33 ASC 470 DEBT

Subjective acceleration clauses

Short-term obligations expected to be refinance

Example of short-term obligation expected to be refinance

ASC 470-20, Debt with Conversion and Other Options

Example of the market value method

Accrued interest upon conversion of convertible debt

Convertible bonds with a “premium put”

Debt convertible into the stock of a consolidated subsidiary

Accounting for a convertible instrument granted or issued to a nonemployee

Convertible bonds with issuer option to settle for cash upon conversion

Own-share lending arrangements related to a convertible debt issuance

Convertible Securities with Beneficial or Contingent Conversion Features

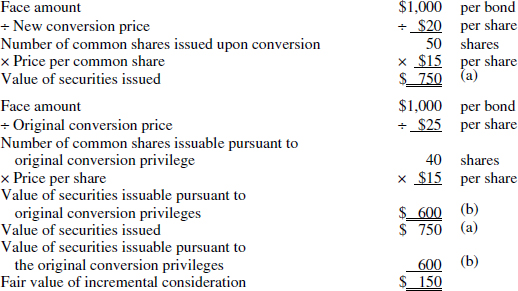

Example 1: Intrinsic value of a conversion feature—fixed dollar terms

Example 2: Intrinsic value of a conversion feature—variable terms

Example 3: Intrinsic value of a conversion feature—contingent price terms

Example 4: Intrinsic value of a conversion feature—contingent feature

Example 5: Intrinsic value of a conversion feature—contingent conversion with variable terms

Example of extinguishment of debt with an embedded conversion feature

Contingent conversion rights triggered by issuer call

Disclosure of contingently convertible securities

Determining applicability of ASC 470-20

Example of induced conversion expense

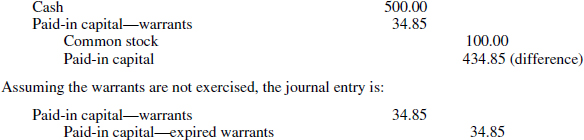

Debt Issued with Stock Warrants

Example of accounting for a bond with a detachable warrant

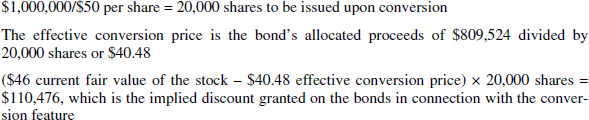

Debt Issued with Conversion Features and Stock Warrants

Example of convertible debt issued with stock warrants

ASC 470-30, Participating Mortgage Loans

Accounting by participating mortgage loan borrowers

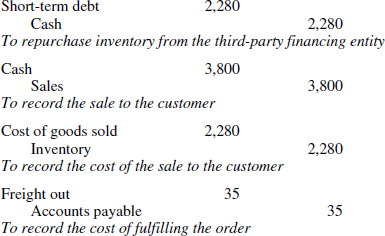

ASC 470-40, Product Financing Arrangements

Example of a product financing arrangement

ASC 470-50, Modifications and Extinguishments

Modifications to conversion privileges

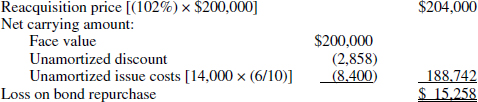

Gain or loss on debt extinguishment

Example of accounting for the extinguishment of debt

ASC 470-60, Troubled Debt Restructurings by Debtors

Is the debtor experiencing financial difficulty?

Has the creditor granted a concession?

Example 1: Settlement of debt by exchange of assets

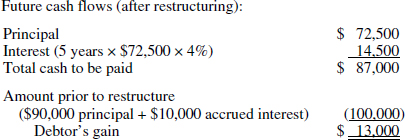

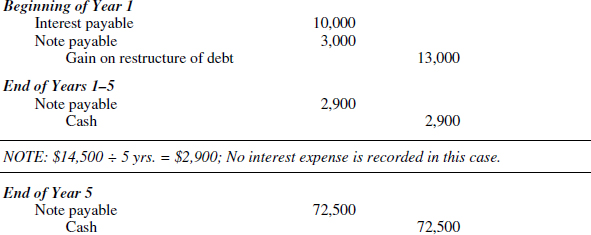

Example 2: Restructuring with gain/loss recognized (payments are less than carrying value)

Example 3: Restructuring with no gain/loss recognized (payments exceed carrying value)

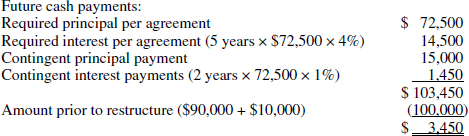

Example 4: Contingent payments

Measuring Liabilities at Fair Value

PERSPECTIVE AND ISSUES

Subtopics

ASC 470, Debt, consists of six subtopics:

- ASC 470-10, Overall, which provides guidance on classification on obligations, such as short-term debt expected to be refinanced on a long-term basis, due-on-demand loans, callable debt, sales of future revenue, increasing rate debt, debt with covenants, revolving credit agreements subject to lock-box arrangements and subjective acceleration clauses, and indexed debt.

- ASC 470-20, Debt with Conversion and Other Options, which provides guidance on debt and certain preferred stock with specific conversion features: debt instruments with detachable warrants, convertible securities in general, beneficial conversion features, interest forfeiture, induced conversions, conversion upon issuer's exercise of call option, convertible instruments issued to nonemployees for goods and services, and own-share lending arrangements issued in contemplation of convertible debt issuance.

- ASC 470-30, Participating Mortgage Loans, provides guidance on the borrower's accounting for a participating mortgage loan if the lender is entitled to participate in appreciation in the fair value of the mortgaged real estate project or the results of operations of the mortgaged real estate project.

- ASC 470-40, Product Financing Arrangements, which provides guidance for determining whether an arrangement involving the sale of inventory is in substance a financing arrangement

- ASC 470-50, Modifications and Extinguishments, provides guidance on all debt instruments extinguishment, except for debt extinguished in a troubled debt restructuring

- ASC 470-60, Troubled Debt Restructurings by Debtors, which addresses measuring and recognition from the debtor's perspective.

Scope and Scope Exceptions

ASC 470-20. ASC 470-20 is divided into two subsections:

- General

- Cash Conversion.

General Subsection. The guidance in the General Subsections does not apply to those instruments within the scope of the Cash Conversion Subsections. The guidance on own-share lending arrangements applies to an equity-classified share-lending arrangement on an entity's own shares when executed in contemplation of a convertible debt offering or other financing.

The guidance in this Section shall be considered after consideration of the guidance in Subtopic 815-15 on bifurcation of embedded derivatives, as applicable (see paragraph 815-15-55-76A).

Cash Conversion Subsections. The guidance in the Cash Conversion Subsections applies only to convertible debt instruments that may be settled in cash (or other assets) upon conversion, unless the embedded conversion option is required to be separately accounted for as a derivative instrument under Subtopic 815-15.

The Cash Conversion Subsections do not apply to any of the following instruments:

- A convertible preferred share that is classified in equity or temporary equity.

- A convertible debt instrument that requires or permits settlement in cash (or other assets) upon conversion only in specific circumstances in which the holders of the underlying shares also would receive the same form of consideration in exchange for their shares.

- A convertible debt instrument that requires an issuer's obligation to provide consideration for a fractional share upon conversion to be settled in cash but that does not otherwise require or permit settlement in cash (or other assets) upon conversion.

For purposes of determining whether an instrument is within the scope of the Cash Conversion Subsections, a convertible preferred share shall be considered a convertible debt instrument if it has both of the following characteristics:

- It is a mandatorily redeemable financial instrument.

- It is classified as a liability under Subtopic 480-10.

