CHAPTER 14

Corporate Debt and Credit Default Swaps

Corporations borrow money to fund their operations, transactions (e.g., mergers and acquisitions), and changes to capital structure (e.g., refinance existing debt, stock repurchases). The loans and bonds used to raise these funds are subject to credit risk, because corporations may not make good on their promises to pay interest and repay principal. Lenders, in turn, require compensation for bearing credit risk in the form of higher returns. The cash flows of credit default swaps (CDS) also depend on the payment or nonpayment of debt obligations but are not themselves obligations of corporate issuers. In other words, through CDS contracts, market participants trade corporate credit risks with each other. While this chapter focuses mostly on corporate debt, much of the discussion applies to sovereign and municipal debt as well, because the debt obligations of many governments have at times been perceived as subject to nontrivial probabilities of default.

Many market participants rely to some extent on rating agencies to measure the credit risk of borrowers and their loans and bonds. The long‐term debt ratings classifications of the three major rating agencies in the United States are given in Table 14.1. More granular breakdowns of each of these broad ratings classifications are also available, and short‐term debt has its own, separate scales.1

TABLE 14.1 Long‐Term Debt Ratings Classifications. The Ratings in Each Entry Are Listed in Decreasing Order of Creditworthiness.

| Speculative Grade/ | |||

|---|---|---|---|

| Agency | Investment Grade | High Yield | Default |

| Moody's | Aaa, Aa, A, Baa | Ba, B, Caa, Ca | C |

| S&P, Fitch | AAA, AA, A, BBB | BB, B, CCC, CC, C | D |

14.1 CORPORATE BONDS AND LOANS

Large and highly creditworthy corporations in the United States tend to borrow money for fixed terms in public markets through commercial paper (CP), medium‐term notes (MTNs), and corporate bonds. CP is typically a discount (i.e., zero coupon) instrument that is either unsecured, backed by a letter of credit from a bank, or secured by assets. CP is exempt from Securities and Exchange Commission (SEC) registration, along with its associated costs, so long as the paper matures in less than 270 days and its proceeds are used for short‐term purposes (rather than, for example, building a factory). With its high credit quality and short‐term maturity, CP is a particularly inexpensive and liquid way for the most creditworthy corporations to raise short‐term funds. CP borrowing does, however, expose a corporation to the funding or liquidity risk of having to roll outstanding CP as it matures into new CP issues.

Corporations sell MTNs in public markets to raise money with customized payment terms. Historically, MTNs primarily filled the maturity gap between CP and longer‐term bonds but are now better characterized as debt instruments customized to suit the needs of individual issuers and investors. MTNs first became popular in the United States in the early 1980s, with the introduction of SEC shelf registrations. These programs allow issuers to register once to sell notes opportunistically, over time, at terms that can be adjusted at the time of each sale.

For longer‐term borrowing in public markets with relatively standard payment terms, corporations sell bonds, which, in the United States, have to be registered with the SEC. Corporate bonds are typically coupon‐bearing, fixed‐rate securities, but there is a much smaller market for floating‐rate notes (FRNs). The interest rate on FRNs is typically set equal to a short‐term reference rate plus a fixed spread, although a reference rate might be multiplied by a factor or leverage, and the spread might vary over time with the credit rating of the issuer. The short‐term reference rate for FRNs had traditionally been the London Interbank Offered Rate (LIBOR) but is now transitioning to the Secured Overnight Financing Rate (SOFR) and other non‐LIBOR alternatives (Chapters 12 and 13).

Smaller and less creditworthy corporations, which cannot typically raise funds in public markets, tend to borrow money through private placements of bonds and through bank loans. In a privately placed bond issue, the borrower tailors terms to satisfy its own requirements and those of a relatively small group of lenders. Insurance companies are the most significant investors in this market, though other asset managers participate as well. Privately placed bonds are exempt from SEC registration precisely because they may be sold only to investors deemed “sophisticated.”

Bank loans tend to be floating‐rate instruments, although borrowers sometimes convert their debt into a fixed rate by paying fixed to and receiving floating from a bank in an accompanying interest rate swap, which the bank, in turn, hedges with a dealer (Chapter 13). From the bank perspective, floating‐rate loans have the advantage of matching floating‐rate liabilities, which are mostly deposits, but also include wholesale funding like commercial paper. Also, floating‐rate loans are the easiest to sell in the secondary market for bank loans.

Traditionally, banks made loans and held them to term. And if a single borrower needed a loan that was too large for one bank, either because funds were not readily available or, more likely, because the resulting credit risk would be too significant for one bank, several banks would form a group or syndicate in which each would make and hold a smaller loan to that large borrower. The last few decades, however, have seen phenomenal growth in the secondary market for loans, which allows banks to sell loans they have made to institutional investors. In this way, banks can earn fees on making, servicing, and monitoring loans without having to warehouse all of the associated credit risk. At present, in fact, the overwhelming majority of relatively low‐quality or leveraged loans are held not by banks, but by institutional investors. While some leveraged loans are bought from banks directly by insurance companies, mutual funds, and hedge funds, much of the growth of the secondary market for bank loans has been through the indirect sale of loans to institutional investors through collateralized loan obligations (CLOs).

