest income recognized but not yet received or write-downs for other-than-temporary impairment.

Operating segment. A component of a public entity. See Section 280-10-50 for additional guidance on the definition of an operating segment.

Readily determinable fair value. An equity security has a readily determinable fair value if it meets any of the following conditions:

- The fair value of an equity security is readily determinable if sales prices or bid-and-asked quotations are currently available on a securities exchange registered with the US Securities and Exchange Commission (SEC) or in the over-the-counter market, provided that those prices or quotations for the over-the-counter market are publicly reported by the National Association of Securities Dealers Automated Quotations systems (NASDAQ) or by Pink Sheets LLC. Restricted stock meets that definition if the restriction terminates within one year.

- The fair value of an equity security traded only in a foreign market is readily determinable if that foreign market is of a breadth and scope comparable to one of the US markets referred to above.

- The fair value of an investment in a mutual fund is readily determinable if the fair value per share (unit) is determined and published and is the basis for current transactions.

Reporting unit. The level of reporting at which goodwill is tested for impairment. A reporting unit is an operating segment or one level below an operating segment (also known as a component).

Retrospective interest method. A method of interest income recognition under which income for the current period is measured as the difference between the amortized cost at the end of the period and the amortized cost at the beginning of the period, plus any cash received during the period.

Security. A share, participation, or other interest in property or an entity of the issuer or an obligation of the issuer that has all of the following characteristics:

- It is either represented by an instrument issued in bearer or registered form or, if not represented by an instrument, is registered in books maintained to record transfers by or on behalf of the issuer.

- It is of a type commonly dealt in on securities exchanges or markets or, when represented by an instrument, is commonly recognized in any area in which it is issued or dealt in as a medium for investment.

- It is either one of a class or series or, by its terms, is divisible into a class or series of shares, participations, interests, or obligations.

Structured note. A debt instrument whose cash flows are linked to the movement in one or more indexes, interest rates, foreign exchange rates, commodities prices, prepayment rates, or other market variables. Structured notes are issued by US government-sponsored enterprises, multilateral development banks, municipalities, and private entities. The notes typically contain embedded (but not separable or detachable) forward components or option components such as caps, calls, and floors. Contractual cash flows for principal, interest, or both can vary in amount and timing throughout the life of the note based on nontraditional indexes or nontraditional uses of traditional interest rates or indexes.

Trading. An activity involving securities sold in the near term and held for only a short period of time. The term trading contemplates a holding period generally measured in hours and days rather than months or years. See paragraph 948-310-40-1 for clarification of the term trading for a mortgage banking entity.

Trading securities. Securities that are bought and held principally for the purpose of selling them in the near term and therefore held for only a short period of time. Trading generally reflects active and frequent buying and selling, and trading securities are generally used with the objective of generating profits on short-term differences in price.

CONCEPTS, RULES, AND EXAMPLES

Debt Securities and Equity Securities with Readily Determinable Fair Values

ASC 320, Investments—Debt and Equity Securities, governs the accounting for passive investments in all debt securities and for equity securities with readily determinable fair values.

Classification of investment securities.

Classification is made and documented at the time of the initial acquisition of each investment. (ASC 320-10-25-1 and 2) The appropriateness of classification is reassessed at each reporting date. ASC 320 requires all debt securities and equity securities with readily determinable fair values to be placed into one of three categories.

Classification of Debt Securities and Equity Securities

with Readily Determinable Fair Values

Presentation.

If a classified statement of financial position is presented, the debt and equity securities owned by an entity are grouped into current and noncurrent portfolios. By definition, all trading securities are classified as current assets. The determination of current or noncurrent status for individual held-to-maturity and individual available-for-sale securities is made on the basis of whether or not the securities are considered working capital available for current operations (ASC 210-10-45). Investments that are held for purposes of control of another entity or pursuant to an ongoing business relationship, for example, stock held in a supplier, would be excluded from current assets and would instead be listed as other assets or long-term investments.

Fair Value Readily Determinable.

The fair value of an equity security is considered readily determinable if:

- Sales prices or bid-and-ask quotations are currently available on SEC-registered exchanges or in an over-the-counter market publicly reported by NASDAQ or by Pink Sheets LLC. Unless qualified for sale within one year, restricted stock does not meet this definition.

- It is traded on a foreign market of comparable breadth and scope to one of the US markets identified above.

- It represents an interest in a mutual fund and fair value per unit (share) is determined and published and is the basis for current transactions.

Held-to-Maturity Debt Securities

If an entity has both the positive intent and the ability to hold debt securities to maturity, those maturities are measured and presented at amortized cost. Each investment in a debt security is evaluated separately. The held-to-maturity category does not include securities available for sale in response to a need for liquidity or changes in:

- Market interest rates

- Foreign currency risk

- Funding sources and terms

- Yield and availability of alternative investments

- Prepayment risk.

For asset-liability management purposes, similar or identical securities may be classified differently depending upon intent and ability to hold. (ASC 320-10-25-4)

Under ASC 860-20-35, securities such as interest-only strips, which can be settled in a manner that could cause the recorded amounts to not be substantially recovered, cannot be classified as held-to-maturity. Dependent upon the circumstances, those securities are to be categorized as either trading or available-for-sale.

Transfers.

In general, transfers to or from this category are not permitted. In those rare circumstances when there are transfers or sales of securities in this category, disclosure must be made of the following in the notes to the financial statements for each period for which the results of operations are presented:

- Amortized cost

- Realized or unrealized gain or loss

- Circumstances leading to the decision to sell or transfer.

ASC 320-10-25-6 lists changes in circumstances that are not considered inconsistent with the transfer, including:

- Material deterioration in creditworthiness of the issuer

- Elimination or reduction of tax-exempt status of interest through a change in tax law

- Major business disposition or combination

- Statutory or regulatory changes that materially modify what a permissible investment is or the maximum level of the security to be held

- Downsizing in response to a regulatory increase in the industry's capital requirements

- A material increase in risk weights for regulatory risk-based capital purposes.

