Another trick done with mirrors

Let’s assume that the company had annual revenues of $20,000,000. And let’s also assume that it had accounts receivable of $4,000,000.

Annual revenues = $20,000,000

Accounts Receivable (A/R) = $4,000,000

We can now do a calculation similar to the one we did for inventory.

![]()

Accountants would say that the company’s accounts receivable is “turning five times.” In other words, during the year, the company must collect five times the value of the accounts receivable to equal the value of the annual revenues.

Once again, we can almost hear you saying, “So what?” And once again, we agree. So let’s try to put this in a form that makes some sense.

![]()

This number, called A/R Days, or Days Sales Outstanding (DSO) tells us that, on average, it takes the firm 73 days to collect its accounts receivable. Let’s see what this means on a daily basis.

Once again, this last calculation is a powerful one. It tells us that, on average, for every day that we could decrease A/R Days in this company, we’d have $54,795 more cash!

Although the figures we used here are fictitious, they do bear great resemblance to many of the firms we’ve known. It is not unusual for companies to have 60+ in A/R Days. This is an enormous waste of cash, and often results in the acquisition of loans to provide the company with the cash it needs to operate.

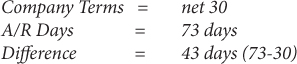

Let’s assume here that the company’s terms are net 30. It expects its customers to pay within 30 days of the invoice date. Let’s see how much cash it could generate if it collected on time.

So far, then, we’ve determined that the company’s customers are taking 43 days “too long” to make payment. The management team has perhaps been so focused on sales that it has taken its eye off the A/R ball. This is very common.

Now, we know that for every day that A/R Days could be reduced, on average, the company would gain $54,795 in cash. Let’s see what 43 days is worth.

43 days X $54,795 = $2,356,164

Almost unbelievably, we’ve found a way to generate more than two million dollars in cash for this company. All we have to do is get the customers to pay on time. Simple, huh?

Well, actually, it’s not. These customers have gotten used to paying late. They’ll be shocked, and probably offended, if we notify them suddenly that now we expect to be paid on time. We’ve helped to create their bad habit by not enforcing our own rules.

But we could, in time, reel them in to something close to our net 30, maybe even all the way. The first step is to gain a few days, and that is relatively easy.

One of the hidden dangers of letting A/R stretch out too long is that it empowers some weaker customers to neglect paying us at all. By the time we decide to chase them down for payment, they’ve become emboldened, or unable, to make the payment. Net 30 then becomes net Never.

The trick here is to remember that your transaction with your customer is an agreement. You provide the goods or services and the customer pays you. You never need to apologize for expecting to be paid on time. It’s part of the agreement.

Once again, please do these calculations for your company. Just follow the steps. And learn to collect your payments on time. You’ll greatly increase your cash flow in one of the easiest ways we know.