Collateralized Loan Obligations

A CLO is a vehicle that purchases a portfolio of leveraged loans financed by the sale of several debt classes or tranches and equity or subordinated notes. Table 14.2 lists the debt tranches of a particular CLO issued in May 2019. Essentially, interest and principal payments from the underlying portfolio of leveraged loans flow to the tranches from the top down, while any credit losses are allocated from the bottom up.2 Senior Secured Floating‐Rate Note Classes X, A‐1, A‐2, and B are paid interest and principal from the underlying loans, while Mezzanine Secured Deferrable classes C, D, and E are paid to the extent that additional cash flows from the underlying loans are available. Any credit losses from the underlying loans are first applied to the equity or Subordinated Notes, then to the Mezzanine tranches, and only then, if necessary, to the Senior Secured tranches. Furthermore, CLO debt tranches are protected by constraints imposed on the creditworthiness of the underlying loans and on the concentration of loans to a particular borrower or industry, along with various ongoing tests as to the sufficiency of interest and collateral. In short, this CLO, from an underlying portfolio of $634,125,000 leveraged loans, created $414,225,000 of X, A‐1, and A‐2 tranches with AAA or Aaa ratings; an additional $64,600,000 B tranches with an AA rating; and so forth.

TABLE 14.2 Tranches of Apidos CLO XXXI, May 2019. All Tranches Mature in April 2031.

| Amount | Rating | Spread over | ||

|---|---|---|---|---|

| Class | Description | ($millions) | S&P/Moody's | LIBOR (bps) |

| X | Sr. Secured FRNs | 4.725 | AAA/– | 65 |

| A‐1 | Sr. Secured FRNs | 370.150 | AAA/Aaa | 133 |

| A‐2 | Sr. Secured FRNs | 39.350 | –/Aaa | 165 |

| B | Sr. Secured FRNs | 64.600 | AA/– | 190 |

| C | Mezzanine Secured Deferrable FRNs | 40.300 | A/– | 255 |

| D | Mezzanine Secured Deferrable FRNs | 36.200 | BBB–/– | 365 |

| E | Mezzanine Secured Deferrable FRNs | 27.400 | –/Ba3 | 675 |

| – | Subordinated Notes | 51.400 | – | – |

| Total | 634.125 | |||

Compensation for buying lower‐rated tranches comes in the form of earning a higher spread. As shown in the last column if Table 14.2, spreads range from 65 basis points for the AAA‐rated X Class to 675 basis points for the Ba3‐rated Class E tranche.3 The return on equity, of course, is determined by whatever is left over after paying all of the more senior claims.

The different credit risk profiles of the different tranches in a CLO tend to attract different groups of investors. Banks tend to hold or purchase the AAA/Aaa and AA/Aa tranches; insurance companies and pension funds invest in a range of tranches; and hedge funds and alternative asset managers buy the lower‐rate tranches. Outside investors and the CLO originators hold the equity.

By way of summarizing trends over the last few decades, the growth of the secondary market for leveraged loans, abetted by the CLO market, has blurred the distinction between leveraged loans and high‐yield bonds. Corporations have greater flexibility to borrow in one market or the other, and asset managers actively decide to invest in one market or the other, with all choices depending on individual preferences or requirements and on market conditions.

Seniority, Covenants, and Call Provisions

When selling a debt issue, a corporation enters into a contract with bondholders, called an indenture, which is enforced by a trustee. Aside from payment terms (e.g., interest, principal, and maturity), the indenture specifies the priority of the issue in the event of default. For example, one bond issue might be secured by a particular set of assets; a second might be unsecured, but “senior” to other issues; and a third might be “subordinated” to higher‐ranking issues. In this example, should a corporation be reorganized or liquidated through bankruptcy according to “strict priority,” proceeds from selling ring‐fenced assets would be applied first to satisfy the claims of the secured bondholders. Any remaining proceeds, together with other assets of the corporation, would be applied next to satisfy the claims of the senior bondholders. Finally, whatever value remains would be used to satisfy the claims of the subordinated bondholders. In practice, because reorganizations involve negotiation and include equity holders, strict priority may not always precisely predict the settlement of debt claims.

Indentures also include covenants to protect the claims of bondholders. Examples include maintaining various financial ratios; restricting the amount of cash that can be paid to stockholders; requiring a corporation to repurchase a debt issue after a change of control; limiting the total amount of new debt incurred by the corporation; and preventing the sale of debt with higher seniority than that of an outstanding debt issue.

As a final point of discussion, indentures often include call provisions or embedded call options, which allow a corporation to repurchase bonds from bondholders at some fixed schedule of prices. A simple example would be a 20‐year bond that the company can repurchase at par or face value anytime after 10 years. A more complex example would be a 4% 30‐year bond that the company can repurchase after 10 years at a price of 102 (100 plus half the coupon); at a price of 101.90 after 11 years; at a price of 101.80 after 12 years.

The original purpose of call provisions was to enable corporations to extinguish a bond issue – without having to track down and purchase every outstanding bond – perhaps to remove covenants that prohibited what had become value‐added activities, or perhaps to change the corporation's existing capital structure. As interest rates became more volatile in the early 1980s, these call provisions became valuable as interest rate options: the value of the right to purchase a bond at some fixed price increases as rates decline (bond prices increase) and also as rate volatility increases. At the same time, of course, corporations issuing debt with call provisions have to pay investors for that option through a higher coupon rate. Chapter 16 describes the pricing of these call provisions.