Other events may prompt a sale or transfer of a held-to-maturity security before maturity (ASC 320-10-25-9).

These events should be:

- Isolated

- Nonrecurring

- Unusual for the reporting entity

- Not able to be reasonably anticipated.

Sales Within Three Months of Maturity date.

The sale of a security within three months of its maturity meets the requirement to hold to maturity, since the interest rate risk is substantially diminished. Likewise, if a call is considered probable, a sale within three months of that date meets the requirement. The sale of a security after collection of at least 85% of the principal outstanding at acquisition (due to prepayments or to scheduled payments of principal and interest in equal installments) also qualifies, since the “tail” portion no longer represents an efficient investment due to the economic costs of accounting for the remnants. Scheduled payments are not required to be equal for variable-rate debt.

The 12/31/12 debt security portfolio categorized as held-to-maturity is as follows:

The statement of financial position would report all the securities in this category at amortized cost and would classify them as follows:

Interest income, including premium and discount amortization, is included in income. Any realized gains or losses are also included in income.

Trading Securities

If an entity has debt and/or equity securities (with readily determinable fair value) that it intends to actively and frequently buy and sell for short-term profits, those securities are classified as trading securities. Unless classified as held-to-maturity securities, under ASC 948 mortgage-backed securities held for sale require classification as trading securities. The securities in this category are required to be carried at fair value on the statement of financial position as current assets. All applicable interest and dividends, realized gains and losses, and unrealized gains and losses on changes in fair value are included in income from continuing operations.

The year one current trading securities portfolio is as follows:

A $400 adjustment is required in order to recognize the decline in fair value. The entry required is

The unrealized loss would appear on the income statement as part of other expenses and losses. Dividend income and interest income (including premium and discount amortization) is included in income. Any realized gains or losses from the sale of securities are also included in income.

An alternative to direct write-up and write-down of securities is the use of an asset valuation allowance account to adjust the portfolio totals. In the above example, the entry would be:

![]()

The valuation allowance of $400 would be deducted from historical cost to obtain a fair value of $6,600 for the trading securities on the statement of financial position.

All trading securities are classified as current assets and the statement of financial position would appear as follows:

![]()

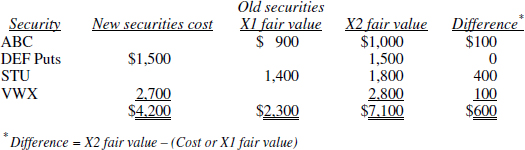

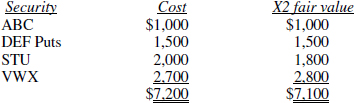

The year two current trading portfolio is as follows:

A $600 adjustment is required in order to recognize the increase in fair value. The entry required is

The unrealized gain would appear on the income statement as part of other income.

- The same information as given in the above example for year one

- In year two, the MNO calls are sold for $1,600 and the XYZ 7% bonds are sold for $2,700.

The entry required to record the sale is:

Under the valuation allowance method, the current trading portfolio would appear as follows:

The required entries to recognize the increase in fair value and the realized gain are:

![]()

To adjust the valuation allowance to reflect the unrealized loss of $100 at the end of year two on the remaining trading portfolio

The statement of financial position under both methods would appear as follows:

![]()

Available-for-Sale Securities

Investments in debt securities and in equity securities with a readily determinable fair value that are not classified as either trading securities or held-to-maturity are classified as available-for-sale. The securities in this category are required to be carried at fair value on the statement of financial position. The determination of current or noncurrent status for individual securities depends on whether the securities are considered working capital (ASC 210-10-45).

Other than the possibility of having some noncurrent securities on the statement of financial position, the major difference between trading securities and available-for-sale securities is the handling of unrealized gains and losses. Unlike trading securities, the unrealized gains and losses of available for sale securities are excluded from net income. Instead, they are reported in other comprehensive income per ASC 220. All applicable interest (including premium and discount amortization) and any realized gains or losses from the sale of securities are included in income from continuing operations.

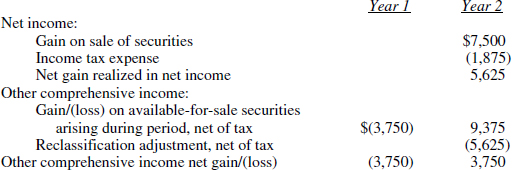

Bonito Corporation purchases 2,500 shares of equity securities at $6 each, which it classifies as available-for-sale. At the end of one year, the quoted market price of the securities is $4, which rises to $9 at the end of the second year, when Bonito sells the securities. The company has an incremental tax rate of 25%. The calculation of annual gains and losses follows:

Bonito reports these gains and losses in net income and other comprehensive income in the indicated years as follows:

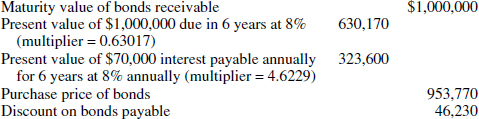

Bonito Corporation purchases 10,000 bonds of Easter Corporation maturing in 6 years, at a price of $95.38, and classifies them as available-for-sale. The bonds have a par value of $100 and pay interest of 7% annually. At the price Bonito paid, the effective interest rate is 8%. The calculation of the bond discount follows:

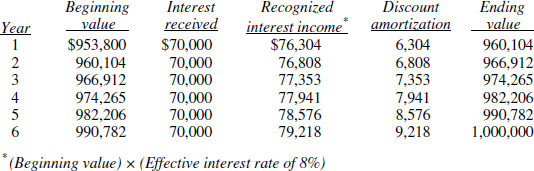

The complete table of interest income and discount amortization calculations for the remaining life of the bonds follows:

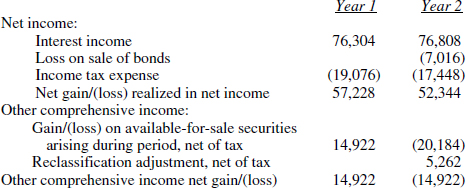

At the end of Year 1, the quoted market price of the bonds is $98, and it is $94 at the end of Year 2. The company has an incremental tax rate of 25%. The following table calculates the before-tax and after-tax holding gains and losses on the investment.

