32 ASC 460 GUARANTEES

Example of product warranty expense

PERSPECTIVE AND ISSUES

Subtopic

ASC 460, Guarantees, consists of one subtopic:

- ASC 460-10, Overall, which provides requirements to be met by a guarantor for certain guarantees issued and outstanding.

ASC 460-10 has two Subsections:

- General, which discusses the guarantor's recognition and disclosure of a liability at the inception of a guarantee

- Product Warranties.

Additional sources of guidance are listed in the Other Sources section at the end of this chapter.

Scope and Scope Exceptions

ASC 460 applies to all entities. ASC 460 applies to guarantee contracts that contingently require the guarantor to make payments (either in cash, financial instruments, shares of its stock, other assets or in services) to the guaranteed party based on any of the following circumstances (ASC 460-10-15-4):

- Changes in a specified interest rate, security price, commodity price, foreign exchange rate, index of prices or rates, or any other variable, including the occurrence or nonoccurrence of a specified event that is related to an asset or liability of the guaranteed party. For example, the provisions apply to the following, as cited by ASC 460:

- A financial standby letter of credit

- A market value guarantee on either securities (including the common stock of the guaranteed party) or a nonfinancial asset owned by the guaranteed party

- A guarantee of the market price of the common stock of the guaranteed party

- A guarantee of the collection of the scheduled contractual cash flows from individual financial assets held by a variable interest entity (VIE)

- A guarantee granted to a business or its owners that the revenue received by the business will equal or exceed some stated amount.

(ASC 460-10-55-2, with reference to ASC 460-10-15-4(a)

One common example of this type of situation is where a hospital lures a doctor to open a practice in an underserved community with a guarantee of fee income for an initial period. ASC 460 explicitly states that these types of assurances are guarantees and must be given accounting recognition.

- Another entity's failure to perform under an obligating agreement. For example, the provisions apply to a performance standby letter of credit, which obligates the guarantor to make a payment if the specified entity fails to perform its nonfinancial obligation.

- The occurrence of a specified event or circumstance (an indemnification agreement), such as an adverse judgment in a lawsuit or the imposition of additional taxes due to either a change in the tax law or an adverse interpretation of the tax law, provided that the guarantor is an entity other than an insurance or reinsurance company.

- The occurrence of specified events under conditions whereby payments are legally available to creditors of the guaranteed party and those creditors may enforce the guaranteed party's claims against the guarantor under the agreement (an indirect guarantee of the indebtedness of others).

Per ASC 460-10-15-7, ASC 460 does not apply to

- A guarantee or an indemnification that is excluded from the scope of Topic 450, Contingencies, primarily employment-related guarantees.

- A lessee's guarantee of the residual value of leased property if the lessee accounts for the lease as a capital lease

- Contingent rents

- A guarantee contract or an indemnification agreement that is issued by either an insurance or a reinsurance company

- Vendor rebates (by the guarantor) based on either the sales revenues of or the number of units sold by the guaranteed party

- Vendor rebates (by the guarantor) based on the volume of purchases by the buyer (because the underlying relates to an asset of the seller not the buyer who receives the rebate).

- Guarantees that prevent the guarantor from recognizing either the sale of the asset underlying the guarantee or the profits from that sale

- A registration payment arrangement within the scope of ASC 825-20-15, Financial Instruments, Registration Payment Arrangements

- A guarantee or an indemnification of an entity's own future performance.

- A guarantee accounted for as a credit derivative instrument at fair value under ASC 815-10-50-4J through 4L.

(ASC 460-10-15-7)

Initial measurements. ASC 460's requirement to recognize an initial liability does not apply to the following types of guarantees (i.e., these guarantees are subject only to ASC 460's disclosure requirements):

- A guarantee that is accounted for as a derivative instrument at fair value under ASC 815.

- A contract that guarantees the functionality of nonfinancial assets that are owned by the guaranteed party (product warranties)

- Contingent consideration in a business combination or an acquisition of a business or nonprofit activity by a not-for-profit entity

- A guarantee that requires the guarantor to issue its own equity shares

- A guarantee by an original lessee that has become secondarily liable under a new lease that relieved the original lessee of the primary obligation under the original lease

- A guarantee issued between parents and their subsidiaries or between corporations under common control

- A parent's guarantee of a subsidiary's debt to a third party (irrespective of whether the parent is a corporation or an individual)

- A subsidiary's guarantee of a parent's debt to a third party or the debt of another subsidiary of the parent.