TABLE 14.3 Call Provision of the Hertz 6s of 01/15/2028. The Bond Was Issued in November 2019.

| Dates | Call Price |

|---|---|

| Before 01/15/2023 | Make‐Whole Price |

| Treasury 2.75s of 02/15/2028 +50bps | |

| 01/15/2023 to 01/14/2024 | 103.00 |

| 01/15/2024 to 01/14/2025 | 101.50 |

| On or after 01/15/2025 | 100.00 |

Since the mid‐1990s, however, the most common call provision has become the make‐whole call. For example, in a private placement in November 2019, Hertz sold the 6s of 01/15/2028, with the make‐whole call provision described in Table 14.3. Before January 15, 2023, Hertz can repurchase the bonds from investors at a yield 50 basis points above the yield of the US Treasury 2.75s of 02/15/2028. From January 15, 2023, on, the call is at the schedule of fixed prices shown in the table. The idea behind the make‐whole call is to give the issuer flexibility to manage its debt without its having to purchase an expensive interest rate option. Unlike the case of a call price that is fixed, when yields fall, the yield of the Treasury benchmark falls too, and the make‐whole call price increases. Hence, the interest rate option value of the make‐whole call is extremely limited. In fact, in theory, the make‐whole call has option value only if the market spread of the Hertz bonds over Treasuries falls: in that scenario, the value of the Hertz bond increases without a corresponding fall in the yield of the Treasury bond and a corresponding increase of the make‐whole price. In practice, however, the value of this spread option is mitigated by setting the make‐whole spread out‐of‐the‐money. For example, when Hertz issued the 6s of 01/15/2028 in November 2019, its spread over the Treasury benchmark was 423 basis points. This means that its bond spread would have to fall a very large ![]() or 373 basis points before the make‐whole provision was in‐the‐money as an option on spread. Overall, of course, the call provision of the Hertz 6s of 01/15/2028 derives option value from the schedule of fixed call prices from January 15, 2023.

or 373 basis points before the make‐whole provision was in‐the‐money as an option on spread. Overall, of course, the call provision of the Hertz 6s of 01/15/2028 derives option value from the schedule of fixed call prices from January 15, 2023.

14.2 DEFAULT RATES, RECOVERY RATES, AND CREDIT LOSSES

While investors in nearly risk‐free government bonds can focus exclusively on interest rate risk, investors in corporate securities have to focus on credit risk as well, often expressed in terms of default rates, recovery rates, and credit losses. After analysis, an investor might estimate that, over a five‐year horizon, a particular portfolio of bonds will experience a default rate of 10%, meaning that, for every $100 of face amount, $10 will default. Furthermore, the investor might estimate that the defaulting bonds in the portfolio will experience a recovery rate of 40% of face amount, or, equivalently, will suffer a loss equal to the remaining 60% of face amount. Putting these two estimates together, the investor expects, over a five‐year horizon, that credit losses on the portfolio will be ![]() .

.

Table 14.4 shows average historical values for these quantities, over the period 1983–2020, for senior unsecured bonds, by rating. The results are useful for appreciating the average magnitude of credit risk. For investment‐grade senior unsecured bonds, the average five‐year default rates and recovery rates are 0.9% and 44.5%, respectively, giving an average credit loss of 0.5%. For speculative‐grade senior unsecured bonds, the average default rate is much higher, at 19.6%, though the average recovery rate is only marginally lower, at 38.3%. Combining these two averages gives a much higher credit loss of 12.2%. The standard assumption in the industry that recovery rates are about 40% is justified by historical data like those presented in Table 14.4.4

While historical averages are useful in thinking about credit risk, credit conditions can vary dramatically over time. For example, extending the sample of Table 14.4 to include the years after the Great Depression raises the five‐year default rate on investment‐grade debt from 0.9% to 1.4%. And within the sample period of the table, Figure 14.1 shows the variability of credit losses for investment‐grade and high‐yield bonds. High‐yield losses were particularly high in the late 1980s, following the rapid growth in that market; in 2000–2002, which included the “dot‐com” crash and the failures of Enron and WorldCom; in the financial crisis of 2007–2009; in 2016, from stresses caused by low prices in energy markets; and, most recently, during the pandemic and economic shutdowns of 2020.

TABLE 14.4 Average Five‐Year Default Rates, Senior Unsecured Bond Recovery Rates, and Credit Losses, 1983–2020. All Entries Are in Percent.

| Default | Recovery | Credit | |

|---|---|---|---|

| Rating | Rate | Rate | Loss |

| Investment Grade | 0.9 | 44.5 | 0.5 |

| Speculative Grade | 19.6 | 38.3 | 12.2 |

| All | 7.4 | 38.9 | 4.6 |

Source: Moody's Investors Service

FIGURE 14.1 Credit Losses for Senior Unsecured Bonds, 1983–2020.

Source: Moody's Investors Service.

Table 14.4 and Figure 14.1 report credit losses for senior unsecured bonds. Investment outcomes vary significantly, however, across loans and bonds of different seniority. Over the same sample period as in the table and figure, Moody's reports that bond recovery rates were 22% for junior subordinated; 38% for senior unsecured; and 54% for first lien (i.e., the highest priority secured claim). For bank loans, average recovery rates were 46% for senior unsecured; 65% for first lien; and 32% for second lien.

A recent example of the impact of seniority, illustrated in Table 14.5, is the price behavior of Hertz bonds through its bankruptcy filing on May 22, 2020. Before the pandemic, as of February 21, 2020, when default was a remote contingency, the prices of Hertz' secured and unsecured bonds were above par, with the higher price of the unsecured reflecting its longer maturity at an above‐market coupon. By May 14, 2020, after the pandemic and shutdowns devastated the rental car business, the prices of Hertz bonds plummeted, with the price of the secured bond now significantly higher: with default imminent, the seniority of the secured bonds was much more important than the seemingly distant prospect of the unsecured bond's cash flows through 2028. Soon after, however, in the wake of the economy's rapid recovery, Hertz's bond prices recovered dramatically as well. There was still much uncertainty as to the bonds' creditworthiness, however. The June 15, 2020, prices in the table show that the secured bonds still sold at a significant premium to the unsecured. By way of epilogue, Hertz emerged from bankruptcy at the end of June 2021, and its bonds recovered their full principal value.

