AUDIT COMPLETION/REPORTING (STUDY OBJECTIVE 10)

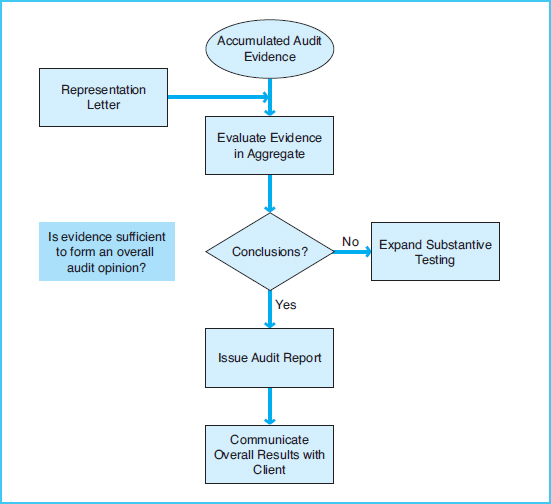

After the tests of controls and substantive audit tests have been completed, auditors evaluate all the evidence that has been accumulated and draw conclusions based on this evidence. This phase is the audit completion/reporting phase. The processes within this final phase of the audit are presented in Exhibit 7-10.

In forming a conclusion, auditors must consider whether the evidence supports the information presented. All of the evidence from all phases of the audit and covering all types of accounts and transactions must be considered collectively so that the auditors can make an overall decision on the fairness of the information. The auditors must also consider whether the extent of testing has been adequate in light of the risks and controls identified during the planning phase versus the results of procedures performed in the testing phases.

The completion phase includes many tasks that are needed to wrap up the audit. For many types of audits, the most important task is obtaining a letter of representations from company management. The letter of representations is often considered the most significant single piece of audit evidence, because it is a signed acknowledgment of management's responsibility for the reported information. In this letter, management must declare that it has provided complete and accurate information to its auditors during all phases of the audit.

For a financial statement audit, when the auditors are satisfied with the extent of testing and a representations letter has been obtained from the client, an audit report must be issued. The audit report expresses the auditors' overall opinion of the financial statements. There are four basic types of reports that could be issued:

Exhibit 7-10 Audit Completion/Reporting Phase Process Map

- Unqualified opinion, which states that the auditors believe the financial statements are fairly and consistently presented in accordance with GAAP or IFRS

- Qualified opinion, which identifies certain exceptions to an unqualified opinion

- Adverse opinion, which notes that there are material misstatements presented

- Disclaimer, which states that the auditors are unable to reach a conclusion.

When reporting on the effectiveness of internal controls auditors must choose between an unqualified, adverse, or disclaimer opinion. Communication is key to the proper conclusion of an audit. In addition to management communicating information in the representations letter and auditors issuing the audit report, auditors must discuss the overall results of the audit with the company's directors.