CHAPTER 47

Focus on Financial Services

Mitigating Risk with Transparency in a Regulated Environment

Governance and risk mitigation are critical factors in the project life cycle, and are known drivers of project success.1 Finding a balance between effective oversight and bureaucracy can be challenging for any project leader. But what happens when external stakeholders take a more active role in project oversight? Such is the case in heavily regulated industries. In the financial services sector, for example, regulatory requirements shift continually as a result of the aftermath of the worst market correction since the Great Depression. In order to remain compliant, firms must stay ahead of changing legislation while ensuring that projected spend is contained within paper-thin margins. As a result, project practices are adapted to better serve the unique challenge of driving change under robust governance.

This chapter focuses on how to implement three strategic practices designed to build trust and transparency in a regulated environment:

1. Develop financial modeling and forecasting core competencies in project leaders.

2. Communicate in terms of results rather than statistics in project reporting.

3. Manage significant change through structured dialogue and highly accessible reports.

MODEL FINANCIALS AT THE PROJECT TEAM LEVEL

Preparing the business case is historically a task for the executive sponsor. In many organizations, the project team is assembled only after the project is presented and funding approved. This approach is changing as thought leaders move project practices to more flexible methodologies.2 No project is launched for the sole purpose of spending time and money. Project leaders must fully understand the financial goals of the project and the economic drivers of those goals in order to effectively manage project costs and drive committed results. In order to do so, project leaders must develop financial modeling core competencies and accept responsibility for accurately forecasting the impact of activity on financial outcomes. Project leaders who communicate in terms of results are far more valuable than those who simply track due dates and spend.

One best practice approach to integrating the vision with the plan is to migrate responsibility for compiling financial data and pro-forma modeling to the project leader. This approach broadens the scope of the project leader to include preparing accurate and manageable budgets through partnership with the executive sponsor and subject-matter experts (SMEs). While the ultimate accountability for the benefit commitment remains with the executive sponsor, the project leader’s understanding of the expected outcomes helps align reality with the vision. The project leader is not expected to approve the direction or validate the input, but must thoroughly understand each item and feel free to challenge or discuss any practical concerns on the front end. Adoption of a simple but thorough pro-forma spreadsheet template is all that is needed to master the input.

CASE EXAMPLE

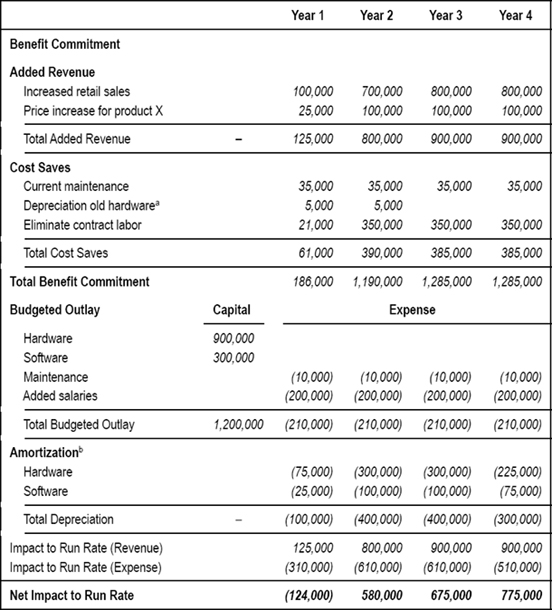

To keep up with competitors’ offerings, a bank approves an online banking project to spend $1.2 million in a capitalized expense to deliver an online loan application and a new set of report functionality for customers. The project will take one year to complete. The benefit is added revenue from sales of the new product and a small fee increase for existing customers. The new product will require newer hardware and software, and full-time employees will replace the contract labor supporting the current product. The new product will launch near the end of the first year and the budget will account for increasing sales momentum over the course of the second year for a steady state by Year 3.

The project lead meets with the executive sponsor to gather the revenue commitments and details regarding staffing changes. The SMEs in technology provide the cost estimates from the vendor along with any internal requirements. Guidelines for amortization are obtained from organizational process assets.

The model depicted in Table 47-1 is a very simplistic view of a pro-forma template for project budgeting. There are many different versions that can serve as well, and project leaders should ensure that organizational process assets are used where they exist.3

If the cost and revenue estimates require an investment to complete, an initial pro-forma can serve as a gate to cap the incremental outlay for the initiation cycle until estimates can be obtained for knowledgeable decision making. The timing can also be adjusted to accommodate the organization’s unique needs and project life cycle. As long as the project lead facilitates the information gathering through funding approval the project will realize enhanced tracking and understanding from the entire project team.

aAssumes write off of corporate asset rather than redeployment. Organizational process assets should be followed.

bAssumes 3 year straight-line depreciation schedule for simplicity of illustration only. Organizational process assets should be followed.

