50 ASC 825 FINANCIAL INSTRUMENTS

ASC 825-10-25, Financial Instruments: The Fair Value Option

Financial statement presentation and disclosure

Statement of financial position

Example of disclosure ASC 820 and ASC 825-10-25 combined with ASC 825-10-50 disclosures

PERSPECTIVE AND ISSUES

Subtopics

ASC 825, Financial Instruments, contains two Subtopics:

- ASC 825-10, Overall, which has two Subsections:

- General, which provides guidance on credit losses on financial instruments with off-balance-sheet credit risk and some disclosures about financial instruments

- Fair Value Option, which provides guidance on the circumstances under which entities may choose the fair value option and the related presentation and disclosure requirements

- ASC 825-20, Registration Payment Arrangements.

Scope and Scope Exceptions

The following items are eligible for the fair value option (also see the chapter on ASC 820 – the summary table in the section of the entitled “The Mixed Attribute Model”):

- All recognized financial assets and financial liabilities except

- Investments in subsidiaries required to be consolidated by the reporting entity

- Interests in variable interest entities required to be consolidated by the reporting entity1

- Employers' and plans' obligations (unfunded or underfunded liabilities) or assets (representing net overfunded positions) for

- (1) Pension benefits

- (2) Other postretirement benefits (including health care and life insurance benefits)

- (3) Postemployment benefits

- (4) Other deferred compensation, termination, and share-based payment arrangements such as employee stock option plans; employee stock purchase plans; compensated absences; and exit and disposal activities

- Financial assets and financial liabilities under leases (this exception does not, however, apply to a guarantee of a third-party lease obligation or a contingent obligation associated with cancellation of a lease)

- Deposit liabilities, withdrawable on demand, of banks; saving and loan associations; credit unions; and other similar depository institutions

- Financial instruments that are, in whole or in part, classified by the issuer as a component of stockholders' equity (including “temporary equity,” also sometimes referred to as “mezzanine”) such as a convertible debt security with a noncontingent beneficial conversion feature.

(ASC 825-10-15-5)

- Firm commitments that would otherwise not be recognized at inception and that involve only financial instruments. An example is a forward purchase contract for a loan that is not readily convertible to cash. The commitment involves only financial instruments (the loan and cash) and would not be recognized at inception since it does not qualify as a derivative.

- A written loan commitment

- Rights and obligations under insurance contracts or warranties that are not financial instruments2 but whose terms permit the insurer (warrantor) to settle claims by paying a third party to provide goods and services to the counterparty (insured party or warranty claimant)

- A host financial instrument resulting from bifurcating an embedded nonfinancial derivative instrument from a nonfinancial hybrid instrument under ASC 815-15-25. An example would be an instrument in which the value of the bifurcated embedded derivative is payable in cash, services, or merchandise but the host debt contract is only payable in cash.

(ASC 825-10-15-4)

Overview

ASC 825-10-25, The Fair Value Option, encourages reporting entities to elect to use fair value to measure eligible assets and liabilities in their financial statements. The objective is to improve financial reporting by mitigating the volatility in reported earnings that is caused by measuring related assets and liabilities differently. Electing entities obtain relief from the onerous and complex documentation requirements that apply to certain hedging transactions under ASC 815. ASC 825-10-25 applies to businesses and not-for-profit organizations and provides management of these entities substantial discretion in electing to measure eligible assets and liabilities at fair value.

Management is given an extraordinary amount of discretion in selecting the assets and/or liabilities for which it chooses to make this election, the fair value option. In general, the election is made on an individual contract or item-by-item basis.

Technical Alert

ASU 2013-03, In February 2013, the FASB issued ASU 2013-03, Clarifying the Scope and Applicability of a Particular Disclosure to Nonpublic Entities. In its meetings related to ASU 2011-04, the Board had decided that nonpublic entities would not be required to disclose “the level in which a fair value measurement would be categorized within the fair value hierarchy for assets and liabilities not recognized at fair value but for which disclosure of fair value is required” After issuance of ASU 2011-04, some constituents noticed an inconsistency between what the Board intended and the actual changes to the codification. With ASU 2013-03, the board clarified that it did exempt nonpublic entities of any size from that disclosure in annual and interim financial statements.

