Chapter 3. The Virtual Asset-Lite Model: Intellectual Property Licensing

"To the winner of the race will go possible Nobel prizes and huge potential profits."

—The Genome Gold Rush

"Priceline will reinvent the DNA of global business."

—Jay Walker

The advent of the New Economy created another twist on innovation. It wasn't just a New Economy; it was now a Knowledge Economy, too. The concepts of innovation and intellectual property (IP) became inextricably intertwined. The most valuable venturing was virtual—building a firm around IP. Patents were the strongest form of currency, not just onerous paperwork. IP licensing was no longer viewed as a mundane legal process. Instead, it was a core corporate strategy and a legitimate, lucrative business model. It was the key to realizing the potential riches of innovation.

The new IP licensing model for innovation was predicated on the basic beliefs that knowledge is power and IP equals profit. Organizing for innovation therefore meant going virtual in a very real sense. Focus on creating and capturing key intangible assets. Protect and license and leverage them. Minimize real investment. Maximize real profit.

It seemed almost anything was patentable: raw ideas, business processes and business models, even life itself. New companies gained huge valuations on the basis of their novel patent portfolios, not necessarily because of their sharp and innovative operating businesses. In Priceline's case, one key asset was U.S. Patent No. 5,794,207—bilateral buyer-driven commerce—better known as name your own price. The IP excitement was much broader than just the Internet. Innumerable genomics companies sprouted to patent the unraveling mysteries of human DNA, for example.

A patent machine became the preferred prototype for a Knowledge Age startup. At the same time, old-line companies, such as IBM and Xerox, were cited as transitioning to new, IP-centered strategies, reaping rich gains and transforming themselves in the process. For 1991, IBM had an already impressive 679 patents granted. A decade later, that annual tally had soared five-fold to 3,411. Both types of companies, new and old, served as models for the New Knowledge Economy.[1]

The Old Economy: Real Companies, Real Products

Until the past decade or so, licensing played a relatively minor role in most firms' innovation strategies. It was largely an afterthought. Licensing one's own inventions to others (out-licensing) had been a reliably, if marginally, lucrative operation for some firms for many years. On the entrepreneurial front, occasionally, there was some Horatio Alger story of the lone, idiosyncratic, garage-lab inventor who struck it rich after winning a legal battle against big business and signing lucrative licensing rights for some newfangled contraption. For the most part, however, patenting and licensing remained a routine and unglamorous activity. Licensing was often viewed as more trouble and expense than it would be worth or was relegated as a tactic for old technologies in secondary markets.

Patents themselves were not viewed as something to be aggressively and proactively commercialized. They were not the essence of innovation, nor were they the key to realizing its value. Instead, patents were a formality and technicality. They were used primarily as a defensive legal tactic to protect and defend one's inventions, and to keep other firms from getting hold of and unjustly exploiting one's own R&D without paying their due. Patenting was a game of denial—to deny competitors traction, to threaten and frighten them, or to pull the rug out from under them if infringement had already taken place. It was a reactive process driven and executed mostly by attorneys. IP management was not a game that most executives and entrepreneurs dreamed of or particularly wanted to play. The real business of innovation continued to revolve around actually transforming the abstract ideas embodied in patents into cold, hard reality: creating, manufacturing, and selling real new products. IP licensing was not a core part of the innovation commercialization strategies of established and successful firms.

On the other side of the equation, few successful companies would have even considered licensing the inventions of others (in-licensing) as an integral part of their core innovation strategies. In-licensing had a stigma attached to it. Although it was perhaps occasionally and regrettably necessary, in-licensing was a second-class approach. It highlighted a firm's own inability to do the real, hard work of R&D. It left a firm at the whims and mercy of others, not in full control of its own destiny in terms of the critical function of invention. In-licensing was like an involuntary tithe that, even worse, might flow directly into the coffers of a more innovative competitor.

Intellectual Property Rules

Times change. The rise of the New Economy brought with it the ascendance of the intangible, in both substance and style. Even with their incredible legacy of innovations and long list of patents to match, the old "smokestack" manufacturing industries had long dominated the economic landscape not so much with their IP as with their extensive real property, plant, equipment, and labor. The paradigm for the emerging knowledge-intensive, technology-driven economy was different.[2]

A new model of innovation, value creation, and company building gained currency. It was no longer about empire building; instead, it was about virtual empire building. Enron CEO Jeffrey Skilling famously exemplified this new attitude as he promoted the new paradigm of the asset-lite firm. It was no longer about commanding and controlling physical assets. Creating and capturing value from innovation now centered on the ownership and rent-seeking exploitation of intangible, knowledge-based estates. According to the U.S. Patent and Trademark Office, the number of patents granted annually nearly doubled during the 1990s (99,077 in 1990 compared to 183,975 in 2000), as did the number of patent applications (176,264 compared to 315,015).

It's difficult to imagine now because management fashion changed so much and so fast, but the concept of an IP-centered business model just a short while ago would have been a curiosity at best. Mostly, such an idea would be met with quizzical looks. An observation from that time offers a glimpse into the rapid and profound change in mindset: "Patents on business methods used to be a rarity, because it seemed legally preposterous to claim ownership of a way of doing business."[3] Beginning in the mid 1990s, however, the U.S. Patent and Trademark Office broadened its own notion of what was patentable, a move subsequently backed by the U.S. courts. Managerial and entrepreneurial thinking dramatically changed as well. The virtual land grab began. The idea of an IP-centered model for creating and capturing the value from innovation became not only widely known and accepted, but even a preferred ideal.

Virtual Assets, Real Profits

The knowledge-intensive, asset-lite approach to innovation commercialization offered a sweet-sounding pitch. The pitch went something like this: Go virtual. Let someone else do the heavy lifting. In the New Economy, the real value resides in IP. Build your company around IP assets, set up smart and aggressive legal and financial structures and processes, and the cash will flow. Many enthusiastically touted such asset-lite approaches even for what had been thought of as old-line businesses (e.g., Enron's transforming a stodgy pipeline company into a dynamic energy-trading and derivative operation).

Central to this new paradigm was a shift toward the idea that innovation's profits spring forth not from real, hard, and tangible assets, but instead flow from ownership and control of key intangibles, such as patents and processes, and software and standards. Physical assets increasingly became thought of as commodities, mundane (if necessary) base materials upon which intellectual capital could work its Midas touch. For leading companies anyway, plant and equipment would be largely passé. Manufacturing was the toil of lesser mortals, admittedly necessary but relatively low value-added work. After all, the dirty job of manufacturing could easily be outsourced for the lowest cost.

The big bonus of the IP-centered, asset-lite approach was that it promised to make financial statements sparkle. With intangible IP itself as a company's core product, relatively little direct incremental "cost" exists in terms of a company's cost of goods sold (COGS). That is, after the base IP is developed and paid for, each unit's incremental cost is miniscule, often near zero. Compared to the old way of doing business (invent-build-sell) in which each unit has very real and substantial costs attached to it, IP gross margins look fantastic. Moreover, the leverage of increased sales is enormous; beyond recovering the initial R&D costs, it's mostly thereafter pure profit.