ASC 470-30. ASC 470-30 does not apply to creditors in participating mortgage loan arrangements and to the following transactions:

- Participating leases

- Debt convertible at the option of the lender into equity ownership of the property

- Participating loans resulting from troubled debt restructurings.

ASC 470-40. The guidance in ASC 470-40 applies to product financing arrangements for “products that have been produced by or were originally purchased by the sponsor or purchased by another entity on behalf of the sponsor.” The arrangement must have the following characteristics:

- The financing arrangement requires the sponsor to purchase the product, a substantially identical product, or processed goods of which the product is a component at specified prices. The specified prices are not subject to change except for fluctuations due to finance and holding costs. This characteristic of predetermined prices also is present if any of the following circumstances exist:

- The specified prices in the financing arrangement are in the form of resale price guarantees under which the sponsor agrees to make up any difference between the specified price and the resale price for products sold to third parties.

- The sponsor is not required to purchase the product but has an option to purchase the product, the economic effect of which compels the sponsor to purchase the product; for example, an option arrangement that provides for a significant penalty if the sponsor does not exercise the option to purchase.

- The sponsor is not required by the agreement to purchase the product but the other entity has an option whereby it can require the sponsor to purchase the product.

- The payments that the other entity will receive on the transaction are established by the financing arrangement, and the amounts to be paid by the sponsor will be adjusted, as necessary, to cover substantially all fluctuations in costs incurred by the other entity in purchasing and holding the product (including interest). This characteristic ordinarily is not present in purchase commitments or contractor-subcontractor relationships.

(ASC 470-40-15-2)

ASC 470-40 does not apply to the following transactions and activities:

- Ordinary purchase commitments in which the risks and rewards of ownership are retained by the seller (for example, a manufacturer or other supplier) until the product is transferred to a purchaser

- Typical contractor-subcontractor relationships in which the contractor is not in substance the owner of product held by the subcontractor and the obligation of the contractor is contingent on substantial performance on the part of the subcontractor.

- Long-term unconditional purchase obligations (for example, take-or-pay contracts) specified by Subtopic 440-10. At the time a take-or-pay contract is entered into, which is an unconditional purchase obligation, either the product does not yet exist (for example, electricity) or the product exists in a form unsuitable to the purchaser (for example, unmined coal); the purchaser has a right to receive future product but is not the substantive owner of existing product.

- Unmined or unharvested natural resources and financial instruments.

- Transactions for which sales revenue is recognized currently in accordance with the provisions of Topic 605.

- Typical purchases by a subcontractor on behalf of a contractor. In a typical contractor-subcontractor relationship, the purchase of product by a subcontractor on behalf of a contractor ordinarily leaves a significant portion of the subcontractor's obligation unfulfilled. The subcontractor has the risks of ownership of the product until it has met all the terms of a contract. Accordingly, the typical contractor-subcontractor relationship shall not be considered a product financing arrangement.

(ASC 470-40-15-3)

ASC 470-50. ASC 470-50 does not apply to the following transactions and activities:

- Conversions of debt into equity securities of the debtor pursuant to conversion privileges provided in the terms of the debt at issuance. Additionally, the guidance in this Subtopic does not apply to conversions of convertible debt instruments pursuant to terms that reflect changes made by the debtor to the conversion privileges provided in the debt at issuance (including changes that involve the payment of consideration) for the purpose of inducing conversion. Guidance on conversions of debt instruments (including induced conversions) is contained in paragraphs 470-2040-13 and 470-20-40-15.

- Extinguishments of debt through a troubled debt restructuring. (See Section 470-6015 for guidance on determining whether a modification or exchange of debt instruments is a troubled debt restructuring. If it is determined that the modification or exchange does not result in a troubled debt restructuring, the guidance in this Subtopic shall be applied.)

- Transactions entered into between a debtor or a debtor's agent and a third party that is not the creditor.

(ASC 470-50-15-3)

Overview

Long-term (or noncurrent) liabilities are liabilities that will be paid or otherwise settled over a period of more than one year, or if longer, greater than one operating cycle.

Debt remains on the books of the debtor until it is extinguished. In most cases, a debt is extinguished at maturity, when the required principal and interest payments have been made and the debtor has no further obligation to the creditor. In other cases, the debtor may desire to extinguish the debt before its maturity. For example, if market interest rates are falling, a debtor may choose to issue debt at the new lower rate and use the proceeds to retire older higher-interest-rate debt. ASC 405-20-40-1 states that a debt is extinguished if either of two conditions is met.

- The debtor pays the creditor and is relieved of its obligation for the liability.

- The debtor is legally released from being the primary obligor under the liability, either judicially or by the creditor.

If a debtor experiences financial difficulties before the debt is repaid, a creditor may need to recognize an impairment of the debt. Under ASC 310-10-35-16, an impairment of the debt is recognized when the present value of the expected future cash flows discounted at the debt's original effective interest rate is less than the recorded investment in the debt. If for economic or legal reasons related to the debtor's financial difficulties, the creditor grants the debtor concessions that would not otherwise have been granted, the debtor must determine how to recognize the effects of the troubled debt restructuring (ASC 470-60).

Some debt is issued with terms that allow it to be converted to an equity instrument (common or, less often, preferred stock) at a future date. When issued, under current GAAP, no value is attributed to the conversion feature. When the debt is converted, the stock issued is generally valued at the carrying value of the debt (ASC 470). In certain situations, a debtor will modify the conversion privileges after issuance of the debt in order to induce prompt conversion of the debt into equity, in which case the debtor must recognize an expense for this consideration (ASC 470-20-40-16).

Debt can also be issued with stock warrants, which allow the holder to purchase a stated number of common shares at a certain price within a defined time period. If debt is issued with detachable warrants, the proceeds of issuance are allocated between the two financial instruments (ASC 470-20-05).

DEFINITIONS OF TERMS

Source: ASC 470

Beneficial Conversion Feature. A nondetachable conversion feature that is in the money at the commitment date.

Callable Obligation. An obligation is callable at a given date if the creditor has the right at that date to demand, or to give notice of its intention to demand, repayment of the obligation owed to it by the debtor.

Carrying Amount. For a receivable, the face amount increased or decreased by applicable accrued interest and applicable unamortized premium, discount, finance charges, or issue costs and also an allowance for uncollectible amounts and other valuation accounts. For a payable, the face amount increased or decreased by applicable accrued interest and applicable unamortized premium, discount, finance charges, or issue costs.

Convertible Security. A security that is convertible into another security based on a conversion rate. For example, convertible preferred stock that is convertible into common stock on a two-for-one basis (two shares of common for each share of preferred).

Debt. A receivable or payable (collectively referred to as debt) represents a contractual right to receive money or a contractual obligation to pay money on demand or on fixed or determinable dates that is already included as an asset or liability in the creditor's or debtor's balance sheet at the time of the restructuring.

Fair Value. The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Firm Commitment. An agreement with an unrelated party, binding on both parties and usually legally enforceable, with the following characteristics:

- The agreement specifies all significant terms, including the quantity to be exchanged, the fixed price, and the timing of the transaction. The fixed price may be expressed as a specified amount of an entity's functional currency or of a foreign currency. It may also be expressed as a specified interest rate or specified effective yield. The binding provisions of an agreement are regarded to include those legal rights and obligations codified in the laws to which such an agreement is subject. A price that varies with the fair value of the item that is the subject of the firm commitment cannot qualify as a fixed price. For example, a price that is specified in terms of ounces of gold would not be a fixed price if the fair value of the item to be purchased or sold under the firm commitment varied with the price of gold.