DEFINITIONS OF TERMS

Conduit Debt Securities. Certain limited-obligation revenue bonds, certificates of participation, or similar debt instruments issued by a state or local governmental entity for the express purpose of providing financing for a specific third party (the conduit bond obligor) that is not a part of the state or local government's financial reporting entity. Although conduit debt securities bear the name of the governmental entity that issues them, the governmental entity often has no obligation for such debt beyond the resources provided by a lease or loan agreement with the third party on whose behalf the securities are issued. Further, the conduit bond obligor is responsible for any future financial reporting requirements.

Fair Value. The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Financial Asset. Cash, evidence of an ownership interest in an entity, or a contract that conveys to one entity a right to do either of the following:

- Receive cash or another financial instrument from a second entity

- Exchange other financial instruments on potentially favorable terms with the second entity.

Financial Instrument. Cash, evidence of an ownership interest in an entity, or a contract that both:

- Imposes on one entity a contractual obligation either:

- To deliver cash or another financial instrument to a second entity

- To exchange other financial instruments on potentially unfavorable terms with the second entity.

- Conveys to that second entity a contractual right either:

- To receive cash or another financial instrument from the first entity

- To exchange other financial instruments on potentially favorable terms with the first entity.

The use of the term financial instrument in this definition is recursive (because the term financial instrument is included in it), though it is not circular. The definition requires a chain of contractual obligations that ends with the delivery of cash or an ownership interest in an entity. Any number of obligations to deliver financial instruments can be links in a chain that qualifies a particular contract as a financial instrument.

Contractual rights and contractual obligations encompass both those that are conditioned on the occurrence of a specified event and those that are not. All contractual rights (contractual obligations) that are financial instruments meet the definition of asset (liability) set forth in FASB Concepts Statement No. 6, Elements of Financial Statements, although some may not be recognized as assets (liabilities) in financial statements—that is, they may be off-balance-sheet—because they fail to meet some other criterion for recognition.

For some financial instruments, the right is held by or the obligation is due from (or the obligation is owed to or by) a group of entities rather than a single entity.

Financial Liability. A contract that imposes on one entity an obligation to do either of the following:

- Deliver cash or another financial instrument to a second entity

- Exchange other financial instruments on potentially unfavorable terms with the second entity.

Firm Commitment. An agreement with an unrelated party, binding on both parties and usually legally enforceable, with the following characteristics:

- The agreement specifies all significant terms, including the quantity to be exchanged, the fixed price, and the timing of the transaction. The fixed price may be expressed as a specified amount of an entity's functional currency or of a foreign currency. It may also be expressed as a specified interest rate or specified effective yield. The binding provisions of an agreement are regarded to include those legal rights and obligations codified in the laws to which such an agreement is subject. A price that varies with the market price of the item that is the subject of the firm commitment cannot qualify as a fixed price. For example, a price that is specified in terms of ounces of gold would not be a fixed price if the market price of the item to be purchased or sold under the firm commitment varied with the price of gold.

- The agreement includes a disincentive for nonperformance that is sufficiently large to make performance probable. In the legal jurisdiction that governs the agreement, the existence of statutory rights to pursue remedies for default equivalent to the damages suffered by the nondefaulting party, in and of itself, represents a sufficiently large disincentive for nonperformance to make performance probable for purposes of applying the definition of a firm commitment.

Liability Issued with an Inseparable Third-Party Credit Enhancement. A liability that is issued with a credit enhancement obtained from a third party, such as debt that is issued with a financial guarantee from a third party that guarantees the issuer's payment obligation.

