END OF CHAPTER MATERIAL

CONCEPT CHECK

- 1. Within the purchasing processes, which of the following is the first document prepared and thereby the one that triggers the remaining purchasing processes?

- The invoice

- The receiving report

- The purchase order

- The purchase requisition

- 2. Personnel who work in the receiving area should complete all of the following processes except

- counting the goods received

- inspecting goods received for damage

- preparing a receiving report

- preparing an invoice

- 3. Which of the given departments will immediately adjust the vendor account for each purchase transaction so that the company will know the correct amount owed to the vendor?

- Purchasing

- Receiving

- Accounts payable

- Shipping

- 4. One of the most critical controls to prevent theft of inventory purchased is to

- require authorization of the purchase requisition

- segregate inventory custody from inventory record keeping

- compare the purchase order, receiving report, and invoice

- segregate the authorization of purchases from the inventory record keeping

- 5. Internal control is strengthened by the use of a blind purchase order, upon which the quantity of goods ordered is intentionally left blank. This blind copy is used in which department?

- The department that initiated the purchase request

- The receiving department

- The purchasing department

- The accounts payable department

- 6. Which of the following questions would most likely be included in an internal control questionnaire concerning the completeness of purchase transactions?

- Is an authorized purchase order required before the receiving department can accept a shipment or the accounts payable department can record a voucher?

- Are prenumbered purchase requisitions used, and are they subsequently matched with vendor invoices?

- Is there a regular reconciliation of the inventory records with the file of unpaid vouchers?

- Are prenumbered purchase orders, receiving reports, and vouchers used, and are the entire sequences accounted for?

- 7. Which of the following controls is not normally performed in the accounts payable department?

- The vendor's invoice is matched with the related receiving report.

- Vendor invoices are selected for payment.

- Asset and expense accounts to be recorded are assigned.

- Unused purchase orders and receiving reports are accounted for.

- 8. In a system of proper internal controls, the same employee should not be allowed to

- sign checks and cancel the supporting voucher package

- receive goods and prepare the related receiving report

- prepare voucher packages and sign checks

- initiate purchase requisitions and inspect goods received

- 9. The document prepared when purchased items are returned is a(n)

- debit memo

- invoice

- receiving report

- sales journal

- 10. Within cash disbursements, all of the following should be true before a check is prepared, except that

- The purchase order, receiving report, and invoice have been matched

- The purchased goods have been used

- Sufficient cash is available

- The invoice discount date or due date is imminent

- 11. A manager suspects that certain employees are ordering merchandise for themselves over the Internet without recording the purchase or receipt of the merchandise. When vendors' invoices arrive, one of the employees approves the invoices for payment. After the invoices are paid, the employee destroys the invoices and related vouchers. To trace whether this is actually happening, it would be best to begin tracing from the

- cash disbursements

- approved vouchers

- receiving reports

- vendors' invoices

- 12. Within accounts payable, to ensure that each voucher is submitted and paid only once, each invoice approved to be paid should be

- supported by a receiving report

- stamped “paid” by the check signer

- prenumbered and accounted for

- approved for authorized purchases

- 13. For proper segregation of duties in cash disbursements, the person who signs checks also

- reviews the monthly bank reconciliation

- returns the checks to accounts payable

- is denied access to the supporting documents

- is responsible for mailing the checks

- 14. Which of the following internal controls would help prevent overpayment to a vendor or duplicate payment to a vendor?

- Review and cancellation of supporting documents after issuing payment

- Requiring the check signer to mail the payment directly to the vendor

- Review of the accounts where the expenditure transaction has been recorded

- Approving the purchase before the goods are ordered from the vendor

- 15. Which of the following is not an independent verification related to cash disbursements?

- The cash disbursements journal is reconciled to the general ledger.

- The stock of unused checks should be adequately secured and controlled.

- The bank statement is reconciled on a monthly basis.

- The accounts payable subsidiary ledger is reconciled to the general ledger.

- 16. Which of the following IT systems is designed to avoid the document matching process and is an “invoiceless” system?

- Computer-based matching system

- Electronic data interchange

- Evaluated receipt settlement

- Microsoft Dynamics®

- 17. Input controls such as field check, validity check, limit check, and reasonableness check are useful in IT systems of purchasing processes to lessen which of the following risks?

- Unauthorized access

- Invalid data entered by vendors

- Repudiation of purchase transactions

- Virus and worm attacks

- 18. Which of the following is most likely to be effective in deterring fraud by upper-level managers?