Bonito sells the bonds at the end of Year 2, and reports these gains and losses in net income and other comprehensive income in the indicated years as follows:

Deferred Income Tax Effects

The recognition of unrealized gains and losses for financial statement purposes is likely to have deferred income tax effects. See the discussion in the chapter on AsC 740, Income Taxes.

Transfers Between Categories

A major reason for the development of the guidance in ASC 320 was the concern that under the prior rules there had been too many instances where management had been able to deliberately affect reported net income by careful selection of portfolio securities to be sold in a given period. The practice, typically known as “gains trading,” was widely blamed for misleading financial reporting, primarily by financial institutions (which generally hold significantly larger investment portfolios than do other business enterprises). In a gains trading situation, management seeking additional net income would sell securities from the nontrading portfolio having low carrying values based on their original acquisition cost versus current market values. Since these securities had not previously been reported at fair value, the gain would be reported in net income of the period of sale. In a variation on this process, securities held in a trading account, but suffering declining value, would be reclassified to a nontrading portfolio, thus averting a charge against net income to reflect the decline.

ASC 320 includes provisions intended to curtail the abuses described above. Transfers from one of the three portfolio classifications to any other are expected to be rare. ASC 320 provisions impose limitations on situations in which it would be permissible to transfer investments between portfolios. With respect to debt securities (discussed in detail later in this chapter), ASC 320 prohibits the use of the “held-to-maturity” classification once it has been “tainted” by sales of securities that had been classified in that portfolio. (ASC 320-10-35-8 and 9)

Securities purchased for the trading portfolio are so classified because it is management's intent to seek advantage in short-term price movements. The fact that management does not in fact dispose of those investments quickly would not necessarily mean that the original categorization was improper or that an expressed changed intent calls for an accounting entry. While transfers out of the trading category are not completely prohibited, they would have to be supported by facts and circumstances making the assertion of changed intent highly credible.

Measurement.

Transfers among portfolios are accounted for at fair value as of the date of the transfer. Generally, investments in the trading category transferred to the available-for-sale category warrant no further recognition of gain or loss, as the carrying value of the investments already reflect any unrealized gains or losses experienced since their original acquisition. The only caveat is that, if the reporting entity's accounting records of its investments, as a practical matter, have not been updated for fair values since the date of the most recently issued statement of financial position, any changes occurring since that time need to be recognized at the date the transfer occurs. The fair value at the date of transfer becomes the new “cost” of the equity security in the available-for-sale portfolio.

In brief, fair value is used for transfers between categories. When the security is transferred, any unrealized holding gains and losses are accounted for in the following manner:

- From trading—Already recognized and not to be reversed

- Into trading—Recognize immediately in income

- Available-for-sale debt security into held-to-maturity—Report the unrealized holding gain or loss at the transfer date as other comprehensive income and amortize the gain or loss over the investment's remaining life as an adjustment of yield in the same manner as a premium or discount. The transferred-in security will probably record a premium or discount since fair value is used. Thus, the two amortizations will tend to cancel each other on the income statement.

- Held-to-maturity debt security into available-for-sale—Recognize in other comprehensive income per ASC 220. Few transfers are expected from the held-to-maturity category.

Neihaus Corporation's investment in Rabin Restaurants' common stock was assigned to the trading portfolio and at December 31, 2012, was reflected at its fair value of $88,750. Assume that in April 2013 management now determines that this investment will not be traded, but rather will continue to be held indefinitely. Under the criterion established by ASC 320, this investment now belongs in the available-for-sale portfolio. Assume also that the fair value at the date this decision is made is $92,000, and that no adjustments have been made to the accounting records since the one that recognized the fair value increase to $88,750. The entry to record the transfer from the trading portfolio to the available-for-sale portfolio is:

![]()

Unrealized gains and losses on trading securities are always recognized in income, and in this example the additional increase in fair value since the last fair value adjustment, $3,250, is recognized at the time of the transfer to the available-for-sale portfolio. Further gains after this date, however, will not be recognized in net income, but rather will be included in other comprehensive income per ASC 220.

For securities being transferred into the trading category, any unrealized gain or loss (that had previously been recorded in accumulated other comprehensive income, as illustrated above) is deemed to have been realized at the date of the transfer. Also, any fair value changes since the date of the most recent statement of financial position may need to be recognized at that time.

NOTE: Items affecting other comprehensive income or loss are required to be recorded net of income tax. For illustrative purposes, the income tax effects of such transactions have been ignored.

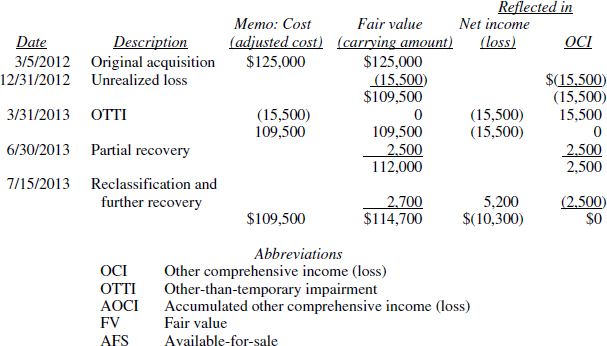

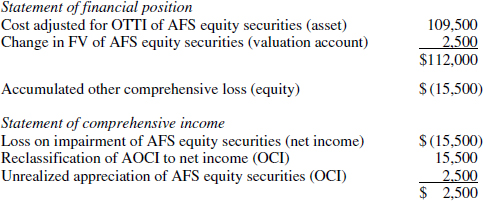

The investment in Mitzen preferred stock was held in the available-for-sale portfolio and had been adjusted at December 31, 2012, from its original acquisition cost of $125,000 to an end-of-year fair value of $109,500 by reflecting in other comprehensive loss the $15,500 unrealized decline in fair value that management judged to be temporary.