(ASC 460-10-25-1)

Product warranties. Per ASC 460-10-15-9 the guidance in the Product Warranties Subsections applies only to product warranties, which include all of the following:

- Product warranties issued by the guarantor, regardless of whether the guarantor is required to make payment in services or cash

- Separately priced extended warranty or product maintenance contracts.

- Warranty obligations that are incurred in connection with the sale of the product, that is, obligations that are not separately priced or sold but are included in the sale of the product.

Overview

There had been a longstanding requirement in GAAP for specific disclosures to be provided about direct and indirect guarantees of the indebtedness of others. ASC 460, Guarantees, explains that guarantees actually embody two separate obligations:

- The contingent obligation to make future payments under the guarantee in the event of nonperformance by the party whose obligation is guaranteed, and

- An obligation to be ready to perform, referred to as a standby obligation, during the period that the guarantee is in effect.

As a result of this bifurcation of the obligation, many guarantees are now required to be recognized as liabilities on the statement of financial position.

DEFINITIONS OF TERMS

Source: ASC 460-10-20

Acquiree. The business or businesses that the acquirer obtains control of in a business combination. This term also includes a nonprofit activity or business that a not-for-profit acquirer obtains control of in an acquisition by a not-for-profit entity.

Acquirer. The entity that obtains control of the acquiree. However, in a business combination in which a variable interest entity (VIE) is acquired, the primary beneficiary of that entity always is the acquirer.

Acquisition by a Not-for-Profit Entity. A transaction or other event in which a not-for-profit acquirer obtains control of one or more nonprofit activities or businesses and initially recognizes their assets and liabilities in the acquirer's financial statements. When applicable guidance in Topic 805 is applied by a not-for-profit entity, the term business combination has the same meaning as this term has for a not-for-profit entity. Likewise, a reference to business combinations in guidance that links to Topic 805 has the same meaning as a reference to acquisitions by not-for-profit entities.

Bargain Purchase Option. A provision allowing the lessee, at his option, to purchase the leased property for a price that is sufficiently lower than the expected fair value of the property at the date the option becomes exercisable that exercise of the option appears, at lease inception, to be reasonably assured.

Bargain Renewal Option. A provision allowing the lessee, at his option, to renew the lease for a rental sufficiently lower than the fair rental of the property at the date the option becomes exercisable that exercise of the option appears, at lease inception, to be reasonably assured. Fair rental of a property in this context shall mean the expected rental for equivalent property under similar terms and conditions.

Business. An integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of dividends, lower costs, or other economic benefits directly to investors or other owners, members, or participants. Additional guidance on what a business consists of is presented in paragraphs 805-10-55-4 through 55-9.

Business Combination. A transaction or other event in which an acquirer obtains control of one or more businesses. Transactions sometimes referred to as true mergers or mergers of equals also are business combinations. See also Acquisition by a Not-for-Profit Entity.

Commercial Letter of Credit. document issued typically by a financial institution on behalf of its customer (the account party) authorizing a third party (the beneficiary), or in special cases the account party, to draw drafts on the institution up to a stipulated amount and with specified terms and conditions; it is a conditional commitment (except if prepaid by the account party) on the part of the institution to provide payment on drafts drawn in accordance with the terms of the document.

Contingency. An existing condition, situation, or set of circumstances involving uncertainty as to possible gain (gain contingency) or loss (loss contingency) to an entity that will ultimately be resolved when one or more future events occur or fail to occur.

Credit Derivative. A derivative instrument that has both of the following characteristics:

- One or more of its underlyings are related to any of the following:

- The credit risk of a specified entity (or a group of entities)

- An index based on the credit risk of a group of entities.

- It exposes the seller to potential loss from credit-risk-related events specified in the contract.

Examples of credit derivatives include, but are not limited to, credit default swaps, credit spread options, and credit index products.

Fair Value. The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Financial Standby Letter of Credit. An undertaking (typically by a financial institution) to guarantee payment of a specified financial obligation.

Gain Contingency. An existing condition, situation, or set of circumstances involving uncertainty as to possible gain to an entity that will ultimately be resolved when one or more future events occur or fail to occur.