- The agreement includes a disincentive for nonperformance that is sufficiently large to make performance probable. In the legal jurisdiction that governs the agreement, the existence of statutory rights to pursue remedies for default equivalent to the damages suffered by the nondefaulting party, in and of itself, represents a sufficiently large disincentive for nonperformance to make performance probable for purposes of applying the definition of a firm commitment.

Lock-Box Arrangement. An arrangement with a lender whereby the borrower's customers are required to remit payments directly to the lender and amounts received are applied to reduce the debt outstanding. A lock-box arrangement refers to any situation in which the borrower does not have the ability to avoid using working capital to repay the amounts outstanding. That is, the contractual provisions of a loan arrangement require that, in the ordinary course of business and without another event occurring, the cash receipts of a debtor are used to repay the existing obligation.

Long-Term Obligations. Long-term obligations are those scheduled to mature beyond one year (or the operating cycle, if applicable) from the date of an entity's balance sheet.

Operating Cycle. The average time intervening between the acquisition of materials or services and the final cash realization constitutes an operating cycle.

Probable. The future event or events are likely to occur.

Product Financing Arrangement. A product financing arrangement is a transaction in which an entity sells and agrees to repurchase inventory with the repurchase price equal to the original sale price plus carrying and financing costs, or other similar transactions.

Public Entity. An entity that meets any of the following criteria:

- Has equity securities that trade in a public market, either on a stock exchange (domestic or foreign) or in an over-the-counter market, including securities quoted only locally or regionally

- Makes a filing with a regulatory agency in preparation for the sale of any class of equity securities in a public market

- Is controlled by an entity covered by the preceding criteria. That is, a subsidiary of a public entity is itself a public entity.

An entity that has only debt securities trading in a public market (or that has made a filing with a regulatory agency in preparation to trade only debt securities) is not a public entity.

Reasonably Possible. The chance of the future event or events occurring is more than remote but less than likely.

Recorded Investment in the Receivable. The recorded investment in the receivable is the face amount increased or decreased by applicable accrued interest and unamortized premium, discount, finance charges, or acquisition costs and may also reflect a previous direct write-down of the investment.

Springing Lock-Box Arrangement. Some borrowings outstanding under a revolving credit agreement include both a subjective acceleration clause and a requirement to maintain a springing lock-box arrangement, whereby remittances from the borrower's customers are forwarded to the debtor's general bank account and do not reduce the debt outstanding until and unless the lender exercises the subjective acceleration clause.

Subjective Acceleration Clause. A subjective acceleration clause is a provision in a debt agreement that states that the creditor may accelerate the scheduled maturities of the obligation under conditions that are not objectively determinable (for example, if the debtor fails to maintain satisfactory operations or if a material adverse change occurs).

Substantive Conversion Feature. A conversion feature that is at least reasonably possible of being exercisable in the future absent the issuer's exercise of a call option.

Time of Issuance. The date when agreement as to terms has been reached and announced, even though the agreement is subject to certain further actions, such as directors' or stockholders' approval.

Time of Restructuring. Troubled debt restructurings may occur before, at, or after the stated maturity of debt, and time may elapse between the agreement, court order, and so forth, and the transfer of assets or equity interest, the effective date of new terms, or the occurrence of another event that constitutes consummation of the restructuring. The date of consummation is the time of the restructuring.

Troubled Debt Restructuring. A restructuring of a debt constitutes a troubled debt restructuring if the creditor for economic or legal reasons related to the debtor's financial difficulties grants a concession to the debtor that it would not otherwise consider.

Units-of-Revenue Method. A method of amortizing deferred revenue that arises under certain sales of future revenues. Under this method, amortization for a period is calculated by computing a ratio of the proceeds received from the investor to the total payments expected to be made to the investor over the term of the agreement, and then applying that ratio to the period's cash payment.

Violation of a Provision. The failure to meet a condition in a debt agreement or a breach of a provision in the agreement for which compliance is objectively determinable, whether or not a grace period is allowed or the creditor is required to give notice of its intention to demand repayment.

Working Capital. Working capital (also called net working capital) is represented by the excess of current assets over current liabilities and identifies the relatively liquid portion of total entity capital that constitutes a margin or buffer for meeting obligations within the ordinary operating cycle of the entity.

CONCEPTS, RULES, AND EXAMPLES

ASC 470-10, Overall

Classification.

The currently maturing portion of long-term debt or of capital lease obligations are classified as current liabilities if the obligations are to be liquidated by using assets classified as current. However, if the currently maturing debt is to be liquidated by using noncurrent assets (i.e., by using a sinking fund that is properly classified as a noncurrent investment) then these obligations are to be classified as long-term liabilities.

Due on Demand Loans.

Obligations that, by their terms, are due on demand (ASC 47010-45-10) or will be due on demand within one year (or the reporting entity's operating cycle, if longer) from the statement of financial position date, even if liquidation is not expected to occur within that period, are required to be classified as current liabilities.

Even noncurrent debt may be due on demand under certain circumstances. Long-term obligations that contain creditor call provisions are to be classified as current liabilities, if as of the statement of financial position date the debtor is in violation of the agreement and either:

- That violation makes the obligation callable, or

- Unless cured within a grace period specified in the agreement, that violation will make the obligation callable.

If either of these two conditions exist, the long-term obligation is required to be classified as a current liability unless either:

- The creditor has waived the right to call the obligation caused by the debtor's violation or the creditor has subsequently lost the right to demand repayment for more than one year (or operating cycle, if longer) from the statement of financial position date, or

- The obligation contains a grace period for remedying the violation, and it is probable that the violation will be cured within the grace period.

If either of these situations applies, management is required to disclose the circumstances in the financial statements.

Demand notes with scheduled repayment terms. In some instances, a demand loan will include a repayment schedule calling for scheduled principal reductions. The loan agreement may contain language such as the following examples:

This term note shall mature in monthly installments as set forth herein, or on demand, whichever is earlier.

Principal and interest are due on demand, or if demand is not made, in quarterly installments commencing on . . .

Under ASC 470-10-45-10, an obligation containing such terms is considered due on demand even though the debt agreement specifies repayment terms. In either instance, the creditor, at its sole discretion, can demand full repayment at any time. This situation is distinguished from a subjective acceleration clause, which is addressed separately below.

Increasing-rate debt.

Arrangements commonly referred to as “increasing-rate notes” are debt instruments that mature at a defined, near-term date, but which can be continually extended (renewed) by the borrower for a defined longer period of time with predefined increases in the interest rate as extensions are elected.

Management of the borrower estimates the effective outstanding term of the debt after considering its plans, ability and intent to service the debt. Based upon this estimated term, the borrower's periodic interest rate is determined using the interest method. Thus, a constant yield is computed over the estimated term resulting in the accrual of additional interest during the earlier portions of the term.

Debt interest costs are amortized over the estimated outstanding term of the debt using the interest method. Any excess accrued interest resulting from repaying the debt prior to the estimated maturity date is an adjustment of interest expense in the period of repayment. The adjustment is not permitted to be treated as an extraordinary item.

The classification of the debt as current or noncurrent is based on the expected source of repayment. Thus, this classification need not be consistent with the period used to determine the periodic interest cost. For example, the time frame used for the estimated outstanding term of the debt could be a year or less, but because of a planned long-term refinancing agreement the noncurrent classification could be used.

Furthermore, the term-extending provisions of the debt instrument are evaluated to ascertain whether they constitute a derivative financial instrument under ASC 815. If so, the derivative element of the instrument is, in all likelihood, not considered “clearly and closely related” to the host instrument (the debt), and thus would have to be reported separately at fair value with changes in fair value reported in net income each period.

Subjective acceleration clauses.