- Internal controls

- An enforced code of ethics

- Matching documents prior to payment

- Segregating custody of inventory from inventory record keeping

DISCUSSION QUESTIONS

- 19. (SO 2) Name the first document that should be prepared when a production employee recognizes that the quantity of goods on hand is insufficient to meet customer demand.

- 20. (SO 2) How does the maintenance of a receiving log enhance internal controls?

- 21. (SO 2) Why should a receiving clerk be denied access to information on a purchase order?

- 22. (SO 2) Under what circumstances would it be necessary to manually update accounts payable prior to the receipt of a vendor's invoice?

- 23. (SO 4) Which department is responsible for making sure that payments are made in time to take advantage of vendor discounts?

- 24. (SO 4) Why would some checks need to include two signatures?

- 25. (SO 4) During the process of reconciling the bank account, why is it necessary to review the dates, payees, and signatures on the canceled checks?

- 26. (SO 4, 6) What specifically does a cash disbursements clerk do when he or she “cancels” an invoice? How does this compare with the procedures followed when computer-based matching in the system is utilized?

- 27. (SO 4) Why should accountants periodically review the sequence of checks issued?

- 28. (SO 2,4) What accounting records are used by accounts payable personnel to keep track of amounts owed to each vendor?

- 29. (SO 5) Identify some inefficiencies inherent in a manual expenditures processing system.

- 30. (SO 5) What are the advantages of BPR?

- 31. (SO 5,6,7,8) List three examples of BPR used in the expenditures processes.

- 32. (SO 6) Explain how system logic errors could cause cash management problems.

- 33. (SO 6) Explain how system availability problems could cause cash management problems.

- 34. (SO 8) How is an audit trail maintained in an IT system where no paper documents are generated?

- 35. (SO 6) What can a company do to protect itself from business interruptions due to power outages?

- 36. (SO 7) What paper document is eliminated when ERS is used?

- 37. (SO 7) Identify compensating controls needed for an effective ERS system.

- 38. (SO 5) What is typically the most time-consuming aspect of the expenditures process?

- 39. (SO 8) Identify each category of risk that can be reduced by using authority tables, computer logs, passwords, and firewalls.

- 40. (SO 6) Explain why the availability of computer systems in the receiving department is such an important component of an automated expenditures process.

- 41. (SO 5,8) Identify three ways that buyers and sellers may be linked electronically.

- 42. (SO 8) What techniques can a company use to reveal problems concerning potential exposure to unauthorized access to its systems?

- 43. (SO 9) How are Web browsers used in e-payables systems?

- 44. (SO 10) Explain how procurement cards provide for increased efficiencies in the accounts payable department.

BRIEF EXERCISES

- 45. (SO 2,4) Describe what is likely to occur if company personnel erroneously recorded a purchase transaction for the wrong vendor. What if a cash disbursement were posted to the wrong vendor? Identify internal controls that would detect or prevent this from occurring.

- 46. (SO 4) Debate the logic used in the following statement: “The person responsible for approving cash disbursements should also prepare the bank reconciliation because he is most familiar with the checks that have been written on that bank account.”

- 47. (SO 8) Expenditures systems are crucial in the automobile manufacturing industry, where hundreds or thousands of parts must be purchased to manufacture cars. Briefly describe how EDI would be beneficial in this industry.

- 48. (SO 2,4) Describe how the matching of key information on supporting documents can help a company determine whether purchase transactions have been properly executed.

- 49. (SO 2,3) Describe how the use of prenumbered forms for debit memos can help a company ascertain that purchase return transactions have not been omitted from the accounting records.

- 50. (SO 5,7) Describe how an ERS system could improve the efficiency of expenditures processes.

- 51. (SO 10) Describe how a procurement card improves the efficiency of purchasing supplies.

PROBLEMS

- 52. (SO 2,3,4) Identify an internal control procedure that would reduce the following risks in a manual system:

- The purchasing department may not be notified when goods need to be purchased.

- Accounts payable may not be updated for items received.

- Purchase orders may be prepared on the basis of unauthorized requisitions.

- Receiving clerks may steal purchased goods.

- Payments may be made for items not received.

- Amounts paid may be applied to the wrong vendor account.

- Payments may be made for items previously returned.

- Receiving clerks may accept delivery of goods in excess of quantities ordered.

- Duplicate payments may be issued for a single purchase transaction.

- 53. (SO 1,10) Chris Smith started a new business, a coffee and pastry cart located at the local library. Chris hired her brother, Pat, as her assistant. Chris and Pat personally make all the purchases of items needed to stock the cart, using procurement cards issued in the name of the company. Because Chris is personally liable for payments made on the procurement cards, she recognizes the need to establish policies for her brother to follow for the use of this card. Suggest some controls that should be in place. Identify some resources that need to be purchased for this business.