So began the great patent race. Patent anything and everything. For entrepreneurs, patents became the high-tech equivalent of lottery tickets. Buy as many tickets as possible to cover your bets and at least one of the numbers would surely hit big. A few companies did hit it big, at least initially, even if their novel, sweeping patent claims proved more than slightly controversial and contestable.[4] Meanwhile, established companies were accused of negligence for letting their extensive patent portfolios gather dust, leaving supposedly trillions in license royalties unrealized. Corporations rushed to dust off their forgotten and neglected "treasures in the attic" to rediscover, assess, and collect their true value. New and old companies, ranging from biotechnology to software, scrambled to stake their claim on everything from the fundamental structure of the human genome to the basic points-and-clicks of e-commerce.

Ins and Outs of Licensing

Fortunately for the new and enthusiastic out-licensing crowd, in-licensing concurrently and complementarily grew in its appeal. Companies became less and less hesitant to source innovation from outside in a movement toward more "open innovation." Not Invented Here (NIH) lost much of its stigma. In a faster, more complex, and more competitive economy, managers increasingly sought whatever pieces of technology it would take to get the job done, no matter what the source.

An explosion of interest in out-licensing was accordingly matched by a like increase of in-licensing activity. The combination of these complementary out-licensing and in-licensing trends led to a dramatic increase in licensing activity by all types of organizations. Even universities and non-profit organizations jumped on the bandwagon. New IP management divisions and technology transfer offices sprouted. IP-centered consulting and advisory firms proliferated. The number of books and articles extolling IP's unparalleled economic power and enormous profit potential soared. In the net, however, the supposedly radical new IP licensing model for innovation was more evolutionary than revolutionary, and more complex and challenging than its proponents suggested.

IBM = IPM (Intellectual Property Management)

IBM's history both foreshadowed and helped set the key trends in IP licensing that emerged during the 1990s. For most of its nearly century-long history, IBM did not actively mine its unique, enormous, world-class IP portfolio. The company extensively licensed for decades, but this was largely because of antitrust consent decrees that required it to freely provide its many patents and technologies to all who applied. IP licensing revenue was not a principal concern. As IBM's dominance of computing began to erode throughout the 1980s, however, the company started to get more serious about generating revenue from new sources. Its intangible assets and IP portfolio proved an irresistible target.

Even as the 1990s began, IBM was still a net payer for IP. However, its new and aggressive licensing initiative dramatically turned the situation around within just a few short years. IBM licensed not only patents, but complex processes and know-how in fields ranging from computing to communications and software to semiconductors. By the decade's end, IBM's IP initiative generated more than $1 billion annually. Even for an organization as large as IBM, these were clearly fantastic gains on heretofore underutilized intangibles. From 1993 to 2002, IBM booked a total of more than $10 billion in IP licensing revenues.

With these results, it's hardly surprising that IBM became one of the exemplars of the innovation-as-IP-licensing movement. As with so many other innovation exemplars, however, there is considerable ambiguity about whether IBM is the IP example that other firms can or should emulate. Moreover, for those seeking a new model for innovation, IBM does not really offer an entirely new template as much as an evolution toward better IP management. In the final analysis, IBM's IP licensing gains are more a byproduct of the firm's fantastic core innovation success, rather than the source of this success. Consider the following exceptional facts.

IBM might have been at the cutting edge of IP management and technology licensing, but it was hardly a virtual company. It remained a very "real" organization. IBM continued to create and sell real products, services, and solutions—more than $80 billion worth every year. It had more than 300,000 employees and billions invested in hundreds of facilities for R&D, manufacturing, and service worldwide. This is what funded the vast majority of IBM's R&D, which in turn led to an ongoing, virtuous cycle from which excess IP was continuously generated and licensed. IBM's IP licensing represented the "excess" generated by its highly successful core R&D and operating business units, the proceeds of which in turn fed additional incremental resources back into this core.

IBM's licensing revenues are backed by an incredibly deep and broad IP portfolio, the result of massive, ongoing investments in R&D representing a century-old history of innovation. The firm invested more than $5 billion per year in R&D; it cumulatively has invested the equivalent of hundreds of billions. Here's another exceptional statistic: IBM employs more than 5,500 Ph.D.s—just Ph.D.s alone, not total researchers. To get a better idea of the scale of IBM's investment in brainpower, consider that during the 1990s, only about 800 Ph.D.s in computer science were earned annually across the entire U.S.

Even against such a backdrop of massive and sustained R&D expenditures and enormous intellectual and human capital, IBM's IP achievements are still impressive. Each year from 1993 to 2003, IBM received more U.S. patents than any other company in the world, a total of more than 25,000. In 2003 alone, IBM received nearly 3,415 patents from the U.S. Patent and Trademark Office; that's more than any other company in history in a single year. The scale and scope of IP generation was outstanding. Yet, this total still equaled less than one patent per year per Ph.D., and Ph.D.s aren't cheap. Given $5 billion in annual R&D expenditures, IBM's $1 billion of annual IP licensing revenues were hardly easy profits. Given these sorts of facts, IBM's IP licensing achievements are no less admirable. But they certainly appear much more proportional and are much more difficult for other companies to imitate or otherwise use as a simple template. However much its IP programs generate returns, the payoff is not out of scale with the rest of IBM's superlative investments and achievements.

Despite its fantastic success in reaping the rewards of its IP, IBM's awakening did not represent a transition to a radically new and different IP licensing model. Its "real" businesses remained the real revenue and profit generators. In contrast, IBM's IP licensing and related revenues were not a steady growth business by any means. They actually declined by 11.2 percent from 2000–2001 and declined a further 34.2 percent from 2001–2002, even as the company's total sales remained relatively steady.

IBM is certainly not alone in reaping significant gains from more active management of an extensive IP portfolio. Other organizations, such as Lucent and Texas Instruments, have also harvested hundreds of millions or more from their more proactive IP licensing. But, like IBM, these are also hardly virtual enterprises centered only around IP. They are distinguished industry leaders with decades-long histories, tens of billions of cumulative R&D investment, and tens or hundreds of thousands of employees. They have real, multibillion-dollar global investments in everything from labs, manufacturing, and marketing to customer service and support. They make real products and provide real services and solutions. This is the key source of ongoing value creation for even these most exemplary of IP managers and technology licensors. IBM's own technology chief put it well: "[W]e consider patents a starting point on the path to true innovation." IP is the beginning, not the end, of innovation.