TABLE 14.5 Hertz Corporation, Selected Bond Prices on Three Dates in 2020.

| Priority | Coupon | Maturity | Feb 21 | May 14 | Jun 15 |

|---|---|---|---|---|---|

| Sr. Secured 2nd Lien | 7.625 | 06/01/2022 | 103.10 | 19.97 | 77.00 |

| Sr. Unsecured | 6.000 | 01/15/2028 | 104.29 | 11.25 | 43.50 |

Potential credit losses are directly relevant for investors expecting to hold bonds to maturity. Investors with shorter horizons, however, are also concerned about credit deterioration, which causes bond prices to fall before a realized default and credit loss. One manifestation of credit changes are rating transitions, in which a rating agency upgrades or downgrades a rating. Table 14.6 gives average historical one‐year transition rates, or, more specifically, the rates at which bonds starting at a particular rating, over the following year, are upgraded, experience no change, are downgraded (including defaults), or become unrated. Becoming unrated may be a negative credit event but could also indicate a credit‐neutral event like an acquisition. In any case, the table shows that downgrades over a one‐year horizon are not uncommon, averaging from about 4% to 10% for bonds rated B or above, and over 28% for CCC/C‐rated bonds. Upgrades occur as well, but with less frequency. Though not shown in the table, upgrades and downgrades vary with the business cycle, like the credit losses in Figure 14.1.

TABLE 14.6 Average One‐Year Transition Rates, 1981–2020. All Entries Are in Percent.

| Rating | Upgrade | No Change | Downgrade | No Rating |

|---|---|---|---|---|

| AAA | 0.0 | 87.1 | 9.8 | 3.1 |

| AA | 0.5 | 87.2 | 8.4 | 3.9 |

| A | 1.6 | 88.6 | 5.4 | 4.4 |

| BBB | 3.3 | 86.5 | 4.3 | 5.9 |

| BB | 4.7 | 77.8 | 8.0 | 9.5 |

| B | 4.8 | 74.6 | 8.3 | 12.3 |

| CCC/C | 13.3 | 43.1 | 28.3 | 15.3 |

Source: S&P Global Ratings; and Author Calculations

14.3 CREDIT SPREADS

Credit spreads are the differences between the relatively high rates earned on fixed income instruments that are subject to credit risk and the relatively low rates on instruments with little or no credit risk. The simplest measure of credit spread is the yield spread, which is the difference between the yield on a bond and the rate or yield on a similar maturity interest rate swap or highly creditworthy government bond. Yield spreads, however, suffer from a number of drawbacks. First, a sufficiently liquid government bond or swap with a similar maturity might not exist. Second, yields reflect not only credit risk, but also the structure of a bond's cash flows. (See the discussion of the “coupon effect” in Chapter 3.) Third, yields reflect the value of embedded options, like the fixed‐price call provisions discussed earlier, which have nothing to do with credit risk.

A better measure of credit spread is referred to in this chapter as the bond spread. This term includes the spread defined in Chapter 3 and the more general option‐adjusted spread (OAS) defined in Chapter 7. In the credit context, a bond spread is computed by assuming no default and finding the spread over a benchmark curve that prices a bond as it is priced in the market. Because the market price incorporates the risk of default while this pricing methodology does not, the bond spread is a metric of credit risk. Unlike yield spreads, bond spreads properly account for maturity and the structure of cash flows. This approach, therefore, is suitable for bonds without embedded options. For bonds with embedded options, OAS is more appropriate: by design, its computation of price accounts for the value of embedded options and, therefore, any remaining spread to the benchmark curve can be reasonably attributed to credit risk. Furthermore, as explained in Chapters 3 and 7, the bond spread and OAS can be interpreted as the extra spread earned by a bond if interest rates are unchanged or hedged against; if the spread is unchanged; and if the bond does not default.

The measures of credit spread in this section are illustrated with the Genworth 4.90s of 08/15/2023, a speculative‐grade bond issued by an insurance company. Table 14.7 gives various measures of credit spread for this bond, as of August 15, 2021, when the 4.90s of 08/15/2023 have exactly two years to maturity. Given the market yield of 5.596% and the two‐year LIBOR swap rate of 0.288%, the yield spread is the difference between those two rates, or 530.8 basis points. The bond spread, given the bond's market price of 98.70 and the term structure of forward swap rates as of the pricing date, is 531.1 basis points.5 Then, in the sense of the previous paragraph, the Genworth bond earns an annual rate of LIBOR plus 531.1 basis points.

TABLE 14.7 Selected Credit Spreads for the Genworth 4.90s of 08/15/2023, as of August 15, 2021. The Price of the Bond is 98.70; Its Yield is 5.596%; and the Par Swap Rate Is 0.288%. Spreads Are in Basis Points.

| Spread Type | Spread |

|---|---|

| Yield Spread | 530.8 |

| Bond Spread | 531.1 |

| Par‐Par Asset Swap Spread | 526.4 |

| Market Value Asset Swap Spread | 533.3 |

Other popular measures of spread are asset swap spreads. The point of an asset swap is to transform a fixed‐rate, coupon bond into an asset that earns a spread over a short‐term rate, like LIBOR. In the context of this chapter, asset swaps enable investors to earn credit spreads without having to bear the interest rate risk of long‐term, fixed‐rate bonds.