- 54. (SO 1,5) Thurston Company is considering a business process reengineering (BPR) project whereby its current (mostly manual) expenditures processing would be converted to an automated system. Brainstorm ideas for this project. Specifically, what processes could be redesigned? What current IT developments should Thurston consider implementing? You may find it helpful to use the Internet to locate information on BPR related to the expenditures process.

- 55. (SO 2,4) The following list presents statements regarding the expenditures processes. Each statement is separate and should be considered to be from a separate company. Determine whether each statement is an internal control strength or weakness; then describe why it is a strength or weakness. If it is an internal control weakness, provide a method or methods to improve the internal control.

- A purchasing agent updates the inventory subsidiary ledger when an order is placed.

- An employee in accounts payable maintains the accounts payable subsidiary ledger.

- Purchasing agents purchase items only if they have received an approved purchase requisition.

- The receiving dock employee counts and inspects goods and prepares a receiving document that is forwarded to accounts payable.

- The receiving dock employee compares the packing list with the goods received and if they match, forwards the packing list to accounts payable.

- An employee in accounts payable matches an invoice to a receiving report before approving a payment of the invoice.

- A check is prepared in the accounts payable department when the invoice is received.

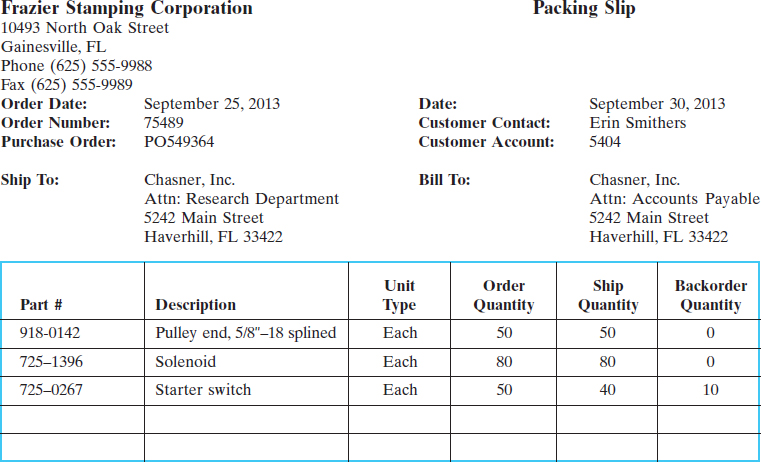

56. (SO 2) The following figure shows a packing list received by Chasner, Inc. When a packing slip arrives at the receiving dock with a shipment, a worker prepares a receiving report. The receiving report triggers the process for payment in accounts payable.

56. (SO 2) The following figure shows a packing list received by Chasner, Inc. When a packing slip arrives at the receiving dock with a shipment, a worker prepares a receiving report. The receiving report triggers the process for payment in accounts payable.

Required:

Assume that Chasner, Inc., is preparing to computerize the manual input processes such as completing a receiving report. Use Microsoft Excel to design an appropriate format for a data entry screen that could be used at the receiving dock to enter information from the packing slip in the company's expenditures system.

- 57. (SO 4) Since the accounts payable system of matching purchase orders, invoices, and receiving reports can often be complex, organizations must routinely check to ensure that they are not making a duplicate payment. The textbook website contains a spreadsheet titled “invoices.xls.” Using your knowledge of spreadsheets and the characteristics of duplicate payments, identify any payments within the spreadsheet that appear to be duplicate or problem payments.

- 58. (SO 8) Volpner Manufacturing Company operates two plants that manufacture shelves and display units for retail stores. To manufacture these items, the purchasing agents purchase raw materials such as steel, aluminum, plastic, lexan, and miscellaneous screws, rubber end caps, bolts, and nuts. Two purchasing agents work at the first, and original, plant location. They do all the purchasing for both plants, which are located in Milwaukee, Wisconsin. Each purchasing agent has a PC that is connected to a company network consisting of a server at the first plant and PCs in both plants. The company has always used mailed purchase orders to purchase items, but they are now considering the installation of an internet EDI system to place purchases.

Required:

Describe the IT controls that Volpner should include when it implements an internet EDI system. For each control you suggest, describe the intended purpose of the control.