The "Knowing" and "Doing" Connection

The bottom line is that so much of the tremendous IP success of organizations like these comes from ongoing investments in actually doing—creating, manufacturing, and marketing competitive world-class, market-leading products—not just knowing. They do not just think and dream and toil in the labs and then simply license their abstract intellectual output. It is too difficult to separate knowing from doing. Even just recognizing the value of IP, much less actually realizing this value, might require a great degree of practical, applied knowledge, experience, and capabilities. Without actually getting its hands dirty in the nitty-gritty of commercialization and competition, it is difficult for an IP-only company to stay in the game and to innovate the next generation of technology and ideas. A surprisingly huge amount of innovation in many industries originally comes from customers and suppliers, for example.[5] Without being involved in such a value chain, an IP-focused firm cannot learn and gain their ideas, inventions, and insights.

The ideal of transforming a company into a virtual corporation built primarily or solely on raw IP remains elusive in practice except for specialized or niche firms. Even for Microsoft, another often-cited example and the most successful and valuable New Economy company, IP licensing (as opposed to product licensing) remains only a minor operation. One of the key architects of IBM's IP management and technology licensing success during the 1990s, Marshall Phelps, took the same role for Microsoft beginning in 2003. Even as Phelps embarked on revamping and expanding Microsoft's IP licensing efforts, he noted that the company did not expect any direct substantial revenues anytime in the foreseeable future.[6] Instead, Microsoft's newly energized IP licensing initiative was designed to support and bolster the company's other core products and services. It was designed to help create a better support structure, not to be the "main game."

Another IBM transplant, Rick Thoman, tried to replicate IBM's IP licensing success at Xerox. He started as the new Xerox president in 1997 and then continued the task as CEO beginning in 1999. Thoman was hired, in large part, for his IP savvy. He had been IBM's CFO for much of the 1990s, helping encourage and manage IBM's explosion of licensing activity. After taking the helm at Xerox, one of Thoman's key strategic initiatives for Xerox was to replicate, if not better, IBM's success at exploiting its IP portfolio. Xerox already was a rich potential mine, with more than 5,000 of its own patents and processes to license. A revamped IP strategy held promise to quickly help boost Xerox's bottom line. Unfortunately, the initiative did little to help Xerox address its core business problems or halt its continuing slide. After little more than a year as CEO, Thoman left Xerox as the company's problems worsened.

The experiences of Microsoft and Xerox offer a key point to ponder. Even the original architects of IBM's own IP-rich licensing strategy could not readily replicate this lucrative model in other global technology leaders like Microsoft and Xerox. Clearly the odds of doing so were very challenging at best.

The Secret of Life (Patent Pending) Itself

Few areas of the New Knowledge Economy embodied the new IP buzz, the new innovation-as-intellectual-property paradigm, more than the exciting and booming field of genomics. An entirely new industry sector was born and literally dozens of companies were founded on this paradigm that knowledge is power and IP equals profit. In this case, the knowledge was that of life itself, decoding and understanding (and, of course, patenting) the human genome. The human genome was viewed as the Rosetta Stone for unraveling the secrets of health and disease.

The promise appeared to be so great that genomics excitement even survived the technology bubble bursting in March 2000. Genomics firms continued to launch successful IPOs that were still spectacular in their own right. Among other cures, genomics was promised as the salvation for a stagnant Big Pharma. The big drug companies' pipelines dried to a trickle despite their massive increases in R&D investment. The old approach to drug discovery and development seemed to have run its course. A rapid increase in fundamental knowledge of human life itself promised to rapidly bring new power to the drug discovery process. It heralded the advent of innumerable new diagnostics, therapies, and cures. Whoever could own the maps to these treasures and the keys to unlock these secrets would surely harvest untold riches.[7] The new genomics leaders could name their price as Big Pharma scrambled for a place in line to license them.

Human Genome Sciences (HGS) and Celera Genomics were two firms that made the biggest splash. J. Craig Venter, formerly of the National Institutes of Health and the founder of the Institute for Genomics Research, provided the brains for both firms. The pioneer for the industry, Human Genome Sciences, formed in 1992 and went public in 1993 as the first pure stock market play on the mapping of the human genome. HGS was the harbinger of many more similar firms to come. More than a dozen were formed just within a year or so of HGS's founding. Progress was slow, however. The revolution took a while to gain momentum.

The real boom began a few years later. Celera Genomics was co-founded in 1998 by Venter and Perkin-Elmer, the pioneering maker of high-speed, automated DNA analysis equipment. During the later 1990s and into 2000, an entire slew of companies joined the genomics revolution and went public: CuraGen, deCODE Genetics, Exelixis, Genaissance, Genomica, Genset, Hyseq, Incyte, Interleukin Genetics, Lexicon Genetics, Medigene, Millenium, Myriad Genetics, Pharmagene, Variagenics, and so on. Some companies focused their efforts on the raw genomics data itself. The pharmacogenomics players focused on decoding the interaction between genes and drugs. Other firms focused on providing services, software, and support for these decoders. Bioinformatics was born.

Complex Secrets

Genomics quickly proved to be slightly more complicated and evolutionary, and less lucrative and revolutionary, than most companies had planned. By the end of 2002, in a quick turn of fortune, many genomics-focused firms were trading for less than their cash in the bank. Their IP pursuits now seemed like dry wells, not gold mines. Of the big players, Celera Genomics had a market capitalization $100 million less than its net cash. One of the smaller players, Variagenics was trading at a market capitalization of less than half its $50 million net cash. In a move toward consolidation and a bid for survival, some players acquired others not for their IP, but simply for their cash, then shut down or liquidated the acquired firm's operations. Clearly, making money from the Rosetta Stone ofthe human genome was a tougher business than many had anticipated.

It's important to note that the difficulties the genomics sector encountered were not because of a lack of fantastic scientific advances. Instead, many companies ran into tough times despite their amazing new scientific discoveries. Regardless of many accusations of grandstanding and hyperbole, the early genomics discoveries truly did represent fantastically rapid and profound biomedical progress. Some of these advances in understanding were even discussed as being worthy of Nobel Prizes. Celera Genomics claimed to have decoded the human genome, after all. Many of the smaller players discovered specific genes that had significant roles in serious ailments such as cancer, depression, diabetes, and obesity.

A lack of scientific discovery and lack of patents were not the reasons for these firms' troubles. Their troubles also were certainly not because of a lack of active and aggressive IP management, either. They were founded with IP management and licensing as the centerpiece of their strategies and business models. Their difficulties were more fundamental: The problem was simply that the basic science and raw IP had very limited commercial value.

Most of the harbingers of the genomics revolution subsequently radically overhauled their strategies. They chose to focus on developing real diagnostics and, especially, real therapies and cures—not just selling raw data and roadmaps—as where the real profits were to be discovered. Some players more clearly and practically focused on diagnostic tests, such as providing not just genomics data, like markers and maps, but creating and delivering actual products for hospitals and labs to use to detect, prevent, and treat disease. Many others chose to embark on the difficult, time-consuming, and expensive path of discovering and developing new drugs.