Indirect Guarantee of Indebtedness. An agreement that obligates the guarantor to transfer funds to a debtor upon the occurrence of specified events, under conditions whereby:

- After funds are transferred from the guarantor to the debtor, the funds become legally available to creditors through their claims against the debtor

- Those creditors may enforce the debtor's claims against the guarantor under the agreement.

Examples of indirect guarantees include agreements to advance funds if a debtor's net income, coverage of fixed charges, or working capital falls below a specified minimum.

Indirectly Related to the Leased Property. The provisions or conditions that in substance are guarantees of the lessor's debt or loans to the lessor by the lessee that are related to the leased property but are structured in such a manner that they do not represent a direct guarantee or loan. Examples include a party related to the lessee guaranteeing the lessor's debt on behalf of the lessee, or the lessee financing the lessor's purchase of the leased asset using collateral other than the leased property.

Lease Term. The fixed noncancelable lease term plus all of the following, except as noted in the following paragraph:

- All periods, if any, covered by bargain renewal options.

- All periods, if any, for which failure to renew the lease imposes a penalty on the lessee in such amount that a renewal appears, at lease inception, to be reasonably assured

- All periods, if any, covered by ordinary renewal options during which any of the following conditions exist:

- A guarantee by the lessee of the lessor's debt directly or indirectly related to the leased property is expected to be in effect.

- A loan from the lessee to the lessor directly or indirectly related to the leased property is expected to be outstanding.

- All periods, if any, covered by ordinary renewal options preceding the date as of which a bargain purchase option is exercisable

- All periods, if any, representing renewals or extensions of the lease at the lessor's option.

The lease term shall not be assumed to extend beyond the date a bargain purchase option becomes exercisable.

Legal Entity. Any legal structure used to conduct activities or to hold assets. Some examples of such structures are corporations, partnerships, limited liability companies, grantor trusts, and other trusts.

Loss Contingency. An existing condition, situation, or set of circumstances involving uncertainty as to possible loss to an entity that will ultimately be resolved when one or more future events occur or fail to occur. The term loss is used for convenience to include many charges against income that are commonly referred to as expenses and others that are commonly referred to as losses.

Minimum Revenue Guarantee. A guarantee granted to a business or its owners that the revenue of the business (or a specific portion of the business) for a specified period of time will be at least a specified minimum amount.

Noncancelable Lease Term. That portion of the lease term that is cancelable only under any of the following conditions:

- Upon the occurrence of some remote contingency

- With the permission of the lessor

- If the lessee enters into a new lease with the same lessor

- If the lessee incurs a penalty in such amount that continuation of the lease appears, at inception, reasonably assured.

Not-for-Profit Entity. An entity that possesses the following characteristics, in varying degrees, that distinguish it from a business entity:

- Contributions of significant amounts of resources from resource providers who do not expect commensurate or proportionate pecuniary return

- Operating purposes other than to provide goods or services at a profit

- Absence of ownership interests like those of business entities.

Entities that clearly fall outside this definition include the following:

- All investor-owned entities

- Entities that provide dividends, lower costs, or other economic benefits directly and proportionately to their owners, members, or participants, such as mutual insurance entities, credit unions, farm and rural electric cooperatives, and employee benefit plans.

Penalty. Any requirement that is imposed or can be imposed on the lessee by the lease agreement or by factors outside the lease agreement to do any of the following:

- Disburse cash

- Incur or assume a liability

- Perform services

- Surrender or transfer an asset or rights to an asset or otherwise forego an economic benefit, or suffer an economic detriment. Factors to consider in determining whether an economic detriment may be incurred include, but are not limited to, all of the following:

- The uniqueness of purpose or location of the property

- The availability of a comparable replacement property

- The relative importance or significance of the property to the continuation of the lessee's line of business or service to its customers

- The existence of leasehold improvements or other assets whose value would be impaired by the lessee vacating or discontinuing use of the leased property

- Adverse tax consequences

- The ability or willingness of the lessee to bear the cost associated with relocation or replacement of the leased property at market rental rates or to tolerate other parties using the leased property.

Performance Standby Letter of Credit. An irrevocable undertaking by a guarantor to make payments in the event a specified third party fails to perform under a nonfinancial contractual obligation.

Probable. The future event or events are likely to occur.

