23 ASC 340 OTHER ASSETS AND DEFERRED COSTS

Preproduction Costs Related to Long-term Supply Arrangements

Insurance Contracts that do not Translate Insurance Risk

PERSPECTIVE AND ISSUES

Subtopics

ASC 340, Other Assets and Deferred Costs, contains three subtopics:

- ASC 340-10, Overall, which provides guidance on certain deferred costs and prepaid expenses.

- ASC 340-20, Capitalized Advertising Costs, which provides guidance on the initial measurement, amortization, realizability, and disclosure of direct response advertising costs reported as assets.

- ASC 340-30, Insurance Contracts that Do Not Transfer Insurance Risk, which provides guidance on how to apply the deposit method of accounting when it is required for insurance and reinsurance contracts that do not transfer risk.

The guidance in ASC 340-10 is limited to a discussion of the nature of prepaid expenses and guidance for preproduction costs related to long-term supply arrangements. The specific guidance for many other deferred costs is included in various other areas of the Codification.

Scope and Scope Exceptions

Per ASC 340-20-15-4:

“Direct-response advertising activities exclude advertising that, though related to the direct-response advertising, is directed to an audience that could not be shown to have responded specifically to the direct-response advertising. For example, a television commercial announcing that order forms (that are direct-response advertising) soon will be distributed directly to some people in the viewing area would not be a direct-response advertising activity because the television commercial is directed to a broad audience, not all of which could be shown to have responded specifically to the direct-response advertising.”

ASC 340-30-15 provides guidance on which transactions are covered and which are not covered by subtopic ASC 340-30. The guidance in the Subtopic includes the following transactions

- Short-duration insurance and reinsurance contracts that do not transfer insurance risk as described in paragraph 720-20-25-1 and, for reinsurance contracts, as described in Section 944-20-15

- Multiple-year insurance and reinsurance contracts that do not transfer insurance risk or for which insurance risk transfer is not determinable.

(ASC 340-30-15-3)

The guidance in ASC 340-30 does not apply to the following transactions and activities:

- Long-duration life and health insurance contracts that do not indemnify against mortality or morbidity risk shall be accounted for as investment contracts under Topic 944. Therefore, such contracts are not covered by this Subtopic.

(ASC 340-30-15-4)

Overview

Prepaid expenses are amounts paid to secure the use of assets or the receipt of services at a future date or continuously over one or more future periods. Prepaid expenses will not be converted to cash, but they are classified as current assets because, if they are not prepaid, they would have required the use of current assets during the coming year (or operating cycle, if longer).

Manufacturers often incur preproduction costs related to products and services they will supply to their customers under long-term arrangements. The supplier may be contractually guaranteed reimbursement of design and development costs, implicitly guaranteed reimbursement of design and development costs through the pricing of the product or other means, or not guaranteed reimbursement of the design and development costs incurred under the long-term supply arrangement.

DEFINITION OF TERMS

Source: ASC 340-30-20

Assuming Entity. The party that receives a reinsurance premium in a reinsurance transaction. The assuming entity (or reinsurer) accepts an obligation to reimburse a ceding entity under the terms of the reinsurance contract.

Ceding Entity. The party that pays a reinsurance premium in a reinsurance transaction. The ceding entity receives the right to reimbursement from the assuming entity under the terms of the reinsurance contract.

Experience Adjustment. A provision in an insurance or reinsurance contract that modifies the premium, coverage, commission, or a combination of the three, in whole or in part, based on experience under the contract.

Insurance Risk. The risk arising from uncertainties about both underwriting risk and timing risk. Actual or imputed investment returns are not an element of insurance risk. Insurance risk is fortuitous; the possibility of adverse events occurring is outside the control of the insured.

Timing Risk. The risk arising from uncertainties about the timing of the receipt and payments of the net cash flows from premiums, commissions, claims, and claim settlement expenses paid under a contract.

Underwriting Risk. The risk arising from uncertainties about the ultimate amount of net cash flows from premiums, commissions, claims, and claim settlement expenses paid under a contract.

CONCEPTS, RULES, AND EXAMPLES

Prepaid Expenses

Types of prepaid expenses.