To create and capture the value of their inventions, the pure IP plays that the genomics companies initially represented were transformed to look more like the old, traditional pharmaceutical companies that supposedly had been passé. Even the shining stars of the genomics revolution conceded that, although raw IP is essential, discovering, developing, and delivering real products is what is commercially valuable. For example, Celera Genomics concluded that it simply could not generate substantial enough revenue from genomics alone; a big enough market just didn't exist. Instead, Celera Genomics realigned itself to bet the entire company on drug discovery and development. The company brought in experienced management and technical talent from old-line, Big Pharma companies such as Roche and DuPont to help it make the shift. Many smaller players followed, in an often-repeated pattern of shifting strategies and science, new management, and market focus. They would struggle to become "real" companies, not simply virtual, knowledge-based, pure IP licensors.

The decision of these genomics firms to focus on building more integrated, product-based businesses does not at all suggest that the knowledge they generated was worth little. In fact, in a larger intangible and societal sense, many of their scientific discoveries were truly invaluable. But, in a hard-nosed, revenue-generating sense, there often are considerable limitations to what raw IP can produce. Raw IP typically has limited commercial value and only a small, niche market. Customers pay richly for solutions, not abstractions. Even the most prolific generators of basic scientific and technical progress struggle with these unavoidable facts.

If You're So Smart, Why Aren't You Rich?

The world's research universities have long been a wellspring of new scientific and technical knowledge and novel, path-breaking inventions. Their experiences also hold valuable lessons about the uses and limits of IP-focused innovation models. University contributions have been essential in advancing innovations of all kinds, from computing and communications to medicine and the life sciences. Indeed, according to the National Science Foundation, universities fund more than half of all basic research in the U.S. In recent years, their mission has expanded beyond pure, basic research.

Much like their for-profit counterparts, academic research institutions caught the lucrative IP licensing fever. They founded and funded increasingly larger, more formal, and more sophisticated IP management units and technology transfer programs. Spurred in part by the Bayh-Dole Act of 1980, which pushed the commercialization of federally supported academic research, American universities were quickly in the lead in this IP commercialization race, far ahead of their Canadian and European counterparts. Membership in the Association of University Technology Managers (AUTM) reflected this booming interest. AUTM membership grew more than three-fold in just a decade, from 1,015 in 1993 to 3,200 by 2003. Increased patenting and increased patent licensing was the first focus and priority of these IP commercialization efforts.

Without a doubt, university IP licensing has grown to be a lucrative side business, at least for a handful of elite institutions. But, even among this elite, a glance at the actual numbers is revealing. Take the most elite of the elite research universities. In 2002, the Massachusetts Institute of Technology (MIT) generated a total of $26 million in gross IP licensing revenues. This is certainly a lucrative incremental revenue stream, but hardly huge for an institution of MIT's size, history, and brainpower. Stanford University's gross licensing receipts ($50 million) almost doubled MITs. Yet, they still constituted less than 2 percent of Stanford's overall revenues. In comparison, Stanford received $247 million just in NIH grants alone that year. The direct returns to research universities' enormous investments in IP are small, however greatly these discoveries contribute in a larger sense.

The limited size of Stanford and MIT's IP licensing revenue was not because they were new to the game. Neither institution was a novice at technology transfer and IP commercialization. They were already two of the long-established and recognized leaders. Viewed against their total annual R&D expenditures and their total revenue bases, IP licensing for even the most elite and successful academic research institutions is a high gross-margin, but still marginal, contribution. Whether good or bad, the fact is that college sports generates plenty more cash for most schools than does cutting-edge IP.

Limitations of the IP-Centric Model

There are several reasons why even these elite IP generators realize limited royalties from their considerable R&D investments. Some of this is undoubtedly because of the fact that they are, of course, non-profit institutions whose main mission is not to make money. In addition, the phenomena of university IP management and technology transfer remain relatively novel concepts, still in their infancy. As with the genomics companies, however, the primary reason for their limited revenues is simply the nature of basic science and raw IP. Basic science is about generating fundamental knowledge, not selling products; it's about generating new discovery, not discovering huge new revenue streams. However much things have changed during the past decade, the university mission still centers around basic research, with some (and increasing) focus on development, but much less on commercialization. Much of research universities' discovery remains in commercial infancy, undeveloped or under developed. It is quite fitting that these world-class generators of scientific and technical knowledge are non-profit organizations, not for-profit companies.

Only a small share of university-generated patents yield significant commercial interest. Of those that do, only a few generate notable returns. For many universities, licensing returns are so meager that IP management costs (for example, running technology transfer offices) exceed revenues. Overall, university IP licensing revenues are based on a relatively small handful of major universities and on a relatively small handful of blockbuster license agreements. Most of this is even more narrowly focused in the life sciences. Universities' massive R&D investments and their prolific spawn of knowledge and invention are invaluable contributions to innovation. Through direct technology transfer mechanisms and through spillovers, university R&D output offers great public benefit and great commercial potential. However, it does not easily translate into quick, large, and direct financial returns.

No matter how promising a technology might seem, for example, often, no licensee can easily be found. This is one reason why spinouts have become an increasingly popular option that many university technology commercialization offices pursue. Spinouts involve forming a real company to push the IP closer to commercialization and thereby demonstrate and realize more value as it grows. A patent itself is just a kernel. Spinouts offer the possibility to further develop and "scale up" the IP, giving it greater value as this process progresses. But, again, this requires building a "real" company.

Size Matters: Scaling Intellectual Property

The process of commercialization is where most innovation value is added. Raw IP remains a critical ingredient or a cornerstone, but it is not even the entire recipe or a whole blueprint, much less a finished product. It is just a beginning, not the end. Raw IP is the start of a process where value is added in ever-larger, non-linear increments at each stage.

Customers are willing to pay premium prices for finished products that provide real solutions for real problems in the here and now. Customers are willing to pay little or nothing for virtual, abstract ideas and inventions that have uncertain value at best. Developing these raw ideas takes a tremendous amount of additional time, risk, and investment. In most cases, as innovation goes all the way through the value chain, from raw IP to full commercialization, its relative gross margins might shrink, but its absolute gross margins grow much larger. Pure, raw IP-based business models, therefore, can often be quite profitable in one sense (for example, gross margins). But, they concomitantly might be quite limited in scale, in terms of both absolute revenue and absolute profit potential.

Why does scale matter? For startups, scalability is a serious limiting factor. The level and nature of startup investments and valuation are critically predicated on certain assumptions about market size and the corresponding revenue and profit potential. If these assumptions are way off the mark, it might be difficult for true economic profit to ever be realized. The genomics companies provide many ready examples. This is why most abandoned their original pure IP-centered models.

A decade after its founding, for example, genomics leader Human Genome Sciences generated less than $5 million in 2002 revenues. The other leader, Celera Genomics, did better. Celera boasted fiscal 2003 revenues totaling $88 million. But even that annual tally was worth just about 1 percent of Pfizer's yearly R&D budget or about two days of sales of Pfizer's Lipitor anti-cholesterol drug. These figures help illustrate how raw IP by itself has inherent scale limitations. This is exactly why Celera radically transformed itself from trying to be a generator, repository, and provider of IP into a nascent drug discovery and development firm (a "real" pharmaceutical company). Real drugs are where the real money is.