Nonpublic Entity. Any entity that does not meet any of the following conditions:

- Its debt or equity securities trade in a public market either on a stock exchange (domestic or foreign) or in the over-the-counter market, including securities quoted only locally or regionally.

- It is a conduit bond obligor for conduit debt securities that are traded in a public market (a domestic or foreign stock exchange or an over-the-counter market, including local or regional markets).

- It files with a regulatory agency in preparation for the sale of any class of debt or equity securities in a public market.

- It is controlled by an entity covered by the preceding criteria.

Publicly Traded Company. See definition in the chapter on ASC 270.

CONCEPTS, RULES, AND EXAMPLES

ASC 825-10-25, Financial Instruments: The Fair Value Option

Flexibility of application.

ASC 825-10-25 provides management with substantial flexibility in electing the fair value option (FVO). Once elected, however, the election is irrevocable unless, as discussed later in this section, a new election date occurs. The election can be made for a single eligible item without electing it for other identical items subject to the following limitations:

- If the FVO is elected with respect to an investment otherwise required to be accounted for under the equity method of accounting, the FVO election is to be applied to all of the investor's financial interests in the same entity (equity and debt, including guarantees) that are eligible items.

- If a single contract with a borrower (such as a line of credit or construction loan) involves multiple advances to that borrower and those advances lose their individual identity and are aggregated with the overall loan balance, the FVO is only permitted to be elected to apply to the larger overall loan balance and not individually with respect to each individual advance.

- If the FVO is applied to an eligible insurance or reinsurance contract, it is also required to be applied to all claims and obligations under the contract.

- If the FVO is elected for an eligible insurance contract (base contract) for which integrated or nonintegrated contract features or coverages (some of which are referred to as “riders”) are issued either concurrently or subsequently, the FVO is required to be applied to those features and coverages. The FVO is not permitted to be elected for only the nonintegrated contract features and coverages, even though they are accounted for separately under ASC 944-30.3

Other than as provided in 1 and 2 above, management is not required to apply the FVO to all instruments issued or acquired in a single transaction. The lowest level of election, however, is at the single legal contract level. A financial instrument that is, in legal form, a single contract is not permitted to be separated into component parts for the purpose of electing the FVO. For example, an individual bond is the minimum denomination of that type of debt security.

An investor in an equity security of a particular issuer may elect the FVO for its entire investment in that equity security including any fractional shares issued by the investee in connection, for example, with a dividend reinvestment plan.

Management of an acquirer, parent company, or primary beneficiary4 decides whether to elect the FVO with respect to the eligible items of an acquiree, subsidiary, or consolidated variable interest entity. That decision, however, only applies in the consolidated financial statements. FVO choices made by management of an acquiree, subsidiary, or variable interest entity continue to apply in their separate financial statements should they choose to issue them.

Timing of the election.

Management may elect the FVO for an eligible item in one of two ways.

- Based on an established policy for specified types of eligible items that it follows consistently, or

- On the date of occurrence of one of the following events:

- The entity initially recognizes the item.

- The entity enters into an eligible firm commitment.

- Financial assets previously required to be reported at fair value with unrealized gains and losses included in income due to the application of specialized accounting principles cease to qualify for that accounting treatment (e.g., a subsidiary subject to ASC 946 transfers a security to another subsidiary of the same parent that is not subject to the ASC).

- The accounting treatment for an investment in another entity changes because

- (1) The investment becomes subject to the equity method of accounting (and, for example, had previously been accounted for under ASC 320 or under the FVO)

- (2) The investor ceases to consolidate a subsidiary or variable interest entity but retains an interest in the entity

- An event requires an eligible item to be remeasured at fair value at the time that the event occurs but does not require fair value measurements to be made at each subsequent reporting date. Specifically excluded from being considered an eligible event are

- (1) Recognition of impairment under lower-of-cost-or-market accounting, or

- (2) Other-than-temporary impairment.

