APPENDIX: RESOURCES EVENTS AGENTS (REA) IN ACCOUNTING INFORMATION SYSTEMS

The chapters of this book explain accounting information systems from the traditional viewpoint of accounting, which is based on a debit and credit model with ledgers and journals. Data from transactions are captured on source documents, recorded in ledgers and journals using debits and credits, and then summarized into reports and financial statements.

An accounting system can be examined through other models. A popular alternative is the REA model. REA is an acronym for resources, events, and agents. The REA model views accounting data collection as a system to collect data about the resources, events, and agents within business processes. Business processes involve events in which resources are exchanged by agents. An example of such an event is a sale. The resources exchanged are inventory and cash. The agents are the company (seller) and the customer (buyer). An REA model suggests that the basic data collected should be the resources, events, and agents in this exchange. Debits, credits, ledgers, and journals are not necessary in such a model. The data are collected and stored in a database that can then be used to provide reports and financial statements. The data include the details about the resources, events, and agents involved in the exchange.

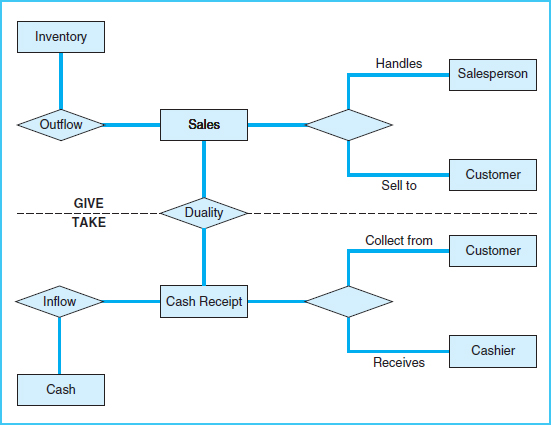

An example of an REA pattern of an exchange is shown in Exhibit 2-16, which demonstrates the basic aspects of REA. First, notice in the middle of Exhibit 2-16 that there is a duality to the exchange. That is, the customer is willing to exchange cash for goods, while the company is willing to exchange an inventory item for cash. In this exchange, there is both outflow and inflow. From the company's perspective, it is an outflow of inventory and an inflow of cash. These are the two events in the duality: a sale and a cash receipt. The resources involved are the inventory of goods and cash. The agents are the salesperson, the customer, and the cashier.

The preceding paragraphs present only a simple explanation of the basics of REA. REA is a rich, complex subject that would require many pages to fully explain. As a model of an accounting system, it is used by some accounting instructors to help students understand the relationship between business processes and the accounting data resulting from the business processes because some faculty members believe it is an excellent model by means of which to teach learn accounting information systems. To properly use it as a model to teach and learn accounting information system concepts, REA should be integrated into the foundation of the entire course and become a part of all or at least most of the concepts covered.

Exhibit 2-16 An REA Pattern for Sales

On a different note, the practical application of REA in accounting systems in real companies or organizations has not become popular. There are at least three reasons that REA has not been widely adopted as a model for real-world accounting systems. First, it does not fit well with traditional accounting systems. As described previously, REA offers a perspective completely different from the traditional view of accounting systems. Therefore, it would be very difficult to integrate REA into legacy systems. Second, the restrictions within REA may not fit all aspects of current accounting conventions. For example, resources in REA are akin to assets. However, a strict interpretation of REA resources would not include goodwill, which is considered an asset in traditional accounting concepts. Finally, some have suggested that the accounting profession is too conservative to adopt such a radically different model of accounting systems.

However, REA is continually being further developed and may someday be an important foundation of accounting systems. Currently, REA is an important basis for concepts being developed for e-business exchanges. A working group entitled the eBusiness Transitionary Working Group (eBTWG) is using REA to develop models for detailed information collection and exchange within e-business. REA is a good fit with the low-level detail required for a purchase order in an e-business exchange, but may not fit as well with an overall accounting system based on traditional accounting concepts. As REA continues to be developed and as business and accounting change in the future, REA may at some point become an important foundation of accounting information systems in businesses and organizations.