TABLE 47-1. EXAMPLE OF A PRO-FORMA TEMPLATE FOR PROJECT BUDGETING

When deployed as an enterprise strategy, this process also provides for the following:

• Standard formatting, which enables integration and aggregation at the portfolio level

• An enterprise view of resource requirements, vendor liability, and SME scheduling

• A stronger partnership between the project leader and the executive sponsor

• Transparency

• A view of project status for third parties without involving SMEs

COMMUNICATE RESULTS RATHER THAN STATISTICS

Building trust in a heavily regulated environment, or any environment, for that matter, is a function of transparency and predictability. When communicating the status of any project or effort, it is important to clearly relay the impact of the current activities, issues, and risks to the benefit commitment. The complexity comes into play for the project manager when there are too much data and not enough story. This is especially true when there is no agreement in place as to what constitutes success.

In the example scenario used in Table 47-1, an unexpected date slippage should be communicated as a delay in bringing the new functionality to market, with a forecast of any run rate impact. Avoid presenting progress in terms of tasks unless specifically requested to do so.

Where external stakeholders are actively involved in oversight, the project leader is expected to balance the requirements of regulatory/compliance processes while meeting the needs of the executive sponsor. Although in most cases the expected results are the same for both stakeholders, the stakeholder responsible for oversight is likely to be far more interested in mitigating risk through effective project processes, whereas the executive sponsor is interested in results. To balance the two, status reports can be presented in terms of both risk and outcome with a few simple adjustments to the work breakdown structure.

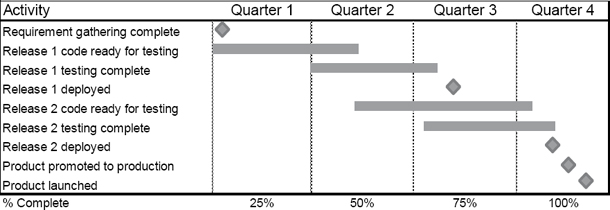

Using the case example cited earlier, Table 47-2 depicts a typical project status report of technical milestones, such as requirements definition, development, testing, and deployment.

The project leader takes the role of translator and uses the report to address schedule, cost, and risk mitigation statuses.

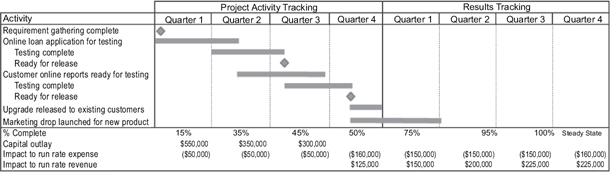

Table 47-3 illustrates that, with simple adjustments in the milestone labels to describe the deliverable rather than the task, the message becomes much clearer. Additionally, the “% Complete” data field is expanded to include results tracking through steady state. Lastly, a high-level view of the planned impact on the run rate has been added as well as the planned capital outlay.

TABLE 47-2. EXAMPLE OF A PROJECT STATUS REPORT WITH TECHNICAL MILESTONES

TABLE 47-3. EXAMPLE OF A PROJECT STATUS REPORT

Although the steps within the work effort have not changed, the understanding of the work effort is increased. Examiners and other key stakeholders can determine if cost and schedule are on track, as well as the financial implications of date slippage. Similarly, internal stakeholders can understand and plan for resource needs and manage any potential impact on the customer.

Lastly, key executives can better guide the volume of organizational change as schedules shift or budgetary issues arise if status reports are results oriented. A CEO is more likely to understand the full impact of a delayed product launch than that of a failed code test.

MANAGE ENVIRONMENTAL CHANGE WITH STRUCTURED DIALOGUE

Highly regulated industries are constantly shifting and changing to address risk. As a result, business models must be flexible to allow for quick adoption of new compulsory requirements. Some changes can directly impact the ability of the project team to deliver committed results. And some are significant enough to warrant closing the project altogether.

Changes in legislation, changes in regulatory or compliance requirements, and abrupt shifts in the capital markets are all examples of environmental change. These changes often require adjustments to the scope of enterprise-level projects to ensure compliance and mitigate risk. Project leaders must be quick and transparent regarding the cause and impact of environmental shifts to minimize disruption. Here are some examples of actions that should be taken:

• Assess the impact of proposed change including downstream effects on affiliated projects, resources, and deliverables.

• Seek input from executive sponsors and decision makers to determine the best course of action.

• Review planned adjustments with regulators and third-party stakeholders for feedback.

• Communicate final changes in the plan to all constituents.

• Follow established change request processes to update plan documents and budgets on all projects affected.

• Ensure all resource management models are adjusted where needed on all projects affected.

• Add any additional risks to the risk matrix with applicable mitigation plans.