Long-term obligations that contain subjective acceleration clauses are classified as current liabilities if circumstances (such as recurring losses or liquidity problems) indicate that it is probable that the lender will exercise its rights under the clause and demand repayment within one year (or one operating cycle, if longer). If, on the other hand, the likelihood of the acceleration of the due date is remote, the obligation continues to be classified as long-term debt on the statement of financial position. Situations between the probable and remote thresholds (i.e., it is deemed reasonably possible that the lender would demand repayment) require disclosure of the existence of the provision of the agreement (ASC 470-10-45).

Debt with covenants.

Most commercial debt agreements contain a range of financial covenants. These covenants legally bind the borrower to comply with their requirements as a condition of the lender extending credit. The failure by the borrower to comply with these conditions often provides the lender with the contractual right to accelerate the due date, commonly to declare the full amount of the debt due and payable on demand. Unless a properly worded waiver is obtained by the borrower in such a situation, its statement of financial position would have to reflect the debt, that which would otherwise be classified as long-term, as a current liability. This in turn might create or complicate issues for management with respect to the assessment of whether there is substantial doubt about the ability of the reporting entity to continue as a going concern.

While a complete waiver, effectively a promise by the lender that it will not exercise its rights under the financial covenants for at least one year from the statement of financial position date, makes it possible to continue presenting the debt as noncurrent, great care must be exercised in interpreting the substance of such an agreement.

In practice, many waivers are not effective and cannot form the basis for continued accounting for the debt as noncurrent. For example, a waiver “as of” the current statement of financial position date provides no real comfort, since the lender is entitled to assert its rights as soon as the very next day. Likewise, a waiver pending (i.e., conditioned on) compliance with the covenants at the next scheduled submission of a borrower's covenant compliance letter (generally quarterly, possibly monthly) offers no assurance that the borrower will successfully meet its obligations, and hence also affords no basis for presentation of the debt as noncurrent.

A loan covenant may require that compliance determinations be made at quarterly or semiannual intervals. A borrower may be in violation of the covenant at the end of its fiscal year and obtain a waiver from the lender, for a period greater than one year, of the lender's right to demand repayment arising from that specific year-end violation. Often, however, the lender will include language in the waiver document that reserves its right to demand repayment should another violation occur at a subsequent measurement date, including those dates that occur during the ensuing year.

Under these circumstances, management of the borrower/reporting entity considers whether both of the following conditions exist under the specific circumstances:

- A violation of one or more covenants that gives the lender the right to call the debt (declare it payable on demand) has occurred at the statement of financial position date, or would have occurred absent a modification of the loan, and

- It is probable that, at measurement dates occurring during the next 12 months, the borrower will be unable to cure the default (i.e., comply with the covenant).

If both of these conditions are present, the borrower is required to classify the debt as a current liability; otherwise, it can continue to classify the debt as noncurrent.

Revolving credit agreements.

Borrowings outstanding under a revolving credit agreement sometimes include both a subjective acceleration clause (as discussed above) and a requirement to maintain a lockbox into which the borrower's customers send remittances that are then used to reduce the debt outstanding. These borrowings are short-term obligations and are classified as current liabilities unless the entity has the intent and ability to refinance the revolving credit agreement on a long-term basis (i.e., the conditions in ASC 470-10-45, as discussed below, are met). However, if the lockbox is a springing lockbox, which is a lockbox agreement in which remittances from the borrower's customers are forwarded to its general bank account and do not reduce the debt outstanding unless the lender exercises the subjective acceleration clause, the obligations are still considered to be long-term since the remittances do not automatically reduce the debt outstanding if the acceleration clause has not been exercised.

Indexed debt.

Occasionally, debt instruments are issued with guaranteed and contingent payments. The contingent payments may be linked to a specific index, like the S&P 500 or the price for a specific commodity. If the right to receive the indexing feature is separable from the debt instrument, the proceeds are allocated between the debt instrument and investor's stated right to receive the contingent payment. (ASC 410-10-25-3 and 25-4)

Short-term obligations expected to be refinanced.

Short-term obligations that arise in the normal course of business and are due under customary trade terms are classified as current liabilities. Under certain circumstances, however, the reporting entity is permitted to exclude all or a portion of these obligations from current liabilities. To qualify for this treatment, management must have both the intent and ability to refinance the obligation on a long-term basis. Management's intent is to be supported by either of the following (ASC 470-10-45-14):

- Post-statement of financial position date issuance of a long-term obligation or equity securities. After the date of the entity's statement of financial position, but before that statement of financial position is issued, a long-term obligation is incurred or equity securities are issued for the purpose of refinancing the short-term obligations on a long-term basis.

- Financing agreement. Before the statement of financial position is issued, the entity has entered into a financing agreement that clearly enables the entity to refinance its short-term obligation on a long-term basis on readily determinable terms that meet all of the following requirements:

- The agreement is noncancelable by the lender (or prospective lender) or investor and will not expire within one year (or one operating cycle, if longer) of the statement of financial position date.

- The replacement debt will not be callable during that period except for violation of a provision of the financing agreement with which compliance is objectively determinable or measurable.

- At the date of the statement of financial position, the reporting entity is not in violation of the terms of the financing agreement and there is no information that a violation occurred subsequent to the statement of financial position and before issuance of the financial statements, unless such a violation was waived by the lender.

- The lender (prospective lender) or investor is expected to be financially capable of honoring the financing agreement.

For the purposes of condition 2b above, violation of a provision is defined as a failure of the reporting entity to meet a condition included in the agreement; or the violation of a provision such as a restrictive covenant, representation, or warranty. A violation is not to be disregarded for this purpose, even if the agreement contains a grace period to cure it and/or if the lender is required to give the borrower notice. The requirement that compliance be objectively determinable or measurable precludes commitments that include subjective acceleration clauses (discussed previously) from being considered qualified financing agreements.

The above scenario is based on an assumption that the refinancing will take place subsequent to the date of the statement of financial position. If, instead, prior to the date of the statement of financial position, the reporting entity receives cash proceeds from long-term financing intended to be used to repay a short-term obligation after the date of the statement of financial position, the cash received is to be classified on the statement of financial position in noncurrent assets if the short-term obligation to be settled with that cash is classified in noncurrent liabilities.

The amount of short-term debt to be reclassified is not permitted to exceed the amount raised by the replacement debt or equity issuance, nor can it exceed the amount specified in the financing agreement. If the amount specified in the financing agreement can fluctuate, then the maximum amount of short-term debt that can be reclassified is equal to a reasonable estimate of the minimum amount expected to be available on any date from the due date of the maturing short-term obligation to the end of the succeeding fiscal year. If no estimate can be made of the minimum amount available under the financing agreement, none of the short-term debt can be reclassified as long-term.

If the short-term debt is refinanced by issuing equity instruments, the portion excluded from current liabilities is to be classified under noncurrent liabilities. Under no circumstances would the reclassified debt be shown in the equity section of the statement of financial position.

If debt or other agreements limit the ability of the reporting entity to fully utilize the proceeds of the refinancing agreement (for example, a clause in another debt agreement sets a maximum debt-to-equity ratio), then only the amount that can be borrowed without violating the limitations expressed in those other agreements can be reclassified as long-term.

ASC 470-10-45-15 states that if an entity uses current assets after the statement of financial position date to repay a current obligation, and then replaces those current assets by issuing either equity securities or long-term debt before the issuance of the statement of financial position, the currently maturing debt must continue to be classified as a current liability at the date of the statement of financial position.