Here's another perspective. A successful $20 million licensing business with high gross margins seems lucrative in the abstract. Taken into context, however, there is often considerable accounting ambiguity in such calculations; for example, if the firm spends $100 million per year on R&D, is any of that expensed to the portfolio of out-licensed IP? Regardless of such important accounting issues, the bottom line is that even a lucrative $20 million licensing operation is likely to have modest impact at best, either to turbocharge an already successful company or rescue a floundering company, with $1 billion or more in sales. Yet, this is approximately the relative scale of IP licensing revenues for an exemplar like IBM.

IP as a Beginning, Not the End

The case of medical imaging startup PointDx clearly illustrates well the indispensable use, but also the inherent limitations, of IP licensing as a core innovation strategy. PointDX's initial endowment of IP helped give it a strong start and some considerable staying power. Even with these early advantages, PointDX still faced the larger challenge of building a company that could help fundamentally transform the practice of radiology.

David Vining had worked as an academic researcher for more than a decade before founding and leading PointDX. In concert with his former university employer, Vining held some of the key patents related to virtual 3D medical imaging. His patented discoveries made possible non-invasive diagnostic techniques to reduce or eliminate the need for more complicated and invasive procedures. During the 1990s, for example, colonoscopy had become an increasingly common procedure to screen for colon cancer and other conditions. Rather than submitting to a dreaded and uncomfortable colonoscopy, however, patients instead might be able to opt for a non-invasive "virtual" colonoscopy. Doctors could get detailed 3D pictures of organs and tissues from the outside without having to prod and probe from the inside.

Virtual colonoscopy itself was a great invention. But Vining had a much larger vision for PointDX. In the process of developing his patented technologies, he realized that the entire practice of radiology was ripe for change. Using recent imaging and computing advances, there was a fantastic opportunity to transform the process from start to finish. Even by the year 2000, much of the process of radiology differed little from its nineteenth-century roots, when doctors first tried to make sense of blurry X-ray films. The basic science and applied "picture-taking" technology had fantastically advanced in some regards (for example, CAT scans and MRIs), but radiology still remained an idiosyncratic and labor-intensive process. Images had to be captured and then developed. Doctors would read the images and dictate their diagnoses. Dictation needed to be transferred and transcribed. Eventually, all the records would get stuck in a folder and (hopefully) appropriately circulated and stored somewhere for later retrieval or transfer.

PointDX sought to digitize and standardize the process from start to finish. With PointDX's systems, doctors would directly interpret digitized onscreen images by using simple and quick point-and-click interfaces and standard, structured diagnostic codes. The radiology value chain would be greatly simplified and compressed. PointDX's type of system promised to eliminate the slow, laborious, and sequential process of imaging, interpretation, diagnosis, dictation, transcription, verification, and feedback. With instant, real-time technology, all the stages of this process instead could be wrapped into one.

The concept promised to significantly reduce diagnostic costs, delays, and errors; more importantly, it promised to speed and improve diagnoses. Images could be shared instantaneously and simultaneously from any number of locations worldwide, allowing for remote or joint interpretation. Text, numerical, and image databases could be automatically constructed and rapidly mined. This sort of rich data mine would foster research and discovery in a way already common to many other medical and other scientific fields, but still novel for radiology.

Despite such a compelling value proposition, transforming the practice of radiology was a daunting task for a small startup. Moreover, in the wake of the technology bubble bursting, funding sources withered. Where would PointDX get cash for development? Just as importantly, how would PointDX be able to successfully deal with health-care giants who might also have interests in, or even designs on, this new market space? For years, General Electric and other medical imaging leaders had already continued to ignore PointDX's existing patent infringement claims.

PointDX pressed on and enlisted help. In the late 1990s, after years of litigation, imaging equipment maker Fonar finally won a $100 million patent-infringement judgment against GE Medical Systems and had settled with other manufacturers. PointDX took notice of the case and retained the services of Fonar's IP counsel. GE and company finally began to pay attention.

By 2003, PointDX settled for agreements awarding it modest though significant patent royalties from GE, Siemens, and Philips. As a result, through this process, PointDX was able to circumvent the more traditional and often onerous venture capital process and yet still proceed to fund development of its larger business plan by using the royalty stream from its basic imaging patents. CEO Vining could have simply cashed out on these royalties and claimed victory. But, however rewarding, patent royalties alone were not nearly enough to build a substantial and sustainable company.

PointDX cleverly and aggressively used its IP to give it development cash and to buy it some time and breathing room. It got the attention of, and helped ink deals with, the biggest global players in medical imaging. PointDX then could more fully concentrate on its core innovation. It could focus on getting product developed and out the door, and on convincing doctors and health care providers to change their deeply entrenched ways.

PointDX's IP licensing tactics did not eliminate its core innovation challenges or eliminate the inherent risk of being a startup. However, at least they helped give the company a chance at a promising new market—a chance it probably otherwise would not have had. PointDX tactically used its fundamental patents to fund and support its larger, longer-term R&D and business development strategy. In turn, by crafting a more comprehensive suite of functions and products that promised to radically simplify and yet increase the power and capabilities of the radiology value chain, PointDX made itself an attractive acquisition candidate for the big players in biomedical equipment and services.

Turning Licensing Inside-Out

With the growth of IP licensing, it's necessary to take a look at this equation from the perspective of the licensee. Out-licensing's more homely twin, in-licensing, received less attention and consideration from innovation enthusiasts. Few have focused their attention on the licensee because the glory and the gains of royalties flow more to the innovative licensor. This one-sided focus is unfortunate because in- and out-licensing are two sides of the same coin. For every licensor, there is obviously at least one licensee (and often many more). The fact is that, for many firms, in-licensing will play a more important role in their core innovation strategies than out-licensing. In more and more situations, successful and profitable innovation commercialization depends more on in-licensing skills and capabilities rather than out-licensing activities.

The two primary drivers of a change in attitudes toward in-licensing are, first, the explosion of technological complexity and, second, rapidly rising economies of scale and scope. With the rise of technological complexity of all kinds of products and services, no company could do everything by itself. All the individual pieces, and all the technology to tie it together, were too much for one company to handle. During the 1990s, in-licensing a bit here and a bit there grew to constitute more of a growing panoply of complex finished products and services. IBM's licensing success was, in large part, driven by this phenomenon.

The Core Role of In-Licensing

RF Micro Devices provides a good example of both the foundational importance of a fundamental kernel of raw IP, but also of the critical and complementary importance of in-licensing. Analog Devices, long a leading semiconductor firm, was going through tough times in 1991. Bill Pratt was one of the engineers the company let go that year. As part of his severance package, Pratt wrangled the rights to some novel IP that he had generated. He had been doing experimental research on a new material, gallium arsenide, to make chips for wireless applications. Pratt used these discoveries to found RF Micro Devices. It was cutting-edge stuff, but a bit too cutting edge. To Analog Devices, it seemed untested, uncertain, and infeasible; the company was happy to let Pratt have it.