At March 31, 2013, the fair value of Mitzen remained at $109,500 and management now believed the unrealized loss to be an other-than-temporary impairment. As discussed in detail later in this chapter, this loss was recognized as a charge to net income at March 31, 2013, and reclassified (“recycled”) from accumulated other comprehensive income into net income to prevent duplication in the financial statements (see summary table below).

At June 30, 2013, the fair value of Mitzen had increased slightly from $109,500 to $112,000. Because Mitzen shares were classified as “available-for-sale,” this increase is reflected in other comprehensive income and is computed as:

Fair value of $112,000 − Cost adjusted for OTTI $109,500 = $2,500.

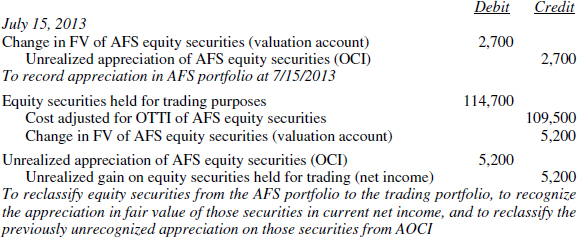

On July 15, 2013, management reverses course and decides to try to sell the investment in the short term. Thus, the shares no longer qualify to be classified as available-for-sale and are now considered securities held for trading purposes. The fair value of the shares held at the date of decision is $114,700.

The activity described above with respect to Mitzen is summarized as follows:

On July 15, 2013, immediately preceding the reclassification of the investment from available-for-sale to trading, the accounting records reflect the following componentized balances (assuming these were the only transactions occurring during the period):

The entry to record the transfer from available-for-sale to trading and the “realization” of the increase in fair value from $112,000 to $114,700 at that date is as follows:

The recognized gain at the time of transfer, in this case, is the sum of the previously unrecognized gain that had been recorded in accumulated other comprehensive income (AOCI), the additional equity account ($2,500) plus the further gain not yet recognized in the investor's financial statements ($2,700). Note that the elimination of the additional equity representing the previously reported unrealized gain will be included in comprehensive income in the current period as a debit, since the additional equity account is being reversed at this time.

Other-than-Temporary Impairment (OTTI)

ASC 320-10-35-17 through 34E address the impairment of individual available-for-sale and held-to-maturity securities.

Scope.

The guidance on impairment of individual available-for-sale and held to maturity securities applies to

- Debt and equity securities within the scope of ASC 320 with the following clarifications:

- All equity securities held by insurance entities are included in the scope of the guidance.

- Entities are not to “look through” the form of their investment to the nature of the securities held by the investee entity. So, for example, if the reporting entity holds an investment in shares of a mutual fund whose investment strategy is to invest primarily in debt securities, management is to assess the mutual fund investment as an equity security, since the shares held by the reporting entity represent equity in the mutual fund, irrespective of the fact that the mutual fund's holdings are comprised primarily of debt.

- If the application of ASC 815-15-25 (recognition of embedded derivatives) results in bifurcating an investment into a host instrument and an embedded derivative, the host instrument would be evaluated for impairment under this guidance if it falls within its scope.

- The standard applies to debt and equity securities that are (a) within the scope of ASC 958-320 (not-for-profit entities' investments in debt and equity securities) and (b) that are held by an investor that reports a performance indicator.

- Cost-method investments in equity securities.

ASC 320-10-35 establishes a multistep decision process to determine if an investment has been impaired, evaluate whether the impairment is other than temporary, and if OTTI is determined to have occurred, measure the impairment loss. It also establishes a discrete model for assessing impairment of cost-method investments that present unique challenges since reasonable estimation of their fair value is often not practical or cost effective.

Unit of accounting.

The unit of accounting to be used for the purpose of performing these steps is the individual security level. This is defined as the level and method of aggregation used by the reporting entity to measure realized and unrealized gains and losses on its debt and equity securities. An example of an acceptable method of aggregation would be for the reporting entity to consider equity securities of an issuer that carry the same Committee on Uniform Security Information Procedures (CUSIP) number that were purchased in separate trade lots to be considered together on an average cost basis.

In considering whether the issuer (i.e., borrower or debtor) of a debt security can prepay or settle the security in a manner that would result in the investor not recovering substantially all of its cost, the investor is not permitted to combine separate contracts such as a debt security and a guarantee or other credit enhancement.

The model set forth for investments, other than those accounted for using the cost method follows.

Step 1—Determine whether the investment is impaired.

An investment is impaired if its fair value is less than its cost. Cost as defined for this purpose includes adjustments made to the cost basis of an investment for accretion, amortization, previous OTTIs, and hedging.3

In assessing impairment of debt securities, the investor is not permitted to combine separate contracts such as guarantees or other credit enhancements.

The assessment of whether an investment is impaired is to be made for each interim and annual reporting period, subject to special provisions that apply to cost-method investments discussed separately below.

After comparing fair value to cost, if cost exceeds fair value, the investment is considered impaired, and the evaluator is to then proceed to Step 2 to evaluate whether the impairment is considered to be “other than temporary.”

Step 2—Evaluate whether the impairment is other than temporary.

If the fair value of the investment is less than its cost at the ending date of a reporting period (the date of the latest statement of financial position), management is tasked with evaluating whether the impairment is temporary, or whether it is “other-than-temporary.” While the term “other-than-temporary” is not defined, FASB affirmatively states that it does not mean permanent. Thus a future recovery of all or a portion of the decline in fair value is not necessarily indicative that an assessment of OTTI made in prior periods was incorrect.