Figure 14.2 illustrates one type of asset swap, the par‐par asset swap, or, more simply, the par asset swap. Thin lines indicate cash flows at the initiation of the asset swap; heavy lines indicate intermediate cash flows; and dashed lines indicate cash flows at the maturity of the swap. At initiation, the asset swapper buys the bond for ![]() per 100 face amount, earning a periodic coupon payment of

per 100 face amount, earning a periodic coupon payment of ![]() . The purchase price is financed with 100 from the repo desk and

. The purchase price is financed with 100 from the repo desk and ![]() from the swap desk.6 Finally, through an interest rate swap to the maturity of the bond, in addition to the up‐front payment just mentioned, the asset swapper periodically pays

from the swap desk.6 Finally, through an interest rate swap to the maturity of the bond, in addition to the up‐front payment just mentioned, the asset swapper periodically pays ![]() in exchange for receiving LIBOR plus the spread,

in exchange for receiving LIBOR plus the spread, ![]() , on 100. Note that this trade requires no cash at initiation; earns LIBOR plus

, on 100. Note that this trade requires no cash at initiation; earns LIBOR plus ![]() minus the repo rate over the life of the bond, so long as the bond does not default; and requires no cash at maturity, again, so long as the bond does not default. Hence, as desired, the investor has converted the fixed coupon payments of a bond into floating payments of LIBOR plus

minus the repo rate over the life of the bond, so long as the bond does not default; and requires no cash at maturity, again, so long as the bond does not default. Hence, as desired, the investor has converted the fixed coupon payments of a bond into floating payments of LIBOR plus ![]() . Of course, there are losses if the bond defaults: in that case, the asset swapper has to make coupon payments to the swap desk and, at maturity, pay 100 to the repo desk, even though these payments will not be fully realized from the defaulted bond.

. Of course, there are losses if the bond defaults: in that case, the asset swapper has to make coupon payments to the swap desk and, at maturity, pay 100 to the repo desk, even though these payments will not be fully realized from the defaulted bond.

The par asset swap spread, ![]() , can be determined by the condition that the interest rate swap with the swap desk is fair, that is, that the initial payment plus the present value of the floating leg equals the present value of the fixed leg, where discounting is at market swap rates.7 Mathematically, let

, can be determined by the condition that the interest rate swap with the swap desk is fair, that is, that the initial payment plus the present value of the floating leg equals the present value of the fixed leg, where discounting is at market swap rates.7 Mathematically, let ![]() and

and ![]() be the factors such that

be the factors such that ![]() gives the present value of the payments of

gives the present value of the payments of ![]() on the fixed side of the swap and such that

on the fixed side of the swap and such that ![]() gives the present value of the payments of

gives the present value of the payments of ![]() on the floating side.8 Let

on the floating side.8 Let ![]() be the discount factor for cash flows at maturity. Also, along the lines of Chapter 13, include a fictional notional amount of 100 at maturity on both legs of the swap, and note that the present value of receiving LIBOR and the final notional amount is par. Then, the fair pricing condition for the swap is,

be the discount factor for cash flows at maturity. Also, along the lines of Chapter 13, include a fictional notional amount of 100 at maturity on both legs of the swap, and note that the present value of receiving LIBOR and the final notional amount is par. Then, the fair pricing condition for the swap is,

FIGURE 14.2 A Par‐Par Asset Swap with Financing.

From Equation (14.1), for a given swap rate curve, as the credit risk of the bond increases, ![]() decreases, which, in turn, increases the asset swap spread,

decreases, which, in turn, increases the asset swap spread, ![]() . Table 14.7 reports that, as of August 15, 2021, the par asset swap spread of the Genworth 4.90s of 08/15/2023 is 526.4 basis points.

. Table 14.7 reports that, as of August 15, 2021, the par asset swap spread of the Genworth 4.90s of 08/15/2023 is 526.4 basis points.

A second flavor of asset swaps, namely, a market value asset swap, is illustrated in Figure 14.3. The market value asset swap differs from the par asset swap in that ![]() is borrowed from the repo desk, rather than 100;

is borrowed from the repo desk, rather than 100; ![]() is paid by the swap desk at the maturity rather than the initiation of the swap; and, as a result, LIBOR plus the spread,

is paid by the swap desk at the maturity rather than the initiation of the swap; and, as a result, LIBOR plus the spread, ![]() , is earned on

, is earned on ![]() rather than 100. Following the same notation and logic as in the case of the par asset swap, the fair market value asset swap spread is given by,

rather than 100. Following the same notation and logic as in the case of the par asset swap, the fair market value asset swap spread is given by,

where the final equality uses Equation (14.1). According to Table 14.7, the market value asset swap spread of the Genworth 4.90s of 08/15/2023, as of August 15, 2021, is 533.3 basis points. The relationship between the two asset swap spreads is quite intuitive: an investor can earn ![]() on 100 or

on 100 or ![]() on

on ![]() , which, from Equation (14.2), gives the same result. The choice between the two asset swap trades, therefore, depends not on earnings, but on collateral and counterparty risk considerations.9

, which, from Equation (14.2), gives the same result. The choice between the two asset swap trades, therefore, depends not on earnings, but on collateral and counterparty risk considerations.9

FIGURE 14.3 A Market Value Asset Swap with Financing.

The final measure of credit spread considered in this section is an effective spread for corporate FRNs no longer priced at par. When an FRN is priced at par, its spread is particularly easy to interpret as a spread over the short‐term rate benchmark received in exchange for bearing credit risk. Over time, however, as the credit quality of the issuer changes, the price of an FRN with a fixed spread changes. As a result, because an investor pays a premium or gets a discount to face amount when buying the FRN, in addition to its spread, that spread is no longer as easily interpreted.