Analog Devices was right. Pratt and RF Micro Devices co-founders Jerry Neal and Powell Seymour struggled for years to get the technology to work, but it simply would not cooperate. Defense and aerospace company TRW had something that might help, however. TRW had developed a different, but related technology that it had been using to produce small quantities of chips for satellite communications. In conjunction with RF Micro Devices's technology, the resulting product was simpler and better—it actually worked as advertised. TRW, however, had no particular focus or interest in the wireless market. So, in exchange for in-licensing the technology, RF Micro Devices gave TRW nearly one-third of its equity. It was a steep price, but RF Micro Devices might have failed without the deal. The technology was essential.

RF Micro Devices's experience highlights how licensing inherently entails the sharing of innovation's value. Whoever has the stronger bargaining position, the more rare and essential assets needed to bring an innovation fully to market, can command more of the gains. Sometimes, the licensor is in the stronger position to capture most of the value, and sometimes, the licensee is in the stronger position. This is an inescapable fact, and one of the key strategic and financial caveats of relying on either out-licensing or in-licensing for innovation commercialization. Armed with TRW's in-licensed technology, RF Micro Devices powered forward with its gallium arsenide breakthroughs and went on to become a global leader in wireless communications chips. Needless to say, TRW earned a good return on its investment as well, cashing out a healthy gain when it sold its equity stake. For RF Micro Devices, in-licensing was the critical key it needed to unlock the value of the innovation it had been working on for years, but could not fully bring to fruition by itself.

The Ins and Outs of In-Licensing

Along with the rise of technological complexity, economies of scale and scope in many industries also soared during the past decade and worked to push the in-licensing trend even further. Increases in scale and scope were not just in R&D, but also in manufacturing and marketing. Bigger scale and scope meant the need for more technology and product to spread out over huge fixed investments. In-licensing offered a ready source. After years of expansion, for example, Big Pharma reached limits to its R&D productivity and desperately needed more drugs to sell through global sales and marketing organizations that had grown ever-larger and more expensive to maintain. In-licensing innovation promised a quick way to fill product pipelines that had been drying up or to otherwise plug holes in their product portfolios.

As important as in-licensing has become, the in-licensing trend itself has sometimes been promoted by questionable assumptions. These assumptions posit in-licensing as not just a compromise, but actually a preferred solution to innovation deficiencies. Don't fret about the lack of productivity of your own R&D labs. Fill the gaps by paying for innovation on the open market through in-licensing deals.

In-licensing is not without risks and costs, however. Just as with any other innovation investments, you get what you pay for. Raw, early stage IP is relatively cheap to license. It also is less proven, more risky, and will take much more time and cash to develop to full commercialization, assuming it does not fail in the process. Later-stage, more fully developed IP (near the actual product stage) might be much less uncertain and feel safer to in-license, but it almost certainly will be exponentially more expensive.

Two of the leading large pharmaceutical companies, Merck and Bristol-Myers Squibb, provide good illustrations of the upsides and downsides of both in-licensing approaches. Merck decided to bet on earlier stage technology by in-licensing a new diabetes drug candidate from Kyorin Pharmaceutical of Japan. The price for the deal was reasonable, but (or, more precisely, because) the compound had not yet been tested in humans. After closing the deal, a troubling longer term assessment of the drug's animal trials came back and Merck suddenly halted human testing. The surprise news dealt a public blow to Merck in the wake of a few other, similarly disappointing announcements just a few months earlier. Earlier stage in-licensing offers greater opportunity at lower cost. But it almost necessarily entails greater uncertainty and risk, and requires much greater additional investment and toil to develop.

Bristol-Myers Squibb seemed to face much less uncertainty when it inked a deal with biotechnology firm ImClone. The September 2001 deal was to license ImClone's revolutionary new cancer drug, Erbitux. By the time of the transaction, Bristol-Myers faced a gnawing shortage of new drugs in its pipeline and patent expirations for some of its key existing products. ImClone's Erbitux seemed a good, safe bet. Based on the positive results of initial trials, the FDA had "fast-tracked" Erbitux and was expected to give final approval shortly. Bristol's own weakened drug pipeline did not put it in the strongest bargaining position, raising the price of the deal. The price tag for such a promising, late-stage drug candidate was quite high. Bristol-Myers paid $1 billion—a 40 percent premium over ImClone's stock price—for a 19.9 percent stake of the company, plus committed another $1 billion in installment payments. Under the agreement, ImClone would still retain the rights to almost 40 percent of Erbitux's net sales or 60 percent of the profits. This was quite a change from the usual 5–15 percent flat royalties that a typical drug-licensing deal might command. Bristol-Myers's deal included the U.S. market, but only joint rights for Japan; Europe was excluded because rights had already been licensed to another firm.

Bristol-Myers's agreement was a blockbuster deal, but mostly for ImClone. For its part, ImClone's rich deal represented the value of more than 15 years of expensive and extensive R&D behind Erbitux and huge market potential ahead of it, as it was just on the cusp of final FDA approval. ImClone was licensing a valuable, nearly finished product, not just raw IP. Even this late-stage deal was not entirely without risk, however. In December 2001, the FDA surprised Bristol-Myers by refusing to let Erbitux move forward, citing the need for ImClone to provide more and better clinical data. Bristol-Myers was caught in the downdraft. The sustained, hard slide in its share price reflected not just this single piece of disappointing ImClone news, but it also reflected skittishness at how dependent Bristol-Myers had become on such expensive and lopsided licensing deals. In-licensing is not without considerable costs and risks under even the best conditions.

The Ambiguity of Intangibles

IP licensing carries other risks and costs as a model for either sourcing or commercializing innovation. These risks and costs are not at all a reason to shun the strategy, but they are reason to proceed with proper due diligence. Ultimately, licensing is a legal agreement between two parties regarding property rights. Ownership and control of such intangible property can be slippery concepts; licensing rights are subject to interpretation and dispute. What geographic territory is covered by the licensing agreement: U.S., Europe, Japan, the world? For what specific application (for example, for what specific product or use)? In what specific shape, form, or formulation? Does the licensing agreement cover just a basic drug, for example, or does it also include derivatives such as extended-release and prolonged-action versions of the drug?

These might seem like trivial issues, but they're not. They can result in disputes with multibillion-dollar implications. The drawn-out battle between Amgen and Johnson & Johnson over their co-developed anemia drugs is one of the more hotly contested licensing battles. More such battles are a virtual certainty in a wide variety of industries as the New Economy, and the role of IP in it continues to grow and evolve.