OTTI of available-for-sale (AFS) equity securities (ASC 320-10-35-32A). When the fair value of an equity security declines, management is to start with a working premise that the decline may necessitate a write-down of the security. With that mindset, management is to investigate the reasons for the decline by considering all available evidence to evaluate the AFS equity investment's realizable value. Many factors should be considered by management in performing the evaluation and, of course, the evaluation will depend on the individual facts and circumstances. The SEC's Stafff Accounting Bulletin Series, Topic 5.M provides a few examples of factors that, when considered individually or in the aggregate, indicate that a decline in fair value of an AFS equity security is other-than-temporary, and that an impairment write-down of the carrying value is required.

- The period of time and the extent to which the fair value has been less than cost.

- The financial condition and near-term prospects of the issuer, including any specific events that might influence the operations of the issuer such as changes in technology that may impair the earnings potential of the investment or the discontinuance of a segment of the business that may affect the future earnings potential; or

- The intent or ability of the holder to retain its investment in the issuer for a period of time sufficient to allow for any anticipated recovery in fair value.

Unless there is existing evidence supporting a realizable value greater than or equal to the carrying value of the investment, a write-down to fair value accounted for as a realized loss is to be recorded. The loss is to be recognized as a charge to net income in the period in which it occurs and the written-down value of the investment in investee becomes the new cost basis of the investment.

It is important to note that, if an investor has decided to sell an impaired AFS equity security, and the investor does not expect the fair value of the security to fully recover prior to the expected time of sale, the security is to be considered OTTI in the period in which the investor decides to sell the security. However, even if a decision to sell the security has not been made, the investor is to recognize OTTI when that impairment has been determined to have been incurred.

OTTI of debt securities. (ASC 320-10-35-33A through 33I) If the fair value of a debt security is less than its amortized cost basis at the date of the statement of financial position, management is to assess whether the impairment is an OTTI.

If management intends to sell the security, then an OTTI is considered to have been incurred.

If management does not intend to sell the security, management should consider all available evidence to assess whether, it is more likely than not, that it will be required to sell the security prior to recovery of its amortized cost basis (e.g., whether the entity's cash or working capital requirements, or contractual or regulatory obligations, will require sale of the security prior to the occurrence of a forecasted recovery). If it is more likely than not that a sale will be required prior to recovery of the security's amortized cost basis, OTTI is considered to have been incurred.

If, at the measurement date, management does not expect to recover the entire amortized cost basis, this precludes an assertion that it will recover the amortized cost basis irrespective of whether management's intent is to continue holding the security or to sell the security. Therefore, when this is the case, OTTI is considered to have been incurred.

Expected recovery is computed by comparing the present value of cash flows expected to be collected (PVCF) from the security to the security's amortized cost basis.

If PVCF is less than amortized cost basis, the entire amortized cost basis of the security will not be recovered; a credit loss has occurred, and an OTTI has been incurred.

Amortized cost basis (ACB) includes adjustments made to the original cost of the investment for such items as:

- Accretion

- Amortization

- Cash collections

- Previous OTTI recognized as charges to net income (less any cumulative-effect adjustments recognized in transitioning to the provisions of FSP 115-2)

- Fair value hedge accounting adjustments.

In determining whether a credit loss has been incurred, management must use its best estimate of the present value of cash flows expected to be collected from the debt security.

The computation, in simple terms, is made by discounting the expected cash flows at the effective interest rate implicit in the security at the date of its acquisition. A methodology for estimation of that amount is described in ASC 310, which is codified in the ASC as follows:

- ASC 310-10-35-21 through 35-37

- ASC 310-30-30-2

- ASC 310-40-35-12.

Many factors influence the estimate of whether a credit loss has occurred and the period over which the debt security is expected to recover (ASC 320-10-35-33F). Examples of these factors include, but are not limited to:

- The length of time and the extent to which the fair value of the security has been less than its amortized cost basis

- Adverse conditions that relate specifically to the security, an industry, or a geographic locale such as:

- Changes in the financial condition of the issuer of the security or, in the case of asset-backed securities, changes in the financial condition of the underlying loan obligors

- Changes in technology

- Discontinuance of a segment of the business that may affect the future earnings potential of the issuer or underlying loan obligors of the security

- Changes in the quality of a credit enhancement

- The historical and implied volatility of the fair value of the security

- The payment structure of the debt security and the likelihood of the issuer being able to make payments that are scheduled to increase in the future; examples of nontraditional loan terms are described in ASC 310-10-50-25, ASC 825-10-55-1, and ASC 825-10-55-2

- Failure of the security's issuer to make scheduled interest or principal payments

- Changes in the rating of the security by a ratings agency

- Recoveries or additional declines in fair value that occur subsequent to the date of the statement of financial position.

In developing the estimate of PVCF for the purpose of assessing whether OTTI has occurred (or recurred), management should consider all available information relevant to the collectability of sums due under the terms of the security, including information about past events, current conditions, and reasonable and supportable forecasts. That information generally is to include:

- The remaining payment terms of the security,

- Prepayment speeds,

- The financial condition of the issuer(s),

- Expected defaults, and

- The value of the collateral.

(ASC 320-10-35-33G)

To accomplish this objective, management should consider, for example:

- Industry analyst reports and forecasts,

- Sector credit ratings, and

- Other market data relevant to the collectability of the security.

(ASC 320-10-35-33H)

Management must also consider how other credit enhancements affect the expected performance of the security, including:

- The current financial condition of the guarantor of the security (unless the guarantee is a separate contract under ASC 320-10-35-23), and/or

- Whether any subordinated interests are capable of absorbing estimated losses on the loans underlying the security.

(ASC 320-10-35-33I) The remaining payment terms of the security could differ significantly from the payment terms in prior periods, such as when securities are backed by nontraditional loans (e.g., reverse mortgages, interest-only debt, adjustable-rate products). As a result, management must consider whether currently performing loans that back a security will continue to perform when required payments increase in the future, including any required “balloon” payments. Management should also consider how the value of any collateral would affect the security's expected performance. If there has been a decline in the fair value of the collateral, management is to assess the effect of that decline on the ability of the entity to collect the balloon payment.

Recognition of an other-than-temporary impairment.