The effective spread converts an FRN's premium or discount into a run rate and adds it to the actual spread. Let the actual spread be ![]() ; the price of the floater

; the price of the floater ![]() ; the present value factor, as before

; the present value factor, as before ![]() ; and the effective spread

; and the effective spread ![]() . Then, investors are indifferent between receiving

. Then, investors are indifferent between receiving ![]() for a price of

for a price of ![]() and

and ![]() for a price of 100 if,

for a price of 100 if,

This section concludes by noting that the trades described here for earning the credit spread are subject not only to the risk of default, but also to financing risk. Whenever a bond is purchased for a relatively long‐term holding period, but is financed with short‐term repo, there is the risk that the repo rate will increase by more than the discounting or benchmark rates. In that case, the bond will earn less than the benchmark short‐term rate (e.g., LIBOR) plus the spread. An even more extreme risk is that repo lenders will refuse to roll positions, because they no longer wish to lend to the borrower, because they no longer wish to lend against a particular bond, or because they need the cash themselves. In that scenario, corporate bond investors with short‐term repo financing will have to sell their bonds, most likely at a loss, to repay outstanding repo loans. Financing risk in the context of credit risk appears again, later in this chapter, as a key difference between bonds and credit default swaps.

14.4 CREDIT RISK PREMIUM

If credit spreads, on average, just compensated for credit losses, then risk‐averse investors would just as soon buy safe government bonds at the same average return, but without the downside risk. For corporate debt to be attractive, therefore, spreads must not only compensate for credit losses, but also provide an additional credit risk premium. This section reviews some evidence that, on average, corporate bond spreads do, indeed, more than compensate for credit losses.

One study estimates that the average corporate yield spread over default‐free bonds in the United States from 1866 to 2008 was 153 basis points, while the average credit loss was only 75 basis points. This long‐term evidence indicates a substantial credit risk premium, in that average spreads are about twice average credit losses.10

Another study, over the more recent period 2002–2015, also finds a significant credit risk premium. Defining the premium as credit spread minus expected losses, the second column of Table 14.8 reports the median ratio of premium to credit spread, and the third column reports the median ratio of premium to expected loss, by rating. To interpret these numbers, consider a Baa‐rated bond at a spread of 200 basis points. At the premium to spread ratio of 76% given in the second column, 76% of 200 or 152 basis points are due to a risk premium, while only the remaining 48 basis points are compensation for expected losses. Expressed in terms of the third column of the table, these 152 basis points of credit risk premium are over three times the expected loss of 48 basis points. Over the sample period of this study, bonds with Baa to B ratings are an investor sweet spot in the sense of providing the highest premium for the amount of risk borne.11

TABLE 14.8 Median Ratios of Premium to Credit Spread and to Expected Loss by Rating, 2002–2015.

| Rating | Premium/Spread (%) | Premium/Expected Loss |

|---|---|---|

| Aaa | 59 | 1.43 |

| Aa | 65 | 1.83 |

| A | 68 | 2.11 |

| Baa | 76 | 3.12 |

| Ba | 80 | 4.01 |

| B | 77 | 3.37 |

| Caa | 71 | 2.49 |

| Ca‐C | 68 | 2.12 |

Source: Berndt, Douglas, Duffie, and Ferguson (2018).

14.5 CREDIT DEFAULT SWAPS

In a single‐name credit default swap (CDS), a protection buyer or CDS buyer pays a fee, premium, or coupon to a protection seller or CDS seller in exchange for a compensation payment in the event that an issuer defaults. Bonds and CDS together comprise the markets for trading credit risk.

A CDS contract is defined by a reference entity, a list of credit events, a term or maturity, reference obligations, and a notional amount. As an example, consider a five‐year CDS on a notional amount of $1 million of Genworth Senior Unsecured 6.5s of 06/15/2034. A payment by the seller of this CDS would be triggered if, before its maturity, Genworth is determined by an industry‐led determinations committee to have experienced a credit event, like a bankruptcy filing or a failure to pay outstanding obligations.12 In that scenario, the protection seller must make the protection buyer whole with respect to $1 million face amount of the underlying bonds. More specifically, through physical settlement of the contract, the protection buyer delivers $1 million face amount of the bond to the protection seller in exchange for $1 million. Alternatively, through cash settlement of the contract, if the price of the bond were determined to be, for example, $400,000, the protection seller pays $600,000 to the protection buyer, again making the protection buyer whole on the $1 million face amount. (The existence of several reference obligations and the CDS delivery option, along with the auction mechanism by which protection sellers compensate protection buyers, is discussed presently.)

In exchange for the compensation payment in the event of default, the protection buyer pays a quarterly premium until the earlier of the maturity of the CDS or the event of default, in addition to paying or receiving an upfront amount at the initiation of the contract. The details of the premium and the upfront amount are discussed herein. For now, however, note that the CDS spread refers to the actual or hypothetical annualized premium on a CDS with an upfront payment of zero. In other words, a protection buyer can be thought of as paying the CDS spread in exchange for compensation in the event of default.

Table 14.9 gives selected sovereign and corporate five‐year CDS spreads as of November 2021. For example, the cost of compensation for a credit event in Greece over the subsequent five years is 112.3 basis points or 1.123% annually. (For sovereigns, which do not file for bankruptcy, credit events include a moratorium on or a repudiation of debt obligations in addition to a failure to pay.) The CDS spread for Genworth, at 378.3 basis points, implies a cost of $37,830 per year to insure against a default of the $1 million face amount of the 6.5s of 06/15/2034 mentioned already. The cost of insuring $1 million face amount of bonds for five years ranges in the table from a low of $910 per year for German government bonds to a high of $62,450 per year for the bonds of MBIA Insurance.