In 1985, Johnson & Johnson agreed to acquire the rights to co-develop, manufacture, and market the genetically engineered anemia drug, erythropoietin (Epogen), from biotech startup Amgen. The deal covered U.S. rights to use the drug for general anemia and for all uses in Europe. Amgen retained all domestic marketing rights for kidney dialysis patients. The drug also held enormous promise for alleviating anemia in cancer patients (typically a result of chemotherapy) and other indications. By 1989, just as final FDA approval for Epogen seemed imminent, Chugai Pharmaceutical of Japan starting exporting its own version of erythropoietin, licensed from Genetics Institute in Boston, to the U.S. Amgen locked into fierce legal action in patent disputes with both Genetics Institute and its partners.

What was more curious was the action of Amgen's own licensee, Johnson & Johnson. Unexpectedly, Johnson & Johnson took legal action of its own against Amgen. Johnson & Johnson filed suit to stop Amgen from going to market with Epogen. With Amgen first to market, Johnson & Johnson feared that physicians would begin prescribing Amgen's Epogen "off-label" for various conditions besides kidney dialysis, shrinking Johnson & Johnson's market potential and market share. Johnson & Johnson accused Amgen of purposefully dragging its feet in helping get Johnson & Johnson's identical version of the drug, Procrit, approved and to market.

In turn, Amgen had its own complaint. Amgen discovered that Johnson & Johnson intended to pursue the broader U.S. anti-anemia market, not just for cancer and related conditions. Johnson & Johnson clearly intended to target the renal (kidney) market that Amgen thought it had contractually reserved for itself in its licensing agreement. Amgen had used the term "dialysis" in its agreement with Johnson & Johnson, intending it as shorthand to generally refer to kidney-related disease. Johnson & Johnson saw the agreement differently and more literally. For Johnson & Johnson, everyone except patients actually currently using dialysis was fair game for its version of epo, Procrit. Amgen feared that Johnson & Johnson would hook doctors of early stage (pre-dialysis) renal patients and then keep them in its fold with Procrit, cutting directly into Amgen's own Epogen dialysis-patient market.

Amgen won its suit against Genetics Institute in 1991. However, the battle with its licensing partner, Johnson & Johnson, intensified as Procrit received FDA approval in 1991, 19 months after Epogen itself. Licensor and licensee were now their own chief competitors. During the next few years, Johnson & Johnson prevailed in most of its legal disputes; Amgen was ordered to pay it hundreds of millions as a result. The dispute's intensity was for good reason. Epo quickly became the most successful biotechnology drug ever introduced. Within just a few years of its introduction, it was a billion-dollar plus drug for both Amgen and Johnson & Johnson.

The licensor-licensee battle took on new dimensions by the end of the decade. In 2001, Amgen had a chance to turn the tables on Johnson & Johnson when the FDA approved Amgen's new, long-acting version of erythropoietin, Aranesp. Johnson & Johnson argued that Aranesp was simply a refined version of the original Epogen and therefore was governed by the original licensing agreement. Amgen disagreed, claiming Aranesp was an altered molecule covered by different patents and therefore outside of the original license. Amgen prevailed in arbitration, winning sole rights to Aranesp. This was not an inconsequential issue for Johnson & Johnson; Procrit accounted for about 20 percent of Johnson & Johnson's earnings by 2002. Amgen's Aranesp quickly gained market share and sharply curbed Procrit's sales. Within two years of its launch, Aranesp already was a billion-dollar plus blockbuster for Amgen, with no share for Johnson & Johnson.

Fortunately, the blockbuster success of epo made it mostly a win-win for both parties, despite all the fierce legal, financial, and marketplace battles. Such situations are not always win-win. Even in the most successful deals, licensing presents unique challenges for both licensor and licensee because of the ambiguous and contestable nature of IP itself. These are problems that the outsourcing of innovation through licensing inherently raises for both licensor and licensee.

In-Licensing: Hollowing Out the Core?

Going it alone truly is increasingly less feasible. In-licensing therefore might be necessary in many situations. Over time, however, relying too much on in-licensing to address core innovation challenges can be a more and more uncertain, unstable, and unsustainable proposition. In the pharmaceutical industry, for example, by 2003 almost half of the biggest blockbuster drugs were not developed by their Big Pharma marketers and instead were in-licensed or otherwise acquired from outside. This situation led some investors and other observers to ask some serious questions: To what end was all the record-setting R&D investment of Big Pharma in recent years? Despite a tripling of R&D spending to more than $30 billion over the past decade and despite a "fast-track" overhaul of the FDA approval process, by 2003, Big Pharma was bringing new drugs to market in the U.S. at the slowest rate in a decade. This was especially the case for truly new therapies, not just "me, too," copycat drugs. A December 2003 study by Bain claimed that, because of the combination of soaring expenses and declining productivity, the return on investment (ROI) on Big Pharma's internally developed new drugs had plunged to just 5 percent. The ROI of Big Pharma's in-licensed new drugs was not much better, at just 6 percent. In their increasingly desperate bid for new drugs, Big Pharma had pushed up the price of licenses and incurred increased co-development and marketing costs at the same time. For neither internal development nor licensing did it seem that ROI was anywhere near the risk-adjusted cost of capital.

The bottom line is that in-licensing is useful, often critical, as part of a more comprehensive innovation strategy. By itself, however, in-licensing is not a simple, comprehensive solution to the core challenges of innovation. While out-licensing raw IP offers limited value creation and value capture and limited sustainability, over-reliance on in-licensing can lead to the hollowing out of a firm's core innovation capabilities. This, in turn, can lead to an ever-weaker position versus licensors, higher (more desperate) prices for licenses, and ultimately less competitiveness and decreased returns, potentially starting a vicious cycle.

Bottom Line: How Real Is the IP Revolution?

So how real is the virtual revolution of innovation as IP licensing? Is out-licensing IP a workable business model for innovation commercialization or is it an inherently limited strategy? Is aggressive in-licensing a sign of nimble prowess in navigating the technology challenges of the New Economy or is it a sign of R&D weakness, a second-class approach to innovation?

The bottom line is that most of the IP-focused innovation movement is quite real—with a few key caveats. Even most of the richest IP licensing companies continue to generate these returns as derivatives or byproducts of their massive, ongoing core R&D efforts. They have not transformed themselves into purely or even primarily virtual, asset-lite, knowledge-based IP licensors. Although exceptions exist, proactive IP management and IP licensing tools and tactics are critically necessary complements to, but not substitutes for, a more comprehensive core innovation strategy. In the vast majority of cases, a "virtual" strategy—relying solely or primarily on either out-licensing or in-licensing—simply will not allow a firm to either create or capture most of the value from innovation.

Nonetheless, smart IP management is no longer optional; it is a necessity. This is true if only in defense (i.e., the best defense is a good offense). Both private and public investors will shy away from startups or mature firms alike if they do not have their IP portfolios clearly and aggressively ordered and protected. Potential partners will not partner with a firm whose IP assets are of ambiguous defensibility, and customers might shun such firms for more certain and safe suppliers. IP management has become a top management concern, not just a legal issue, and a necessary cost of doing business.