If, as a result of Step 2, management judges the impairment to be other than temporary, the reporting entity recognizes an impairment loss as a charge to net income for the entire difference between the investment's cost and its fair value at the date of the statement of financial position. The impairment measurement must not to include any partial recoveries that might have occurred subsequent to the date of the statement of financial position but prior to issuance of the financial statements.

The reduced carrying amount of the investment becomes that investment's new cost basis. This new cost basis is not changed for any subsequent recoveries in fair value. Subsequent recoveries in the fair value of available-for-sale securities are included in other comprehensive income; subsequent decreases in fair value are evaluated as to whether they are other than temporary in nature. If considered temporary, the decrease is recorded in other comprehensive income. If considered other than temporary, the decrease is to be recognized as a component of net income for the period as previously described.

Determining OTTI of debt securities to be recognized in net income and in other comprehensive income (OCI). ASC 320 permits reporting entities to split OTTI of debt securities into two components and thus recognize only a portion of the OTTI as a charge to net income when incurred. The remaining portion is to be accounted for through other comprehensive income as described in the following paragraphs.

When an OTTI has been incurred with respect to a debt security, the amount of the OTTI recognized in net income is dependent upon whether management intends to sell the security or more likely than not will be required to sell the security prior to recovery of its ACB, less any recognized current period credit loss, as explained below.

As discussed previously, if management intends to sell the security or more likely than not will be required to sell the security prior to recovery of its amortized cost basis, less any current period credit loss, the OTTI to be recognized in net income equals the entire difference between the investment's amortized cost basis and its fair value at the date of the statement of financial position. Stated differently, in this situation, the entire amount of the OTTI is deemed to be a credit loss and is recognized as an immediate charge to net income in its entirety.

- Management does not intend to sell the security, and

- It is more likely than not the entity will not be required to sell the security prior to recovery of its amortized cost basis less any current period credit lost, the OTTI is to be separated into two components as follows:

Component 1: The amount representing the credit loss, and

Component 2: The remaining amount, which is presumed to be related to all other factors (but that economically is inseparable from the factors that would cause a loss to be characterized as being from deteriorated credit quality).

Component 1 is to be recognized in its entirety in net income and Component 2 is to be recognized in OCI, net of applicable income taxes.

The previous ACB less Component 1 of the current year's OTTI that represents the current period credit loss is to become the new amortized cost basis of the investment prospectively. That new ACB is not to be adjusted for subsequent recoveries in fair value. The amortized cost basis is to be adjusted, however, for accretion and amortization, as described in the next section.

In January 2013 new information comes to the attention of Neihaus Corporation management regarding the viability of Mitzen Corp. Based on this information, it is determined that the decline in Mitzen preferred stock is probably not a temporary one, but rather is other than temporary (i.e., the asset impairment requires financial statement recognition). ASC 320 prescribes that such a decline be reflected in net income and the written-down value be treated as the new cost basis. The fair value has remained at the amount last reported, $109,500. Accordingly, the entry to recognize the fact of the investment's permanent impairment is as follows:

Any subsequent recovery in this value would not be recognized in net income unless realized through a sale of the investment to an unrelated entity in an arm's-length transaction, as long as the investment continues to be categorized as “available-for-sale,” as distinct from “held-for-trading.” However, if there is an increase in value (not limited to just a recovery of the amount of the loss recognized above, of course) the increase will be added to the investment account and shown in a separate account in stockholders' equity, since the asset is to be marked to fair value on the statement of financial position.

It should be noted that the issue of other-than-temporary impairment does not arise in the context of investments held for trading purposes, since unrealized holding gains and losses are immediately recognized without limitation. In effect, the distinction between realized and unrealized gains or losses does not exist for trading securities.

In March 2013 further information comes to management's attention, which now suggests that the decline in Mitzen preferred was indeed only a temporary decline; in fact, the value of Mitzen now rises to $112,000. Since the carrying value after the recognition of the impairment was $109,500, which is treated as the new cost basis for purposes of measuring further declines or recoveries, the increase to $112,000 will be accounted for as an increase to be reflected in the additional stockholders' equity account (AOCI), as follows:

Note that this increase in fair value is not recognized in current net income, since the investment is still considered to be available-for-sale, rather than a part of the trading portfolio. Even though the previous decline in Mitzen stock was realized in current net income, because judged at the time to be an OTTI, the recovery is not permitted to be recognized in net income. Rather, the change in fair value will be included in other comprehensive income and then displayed in AOCI.

Subsequent measurement after recognition of an OTTI.

After recognition of an OTTI, the impaired security is to be accounted for as follows. Management is to account for the debt security subject to OTTI as if that security had been purchased on the measurement date of the OTTI at an amortized cost basis equal to the previous amortized cost basis less Component 1 of the OTTI (the portion recognized as a charge to net income as a current period credit loss).

Debt securities classified as available-for-sale (AFS). Subsequent increases and decreases in the fair value of AFS securities, if not caused by an additional OTTI, are to be included in OCI.

Debt securities classified as held-to-maturity. The OTTI recognized in OCI for held-to-maturity securities is to be prospectively accreted (sometimes referred to as “recycling”) from other comprehensive income (OCI) to the amortized cost of the debt security over its remaining life based on the amount and timing of future estimated cash flows. That accretion is to increase the security's carrying value and is to continue until the security is sold, matures, or there is an additional OTTI charged to net income. If the security is sold, guidance on the effect of changes in circumstances that would not call into question management's intent to hold other debt securities to maturity in the future is discussed in a previous section of this chapter and is provided in the following authoritative literature:

- ASC 320-10-25-6, and 25-9

- ASC 320-10-25-14

- ASC 320-10-50-11.

Additional guidance with respect to subsequent period accounting. For debt securities for which OTTI has been recognized as a charge to net income, the difference between the new amortized cost bais and the cash flows expected to be collected is to be accreted following existing guidance on interest income. Management is to continue to estimate the PVCF expected to be collected over the remaining life of the debt security.