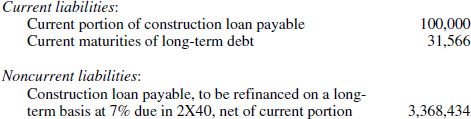

Duboe Distribution Co. has obtained $3,500,000 of bridge financing in the form of a construction loan to assist it in completing construction of a new public warehouse. All construction is completed by the date of the statement of financial position, after which Duboe has the following three choices for refinancing the bridge loan:

- Enter into a 30-year fixed-rate mortgage for $3,400,000 at 7% interest, leaving Duboe with a $100,000 shortfall it would have to repay with available cash. Under this scenario, Duboe reports as current debt the $100,000, as well as $31,566, the portion of the mortgage principal due within one year, with the remainder of the mortgage itemized as long-term debt. The presentation follows:

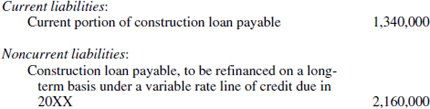

- Pay off the bridge loan with Duboe's existing variable-rate line of credit (LOC), which expires in two years. The maximum allowable amount that can be borrowed under the LOC is 80% of Duboe's eligible accounts receivable, defined as those accounts receivable not more than 90 days old. Over the two-year remaining term of the LOC, the lowest level of qualifying accounts receivable is expected to be $2,700,000. Thus, only $2,160,000 ($2,700,000 × 80%) of the debt would be classified as long-term, while $1,340,000 is classified as a short-term obligation. The presentation follows:

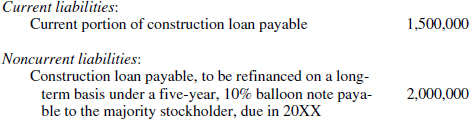

- Obtain a 10% loan from Duboe's majority stockholders, with a balloon payment due in five years. Under the terms of this arrangement, the owner is entitled to withdraw up to $1,500,000 of funding at any time, even though $3,500,000 is currently available to Duboe. Under this approach, $1,500,000 is callable, and therefore must be classified as a short-term obligation. The remainder is classified as long-term debt. The presentation follows:

The presentations illustrated above would be accompanied by note disclosures under ASC 470-10-50-4 of the general terms of the financing agreement, as well as the terms of the new obligation incurred, or expected to be incurred, as a result of the refinancing. If part or all of the refinancing will be achieved through the issuance of equity, the notes should disclose a description of the securities issued or expected to be issued as a result of the refinancing. In addition, should the debtor decide on the third course of action, the notes would be supplemented with the required related-party disclosures.

ASC 470-20, Debt with Conversion and Other Options

Convertible Debt

Bonds are frequently issued with the right to convert into common stock of the company at the holder's option. Convertible debt is typically used for two reasons. First, when a specific amount of funds is needed, convertible debt often allows a lesser number of shares to be issued (assuming conversion) than if the funds were raised by directly issuing the shares. Thus, less dilution occurs. Second, the conversion feature allows debt to be issued at a lower interest rate and with fewer restrictive covenants than if the debt was issued without it.

Features of convertible debt typically include (1) a conversion price 15-20% greater than the fair value of the stock when the debt is issued; (2) conversion features (price and number of shares) which protect against dilution from stock dividends, splits, etc.; and (3) a callable feature at the issuer's option, which is usually exercised once the conversion price is reached (thus forcing conversion or redemption).

Convertible debt also has its disadvantages. If the stock price increases significantly after the debt is issued, the issuer would have been better off by simply issuing the stock. Additionally, if the price of the stock does not reach the conversion price, the debt will never be converted (a condition known as overhanging debt).

When convertible debt is issued and the conversion price is greater than the fair value of the stock on the issuance date, no value is apportioned to the conversion feature when recording the issue (ASC 470-20-05). The debt and its interest are reported as if it were a nonconvertible debt. Upon conversion, the stock may be valued at either the book value or the fair value of the bonds.

If the book value approach is used, the new stock is valued at the carrying value of the converted bonds. This method is widely used since no gain or loss is recognized upon conversion, and the conversion represents the transformation of contingent shareholders into shareholders. It does not represent the culmination of an earnings cycle. The primary weakness of this method is that the total value attributed to the equity security by the investors is not given accounting recognition.

Assume that a $1,000 bond with an unamortized discount of $50 and a fair value of $970 is converted into 10 shares of $10 par common stock whose fair value is $97 per share. Conversion using the book value method is recorded as follows:

The alternative market value approach assumes the new stock issued is valued at market (i.e., the fair value of the stock issued or the fair value of the bonds converted, whichever is more easily determinable). A gain (loss) occurs when the fair value of the stocks or bonds is less (greater) than the carrying value of the bond.

Assume the same facts as the example above. The entry to record the conversion is

The weakness of this method is that a gain or loss can be reported as a result of an equity transaction. Only the existing shareholders are affected, as their equity will increase or decrease, but the firm as a whole is unaffected. For this reason, the market value approach is not widely used.

When convertible debt is retired, the transaction is handled in the same manner as nonconvertible debt: the difference between the acquisition price and the carrying value of the bond is reported currently as a gain or loss.

Accrued interest upon conversion of convertible debt.

Per ASC 470-20-40-11, if terms of the convertible debt instrument provide that any accrued interest at the date of conversion is forfeited by the former debt holder, the accrued interest (net of income tax) from the last payment date to the conversion date should be charged to interest expense and credited to capital as a part of the cost basis of the securities issued.

Convertible bonds with a “premium put.”

Some convertible bonds contain mutually exclusive features, with one obviously being the right to convert to the issuer's common or preferred stock. In some instances, the other feature is the right, usually on specified dates before or at the stated maturity of the debt, to cause the issuer to repurchase the debt at a price higher than par or the issuance price. This is known as a “premium put” feature. An early view of premium puts held that the issuer should accrue a liability for the put premium over the period from the date of issuance to the initial put date, and that this accrual should continue regardless of fair value changes. It further held if the put expires unexercised and if—as would be highly likely if the holders chose to ignore the right to put the debt back to the issuer—the fair value of the common stock exceeds the put price at expiration date, the put premium should be credited to additional paid-in capital. Additionally, it held that if the put were to expire unexercised (in the situation where the debt maturity is later than the last put exercise date) and if the put price exceeds the fair value of the common stock at that date, the put premium should be amortized as a yield adjustment over the remaining term of the debt, reducing interest cost.

Under ASC 815, an embedded put is a derivative instrument subject to that standard. This “grandfathered” permission for entities not to account separately for embedded premium puts in pre-1998 or pre-1999 hybrid instruments issued at par; the earlier view was to continue to apply to an entity which elected not to separately account for the embedded derivative. However, separate accounting was required for convertible debt not “grandfathered” under this provision, and thus, ASC 815 does apply to more recently issued convertible debt having premium put features.

ASC 460-10 requires explicit recognition of guarantees at their inceptions (see Chapter 19 for complete discussion of this topic). A premium put is a form of guarantee arrangement, and thus the fair value of the put must now be recognized at the date of issuance of the convertible debt bearing this feature, unless the put is accounted for as a derivative (and thus also recorded at fair value) under ASC 815. As a practical matter, in either case a liability will be recognized for the fair value of the put option embedded in the convertible debt.

Under ASC 815 this derivative financial instrument will be marked to fair value at each financial reporting date. Whether the adjustment increases or decreases the recorded amount from one period to the next depends largely on the price performance of the issuer's stock, since increasing value of the stock raises the likelihood of conversion and thus decreases the perceived value of the put option. In the author's opinion, any adjustment to the carrying value of the put option should result in adjustments to the entity's interest expense for the period.

Debt convertible into the stock of a consolidated subsidiary.