Prepaid expenses are amounts paid to secure the use of assets or the receipt of services at a future date or continuously over one or more future periods. Prepaid expenses will not be converted to cash, but they are classified as current assets because, if they are not prepaid, they would have required the use of current assets during the coming year (or operating cycle, if longer). Examples of items that are often prepaid include dues, subscriptions, maintenance agreements, memberships, licenses, rents, and insurance.

The examples of prepaid expenses cited in the previous paragraph are unambiguous. This is, however, not always the case. In negotiating union labor contracts, the parties may agree that the union employees will be entitled to receive a lump-sum cash payment or series of payments in exchange for agreeing to little or no increase in the employees' base wage rate. These lump-sum arrangements ordinarily do not require the employee to refund any portion of the lump sum to the employer in the event that the employee terminates employment during the term of the labor agreement. Further, it is assumed by the parties that, upon termination of a union member, the employer will replace that individual with another union member at the same base wage rate to whom no lump sum would be due. Management believes that the lump-sum payment arrangement will reduce or eliminate raises during the contract term and that these lump-sum payments will benefit future periods. To record these lump sums as prepaid expenses, ASC 710-10-25 specifies that, based on a careful review of the facts and circumstances around the contract and negotiations, the payments must clearly benefit a future period in the form of a lower base wage rate than would otherwise have been in effect. Further, the amortization period is not permitted to extend beyond the term of the union contract. The presumption of replacing terminating union members with other union members at the same wage rate is essential to this conclusion and, thus, this accounting treatment is only applicable to union contracts and is not permitted to be applied by analogy to account for individual employment contracts or other compensation arrangements. The SEC observer noted that accounting for this transaction as a prepaid expense is only appropriate when there is no evidence of any kind that the lump-sum payment or payments are related to services rendered in the past.

Amortization.

Prepaid expenses are amortized to expense on a ratable basis over the period during which the benefits or services are received. For example, if rent is prepaid for the quarter at the beginning of the quarter, two months of the rent will be included in the prepaid rent account. At the beginning of the second month, the equivalent of one month's rent (half the account balance) would be charged to rent expense. At the beginning of the third month, the remaining prepayment would be charged to rent expense.

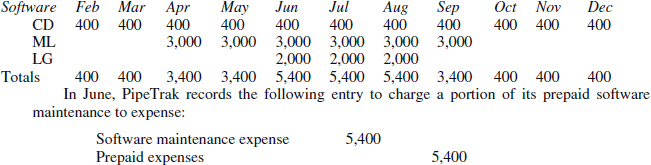

The PipeTrak Company starts using geographical information systems (GIS) software to track the locations of the country's pipeline infrastructure under a contract for the Department of Homeland Security. It pays maintenance fees on three types of GIS software, for which the following maintenance periods are covered:

It initially records these fee payments as prepaid expenses. PipeTrak's controller then uses the following amortization table to determine the amount of prepaid expenses to charge to expense each month:

Preproduction Costs Related to Long-Term Supply Arrangements

Manufacturers often incur costs referred to as preproduction costs, related to products that they will provide to their customers under long-term supply arrangements. ASC 340-10-25 states the following with respect to these costs:

- Costs of design and development of products to be sold under long-term supply arrangements are expensed as incurred.

- Costs of design and development of molds, dies, and other tools that the supplier will own and that will be used in producing the products under the long-term supply arrangement are capitalized as part of the molds, dies, and other tools (subject to an ASC 360 recoverability assessment when one or more impairment indicators is present). There is an exception, however, for molds, dies, and other tools involving new technology, which are expensed as incurred as research and development costs under ASC 730.

- If the molds, dies, and other tools described in 2 above are not to be owned by the supplier, then their costs are expensed as incurred unless the supply arrangement provides the supplier the noncancelable right (as long as the supplier is performing under the terms of the supply arrangement) to use the molds, dies, and other tools during the term of the supply arrangement.