- 59. (SO 2,3,4) Zifner, Inc., is a small company with three people working in the expenditures processes. One of the three employees is the supervisor of the other two. Some tasks that must be accomplished within the expenditures processes are the following:

- Accounts payable record keeping

- Authorization of new vendors

- Authorization of purchase returns

- Authorization of purchases

- Cash disbursements record keeping

- Check-signing authority

- Custody of inventory in the receiving area

- Maintaining custody of cash

- Preparation of a debit memo for a purchase return

Required:

Consider the duties you would assign to each of the three employees (supervisor, employee 1, and employee 2). No employee should have more than three tasks, and there should be a proper separation of duties to achieve appropriate internal control. List the three people, the duties you assigned to each, and a description of why those assignments should achieve proper separation of duties.

- 60. (SO 7) Using a search engine, search the Internet for information about evaluated receipt settlement, or ERS. You may have more success searching for the terms “ERS” and “invoices” together in one search. From what you read about ERS on the Web, what do you think appear to be the difficulties encountered when a company chooses to implement ERS?

- 61. (SO 9) Using a search engine, search the Internet for information about electronic invoice presentment and payment. You may have more success searching for the terms “EIPP” and “invoices” together in one search. On some websites, it may be called EIP rather than EIPP. From what you read about EIPP on the Web, what would you say are the advantages and disadvantages of EIPP? One of the concepts about EIPP is that it should benefit both the buying company and the selling company. What do you think the benefits are to the buyer and to the seller?

- 62. (SO 9) Using a search engine, search the Internet for an article titled “B2B EIPP: The Mystery Unraveled.” Briefly describe what the article calls “customer advantages” of adopting EIPP.

63. (SO 11) Suppose you are an accounts payable clerk for a small home improvements contractor. This morning one of the site supervisors submitted an invoice requesting immediate payment to a new vendor for items he claims were delivered directly to a work site. The supervisor attached a note to the invoice asking that the check be returned to him upon issuance so that he could personally deliver it to the vendor. This would ensure the timeliness of future deliveries. He claims that unless the payment is made immediately, there will be delivery delays on items needed to complete this job, as well as delays on items for another contract in progress. Although you are suspicious of this unusual request, you are tempted to accommodate it. You know that timely completion and collection on these contracts is critical to the company's production scheduling and cash management. Moreover, the company president is on vacation and therefore not available to grant special authorization for this payment. Speculate on the type of fraud that could be in process here. What (if anything) could you do to ascertain the propriety of the transaction and still make the payment today?

63. (SO 11) Suppose you are an accounts payable clerk for a small home improvements contractor. This morning one of the site supervisors submitted an invoice requesting immediate payment to a new vendor for items he claims were delivered directly to a work site. The supervisor attached a note to the invoice asking that the check be returned to him upon issuance so that he could personally deliver it to the vendor. This would ensure the timeliness of future deliveries. He claims that unless the payment is made immediately, there will be delivery delays on items needed to complete this job, as well as delays on items for another contract in progress. Although you are suspicious of this unusual request, you are tempted to accommodate it. You know that timely completion and collection on these contracts is critical to the company's production scheduling and cash management. Moreover, the company president is on vacation and therefore not available to grant special authorization for this payment. Speculate on the type of fraud that could be in process here. What (if anything) could you do to ascertain the propriety of the transaction and still make the payment today?- 64. (SO 11) Two of the most common ways that employees commit fraud against their employers is the misstatement of reimbursable expense accounts and the misuse of office supplies for personal purposes. Although these schemes are usually not individually significant, their magnitude can be damaging if these practices are widespread. Develop suggestions for internal controls that could curb the occurrence of such fraudulent activities.

CASES

- 65. Kludney Incorporated has the following processes related to purchasing: When it is determined that an item should be ordered, the purchasing department prepares a three-copy purchase order. The first copy is mailed to the vendor, the second copy is filed by PO number in the purchasing department, and the third copy is forwarded to inventory control. Inventory control updates the inventory ledger with the quantities that were ordered and files the purchase order copy by date.

When ordered items arrive at the receiving dock, the packing slip is inspected and a two-copy receiving report is prepared. The first copy is forwarded to the purchasing department, where it is filed with the purchase order. The second copy is filed in the receiving department by date. The packing slip is forwarded to the accounts payable department.

Vendors mail invoices directly to the accounts payable department. The accounts payable department reviews the invoice and related packing slip, prepares a cash disbursement voucher, updates the accounts payable ledger, and files the invoice by date. The cash disbursement voucher is forwarded to the cash disbursements department. The packing slip is returned to the receiving department. The cash disbursements department prepares a twocopy check, mails the first copy to the vendor, and forwards the second copy to the general ledger department. The cash disbursement voucher is forwarded to the accounts payable department where it is filed with the invoice.

The general ledger department updates the general ledger accounts, using the second copy of the check, and then forwards the check copy to cash disbursements to be filed by check number.