TABLE 14.9 Selected Sovereign and Corporate Five‐Year CDS Spreads, as of November 2021. Spreads Are in Basis Points.

| Sovereign | Spread | Corporate | Spread |

|---|---|---|---|

| Germany | 9.1 | Marsh & McLennan | 25.3 |

| United States | 16.0 | JPMorgan Chase | 53.8 |

| Spain | 35.2 | BBVA Bancomer | 70.3 |

| China | 48.9 | Ally Financial | 105.7 |

| Italy | 89.6 | Fairfax Financial | 154.5 |

| Greece | 112.3 | Banco do Brasil | 218.5 |

| Brazil | 265.8 | Genworth | 378.3 |

| Turkey | 469.6 | MBIA Insurance | 624.5 |

Whereas single‐name CDS allow market participants to trade the credit of a single name, index CDS allow for the trading of broader credit portfolios. The five most popular index CDS are: CDX.NA.IG, which represents a portfolio of 125 single‐name CDS on North American (NA), investment‐grade (IG) names; CDX.NA.HY, on 100 single‐name CDS on North American, high‐yield (HY) names; iTraXX Europe Main, on 125 single‐name CDS on European, investment‐grade names; iTraXX Europe Crossover, on 50 single‐name CDS on European, high‐yield names; and iTraxx Europe Senior Financials, on senior debt of 25 names in that sector. The detailed workings of CDS indexes are described in the London Whale case study presented later. Note that industry jargon is different for index than for single‐name CDS. The buyer of index CDS receives the premium and pays compensation in the event of default – just like the buyer of a portfolio of bonds – while the seller of index CDS pays the premium and receives compensation in the event of default – just like the short seller of a portfolio of bonds.

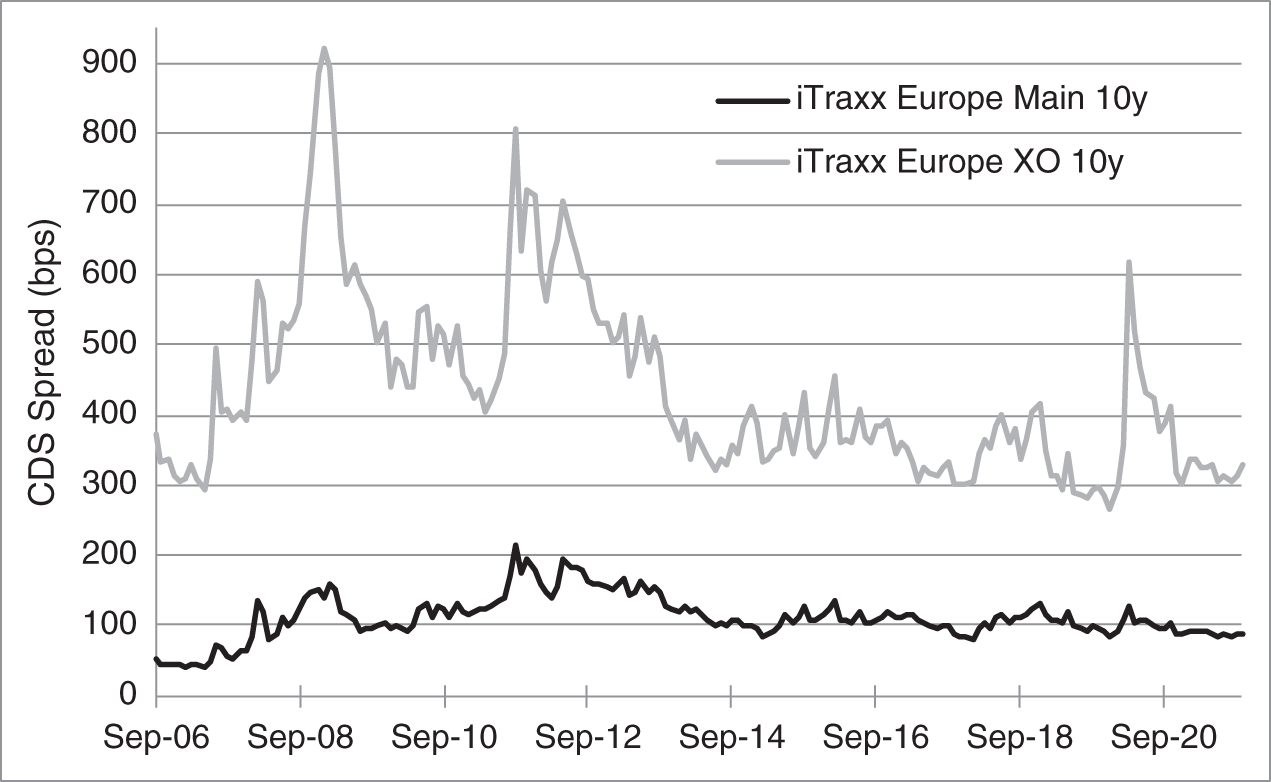

Figure 14.4 graphs historical CDS spreads for the 10‐year iTraxx Europe Main and iTraxx Europe Crossover (XO) indexes. The cost of protection for the XO index spiked during the financial crisis of 2007–2009, during the height of the European sovereign debt crisis in 2011–2012, and at the start of the pandemic and economic shutdowns in early 2020. (The behavior of CDX.NA.HY, not shown, was qualitatively similar, though it spiked to significantly higher levels during the financial crisis.) The fluctuations of the iTraxx Europe Main have been comparatively modest, reaching 200 basis points during the sovereign debt crisis, but settling in recent years at about 100 basis points.

Figure 14.5 shows the slope of the term structure of CDS spreads for the iTraxx Europe XO index, in particular, the difference between the 10‐ and three‐year index CDS spreads. In normal times, the annual cost of protection is higher for 10 years than for three years, because greater possibilities of disruption arise in the more distant future. During the financial crisis and at the height of the European sovereign debt crisis, however, the cost of three‐year protection was greater than or equal to the cost of 10‐year protection. In particularly stressful financial times, near‐term events are the most uncertain, after which – at least for all surviving entities – credit risk is likely to have returned to levels that prevail in calmer times.

