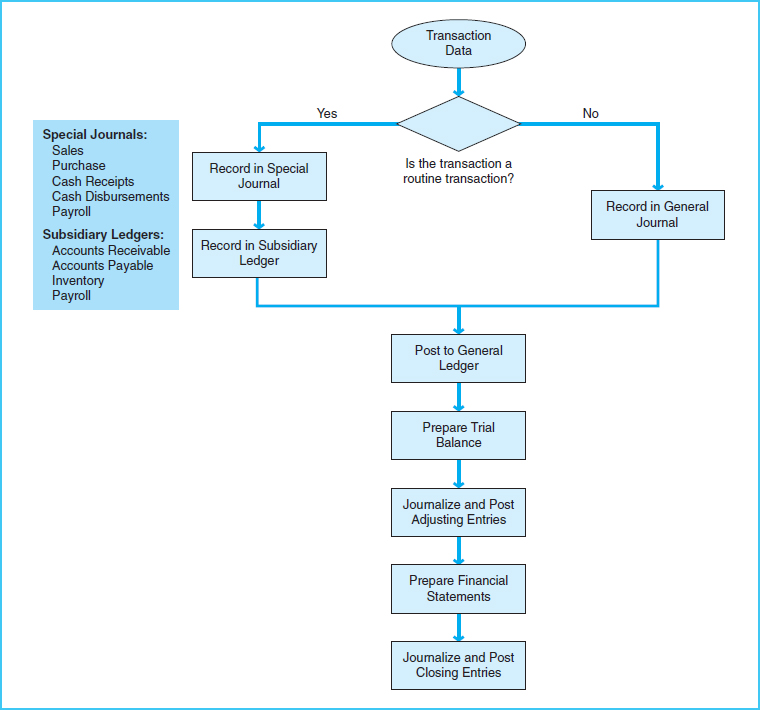

GENERAL LEDGER PROCESSES (STUDY OBJECTIVE 5)

Reexamine Exhibit 12-2 and notice that each of the processes described in this chapter and previous chapters feed data into the general ledger. The general ledger provides details for all the accounts within the chart of accounts. Recall from your accounting courses that the general ledger is the entire set of T-accounts for the organization. Each set of processes affects general ledger accounts. For example, sales and sales return processes affect the accounts receivable, sales, inventory, and cost of goods sold accounts. For manual accounting systems, the process in which transactions are posted to the general ledger is called the accounting cycle. Exhibit 12-5 is a summary of the processes in the accounting cycle.

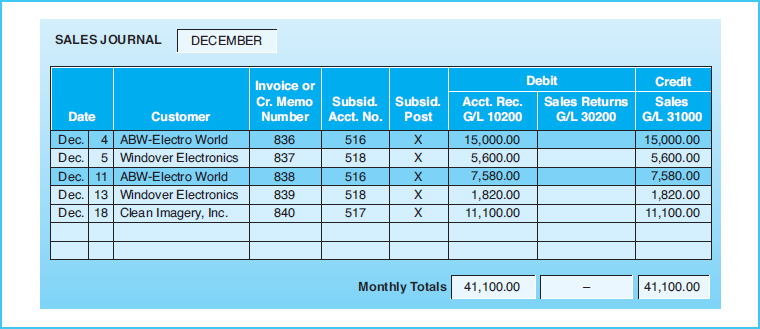

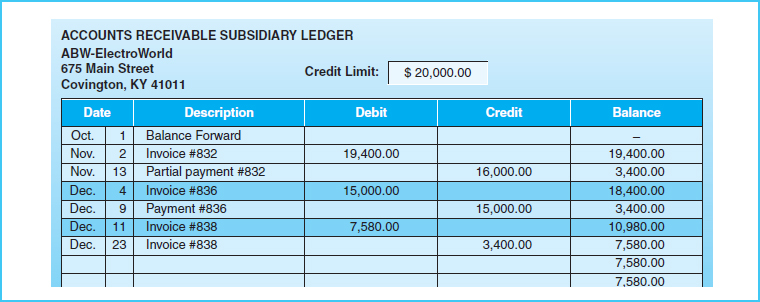

Business processes in an organization consist of various accounting transactions. When an event occurs, the accountant must decide whether the transaction is a regular, recurring transaction. If the transaction is regular and recurring, it would be recorded in a special journal. Special journals are established to record specific types of transactions. For example, a sale to a customer would be recorded in a special journal called the sales journal. The sales journal would be the appropriate place to record all credit sales. The sales journal is designed to have columns to record the amount of the sale and the corresponding receivable. That is, one column exists for sales dollar amounts (a credit), and one column for accounts receivable amounts (a debit). In addition, regular, recurring transactions are posted to subsidiary ledgers. Subsidiary ledgers maintain the detail information regarding routine transactions, with an account established for each entity. For example, a credit sale to a customer must be recorded in the accounts receivable subsidiary ledger. This subsidiary ledger maintains transaction details and balances for each individual customer. At regular intervals, such as the end of each day or end of each week, the subtotals of the special journals are posted to general ledger accounts. Exhibit 12-6 shows the sales journal, a special journal. The subtotals of $41,100 in the sales journal would be posted to the general ledger accounts of accounts receivable and sales. Exhibit 12-7 shows a page from a subsidiary ledger called the accounts receivable subsidiary ledger. Notice that the December 4 and December 11 sales to ABW-Electro World that are recorded in the sales journal are also posted to the subsidiary ledger.