Required:

- Draw a document flowchart of the purchase processes of Kludney.

- Identify any weaknesses in internal controls within the purchase processes and indicate the improvements you would suggest.

- 66. Jounta Enterprises is a wholesaler that purchases consumer merchandise from many different suppliers. Jounta then sells this merchandise to many different retail chain stores. The following paragraphs describe the expenditures processes at Jounta:

Warehouse employees constantly monitor the level of each merchandise item by assessing how many remaining boxes of items are on warehouse shelves. When a warehouse worker sees the need to order a particular product, he fills out a postcard-size order requisition form with the product name and item number. The number is Jounta's item number.

When the purchasing department receives a requisition from the warehouse employee, a buyer looks up the last purchase of that item and completes a purchase order to buy the item from that vendor. The manager of the purchasing department approves the purchase order before it is mailed to the vendor. One copy of the purchase order is mailed to the vendor, one copy is filed in the purchasing department, one copy is forwarded to the receiving department, and one copy is forwarded to the accounts payable department.

When the receiving department receives an order, it compares the packing slip with the purchase order. If no purchase order exists, the item is returned to the vendor. A receiving report is prepared for the number of items indicated on the packing slip. One copy of the receiving report is filed in the receiving department, one copy is forwarded to the purchasing department, and one copy is forwarded to the accounts payable department. Items received are then transported to the warehouse.

When the accounts payable department receives an invoice from the vendor, an employee in the accounts payable department compares the purchase order, receiving report, and invoice. If the three documents match correctly, a cash disbursement voucher is prepared. If it does not match, the employee contacts the vendor to try to reconcile the differences. The cash disbursement voucher is reviewed by the manager of the accounts payable department. If it appears correct to her, she writes a check and forwards the check to the treasurer to be signed and mailed to the vendor.

Required:

- List any strengths and weaknesses in the internal control procedures of Jounta Enterprises.

- Draw a document flowchart of the expenditure processes.

- Describe any benefits that Jounta may receive by installing a newer, IT system to process purchases, goods received, accounts payable, and checks. Be specific as to how IT systems could benefit each of the processes described.

- 67. Crandolf Metals, Inc., is a manufacturer of aluminum cans for the beverage industry. Crandolf purchases aluminum and other raw materials from several vendors. The purchasing process at Crandolf occurs as follows:

When inventory of any raw material seems low, a purchasing agent examines the records to determine the vendor who supplied the last purchase of that raw material. The purchasing agent prepares a three-copy purchase order and mails the top copy to the vendor. One copy is filed in the purchasing department, and one copy is forwarded to the inventory control department (inventory record keeping). Inventory control personnel update the inventory subsidiary ledger and file the purchase order by number in the inventory control files.

When the goods arrive at the receiving dock, a receiving report is prepared from information on the packing slip. One copy of the receiving report is filed in the receiving department, and one copy is forwarded to purchasing so that the purchasing department is informed of the receipt of goods.

The vendor mails an invoice for the raw materials directly to the accounts payable department. When the invoice is received, accounts payable personnel prepare a cash disbursement voucher to approve payment. The voucher is forwarded to the cash disbursements department. The accounts payable department also updates the accounts payable subsidiary ledger and files the invoice by invoice number.

Upon receiving the cash disbursement voucher, an employee in the cash disbursements department prepares a two-copy check. The top copy of the check is mailed to the vendor, and the second copy is forwarded to the general ledger department. The cash disbursement voucher is stamped “paid” and returned to the accounts payable department. The voucher is filed with the invoice in the accounts payable department.

The general ledger department records the check in the general ledger and returns the check copy to the cash disbursements department, where it is filed.

Required:

- Draw two process maps to reflect the business processes at Crandolf. One process map should depict the purchasing processes, and the second process map should depict the cash disbursements processes.

- Draw two document flowcharts to reflect the records and reports used by these processes at Crandolf. One flowchart should depict the purchasing processes, and the second flowchart should depict the cash disbursements processes.

- Describe any weaknesses in these processes or internal controls. As you identify weaknesses, also describe your suggested improvements.

- Draw two new process maps that include your suggested improvements. One process map should depict the purchasing processes, and the second process map should depict the cash disbursement processes.

- 68. The United States General Accounting Office (GAO) Office of Special Investigations was responsible for investigating a potential purchase fraud case. The man who allegedly committed the fraud was Mark J. Krenik, a former civilian employee of the U.S. Air Force.