According to ASC 47020-25, in the consolidated financial statements, (1) debt issued by a consolidated subsidiary that is convertible into that subsidiary's stock and (2) debt issued by a parent company that is convertible into the stock of a consolidated subsidiary should be accounted for in accordance with ASC 470-20-05. That is, no portion of the proceeds from the issuance of the debt should be accounted for as attributable to the conversion feature. ASC 470-20-25 did not apply to convertible debt instruments that require a cash settlement by the issuer of an in-the-money conversion feature, that provide the holder an option to receive cash for an in-the-money conversion feature, or that have a beneficial conversion feature.

Accounting for a convertible instrument granted or issued to a nonemployee.

ASC 470-20-30 describes the accounting for a convertible instrument that is used to pay a nonemployee for goods or services if that instrument contains a nondetachable conversion option. The measurement date under ASC 505-50 should be used to measure the intrinsic value of the conversion option rather than the commitment date. The proceeds from issuing the instrument for purposes of determining whether a beneficial conversion option exists is the fair value of the instrument or the fair value of the goods and services received, whichever is more reliably measured. The fair value of the convertible instrument can be measured by applying ASC 505-50. (For details, see Chapter 26.) Once the convertible instrument is issued, distributions paid or payable are financing costs rather than adjustments of the cost of the goods or services received.

If a purchaser of a convertible instrument that contains an embedded beneficial conversion option provides goods or services to the issuer under a separate contract, the contracts should be considered separately unless the separately stated pricing is not equal to fair value. If not equal to fair value, the terms of the respective transactions should be adjusted. The convertible instrument should be recognized at its fair value with a corresponding increase or decrease to the purchase price of the goods or services.

Convertible bonds with issuer option to settle for cash upon conversion.

ASC 81515-55 addressed a variant of convertible bonds that give the issuer (the reporting entity) the option of settling for cash, rather than stock, at the time conversion is elected by holders. In some versions of this arrangement, the debtor would be obligated to settle in cash, based on the stock price at the conversion date. In others, the issuer would have the option to deliver shares or cash based on the contractual conversion rate, or more complex formulae might cause partial settlement in cash.

ASC 815 requires that in the situation of a mandatory cash settlement upon conversion, the embedded derivative (which is a cash-settled written call option) must be accounted for separately from the debt, and changes in the derivative's fair value will be reported currently in earnings. When the conversion option can be settled in stock, however, the embedded derivative is indexed only to the issuer's stock and thus, under ASC 815-40 would not be separately accounted for.

If a convertible bond is issued with terms that require the issuer to satisfy the obligation (the amount accrued to the benefit of the holder exclusive of the conversion spread) in cash and to satisfy the conversion spread (the excess conversion value over the accreted value) in either cash or stock, the debt should be accounted for like convertible debt (that is, as a combined instrument under current GAAP) if the conversion spread meets the requirements of ASC 815-40. If the conversion spread feature does not meet those provisions, ASC 815 requires that the embedded derivative be separated from the debt host contract and accounted for by the issuer separately as a derivative instrument.

If a convertible bond is issued with terms that permit the issuer to satisfy the entire obligation in either stock or cash, the bond should be accounted for as conventional convertible debt. If the holder exercises the conversion and the issuer pays cash, the debt is extinguished and the issuer should account for the transaction in accordance with ASC 470-50. ASC 47050-45-1 removed the mandatory extraordinary item treatment for any gain or loss on debt extinguishment, but if the criteria in ASC 225-20-45 are met (which is thought to be unlikely) extraordinary classification is still possible.

ASC 470-20-40-12 provides accounting guidance with respect to a financial instrument that contains the following provisions:

- Instrument is convertible at the option of its holder into a fixed number of shares of the issuer's common stock.

- At conversion, the issuer must settle the obligation to the holder as follows:

- Payment in cash for the accreted value of the obligation (for a zero-coupon obligation, the accreted value is the amount received from the holder at issuance plus interest accreted from date of issuance to date of settlement)

- Payment in either cash or stock to satisfy the conversion spread (the difference between the conversion value over the accreted value)

- If the holder does not exercise the conversion option, the issuer is obligated to settle the accreted value of the debt in cash at maturity.

Questions have arisen regarding the accounting for the settlement of this instrument partially in cash (the recognized liability) and partially in stock (the unrecognized equity instrument). ASC 470-20-40-12 states that only the cash payment is to be considered in computing gain or loss on settlement of the recognized liability. Shares transferred to the holder to settle the excess conversion spread represented by the embedded equity instrument are not considered part of the settlement of the debt component of the instrument.

ASC 470-20 specifies that issuers of convertible debt instruments that may be settled in cash upon conversion should separately account for the liability and equity components in a manner that will reflect the entity's nonconvertible debt borrowing rate when interest cost is recognized in subsequent periods. An exception to this rule, however, is when an embedded conversion option must be accounted for as a derivative instrument. Convertible preferred shares categorized as equity in the statement of financial position are also excluded from the effects of ASC 470.

For instruments addressed by ASC 470, initial measurement of the carrying amount of the liability component is to be determined by measuring the fair value of a similar liability (including any embedded features other than the conversion option) that does not have an associated equity component. The carrying amount of the equity component represented by the embedded conversion option is then computed by deducting the fair value of the liability component from the initial proceeds ascribed to the convertible debt instrument as a whole. Embedded features that are determined to be nonsubstantive at the issuance date are not to affect the initial measurement of the liability component. In this context, an embedded feature other than the conversion option (including an embedded prepayment option) is to be considered nonsubstantive if, at issuance, the issuer concludes that it is probable that the embedded feature will not be exercised. If the allocation to the liability component using this methodology results in a difference in basis versus that reported for tax purposes, then interperiod tax allocation (deferred tax accounting) must also be applied.

Convertible debt instruments affected by the foregoing requirements are not available to be accounted for under the fair value option. Rather, the debt must be reported in subsequent periods at amortized cost. The variance between the convertible debt's face value and the amount of proceeds that are allocated to the debt instrument, net of the amount allocated to the conversion feature, must be treated as a discount to be accreted using the effective yield method as additional interest expense. The accretion period is to be based on the expected term of a similar instrument lacking the conversion feature. The expected life is not subject to reassessment in later periods, unless there is a modification to the terms of the instrument. The equity component would not be reassessed either, unless it ceases to meet the criteria set forth in ASC 470, in which case the difference between the amount previously recognized in equity and the fair value of the conversion option at the date of the reclassification as a liability at fair value is to be accounted for as an adjustment to stockholders' equity.

ASC 470-50 provides guidance on derecognition of convertible obligations that can be settled in whole or in part for cash. It stipulates that the proceeds transferred to effect the extinguishment of the liability and the reacquisition of the associated conversion feature are to be allocated first to the extinguishment of the liability component equal to the fair value of that component immediately prior to extinguishment. Any difference between the consideration attributed to the liability component and the sum of (1) the net carrying amount of the liability component and (2) any unamortized debt issuance costs is to be recognized in the statement of financial performance as a gain or loss on debt extinguishment. Following this, any remaining settlement consideration is to be assigned to the reacquisition of the equity component, with recognition of that amount as a reduction of stockholders' equity. Any costs incurred (e.g., banker fees) are to be allocated pro rata to the debt and equity in proportion to the allocation of consideration transferred at settlement, and accounted for as debt extinguishment costs and equity reacquisition costs, respectively.

If an instrument within the scope of the above-described staff position is modified such that the conversion option no longer requires or permits cash settlement upon conversion, it is necessary to account for the components of the instrument separately, unless the original instrument is required to be derecognized under ASC 470-50. If an instrument is modified or exchanged in a manner that requires derecognition of the original instrument under ASC 470-50 and the new instrument is a convertible debt instrument that may not be settled in cash upon conversion, the new instrument would be subject to ASC 470-50.