Exhibit 12-5 Accounting Cycle Process Map

Some transactions are not regular, recurring transactions, and thus are not recorded in special journals and subsidiary ledgers. The transactions in capital and investment processes are examples of nonroutine transactions. These nonroutine transactions are entered in the general journal and posted to the general ledger.

At period end, it is important to ensure that all revenue, expenditure, payroll, payable, and receivable transactions have been posted to the general ledger. This includes accruing any transactions that occur as of the end of the period. After all transactions are accrued and posted, a trial balance is prepared from the general ledger account balances.

After correction of any recording or posting errors, the adjusting entries are recorded in the general journal and posted to the general ledger. The financial statements are prepared from the adjusted balances in the general ledger. To prepare the general ledger for the next accounting period, and to transfer earnings to retained earnings, closing entries are recorded in the general journal and posted to the general ledger. This ends the accounting cycle for the current fiscal period, and the cycle begins anew in the next fiscal period.

Exhibit 12-6 A Special Journal

Exhibit 12-7 A Subsidiary Ledger

These examples of accounting records focus only on sales and receivables. There are similar special journals and subsidiary ledgers for other regular, recurring transactions such as purchases, cash receipts, cash disbursements, and payroll. Also, there are other subsidiary ledgers such as accounts payable, inventory, payroll, and fixed assets. When a transaction occurs, the accountant must choose the correct set of special journals and subsidiary ledgers in which to record the transaction.

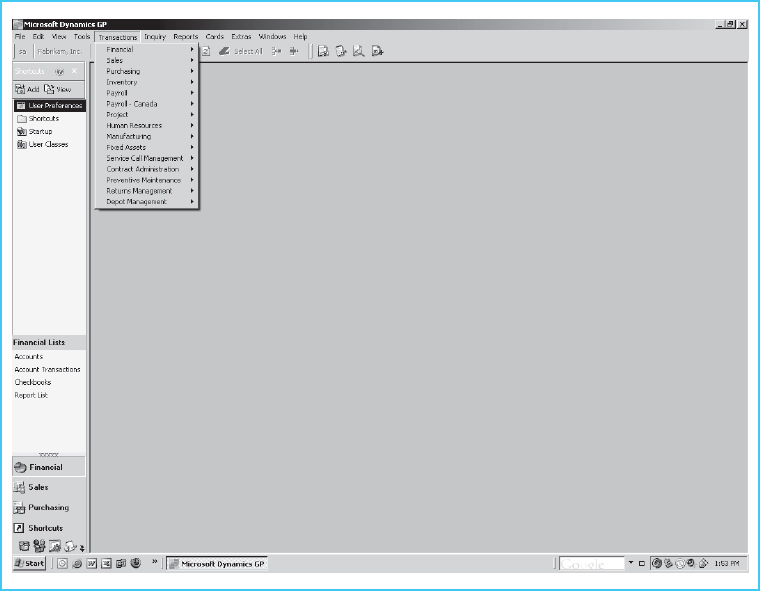

While very few organizations use manual accounting systems, much of the accounting software in use today is built on the concepts underlying the manual accounting cycle processes. For example, when entering transactions in Microsoft Dynamics® accounting software, one must choose the correct module from the menu. This module selection is similar to choosing the correct special journal. Exhibit 12-8 has a screen capture of the module selection menu from Microsoft Dynamics®. As examples, if a payroll transaction is to be processed in the software, the user would choose “Payroll,” and for sales transactions the user would choose “Sales.” Therefore, whether the accounting system is manual or computerized, we must understand the processes and the special journals, subsidiary ledgers, and general ledger accounts in an accounting system.

Transaction recording in special journals and subsidiary ledgers takes place at the time the transaction occurs. Thus, the special journals and subsidiary ledgers are updated as the processes for that journal occur. The revenue transactions, such as those described in Chapter 8, would be recorded in the correct special journal as the related shipping transaction takes place. Only the posting to the general ledger occurs at a later time. The remainder of this chapter focuses only on the general ledger process. In other words, the discussion of the general ledger processes assumes that transactions have already been recorded in special journals and subsidiary ledgers as the transactions occurred.