Mr. Krenik was the Air Force's technical representative on contracts with Hughes STX. Hughes STX provided hardware, software maintenance, technical support, and training to the Air Force. Part of Mr. Krenik's alleged fraud included opening accounts under his control at banks in Maryland. The accounts were opened under the names Hughes STX and ST Systems Corporation. A section of the GAO report on this fraud investigation reads as follows:3

On December 15, 1992, Mr. Krenik opened post office box 215 in Vienna, Virginia, in his own name. On December 24, 1992, Mr. Krenik delivered to the Air Force Finance Office 11 bogus invoices totaling $504,941.19. Accompanying the invoices were the respective DD-250s, on which Mr. Krenik had falsely certified that work had been performed and deliveries made. Special instructions on the invoices directed that payments be remitted to ST Systems Corporation at the Vienna, Virginia post office box.

Mr. Krenik deposited the checks in the accounts he controlled at the Maryland banks. His fraud was unsuccessful because bank employees became suspicious when he tried to withdraw large sums from the accounts.

Required:

Describe internal controls that should have been in place at the Air Force to help prevent such fraud.

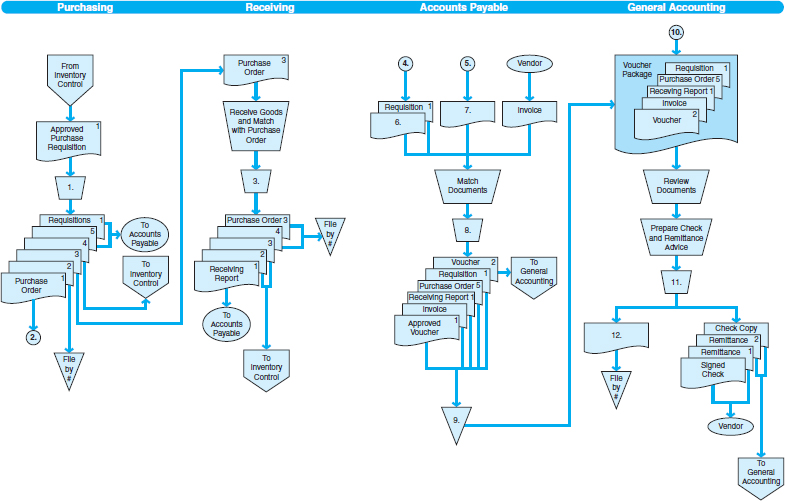

- 69. The document flowchart given next shows part of the purchasing and cash disbursement processes for Roufler, Inc., a small manufacturer of gadgets and widgets. Some of the flowchart symbols are labeled to indicate operations, controls, and records.

Required:

For each of the symbols in the flowchart (numbered 1 through 12), select one response (lettered A through T) from the answer lists. Each response may be selected once or not at all.

| Operations and controls: | Connectors, documents, departments, and files: |

| A. Approve receiving report | K. Canceled voucher package |

| B. Prepare and approve voucher | L. From Purchasing |

| C. Prepare purchase order | M. From Receiving |

| D. Prepare purchase requisition | N. From Accounts Payable |

| E. Prepare purchases journal | O. Purchase order no. 5 |

| F. Prepare receiving report | P. Receiving report no. 1 |

| G. Prepare sales journal | Q. Inventory Control |

| H. Prepare voucher package | R. To vendor |

| I. Sign check and cancel voucher package | S. Treasurer |

| J. Accounts Payable | T. Unpaid voucher file |

(Excerpt from Adapted CPA Simulation Problem)

CONTINUING CASE: ROBATELLI'S PIZZERIA

Reread the continuing case on Robatelli's Pizzeria at the end of Chapter 1. Consider the following issues that relate to Robatelli's purchases of ingredients and supplies, then answer the questions pertaining to its expenditure processes.

As mentioned in the opening part of the Robatelli's Pizzeria case, there are now 53 locations throughout the greater Pittsburgh area. Each one of those restaurant locations needs an ongoing supply of the many ingredients of pizzas and the other foods served. The raw materials each restaurant needs to make and sell pizzas and other menu items are things such as flour, salt, sugar, tomatoes, potatoes, lettuce, tomato paste, spices, meats, cheeses, and buns, as well as supplies such as napkins, take-out packages and doggy-bag containers.

Each restaurant must maintain an inventory of all of these items in order to properly serve customers. However, it is a difficult balance to maintain the right amount of each of these items. As you know from your experience in eating at restaurants, it can leave a negative impression in your mind if the restaurant has run out of the food you intended to order. Thus, there must always be enough ingredients and supplies to meet customers' desires.

