INTRODUCTION TO PAYROLL AND FIXED ASSET PROCESSES (STUDY OBJECTIVE 1)

This chapter is an extension of Chapter 9, as it continues to present the vital processes of acquiring the resources needed to run the business, recording the resulting liabilities, and making the related payments at a later date. The distinction here is the types of resources involved and the frequency of the record keeping and payments.

The most frequent types of revenues and expenditure transactions were discussed in Chapters 8 and 9. The processes related to buying goods from vendors and selling goods to customers presented in those chapters are so common that they are typically encountered every day. These processes are sometimes called routine business processes because they involve the transactions that a business encounters on a regular, recurring basis. The volume of those transactions tends to be so large that the transactions and the related accounting activities become routine, almost like second nature, to the employees responsible for handling them. Therefore, specific authorization for each individual routine transaction is not necessary. For example, it would be an overwhelming task to specifically authorize every sale or purchase before it could be processed. On the other hand, there are many different types of transactions that do not occur regularly. They are sometimes called nonroutine transactions due to their limited occurrence and their requirement for specific authorization.

This chapter presents two categories of expenditures that do not occur nearly as often as the inventory purchases discussed in Chapter 9—namely, expenditures for human resources and capital resources. The processes that comprise acquiring and maintaining these valuable business resources specifically involve (1) paying wages and salaries to employees (payroll) and (2) accounting for property, plant, and equipment (fixed assets).

Although the processes surrounding payroll and fixed assets transactions are by no means unusual, they do not typically occur every day. Rather, they are triggered by events that tend to occur irregularly, such as the hiring or firing of an employee and the purchase or disposal of a machine. Also, these processes typically involve a smaller number of transactions. Therefore, they have characteristics of nonroutine transactions. However, during the life of these resources, these transactions (namely, the related paychecks or depreciation) need to be accounted for on a regular, recurring basis—typically, weekly, biweekly, monthly, or quarterly. This means that they have features of both routine and nonroutine processes. Some components have similarities to those discussed in Chapters 8 and 9, such as the cash disbursements activities common to all of these processes; but the differences are significant enough to warrant their presentation in a separate chapter. Additional topics with unique characteristics, including the conversion process and various treasury and administrative processes, will be addressed in Chapters 11 and 12, respectively.

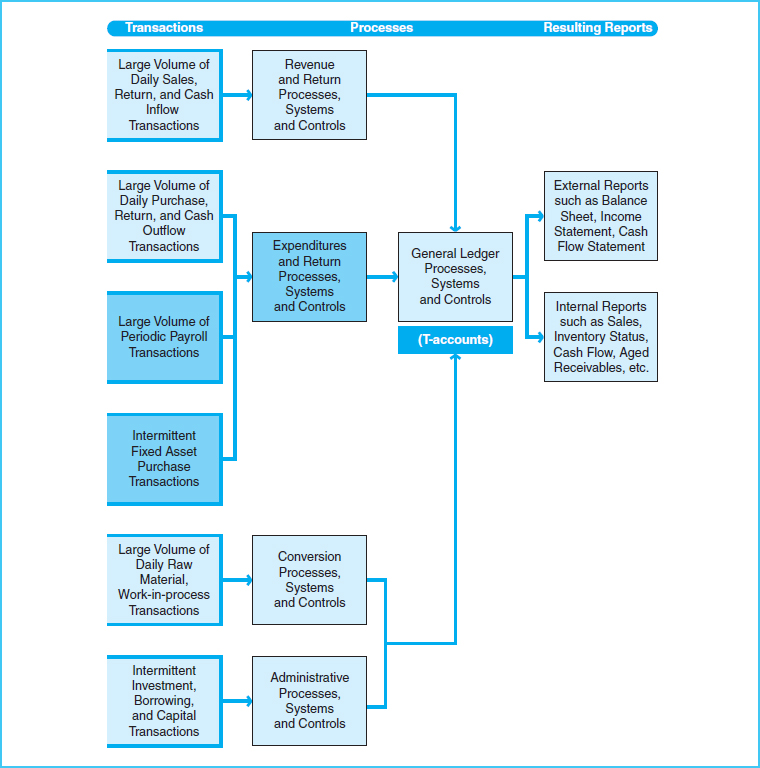

Exhibit 10-1 highlights the portions of the expenditure processes addressed in this chapter, as they relate to the overall accounting system. A company must have systems in place to capture, record, summarize, and report activities for both routine and nonroutine processes. Payroll processes include the policies and procedures that employees follow in acquiring and maintaining human resources, capturing and maintaining employee data, paying the employees for their time worked, and recording the related cash and payroll liabilities and expenses. Fixed asset processes include the policies and procedures involved in purchasing property, capturing and maintaining relevant data about the assets, paying for and recording the related assets, recording depreciation and other expenses, and accounting for gains or losses.

Various risks that may affect these types of expenditure transactions are also addressed in this chapter, including the following:

- Recorded expenditures may not be valid; that is, they may involve a fictitious employee or vendor, or they may have been prepared in duplicate.

- Expenditure transactions may be recorded in the wrong amount.

- Valid expenditure transactions may have been omitted from the accounting records.

- Expenditure transactions may have been recorded in the wrong employee or vendor account.

- Transactions may not have been recorded in a timely manner.

- Transactions may not have been accumulated or transferred to the accounting records correctly.

Exhibit 10-1 Expenditure Processes within the Overall System

The first part of this chapter presents the payroll processes, beginning with features of a typical traditional system and the related controls and followed by trends in computer-based systems. The latter part of the chapter gives a similar presentation of fixed asset systems. The internal controls procedures that help reduce the risks are presented following the discussion of each process category. Finally, ethics issues related to these expenditure processes are covered.

Keep in mind that individual companies may have differences in their payroll and fixed assets practices. This chapter provides common, simple methods of conducting these business processes. The sections on these methods should help you understand most accounting systems involving these expenditure processes, even if they are not exactly like the ones you may have seen in your personal experience.