(ASC 825-10-25-4)

Among the events that require initial fair value measurement or subsequent fair value remeasurements of this kind are

- (1) Business combinations,

- (2) Consolidation or deconsolidation of a subsidiary or variable interest entity, and

- (3) Significant modifications of debt, as defined in ASC 470-50, Debt—Modifications and Extinguishments.

(ASC 825-10-25-5)

Financial statement presentation and disclosure

Statement of financial position.

ASC 825-10-25 requires the reporting entity to report assets and liabilities for which the FVO was elected in a manner that separates those amounts from carrying amounts of similar assets and liabilities measured using another measurement method. Two alternatives are provided.

- Present the aggregate fair value and non-fair value amounts on the same line of the statement of financial position and parenthetically provide the amount measured at fair value that is included in the aggregate amount.

- Present two separate line items to display the fair value and non-fair value carrying amounts.

The manner in which the first alternative is illustrated in ASC 825-10-25 could potentially confuse or mislead readers.

| Private equity investments ($75 at fair value) | $125 |

This caption could easily be misunderstood by the reader to mean that the reporting entity holds private equity investments with an aggregate carrying value of $125 whose fair value has declined to $75 thus implying a $50 unrealized loss. In fact, this caption is intended to convey the fact that the reporting entity holds private equity investments with an aggregate carrying value of $125 and that the $125 is comprised of $75 valued at fair value in accordance with an election of the FVO and $50 using another measurement attribute such as the cost method or equity method.

If using parenthetical disclosure, it would be less misleading if the amount were presented as follows:

![]()

This can get cumbersome and is still confusing. It becomes even more unwieldy when considering the fact that reporting entities customarily present two or three years' comparative statements of financial position and that not-for-profit organizations often use tabular formats for their statements of financial position that present separate columns for unrestricted net assets, temporarily restricted net assets, and permanently restricted net assets.

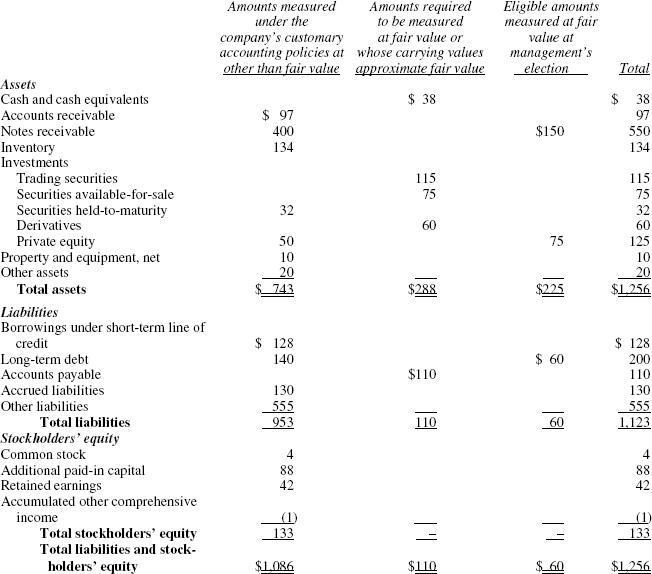

Another source of confusion is the fact that existing GAAP requires certain items (such as derivatives, trading securities, and available-for-sale securities) to be stated at fair value without consideration of the FVO. Therefore, it is conceivable that a single statement of financial position will contain financial instruments that are stated at fair value due to a requirement in GAAP, financial instruments that are stated at fair value due to management's election of the FVO, and financial instruments that are stated using some other attribute such as cost method or equity method, or, as is permitted for investments in certain debt securities, using amortized cost. When this is the case, the reporting entity may wish to use a format such as the one shown in the sample “Consolidated Statement of Financial Position” for the Young Aviation Chopper and Helicopter Works, Inc.

Many variations can be derived from this method of presentation. For example, subtotals are only necessary to be presented for the total column since the notes to the financial statements provide fair value totals by major class. The financial statement preparer may wish to augment this presentation by including a column that subtotals all amounts stated at fair value irrespective of whether they are subject to the FVO election.