Related Parties. Related parties include:

- Affiliates of the entity

- Entities for which investments in their equity securities would be required, absent the election of the fair value option under the Fair Value Option Subsection of Section 825-10-15, to be accounted for by the equity method by the investing entity

- Trusts for the benefit of employees, such as pension and profit-sharing trusts that are managed by or under the trusteeship of management

- Principal owners of the entity and members of their immediate families

- Management of the entity and members of their immediate families

- Other parties with which the entity may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting parties might be prevented from fully pursuing its own separate interests

- Other parties that can significantly influence the management or operating policies of the transacting parties or that have an ownership interest in one of the transacting parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully pursuing its own separate interests.

Underlying. A specified interest rate, security price, commodity price, foreign exchange rate, index of prices or rates, or other variable (including the occurrence or nonoccurrence of a specified event such as a scheduled payment under a contract). An underlying may be a price or rate of an asset or liability but is not the asset or liability itself. An underlying is a variable that, along with either a notional amount or a payment provision, determines the settlement of a derivative instrument.

Variable Interest Entity. A legal entity subject to consolidation according to the provisions of the Variable Interest Entities Subsections of Subtopic 810-10.

Warranty. A guarantee for which the underlying is related to the performance (regarding function, not price) of nonfinancial assets that are owned by the guaranteed party. The obligation may be incurred in connection with the sale of goods or services; if so, it may require further performance by the seller after the sale has taken place.

Weather Derivative. A forward-based or option-based contract for which settlement is based on a climatic or geological variable. One example of such a variable is the occurrence or nonoccurrence of a specified amount of snow at a specified location within a specified period of time.

CONCEPTS, RULES, AND EXAMPLES

Guarantees

While disclosures of at least some guarantees had been common under GAAP, the economic significance of such arrangements had rarely been measured or disclosed in the past. ASC 460, Guarantees, significantly altered past practice by requiring that the fair value of guarantees be recognized as a liability.

ASC 460 establishes the notion that a guarantee actually consists of two distinct components. These two obligations have quite different accounting implications.

Noncontingent obligation. The first of these components is a noncontingent obligation, namely, the obligation to stand ready to perform over the term of the guarantee in the event that the specified triggering events or conditions occur. This stand-ready obligation is unconditional and thus is not considered a contingent obligation.

Contingent obligation. The second component, which is a contingent obligation, is the obligation to make future payments if those triggering events or conditions occur.

Initial recognition. At the inception of a guarantee, the guarantor would recognize a liability for both the noncontingent and contingent obligations at their fair values. However, in the unusual circumstance that a liability is recognized under ASC 450-20 for the contingent obligation (i.e., because it is deemed probable of occurrence and reasonable of estimation that the guarantor will pay), the liability to be initially recognized for the noncontingent obligation would only be the portion, if any, of the guarantee's fair value not already recognized to comply with ASC 450-20.

It is important to stress that this does not mean that the guarantor records the entire face amount of the guarantee; rather, it is the fair value of the stand-ready obligation that would be recognized. When a guarantee is issued in a stand-alone, arm's-length transaction with an unrelated party, the fair value of the guarantee (and thus the amount to be recognized as a liability) is the premium received by the guarantor. When a guarantee is issued as part of another transaction (such as the sale or lease of an asset) or as a contribution to an unrelated party, the fair value of the liability is measured by the premium that would be required by the guarantor to issue the same guarantee in a stand-alone, arm's-length transaction with an unrelated party.

In practice, if the likelihood that the guarantor will have to perform is judged to be only “reasonably possible” or “remote,” the only amount to be recorded will be the fair value of the noncontingent obligation to stand ready to perform. If, however, the contingency is probable of occurrence and can be reasonably estimated under ASC 450-20, that amount must be recognized and the liability under the guarantee arrangement will be the greater of (1) the fair value computed as explained above, or (2) the amount computed in accordance with ASC 450-20's provisions.

When initially issued, the guidance on computing guarantees where no market information is available made reference to CON 7. In so doing, FASB endorsed the use of the discounted, probability-weighted cash flow method for estimating the stand-ready obligation.

Since, in the author's opinion, in the absence of other, better input data, such as the pricing of insurance to assume the risk of performing on the guarantee, the probability-weighted present value of possible future cash flows could serve as useful input to determining the fair value of guarantees made, the following example is presented.