For debt securities accounted for under Emerging Issues Task Force (EITF) 99-20 (i.e., specified beneficial interests in securitized financial assets) management is to apply the provisions of ASC 325-40 to account for changes in the PVCF.

For all other debt securities, if subsequent evaluation indicates a significant increase in the PVCF or if actual cash flows are significantly greater than cash flows previously expected, those changes are to be accounted for as a prospective adjustment to the accretable yield of the security under ASC 310-30, even if the debt security would not otherwise be subject to the scope of that standard.

Income statement presentation.

In periods in which management determines that a decline in the fair value of a security below its amortized cost basis is other than temporary, management is to present the total OTTI in the income statement with an offset for the amount of the total OTTI that is recognized in OCI, if any (Component 2).

In the financial statement where the components of accumulated other comprehensive income (AOCI) are reported, management is to separately present the amounts recognized in AOCI related to held-to-maturity and available-for-sale debt securities for which a portion of an OTTI has been recognized as a charge to net income.

Subsequent accounting for debt securities after recognition of OTTI.

After recognizing a loss from other-than-temporary impairment with respect to a debt security, the investor is to treat the security as if it had been purchased on the measurement date on which the impairment was recognized. If the security had been originally purchased at a premium, the impairment charge will either reduce or eliminate the premium or if the impairment is large enough cause the reporting entity to record a discount. If the security had been purchased at its face amount or a discount, the impairment charge will result in recording or increasing the discount.

After recording the adjustment for the impairment, the adjusted premium or discount is to be amortized prospectively over the remaining term of the debt security based on the amount and timing of future estimated cash flows.

Cost-Method Investments

By their nature, cost-method investments normally do not have readily determinable fair values. Consequently, ASC 320-10-35-25 provides a different model for determining whether a cost-method investment is other-than-temporarily impaired. The determination is made as follows:

- If the investor has estimated the investment's fair value (e.g., for the purposes of the disclosures of the fair value of financial assets required by ASC 825-10-50), that estimate is to be used to determine if the investment is impaired for those reporting periods in which the investor estimates fair value. If the fair value is less than cost, the investor would proceed to Step 2 of the impairment protocol described previously.

- For reporting periods in which the investor has not estimated the fair value of the investment, the investor is required to evaluate whether an event or change in circumstances has occurred during the period that may have a significant adverse effect on the fair value of the investment. Such events and circumstances are referred to as impairment indicators and include, but are not limited to:

- A significant deterioration in the earnings performance, credit rating, asset quality, or business prospects of the investee

- A significant adverse change in the economic, regulatory, or technological environment of the investee

- A significant adverse change in the general market condition of either the geographic area or the industry in which the investee operates

- A solicited or unsolicited bona fide offer to purchase, an offer by the investee to sell, or a completed auction process for the same or similar security for an amount less than the cost of the investment

- Existing factors that raise significant concerns regarding the ability of the investee to continue as a going concern, such as negative cash flows from operations, working capital deficiencies, or noncompliance with debt covenants or statutory capital requirements.

If an impairment indicator is present, the investor is required to estimate the investment's fair value and compare the estimated fair value to the cost of the investment. If the fair value is less than cost, the investor is to proceed to Step 2, as previously described, to evaluate whether the impairment is other than temporary.

Additionally, if a cost-method investment had previously been evaluated under Step 2 as to whether impairment was other than temporary, and the investor had previously concluded that the investment was not other-than-temporarily impaired, the investor is required to continue to make this evaluation by estimating the investment's fair value in each subsequent interim and annual reporting period until either (1) the investment's fair value recovers to an amount that equals or exceeds the cost of the investment, or (2) the investor recognizes an other-than-temporary impairment loss.

Option Contracts

Call and put options can serve as valuable hedging instruments or as highly leveraged speculative investments. Options give one party, the holder, the right but not the obligation to either buy (call) or sell (put) a fixed quantity of an instrument at a defined price. The counterparty, known as the writer of the option, has no choice to make and must perform if called upon to do so by the holder.

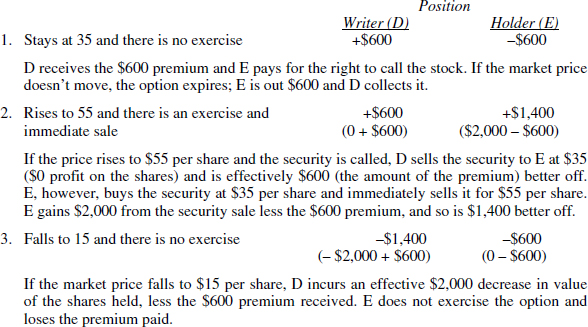

One call contract gives the holder the right to buy 100 shares of the underlying security at a specific exercise price, regardless of the market price. The seller (writer) of the call, on the other hand, must sell the security to the buyer at that specified exercise price, regardless of the market price. For example, assume a Dreamy July 35 call has a quoted market price of $6 (per share or $600 per contract). These facts indicate that a buyer that pays $600 to a seller for a call has the right to purchase 100 shares of Dreamy at any time until July (typically, the end of trading on the third Friday of the month quoted) for $35 per share. The buyer can exercise this right at any time until it expires. The writer of the call must stand ready to deliver 100 shares to the buyer for $35 per share until expiration. Typically, the holder expects the market price to rise and the writer expects the market price to stay the same or to fall.

A put is the opposite of a call. A put gives the holder of the put the right to sell the underlying security at the exercise price regardless of the market price. It gives the writer of the put the obligation to buy at the exercise price, if so demanded by the holder. Typically, the holder of a put option expects the market price to fall, and the writer expects the market price to stay the same or to rise.

There are many compound options used by traders and investors, all of which consist of combinations of one or more calls and puts, in some cases having differing expiration dates. Strips, straps, straddles, and spreads are combinations and/or variations of the basic call and the basic put. These and other compound instruments should be analyzed in terms of their constituent elements, and accounted for accordingly.