Two factors make it difficult to maintain enough inventory of food and supplies: predicting demand, and time or space limitations. First, it can be difficult to predict customer demand for any particular day or week. The less predictable the stream of customers eating at the restaurant, the harder it can be to know how much inventory of food and supplies to keep. Secondly, time and space limit the amount of inventory a restaurant can keep. Food inventory is perishable, and much of it has a very short shelf life. For example, lettuce and tomatoes may remain fresh for only a couple of days. Other food items, such as flour and salt, may remain usable for months. But even for items with a long shelf life, it is hard to keep a large inventory at a restaurant because of limited storage space. Most of the space in a restaurant is for customer dining and the kitchen.

Robatelli's uses a central commissary to prepare some of the ingredients before they are shipped to the restaurant. For example, the individual restaurant locations do not make dough on the premises. The flour, salt, yeast, and other ingredients are maintained, mixed, and prepared at the commissary, and this premade dough is then shipped by truck to restaurants daily. The pizza sauce and many ingredients for sandwiches and salads are also premade at the commissary.

All of these factors taken together mean that Robatelli's must continually be purchasing the ingredients for pizzas and other foods, and supplies. These inventory items must be delivered to the commissary and then to each of the 49 Robatelli's locations to ensure that they never run out of the items needed to serve customers. Since there is a short shelf life for much of the inventory, the purchasing takes place on a daily basis to keep the commissary and each restaurant location properly stocked.

Required:

- Describe how you believe an efficient and effective purchasing system should be organized at Robatelli's. Consider details such as the following:

- How many purchasing agents should be employed?

- Where will these purchasing agents be located?

- How will the necessary information for purchasing flow between restaurants and these purchasing agents?

- How will IT systems be used in purchasing?

- How and when will purchased items be delivered to the restaurants? (Remember that all 49 locations are within the Pittsburgh area, and none would be more than a one-hour drive from the corporate Headquarters.)

- Draw a process map of your proposed purchasing system.

- Describe any IT controls that would be necessary or desirable in your purchasing system.

SOLUTIONS TO CONCEPT CHECK

- (SO 2) Within the purchasing processes, the first document prepared, and thereby the one that triggers the remaining purchasing processes, is d. the purchase requisition. When a determination has been made that more supplies or inventory must be purchased, a purchase requisition is prepared and then forwarded to other departments to begin the purchasing processes.

- (SO 2) Personnel who work in the receiving area should complete all of the following processes except d. preparing an invoice. When goods arrive at the receiving department, workers should inspect the goods for damage, count the goods, and prepare a receiving report. The invoice is prepared by the vendor.

- (SO 2) The department that will immediately adjust the vendor account for each purchase transaction so that the company will know the correct amount owed to the vendor is c. accounts payable. Accounts payable maintains records of the amounts owed to vendors, in the form of an accounts payable subsidiary ledger. When purchase transactions occur, accounts payable should update the accounts payable subsidiary ledger to show the new amount owed to the vendor.

- (SO 2) One of the most critical controls to prevent theft of inventory purchased is to b. segregate inventory custody from inventory record keeping. Each of the remaining options are good internal controls, but not all of them help deter theft of inventory. The best control to prevent theft of inventory is to segregate custody from record keeping. Segregating these makes it much more difficult for a person to steal inventory and alter inventory records.

- (CPA Adapted) (SO 2) Internal control is strengthened by the use of a blind purchase order, upon which the quantity of goods ordered is intentionally left blank. This blind copy is used in b. the receiving department. This control allows the goods to be independently inspected and counted upon receipt. Receiving department employees must actually count the goods rather than just check off an amount. Each of the other options are for departments that need to know the quantity of goods in order to complete their responsibilities.

- (CPA Adapted) (SO 2) The following question would most likely be included in an internal control questionnaire concerning the completeness of purchasing transactions: d. Are prenumbered purchase orders, receiving reports, and vouchers used, and are the entire sequences accounted for? Accounting for an entire sequence of prenumbered documents provides preventive control against record omissions. In other words, it helps ensure the completeness of the records. Option a. is incorrect because it is concerned with the assertion regarding authorization. Although options b. and c. each have some relevance to the completeness assertion, b. is not the best response because purchase requisitions may not always result in a purchase transactions (rather, purchase orders and receiving reports are better indicators that a purchase transaction occurred) and c. is incorrect because vouchers represent purchase transactions that should have already been recorded; accordingly, this control would be more likely to address completeness of the inventory records.

- (CPA Adapted) (SO 2,4) The following control is not normally performed in the accounts payable department: d. Unused purchase orders and receiving reports are accounted for. In order to enhance the effectiveness of internal controls via segregation of duties, this task is normally performed by an employee who does not have access to the accounts payable records. This prevents the opportunity to create a fictitious purchase transaction and record it in the company's accounting records. Each of the other options represent accounts payable department tasks.