On the other hand, if a convertible debt instrument is not at first subject to this guidance, but is later modified so as to become subject to it, then ASC 470-50 is to be applied to ascertain whether the original instrument is to be derecognized. If not, the issuer is to apply the guidance in this staff position prospectively from the date of the modification. In such a circumstance, the liability component is to be measured at its fair value as of the modification date, with the carrying amount of the equity component represented by the embedded conversion option to be determined by deducting the fair value of the liability component from the overall carrying amount of the convertible debt instrument as a whole. At the modification date, a portion of any unamortized debt issuance costs incurred previously is to be reclassified and accounted for as equity issuance costs based on the proportion of the overall carrying amount of the convertible debt instrument that is allocated to the equity component.

Finally, there is the matter of an induced conversion. If the terms of an instrument addressed by this staff position are revised to induce early conversion (e.g., by offering a more favorable conversion ratio or paying other additional consideration in the event of conversion before a specified date), then the entity is to recognize a loss equal to the fair value of all securities and other consideration transferred in the transaction in excess of the fair value of consideration issuable in accordance with the original conversion terms. The settlement accounting (derecognition) treatment described above is then to be applied using the fair value of the consideration that was issuable in accordance with the original conversion terms. Derecognition transactions in which the holder does not exercise the embedded conversion option are not affected, however.

Expanded disclosures have also been mandated by this staff position. As of each date for which a statement of financial position is presented, the reporting entity is to disclose the following:

- The carrying amount of the equity component

- The principal amount of the liability component, its unamortized discount, and its net carrying amount

As of the date of the most recent statement of financial position that is presented, the reporting entity must disclose the following:

- The remaining period over which any discount on the liability component will be amortized.

- The conversion price and the number of shares on which the aggregate consideration to be delivered upon conversion is determined.

- The amount by which the instrument's if-converted value exceeds its principal amount, regardless of whether the instrument is currently convertible. (This disclosure is required only for public entities.)

- Information about derivative transactions entered into in connection with the issuance of instruments within the scope of the staff position, including the terms of those derivative transactions, how those derivative transactions relate to the instruments within the scope of the staff position, the number of shares underlying the derivative transactions, and the reasons for entering into those derivative transactions. (An example of a derivative transaction entered into in connection with the issuance of an instrument within the scope of this staff position is the purchase of call options that are expected to substantially offset changes in the fair value of the conversion option.) This disclosure is required regardless of whether the related derivative transactions are accounted for as assets, liabilities, or equity instruments.

For each period for which a statement of financial performance is presented, the entity is to also disclose the following:

- The effective interest rate on the liability component for the period

- The amount of interest cost recognized for the period relating to both the contractual interest coupon and amortization of the discount on the liability component.

Own-share lending arrangements related to a convertible debt issuance.

An entity may enter into a share-lending arrangement with an investment bank, whereby it lends shares to the bank to facilitate investors' ability to hedge the conversion option in the entity's convertible debt issuance. The entity issues the share in exchange for a nominal loan processing fee; the investment bank returns the shares upon the maturity or conversion of the convertible debt.

In a share-lending arrangement, the entity issuing shares measures them at their fair value and recognizes them as a debt issuance cost, which offsets the additional paid-in capital account. If it subsequently becomes probable that the counterparty will default, then the entity recognizes an expense equaling the fair value of any unreturned shares on that date, minus the fair value of probable share recoveries, which offsets the additional paid-in capital account. The entity continues to remeasure the fair value of unreturned shares until the consideration payable by the counterparty becomes fixed.

An entity having an outstanding own-share lending program should disclose the following:

- Description of the arrangement.

- All significant terms of the arrangement, including the number of shares involved, the agreement term, any cash settlement terms, and any counterparty collateral requirements.

- The reason for entering into the arrangement.

- The fair value of loaned shares at the balance sheet date.

- The treatment of loaned shares in calculating earnings per share.

- Classification of any issuance costs.

- The unamortized amount of issuance costs, and the related interest cost for the reporting period.

- Any dividends paid on the loaned shares that will not be reimbursed.

- If the counterparty will probably default on the arrangement, the amount of expense related to the default that is reported in the statement of earnings. In subsequent periods, note any material changes in the amount of this expense.

Convertible Securities with Beneficial or Contingent Conversion Features

Beneficial conversion.

Reporting entities sometimes issue convertible securities (debt or preferred stock) that are “in the money” at the issuance date (i.e., where it would be economically advantageous to the holders if the securities were converted immediately). That type of conversion feature is called an “embedded beneficial conversion feature.” Variations of such securities may be converted at a fixed price, a fixed discount to the fair value at date of conversion, a variable discount to the fair value at conversion, or the conversion price may be dependent upon future events. In addition, the conversion feature can be exercisable at issuance, at a stated date in the future, or upon the happening of a future event (such as an IPO). ASC 470-20 addressed the assorted accounting issues arising for issuers of such securities (the reporting entity or debtor).

In contrast with GAAP governing convertible securities lacking this feature, embedded beneficial conversion features are valued separately at issuance. The feature is recognized as additional paid-in capital by allocating a portion of the proceeds equal to the intrinsic value of the feature. The intrinsic value is computed at the commitment date as (1) the difference between the conversion price and the fair value of the common stock (or other securities) into which the security is convertible, multiplied by (2) the number of shares into which the security is convertible.

For convertible debt securities, a discount on the debt may result from the allocation of a portion of the proceeds to the conversion feature. For convertible instruments that have a stated redemption date, a discount resulting from recording a beneficial conversion option shall be required to be amortized from the date of issuance to the stated redemption date of the convertible instrument, regardless of when the earliest conversion date occurs. For convertible instruments that do not have a stated redemption date, such as perpetual preferred stock, a discount resulting from the accounting for a beneficial conversion option is to be amortized from the date of issuance to the earliest conversion date.

If the conversion feature has multiple steps, the computation of the intrinsic value is made using the conversion terms most beneficial to the investor. For example, if the security was convertible at a 10% discount to fair value after three months and then at a 25% discount to fair value after one year, the 25% discount terms would be used to measure the intrinsic value of the feature. Any resulting discount on the convertible debt would be amortized to the earliest date at which the particular discount (25% in this case) could be achieved (one year). However, at any financial statement date, the cumulative amortization recorded must be the greater of (1) the amount computed using the effective interest method of amortization or (2) the amount of the benefit the investor would receive if the securities were converted at that date. If the securities are converted prior to the full amortization of the discount, the unamortized discount is to be included in the amount transferred to equity upon conversion.

If a convertible debt security having a beneficial feature is extinguished prior to conversion, a portion of the reacquisition price of the debt security is allocated to the beneficial conversion feature. That portion is measured as the intrinsic value of the conversion feature at the extinguishment date. Since the beneficial conversion feature was originally recognized as equity, the redemption or cancellation of this feature would give rise not to gain or loss, but rather to an adjustment within stockholders' equity. For example, if $2,000 of the redemption payment was identified with the beneficial feature to which $1,200 had originally been allocated, the net result would be that the original allocation would be eliminated and an $800 charge would be made against retained earnings (analogous to a loss on a treasury stock transaction). Any residual beyond the allocated cost of redeeming the beneficial conversion feature would be allocated to the retirement of the debt security, and a gain or loss on extinguishment would be reported in current earnings.

Contingent conversion.

If the security becomes convertible only upon occurrence (or failure to occur) of a future event outside the control of the investor, or if the conversion terms change based on the occurrence (or failure to occur) of a future event, the value of the contingent beneficial conversion feature should be measured as of the commitment date; but it is not recognized in the financial statements until the contingency is resolved. This may be combined with a beneficial conversion feature. For example, a debt instrument issued with a conversion feature at 20% below then-fair value, to become effective conditioned on the consummation of a planned refinancing, would be contingently convertible with a beneficial feature. According to ASC 470-20, any contingent beneficial conversion feature should be measured at the commitment date, but not reflected in earnings until the contingent condition has been met.