Writer D owns 100 shares of Dreamy at a cost of $75 per share and sells 1 Dreamy July 35 call to Holder E at $6. The following positions result if the market price:

The issue in accounting for options is whether cost or fair value—or some combination—is to be used in accounting for the option itself and for the associated underlying security. For instance, assume M buys 100 shares of XYZ at $15 per share and the security price immediately moves to $25 per share. At this point, M buys a November 25 put contract at $100 for the contract. M has effectively hedged and guaranteed a minimum profit of $900 [(100 shares × $10) − (100 shares × $1)] regardless of market price movement, since XYZ can be sold for $25 per share until the third Friday in November. If the price continues upward, the put will expire unexercised and M will continue to benefit point for point. If the price stays the same, M locks in a profit of $900. If the price falls, M has locked in a profit of $900. The question is whether, under this fact pattern, both the option and the security can be accounted for at historical cost or at fair value or at some combination of the two.

Change in Fair Value Measurements After Year-end, Disclosures, and Elections

Changes in fair value after the date of the statement of financial position.

Under GAAP, events occurring after the date of the statement of financial position are generally not recognized as adjustments to the financial statements. However, disclosure may be necessary if, absent that information, the user of the financial statements would be misled. While not addressed explicitly by ASC 320, presumably material changes in fair value occurring subsequent to the date of the statement of financial position but prior to issuance of the financial statements should be disclosed by management.

Sometimes changes in fair value can be indicative of the underlying cause of the price fluctuations. Of most interest here would be declines in value of available-for-sale securities held at the date of the statement of financial position, which suggest that an “other-than-temporary” impairment has occurred. If the decline actually occurred after year-end as evidenced by a bankruptcy filing, then the event would be disclosed but not reflected in the year-end statement of financial position. However, in some instances, the subsequent decline would be seen as a “confirming event” which provided evidence that the classification or other treatment of an item on the date of the statement of financial position was incorrect. Thus, if a decline in the fair value of available-for-sale securities at the date of the statement of financial position had been accounted for as temporary (and hence reported in other comprehensive income) a further decline after the statement of financial position date might suggest that the decline as of the statement of financial position date had, in fact, been a permanent impairment. Note that any further value decline after year-end would not be recorded in the financial statements; the only question to be addressed is whether the decline that occurred prior to year-end should have been treated as a permanent impairment rather than as a temporary market fluctuation.

If it is clear that the impairment at year-end had, in fact, been other than temporary in nature, then the financial statements are to be adjusted to reflect this loss in net income. Absent sufficient basis to reach this conclusion, the appropriate course of action is to not adjust the statements, but merely to disclose the (material) change in fair value that occurred subsequent to year-end including, if appropriate, a statement to the effect that the later decline was deemed to be an OTTI and will be reflected in the net income of the next year's financial statements. It should also be made clear that the decline occurring prior to year-end was not considered to be an other-than-temporary impairment at that time.

The FASB staff noted that when an entity has decided to sell a security classified as available-for-sale having a fair value less than cost at year-end, and it does not reasonably expect a recovery in value before the sale is to occur, then a write-down for an other-than-temporary decline is prescribed. This would most obviously be necessary if the actual sales transaction, anticipated at year-end, occurs prior to the issuance of the financial statements.

Mutual funds invested in US government contracts. ASC 320-10-50 holds that investments in open-end mutual funds that invest in US government securities are to be reported at fair value per ASC 320. Investments in mutual funds that invest solely in US government debt securities are deemed to be equity investments (since it is the shares of the fund, and not the ultimate debt securities, that are owned), and therefore cannot be classified as held-to-maturity investments.

Forward contracts and options. ASC 815-10-35 addresses the accounting for certain forward contracts and purchased options to acquire securities covered by ASC 320. It applies only when the terms require physical settlement. It stipulates that forward contracts and purchased options (which are not classified as derivatives, having no intrinsic value at acquisition) are to be designated and accounted for as prescribed by ASC 320. These forwards and options would not be eligible for designation as hedging instruments.

Structured Notes. ASC 320-10-35 deals with the complex area of “structured notes,” in particular with the matters of the recognition of interest income and of the statement of financial position classification of such instruments. According to this consensus, when recognizing interest income on structured note securities in an available-for-sale or held-to-maturity portfolio, the retrospective interest method is to be used if three conditions are satisfied. These conditions are:

- Either the original investment amount or the maturity amount of the contractual principal is at risk

- Return of investment on note is subject to volatility arising from either:

- No stated rate or stated rate that is not a constant percentage or in same direction as changes in market-based interest rates or interest rate index, or

- Fixed or variable coupon rate lower than that for interest for traditional notes with similar maturity, and a portion of potential yield based on occurrence of future circumstances or events

- Contractual maturity of bond is based on a specific index or on occurrence of specific events or situations outside the control of contractual parties.

This does not apply to structured note securities that, by their nature, subject the holder to reasonably possible loss of all, or substantially all, of the original invested amount (other than due to debtor failure to pay amount owed). In those instances, the investment is to be carried at fair value with changes in value recognized in current earnings.

The retrospective interest method requires that periodic income be measured by reference to the change in amortized cost from period beginning to period end, plus any cash received during the period. Amortized cost is determined with reference to the conditions applicable as of the respective date of the statement of financial position. Other-than-temporary declines in fair value would also have to be recognized in earnings, consistent with ASC 320 requirements for held-to-maturity investments.

1 A transaction gain or loss on a foreign-currency-denominated held-to-maturity security is accounted for according to ASC 830-20.

2 “If an available for sale security is designated as being held in a fair value hedge, all or a portion of the unrealized gain or loss should be recognized in earnings.” (ASC 815-25-35-1)

3 ASC 815-25-35 indicates that, with respect to a qualifying fair value hedge, the change in fair value of the hedged item that is attributable to the hedged risk is record as an adjustment to the carrying amount of the hedged item and is recognized currently in net income.