Disruption as a result of change, whether environmental or otherwise, is only detrimental to a project when the effect is an unpredictable outcome. If the organization knows what to expect when change occurs, the risk of change is minimized. Many projects have been delayed at the last minute as a result of an uninformed and surprised key stakeholder. There are two strategies to use for managing time-sensitive project communications:

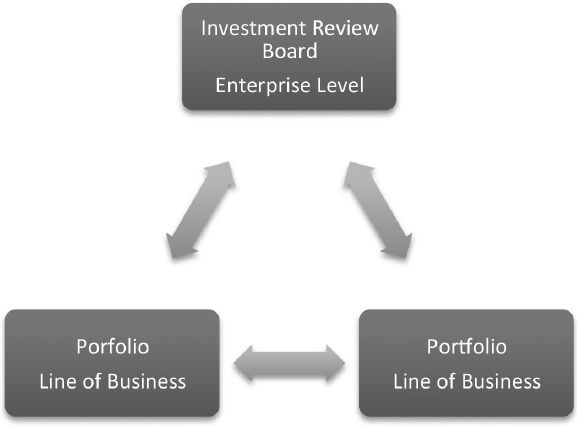

FIGURE 47-1. COMMUNICATION FLOW BETWEEN AND AMONG LINES OF BUSINESS AND EXECUTIVES

1. Implement structured dialogue through a predictable forum where updates are given and issues are escalated. The framework should include the following:

• Consistent, recurring meetings scheduled in advance at predictable dates/times

• A planned agenda with reports distributed in advance of the meetings

• Participants who are at a senior level of the organization are responsible for enterprise-level project results

• Project leaders presenting template-based reports for discussion

• Formal minutes accessible to key stakeholders (internal and external)

Figure 47-1 illustrates a structured dialogue within portfolios as well as oversight from an enterprise-level investment review for senior executives.

2. Create a single repository of highly accessible reports. Open access to certain project information creates a nimble environment able to adapt more quickly to changing needs and requirements. It also builds trust with key stakeholders charged with oversight of project processes and enables more efficient monitoring for internal and external auditors and examiners. The repository need not include sensitive data, but should allow read-only access to plans, reports, and forecasts, noting the dates of all approved changes with commentary notes.

CONCLUSION

Project leaders must understand fully the goals and expected results of any project. Adding a simple pro-forma template to project initiation documents as an exercise performed by project leaders enhances their command of the financial detail. Project leaders are better positioned to engage as partners with executive sponsors if they demonstrate financial modeling and forecasting skill sets and can put together the cost/benefit analysis.

It is important when presenting project status updates to use language that the audience can understand. Two key stakeholders in a highly regulated environment are the examiners and the executive sponsor. The project manager must balance information presented to accommodate risk mitigation through effective processes and governance as well as expected results and financial commitments. Project status reports should address potential impacts to the expected results. Simple adjustments can be made to the work breakdown structure to focus on results rather than on tasks. Adding run-rate impact to presentations helps the audience to understand the full impact of the progress made and issues at hand.

Highly regulated industries are constantly shifting and changing requirements to address risk. Shifts can be significant enough to delay a project or stop it altogether. Communication and transparency are critical to adapting to new compulsory rules or requirements. Strong partnerships with internal and external stakeholders responsible for governance are important to the success of work efforts. Two strategies for managing time sensitive communications are (1) implement structured dialogue through a predictable forum where updates are given and issues are escalated, and (2) create a single repository of highly accessible reports.

All of the strategies and practices outlined in this chapter are given within the context of highly regulated industries, with a focus on financial services. Open dialogue, inclusion, and transparency are always the best ways to mitigate risk in any project endeavor.

DISCUSSION QUESTIONS

![]() Revise the pro-forma template and remove the revenue. Discuss the implications of a project that negatively impacts run rate. When would such a project be approved?

Revise the pro-forma template and remove the revenue. Discuss the implications of a project that negatively impacts run rate. When would such a project be approved?

![]() Create a structured dialogue model for your current organization. Discuss the reasons for your choices.

Create a structured dialogue model for your current organization. Discuss the reasons for your choices.

![]() Why should everyone have access to project information? What sensitive data elements should not be accessible in the repository?

Why should everyone have access to project information? What sensitive data elements should not be accessible in the repository?

REFERENCES

1 “Federal Financial Institutions Examination Council (FFIEC) Information Technology Examination Handbook, Development and Acquisition Booklet”, last modified April 2004, http://ithandbook.ffiec.gov/it-booklets/development-and-acquisition.aspx.

2 Team Technologies, Inc. of Middleburg, VA, in cooperation with Operations Core Services, “The Logframe Handbook, A Logical Framework Approach to Project Cycle Management,” public disclosure authorized, The World Bank, 1997.

3 Project Management Institute, A Guide to the Project Management Body of Knowledge (PMBOK® Guide), 5th edition (Newtown Square, PA: PMI, 2013), p, 27.