The definition of “conventional contingently convertible debt instrument” is later addressed by ASC 815-40-25. The issue arises because of one of the requirements under ASC 815—namely, that embedded derivatives be bifurcated and accounted for separately under certain conditions, but with an exception for accounting for conversion privileges by issuers of certain convertible securities. Thus, instruments that provide holders the right to convert at a fixed ratio (or equivalent cash value, at the issuer's discretion), for which option exercise is based on either the passage of time or a contingent event, are deemed “conventional.”

ASC 815-15 also states that, when a previously bifurcated conversion option in a convertible debt instrument no longer meets the bifurcation criteria in ASC 815, one should reclassify the fair value of the liability for the conversion option to shareholders' equity. If a debt discount was recognized when the conversion option was bifurcated, then it should continue to be amortized. Disclosure requirements include a description of the changes causing the termination of bifurcation, as well as the amount of the liability reclassified to stockholders' equity.

ASC 470-20 covers convertible securities with beneficial conversion features. The following summarizes this topic:

- If an instrument includes both detachable instruments (e.g., stock purchase warrants) and an embedded beneficial conversion option, the proceeds of issuance should first be allocated among the convertible instrument and the other detachable instruments based on their relative fair values. Then ASC 470-20-35 should be applied to determine the amount allocated to the convertible instrument if the embedded conversion option has an intrinsic value.

- If the conversion price could change upon the occurrence of a future event, assume that there are no changes to the current circumstances except the passage of time. Use the most favorable price that would be in effect if nothing were changed at the conversion date in order to measure the intrinsic value of an embedded conversion option. Changes to the conversion terms that are caused by future events not controlled by the issuer are recognized if and when the trigger event occurs.

- If there is no intrinsic value to a conversion right at issuance, but the conversion price resets after the commitment date and, upon reset, the conversion price is greater than the fair value of the underlying stock, the beneficial conversion amount is recognized when the reset occurs. The beneficial conversion amount is measured by the number of shares that will be issued upon conversion, multiplied by the decrease in price between the original conversion price and the reset price.

- The definition of commitment date for purposes of applying ASC 470-20 should be the same as the definition of a firm commitment in ASC 815. If an instrument includes both detachable instruments and an embedded beneficial conversion option, the commitment date should also be used when determining the relative fair values of all the instruments issued.

- If a convertible instrument has a stated redemption date, a discount resulting from recording a beneficial conversion option should be amortized from the date of issuance to the stated redemption date, regardless of when the earliest conversion occurs. If the instrument has beneficial conversion features, the unamortized discount remaining at the date of conversion should be immediately recognized as interest expense or as a dividend, as appropriate.

- If the terms of a contingent conversion option do not permit an issuer to compute the number of shares that the holder would receive upon conversion, the issuer should wait until the contingent event occurs and then compute the number of shares that would be received. The number of shares that would be received is compared to the number of shares that would have been received if the contingent event had not occurred to determine the excess number of shares. The number of excess shares multiplied by the stock price as of the commitment date equals the incremental intrinsic value that should be recognized.

- If an instrument includes a beneficial conversion option that expires at the end of a stated period and the instrument then becomes mandatorily redeemable at a premium, ASC 470-20 states that the proceeds of issuance were to be allocated between the debt and the embedded beneficial conversion features. The debt amount was then to be accreted to the redemption amount over the period to the required redemption date. ASC 480, however, requires that mandatorily redeemable stock be classified as a liability, measured initially at fair value, with a corresponding decrease to equity and no gain or loss recognized. Thus, this situation is no longer governed by ASC 470-20.

- If interest or dividends are paid in kind, the commitment date for the paid-in-kind securities is the commitment date for the original instrument if the payment in kind is not discretionary. The payment is not discretionary (1) if neither the issuer nor the holder can elect other forms of payment for the interest or dividends and (2) if the original instrument is converted before dividends are declared or interest is accrued, the holder will always receive the number of shares as if all dividends or interest have been paid in kind (ASC 470-20-30-17). If the payment in kind is discretionary, the commitment date for the paid-in-kind securities is the date that the interest is accrued or the dividends are declared.

- If an issuer issues a convertible instrument as repayment of a nonconvertible instrument, the fair value of the newly issued convertible instrument equals the redemption amount owed at the maturity date of the old debt. That is, the carrying amount of the old debt is the proceeds received for applying ASC 470-20 to the new debt.

Several tentative conclusions were also expressed, but have not been resolved.

- If a convertible instrument is extinguished prior to its maturity date, no portion of the reacquisition price should be allocated to the conversion option if that option had no intrinsic value at the issuance date.

- The intrinsic value of a conversion feature at an early extinguishment date of convertible debt is recorded as a decrease in additional paid-in capital, which may result in a reduction in additional paid-in capital that is larger than the amount originally recorded in paid-in capital at issuance.

- If an entity redeems convertible preferred stock with a beneficial conversion feature, the intrinsic value of the conversion feature that was recorded at issuance is reversed, and the remaining reacquisition price is allocated to the reacquisition of the stock. Any excess of that portion over the carrying amount of the stock is an adjustment to earnings available to common shareholders.

- If a company issues a warrant that allows the holder to acquire a convertible instrument for a stated price and that warrant is classified as equity, the date used to measure the intrinsic value of the conversion option is the commitment date for the warrant, not its exercise date, provided that the issuer received fair value for the warrant when issued. The deemed proceeds for determining whether a beneficial conversion option exists are equal to the sum of the proceeds received for the warrant and the exercise price of the warrant. If that sum is less than the fair value of the common stock that would be received upon exercise of the convertible instrument that would be obtained upon exercise of the warrant, the excess represents a deemed distribution to the holder of the warrant, which is to be recognized over the life of the warrant. The deemed distribution is limited to the proceeds received for the warrant; that is, if the deemed distribution is larger than the proceeds received, the difference is not recognized until the warrant is exercised. If the issuer received less than fair value for the warrant upon issuance, the exercise date of the warrant should be used to measure the intrinsic value of the conversion option.

- If a company issues a warrant that allows the holder to acquire a convertible instrument for a stated price and that warrant is classified as a liability, the date used to measure the intrinsic value of the conversion option is the exercise date for the warrant, not its commitment date. The deemed proceeds for determining whether a beneficial conversion option exists are equal to the sum of the fair value of the warrant on the exercise date and the exercise price of the warrant.

- If a conversion feature permits the holder to receive both common stock and warrants to acquire common stock, the intrinsic value of the conversion option is measured as the difference between (1) the proceeds allocated to the common stock portion of the conversion feature and (2) the fair value at the commitment date of the common stock to be received by the holder upon conversion.

The guidance in ASC 470-20 should be used to evaluate whether the issuer controls settlement of the conversion feature of convertible preferred stock. If the issuer does not control settlement, the convertible preferred stock is considered temporary equity.

Software Solutions issues $1,000,000 of convertible debt, which is convertible into $10 par common stock at a price of $50 per share. The fair value of the common stock on the commitment date of the issue is $60. The intrinsic value of the conversion feature is computed as follows:

![]()

Software Solutions would make the following entry to recognize the issuance of the bonds at 100:

If the price at which the bond is convertible to stock changes over the life of the bond, the intrinsic value should be computed using the terms that are most beneficial to the holder. The most favorable conversion price that would be in effect, assuming that there are no changes to the current circumstances except for the passing of time, should be used to measure the intrinsic value.