Separate sections of assets and liabilities could contain separate line items enumerating the eligible items within each for which the FVO was elected by management.

Young Aviation Chopper and Helicopter Works, Inc.

Consolidated Statement of Financial Position

December 31, 2013

(Unclassified for Illustrative Purposes)

Statement of cash flows.

ASC 825-10-25 requires cash receipts and cash payments related to items measured at fair value to be classified in the statement of cash flows according to their nature and purpose. Inexplicably, however, ASC 825-10-25 leaves the provision of ASC 230 unchanged that requires returns on investments (interest and dividends) to be accounted for as operating activities.

Disclosure objectives.

Consistent with the approach in ASC 820, ASC 825-10-25 provides financial statement preparers with the principal objectives associated with fair value option disclosures and then sets forth in detail the disclosures FASB deems necessary to meet the objective. The principal objectives are to facilitate comparisons (1) between entities that choose different measurement attributes for similar assets and liabilities, and (2) between assets and liabilities in the financial statements of an entity that elects to use different measurement attributes for similar assets and liabilities. FASB indicates that it expects the disclosures to result in

- Information sufficient to enable financial statement users to understand

- The reasons why management elected or partially elected the FVO

- How changes in fair values affected net income for the period

- The differences between fair values and contractual cash flows for certain items

- The information that would have been required to be disclosed about certain items (e.g., equity-method investments, nonperforming loans) absent the FVO election.

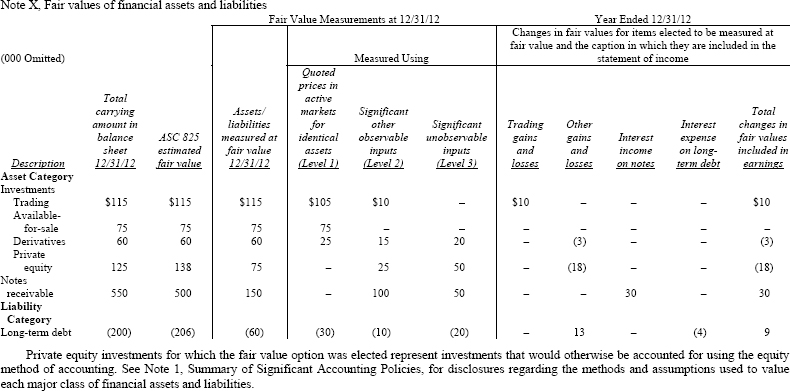

Although not required by ASC 825-10-25, FASB encourages management to present the disclosures it requires in combination with related fair value disclosures required to be disclosed by parts of the codification (such as ASC 825-10-50 and ASC 820).

The following example does not purport to illustrate all of the disclosure requirements specified within GAAP. Instead, it is presented to illustrate how the financial statement preparer might organize the required tabular disclosures by integrating the ASC 825-10-50 disclosures regarding the fair value of financial instruments with the ASC 820 and ASC 825-10-25 disclosures discussed in this chapter.

Young Aviation Chopper and Helicopter Works, Inc.

Notes to Financial Statements

December 31, 2012

1 Under ASC 805, consolidated variable interest entities are referred to as subsidiaries in the same manner as consolidated voting interest entities.

2 Insurance contracts that require or permit the insurer to settle claims by providing goods or services instead of by paying cash are not, by definition, financial instruments. Similarly, warranties that require or permit the warrantor to settle claims by providing goods and services in lieu of cash do not constitute financial instruments.

3 ASC 944-30-20 defines a nonintegrated contract feature in an insurance contract as a feature in which the benefits provided are not related to or dependent on the provisions of the base contract. For the purposes of applying the FVO election, neither an integrated nor a nonintegrated contract feature or coverage qualifies as a separate instrument.

4 Under ASC 805 a primary beneficiary is referred to as a parent in the same manner as a company that consolidates a voting interest entity.