- (CPA Adapted) (SO 2,4) In a system of proper internal controls, the same employee should not be allowed to c. prepare voucher packages and sign checks. This violates the segregation of duties principles in that it would permit record keeping (preparation of voucher packages) and custody (check-signing authority) functions to be carried out by the same employee. Each of the other options represents tasks that ARE typically performed by the same employee or within the same department.

- (SO 3) The document prepared when purchased items are returned is the a. debit memo. When purchased items are to be returned, a debit memo is prepared. An invoice is prepared by the vendor. A receiving report is prepared when purchased goods are received. A sales journal is part of the revenue processes, not the purchasing processes.

- (SO 4) Within cash disbursements, all of the given statements should be true before a check is prepared, except for b. The purchased goods have been used. Prior to approving payment for purchased goods, the processes in the company should ensure that the purchase order, receiving report, and invoice have been matched; sufficient cash is available; and either the invoice due date or discount date warrants payment. A company could not wait until the goods are used to pay, since vendors want payment upon the due date.

- (CPA Adapted) (SO 4) A manger suspects that certain employees are ordering merchandise for themselves over the Internet without recording the purchase or receipt of the merchandise. When vendor's invoices arrive, one of the employees approves the invoices for payment. After the invoices are paid, the employee destroys the invoices and related vouchers. To trace whether this is actually happening, it would be best to begin tracing from the a. cash disbursements. The record of payment would be the only option for possibly uncovering this scheme. Since these fraudsters are not recording the receipt of merchandise and they are destroying invoices and vouchers, options b., c., and d. would each be incorrect.

- (CPA Adapted) (SO 4) Within accounts payable, to provide assurance that each voucher is submitted and paid only once, each invoice approved to be paid should be b. stamped “paid” by the check signer. This represents the cancellation of the invoice, which should prevent a duplicate payment. Although each of the other options represents an internal control, they are not effective at preventing duplicate payments.

- (CPA Adapted) (SO 4) For proper segregation of duties in cash disbursements, the person who signs checks also b. returns the checks to accounts payable. This allows for the recording of the payments (separate from the custody and authorization functions). Option c. is incorrect because check signers typically review supporting documentation to determine the propriety of the payment. Options a. and d. are incorrect because they would represent violations of proper segregation of duties.

- (CIA Adapted) (SO 4) The internal control that would help prevent overpayment to a vendor or duplicate payments to a vendor is a. review and cancellation of supporting documents when a check is issued. Option b. is incorrect because it represents a violation of segregation of duties and would not necessarily prevent a duplicate payment. Although options c. and d. are internal controls, neither is effective in the prevention of duplicate payments.

- (SO 4) The following is not an independent verification related to cash disbursements: b. The stock of unused checks should be adequately secured and controlled. This is a security control, not an independent verification. Independent verifications are independent checks on accuracy and completeness, such as reconciliations.

- (SO 5,7) The IT system designed to avoid the document-matching process and that is an “invoiceless” system is c. evaluated receipt settlement (ERS). In an ERS system, there is an invoiceless match that takes place by matching the purchase order to the goods received. If the PO matches the goods, payment is made to the vendor. This eliminates the need for the vendor to send an invoice, since payment is approved as soon goods are received (when they match a purchase order). Thus, it is an invoiceless system.

- (SO 5,8) Input controls such as field check, validity check, limit check, and reasonableness check are useful in IT systems of purchasing processes to lessen the risk of b. invalid data entered by vendors. IT controls such as field check, validity check, limit check, and reasonableness check are input validation controls. They are intended to prevent or detect the invalid input of data. These controls are of little or no value in preventing unauthorized access, repudiation of transactions, or virus and worm attacks.

- (SO 11) The option most likely to be effective in deterring fraud by upperlevel managers is b. an enforced code of ethics. Upper-level managers are above the level of internal controls; therefore, internal control systems, matching documents, or segregating duties have little impact on the prevention of fraud by upper-level management. Having and enforcing a code of ethics sets the proper “tone at the top” and makes it more difficult for upper-level managers to conduct fraud.

1Suzanne Hurt, “Why Automate Payables and Receivables?” Strategic Finance, April 2003, p. 2.

2http://cdn.walmartstores.com/statementofethics/pdf/U.S._SOE.pdf

3Report to the Chairman, Subcommittee on Administrative Oversight and the Courts, Committee on the Judiciary, U.S. Senate. General Accounting Office, September 1998, p. 10.