Example of estimating the fair value of a guarantee using CON 7 when recognition of a loss contingency under ASC 450 would not be otherwise required

Big Red Company guarantees a $1,000,000 debt of Little Blue Company for the next three years in conjunction with selling equipment to Little Blue. Big Red evaluates its risk of payment as follows:

- (1) There is no possibility that Big Red will pay during year 1.

- (2) There is a 15% chance that Big Red will pay during year 2. If it has to pay, there is a 30% chance that it will have to pay $500,000 and a 70% chance that it will have to pay $250,000.

- (3) There is a 20% chance that Big Red will pay during year 3. If it has to pay, there is a 25% chance that it will have to pay $600,000 and a 75% chance that it will have to pay $300,000.

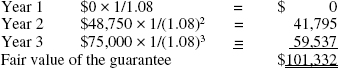

The expected cash flows are computed as follows:

Year 1 100% chance of paying $0 = $0

Year 2 85% chance of paying $0 and a 15% chance of paying (.30 × $500,000 + .70 × $250,000 =) $325,000 = $48,750

Year 3 80% chance of paying $0 and a 20% chance of paying (.25 × $600,000 + .75 × $300,000 =) $375,000 = $75,000

The present value of the expected cash flows is computed as the sum of the years' probability-weighted cash flows, here assuming an appropriate discount rate of 8%.

Based on the foregoing, a liability of $101,332 would be recognized at inception. This would reduce the net selling price of the equipment sold to Little Blue, thereby reducing the profit to be reported on the sale transaction.

Example of estimating the fair value of a guarantee using CON 7 when recognition of a loss contingency under ASC 450 is also required

Assume the same basic facts as in the foregoing example, but now also assume that it has been determined that there is a 60% likelihood that the buyer will eventually default and, after legal process, Big Red will have to repay debt amounting to $400,000 at the end of the fifth year. Assume also that a likelihood of 60% is deemed to make this contingent obligation “probable” under ASC 450. The present value of that payment is $272,233, but ASC 450 does not address or seemingly anticipate the application of present value methods. Thus, it would appear that accrual of the full $400,000 expected loss is required, unaffected by expected timing or by the probability (60%, in this example) that it will occur. Since this amount exceeds the amount computed under ASC 460, no additional amount would be recognized in connection with the noncontingent obligation to stand ready to perform.

If, instead of the immediate foregoing facts, the probable repayments were estimated to be $75,000, then the liabilities to be recognized would total $101,322, of which $75,000 would be required to satisfy the provisions of ASC 450, and the incremental amount, $26,332, would be attributed to the noncontingent obligation.

The entry to record the liability depends upon the circumstances under which the guarantee arose. If the guarantee was issued in a stand-alone transaction for a premium, the offset would be to the asset accepted for the premium's payment (most likely, cash or a receivable). If the guarantee was issued in conjunction with the sale of assets, the proceeds would be allocated between the sale of the asset and the guarantee obligation, so that the profit (loss) on the sale of the asset would be reduced (increased). If the guarantee was issued in conjunction with the formation of a business accounted for under the equity method, the offset would be an increase in the carrying amount of the investment. If the guarantee was issued to an unrelated party for no consideration, an immediate expense would be recognized. If a residual value guarantee was provided by a lessee-guarantor, the offset would be reported as prepaid rent and then amortized over the term of the lease to rent expense. The residual value of equipment by the manufacturer is recognized by the manufacturer as an asset (included in the seller/lessor's net investment in lease).

Subsequent measurement. After initial recognition, the liability is adjusted as the guarantor either is released from risk or is subject to increased risk. ASC 460 does not prescribe the accounting for guarantees subsequent to initial recognition, and there is no requirement to reassess the fair value of the guarantee after inception. In fact, ASC 460 only addresses measurement of a guarantor's liability at the inception of the guarantee and fair value is only to be used in subsequent accounting for the guarantee if the use of that method can be justified under other authoritative guidance. ASC 460 cannot be cited to support adjustments to fair value subsequent to initial recognition.

However, if the guarantor is subsequently released from risk, logically that could be recognized in one of three ways, in the authors' opinion, although no guidance is provided by ASC 460. First, the liability could simply be written off at its expiration or settlement. Second, the liability could be amortized systematically over the guarantee period. Third, the liability might be adjusted to reflect changing fair value, which presumably declines over time as the risk of having to perform decreases. Furthermore, changes dictated by the provisions of ASC 450 (e.g., as a previously “remote” contingency becomes a “probable” one) must be accounted for under that requirement, apart from the requirements of ASC 460.