To offset these IP management costs, it makes sense to try to actively generate offsetting revenue from IP as well. If the organization's IP portfolio has sufficient scale and scope, establishing a substantial internal IP management division and staff might make sense as long as the proceeds exceed the costs. Accounting can get complicated in these situations, however, as the firm's operating businesses typically have funded most of the R&D. Much of the enthusiasm for IP licensing neglects these sorts of issues (such as billions and decades of cumulative R&D) and treats IP revenues as if they were just an unexpected windfall rather than returns to considerable investments.

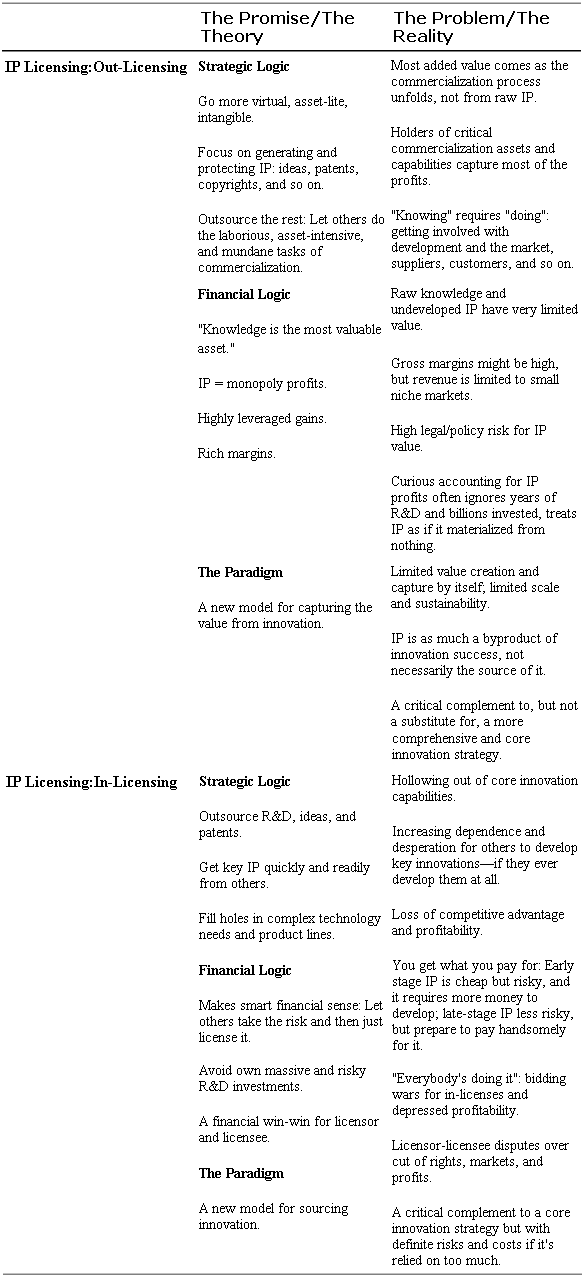

If an organization's IP portfolio lacks scale on its own merits and represents non-core assets, outsourcing much of the footwork might make good sense. An entire industry of advisors and consultants exists specifically for these purposes: Acorn Technologies, InteCap, IPValue, Product Genesis, ThinkFire, and so on. Either fee-based or gain-sharing relationships can be set up to let parent company executives focus on their core businesses while their partners and advisors focus on seeking and closing licensing and other IP commercialization deals. Even larger organizations with great stores of IP have found such assistance to be useful. In 2003, for example, Xerox signed a 5-year agreement with IPValue, making them a worldwide agent for external commercialization of Xerox's IP assets. Such deals can help keep IP management and licensing from becoming an undue distraction that detracts from a firm's core innovation and thereby destroys value overall. Core innovation must be the main game; IP management and licensing need to support, not detract from, this primary goal (see Table 3-1).

Table 3-1. IP and Licensing: A New Model for Innovation?

The Future of Innovation as IP Licensing

Beyond the caveats previously discussed, the future of an IP-centric model remains unclear in many ways. The increasing rapidity of technological progress means that technology lifecycles continue to be compressed, making a 20-year patent commercially valuable for as little as just a few years. New technologies and patents might leapfrog old ones even before R&D costs are recouped. The business of "inventing around" and otherwise (quite legally) mimicking IP also continues to flourish. Even a good patent is no longer necessarily much of an effective monopoly. Pfizer's Viagra was a successful new product, for example, but it did not take long before the introduction of Levitra and Cialis seriously slashed into its market share.

Moreover, the concept and future of IP itself remains in flux. This is not a trivial issue for an IP-only innovation strategy. All the profits from IP flow solely from governments' willing recognition and enforcement of patents as officially sanctioned monopolies. The trend is not unidimensionally for increasing IP protection. In many cases, the trend actually is toward considering weakening such restrictions.[8] Even some ideological free marketeers note that a "patent-anything-and-everything" mania threatens to stifle innovation more than foster it and otherwise harm the public good. Courts, regulators, and legislatures have not been deaf to such concerns, whether in regard to software, creative content, or medicine.

In most of the world outside the U.S., for example, IP protection has tended to grow and strengthen. However, it still remains relatively weak and varied. Emerging markets remain huge consumers of U.S. firms' IP, although most of it nets the IP "owners" little or nothing. Europe hesitates to endorse software patents, much less the rest of the world recognizing and enforcing U.S. companies' patents on the human genome. Poorer countries continue to feel a right and an imperative, for both social and economic reasons, for more lax or varied IP protections. Ill citizens earning $500 or even $5,000 per year, for example, cannot afford $5,000 or $15,000 worth of patented HIV drugs annually. U.S. IP standards and practices are not the only ones, and no predestination states that they will prevail globally. Both domestically and abroad, more public and private stakeholders resist high "tolls" companies charge for patents that, of course, are granted and enforced at the discretion of their governments in the first place.

In an increasingly global economy, these issues cannot be ignored. The more a company pursues an IP-centered innovation model, the more the outcomes of these legal and policy debates will outright determine company success or failure. The policy and legal risks for IP-centric firms are enormous, with the very real possibility of abrupt, value-vaporizing downsides. Genomics stocks reeled in early 2000, for example, after Bill Clinton and Tony Blair's offhand observations about the need to freely disseminate to humanity the decoded human genome data.

Regardless of these persistent uncertainties and unforeseen changes, IP has assumed greater importance in the New Economy now and for the foreseeable future. The intangible, knowledge-based content of the U.S. and global economies will continue to increase. Technological complexity and economies of scale and scope will continue to push companies to more actively license (both in- and out-license). Smart and aggressive IP management strategies will be essential for helping capture more of innovation's value. In this sense, the enthusiasts for an IP-centered model of innovation had a very real case, even if sometimes overstated. This new approach is only part of a continuing evolution, however, not a revolution. For most firms, IP licensing will remain a critical part of a more comprehensive innovation strategy, not an entirely new innovation model on its own.