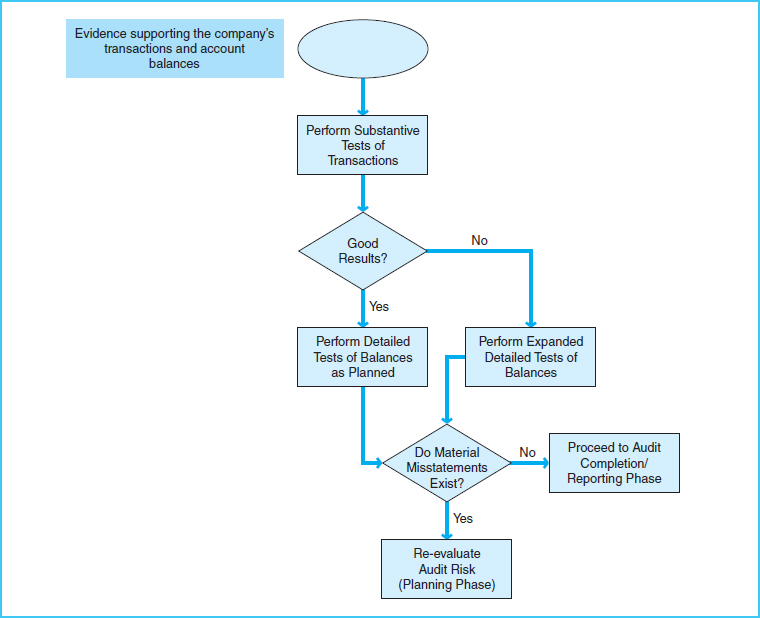

TESTS OF TRANSACTIONS AND TESTS OF BALANCES (STUDY OBJECTIVE 9)

The auditor's tests of the accuracy of monetary amounts of transactions and account balances are known as substantive testing. Substantive testing is very different from testing controls. Substantive tests verify whether information is correct, whereas control tests determine whether the information is managed under a system that promotes correctness. Some level of substantive testing is required regardless of the results of control testing. If weak internal controls exist or if important controls are not in place, extensive substantive testing will be required. On the other hand, if controls are found to be effective, the amount of substantive testing required is significantly lower, because there is less chance of error in the underlying records. Exhibit 7-9 presents a process map of the substantive testing phase of the audit.

In an IT environment, the evidence needed to determine the correctness of transactions and account balances is contained in electronic data files within the computer system, from where it may be pulled by specialized audit techniques. Some techniques used to test controls can also be used to test transactions and financial statement balances. For example, parallel simulations, the test data method, the embedded audit module, and the integrated test facility can be used for both control testing and substantive testing.

Recent trends such as advances in automated controls; new compliance requirements; integration of governance, risk management, and compliance (GRC) activities; and real-time financial reporting have created the need for continuous auditing. Continuous auditing, or continuous monitoring, is a process of constant evidence-gathering and analysis to provide assurance on the information as soon as it occurs or shortly thereafter. It can be performed by management or auditors.

Exhibit 7-9 Substantive Testing Phase Process Map

When companies use automated controls and maintain critical business information in electronic form, auditors can analyze the relevant data throughout the period. Continuous monitoring of internal controls is important so that control deficiencies can be detected before they become significant. Exceptions can be evaluated and corrected in time to improve operational performance and avoid reporting issues. Chapter 15 discusses how ERP systems can be used to monitor internal controls.

Continuous auditing techniques, such those available with the embedded audit module approach, are a very popular form of substantive testing. When companies use e-commerce or e-business systems to conduct business online, auditors know that financial accounting information is produced in real time and is immediately available for auditing purposes. The SEC, PCAOB, and AICPA also approve of the use of continuous auditing. In response to corporate failures, such as those at Enron and WorldCom, continuous auditing helps auditors stay involved with their client's business and perform audit testing in a more thorough manner.

Continuous auditing generally requires that the auditors' access their client's systems online so that audit data can be obtained on an ongoing basis. Audit data are then downloaded and tested by auditors as soon as possible after the data are received.

Most auditors use generalized audit software (GAS) or data analysis software (DAS) to perform audit tests on electronic data files taken from commonly used database systems. These computerized auditing tools make it possible for auditors to be much more efficient in performing routine audit tests such as the following:

- Mathematical and statistical calculations

- Data queries

- Identification of missing items in a sequence

- Stratification and comparison of data items

- Selection of items of interest from the data files

- Summarization of testing results into a useful format for decision making

The use of GAS or DAS is especially useful when there are large volumes of data and when there is a need for correct information. These programs allow audit tests to be completed quickly, accurately, and thoroughly, therefore providing auditors with a way to meet the growing needs of decision makers who expect precise, immediate information.