Fees for guaranteeing a loan. According to ASC 605-20-25-9, fees received for guaranteeing another entity's obligation are to be recognized as income over the guarantee period, rather than at the time of receipt, consistent with other standards governing service fee income recognition. The guarantor is to perform ongoing assessments of the probability of loss related to the guarantee and recognize a liability if the conditions in ASC 450 are met. Upon entering into a guarantee arrangement, the guarantor is required to recognize the stand-ready obligation under the guarantee. The contingent aspect of the guarantee would only be recognized if the conditions defined by ASC 450 are met.

Impact of ASC 460 on revenue recognition on sales with a guaranteed minimum resale value. The authoritative GAAP governing lease accounting holds that manufacturers are precluded from recognizing sales of equipment when they provide purchasers with guarantees of resale value, unless the criteria for sales-type lease accounting are met (ASC 840-10-55-12 et seq.). It states that minimum lease payments, used to ascertain whether a given lease would be an operating or sales-type (capital) lease, are to include the difference between the initial proceeds and the guaranteed amount. Under these circumstances, the fair value of the resale value guarantee is not recognized by the manufacturer, because ASC 460 does not apply to an asset of the guarantor. Given that the manufacturer would report the residual value as an asset, the guarantee does not fall within the domain of ASC 460.

Disclosure requirements. Disclosures can be found in the checklist in the Appendix.

Product Warranties

Product warranties providing for repair or replacement of defective products may be sold separately or may be included in the sale price of the product. ASC 460-10-25-5 points out that “because of the uncertainty surrounding claims that may be made under warranties, warranty obligation fall within the definition of a contingency” and losses are accrued under the conditions in ASC 450-20-25 are met:

- If it is probable that an obligation has been incurred because of a transaction or event that occurred on or before the date of the financial statements and

- If the amount of the obligation can be reasonably estimated.

These conditions may be made for individual elements or groups of items and the particular parties making claims my not be identified at the time of the accrual.

If the warranty extends into the next accounting period, a current liability for the estimated amount of warranty expense expected in the next period must be recorded. If the warranty spans more than the next period, the estimated liability must be partitioned into a current and long-term portion. ASC 460 requires disclosure of product warranties in the notes to financial statements. Disclosure requirements can be found in the Appendix.

The Churnaway Corporation manufactures clothes washers. It sells $900,000 of washing machines during its most recent month of operations. Based on its historical warranty claims experience, it records an estimated warranty expense of 2% of revenues with the following entry:

![]()

During the following month, Churnaway incurs $10,000 of actual labor and $4,500 of actual materials expenses to perform repairs required under warranty claims, which it charges to the warranty claims accrual with the following entry:

Churnaway also sells three-year extended warranties on its washing machines that begin once the initial one-year manufacturer's warranty expires. During one month, it sells $54,000 of extended warranties, which it records with the following entry:

![]()

This liability is unaltered for one year from the purchase date, after which the extended warranty servicing period begins. Churnaway recognizes the warranty revenue on a straight-line basis over the 36 months of the warranty period, using the following entry each month:

![]()

Software vendors/licensors often include, as part of their customary contractual terms, an indemnification clause that indemnifies the licensee against liability and damages (including costs of legal defense) that could arise in the event that a third party claims patent, copyright, trademark, or trade secret infringement with respect to the licensor's software. The indemnification requires the licensor/guarantor to make a payment to the licensee/guaranteed party based on the occurrence of an infringement claim against the licensor that results in liabilities or damages related to the licensed software being used by the licensee. Under such a scenario, an infringement claim covered by the indemnification could impair the ability of the licensee to use the licensed software if, for example, a court orders an injunction or assesses damages.

The indemnification qualifies for the scope exception in ASC 460-10-25-1(b) (discussed in the Scope and Scope exceptions at the beginning of this chapter) as a product warranty or other guarantee for which the underlying is related to the performance of a nonfinancial asset (the software) owned (leased) by the guaranteed party since the licensed software cannot function as intended until the seller-licensor cures the alleged infringement defect.

These arrangements are subject to the same disclosure requirements imposed on other warranty obligations.