(ASC 340-10-25-1)

- If there is a legally enforceable contractual guarantee for reimbursement of design and development costs that would otherwise be expensed under these rules, the costs are recognized as an asset as incurred. Such a guarantee must contain reimbursement provisions that are objectively measurable and verifiable. The ASC provides examples illustrating this provision. (ASC 340-20-25-3)

Under these rules, preparers are encouraged (and SEC registrants are required) to disclose the following information (ASC 340-10-S99-3):

- The accounting policy for preproduction design and development costs.

- The aggregate amounts of:

- Assets recognized pursuant to agreements providing for contractual reimbursement of preproduction design and development costs.

- Assets recognized for molds, dies, and other tools that the supplier owns.

- Assets recognized for molds, dies, and other tools that the supplier does not own.

It is important to note that the above provisions do not apply to assets acquired in a business combination that are used in research and development activities. Instead, such assets are accounted for in accordance with ASC 805, which permits recognition of in-process research and development assets.

Capitalized Advertising Costs

The costs of advertising are expensed either as costs are incurred or the first time the advertising takes place (e.g., when the television advertisement is aired or printed copy is published), if later (720-35-25). However, if both of the following conditions are met, those costs can be capitalized:

- The primary purpose is to elicit sales to customers who could be shown to have responded specifically to the advertising, and

- The advertising results in probable future economic benefits.

The future benefits to be received are the future revenues arising as a direct result of the advertising. The company is required to provide entity-specific persuasive evidence that there is a linkage between the direct-response advertising and these future benefits. These costs are then amortized over the period in which the future benefits are expected to be received.

Advertising expenditures are sometimes made subsequent to the recognition of revenue (such as in “cooperative advertising” arrangements with customers). In order to achieve proper matching, these costs are to be estimated, accrued, and charged to expense when the related revenues are recognized. (ASC 340-20-25-2)

Insurance contracts that do not translate insurance risk

Deposit accounting.

Insurance risk is comprised of timing risk and underwriting risk, and one or both of these may not be transferred to the insurer (assuming entity in the case of reinsurance) under certain circumstances. For example, many workers' compensation policies provide for experience adjustments which have the effect of keeping the underwriting risk with the insured, rather than transferring it to the insurer; in such instances, deposit accounting would be prescribed.

Under the provisions of ASC 340-30, for contracts that transfer only significant timing risk, or that transfer neither significant timing nor underwriting risk, a deposit asset (from the insured's or ceding entity's perspective, respectively, for insurance and reinsurance arrangements) or liability (from the insurer's or assuming entity's perspective, respectively, for insurance and reinsurance arrangements) should be recognized at inception. The deposit asset or liability should be remeasured at subsequent financial reporting dates by calculating the effective yield on the deposit to reflect actual payments to date and expected future payments. Yield is to be determined as set forth in ASC 310-20, using the estimated amounts and timings of cash flows. The deposit is to be adjusted to that which would have existed at the statement of financial position date had the new effective yield been applied since inception of the contract; thus, expense or income for a period will be determined by first calculating the necessary amount in the related statement of financial position account.

For contracts that transfer only significant underwriting risk, a deposit asset or liability is also established at inception. However, subsequent remeasurement of the deposit does not occur until such time as a loss is incurred that will be reimbursed under the contract; instead, the deposit is reported at its amortized amount. Once the loss occurs, the deposit should be remeasured by the present value of expected future cash flows arising from the contract, plus the remaining unexpired portion of the coverage. Changes in the deposit arising from the present value measure are to be reported in the insured's income statement as an offset against the loss to be reimbursed; in the insurer's income statement, the adjustment should be reported as an incurred loss. The reduction due to amortization of the deposit is reported as an adjustment to incurred losses by the insurer. The discount rate used to compute the present value is to be the rate on government obligations with similar cash flow characteristics, adjusted for differences in default risk, which is based on the insurer's credit rating. Rates are determined at the loss date(s) and not revised later, absent further losses.

For insurance contracts with indeterminate risk, the procedures set forth in ASC 944-605 (the open-year method) should be applied. (ASC 340-25-05-8) This involves the segregation, in the statement of financial position, of amounts that have not been adjusted due to lack of sufficient loss or other data. When sufficient information becomes available, the deposit asset or liability is adjusted, which is to be reported as an accounting change per ASC 250.