Uses of CDS

This introduction to CDS now turns to market participants. An often cited use case is a corporate bond investor hedging the default risk of a bond by buying CDS protection. This case does not really stand on its own, however, because an investor is likely to give up most if not all of the bond's credit spread by buying protection. Or, put another way, an investor not wanting to bear the credit risk of a particular bond can just sell that bond. Other use cases, therefore, are worth exploring.

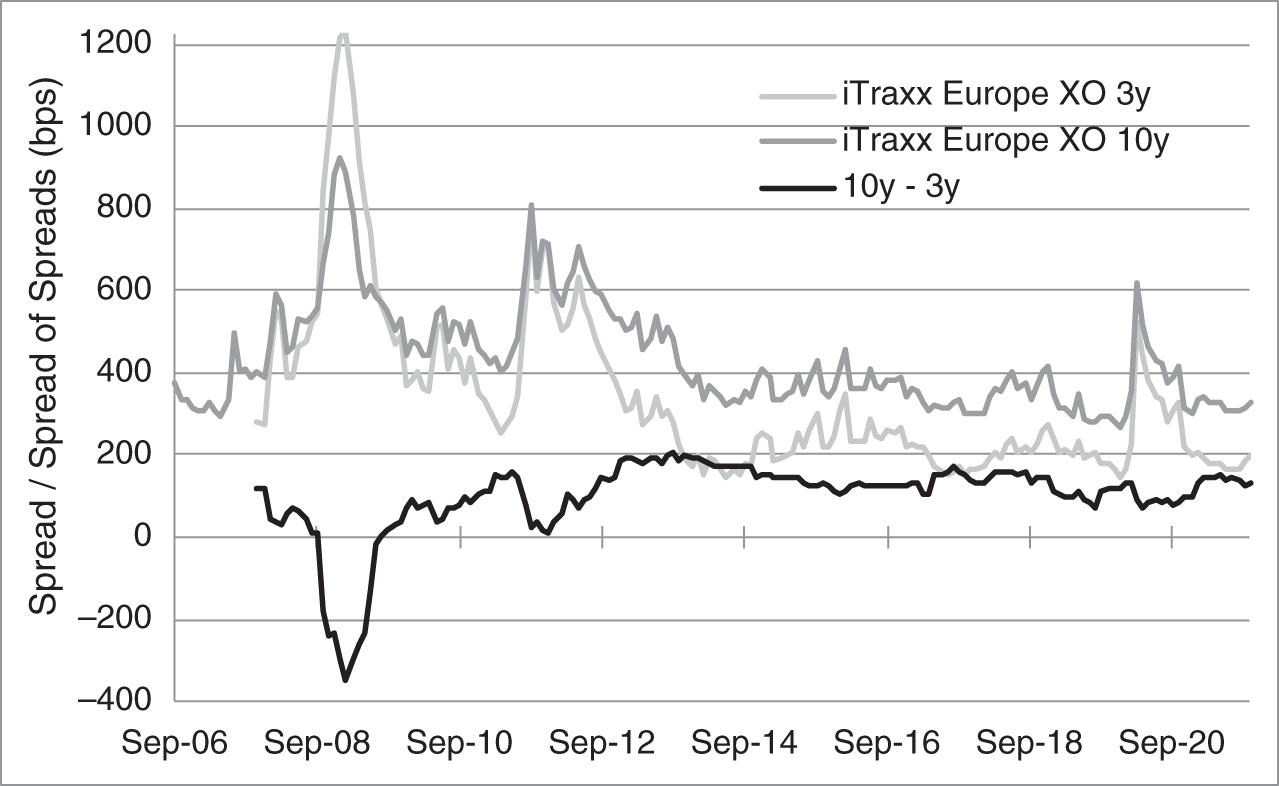

FIGURE 14.4 iTraxx Europe 10‐Year CDS Indexes.

FIGURE 14.5 iTraxx Europe 10‐Year versus Three‐Year Crossover CDS Indexes.

As mentioned earlier and discussed presently, selling CDS protection very much resembles buying a bond: both the protection seller and the investor receive coupons over time and lose money in the event of a default. Many sellers of protection, therefore, choose to bear credit risk through CDS rather than bonds. One reason might be that the relatively few CDS contracts on a particular name (e.g., a five‐ and 10‐year) are more liquid than that name's many outstanding bond issues. Similarly, selling protection on an index might be a lot less costly than assembling a similarly diversified portfolio by buying individual corporate bonds. Even if an asset manager ultimately wants to hold the bonds, the fastest way to put on the position might be to sell protection and then, over time, buy the bonds and unwind the protection sold. A second reason to prefer selling protection over buying bonds might be to isolate credit risk from interest rate risk. Many insurance companies, for example, engage in replication synthetic asset transactions (RSATs), in which, for example, they buy government bonds of a maturity that suits their asset–liability management requirements and then sell protection on a credit that they like for investment purposes. A third reason, also discussed in this chapter, is that selling protection allows an investor to take risk with relatively little capital, whereas buying a bond requires that cash be available or explicitly borrowed.

Protection buyers, on the other hand, very much resemble short sellers: both pay coupons over time and win money in the event of a default. One reason to short corporate credit in CDS form is that it may be most efficient to do so, given the relatively significant trouble and expense of borrowing corporate bonds to short them. A second reason, paralleling a discussion in the previous paragraph, is that an investor might want to sell a corporate bond, but its liquidity would require a gradual, relatively slow unwind. In that case, if urgency is important, the best strategy might be to buy protection immediately in the more liquid CDS market, and then gradually sell the bond and unwind the purchased protection. A third reason to buy CDS protection is to hedge against risks that are not traded at all. For example, an entity doing business with Italian firms that have no publicly traded debt or related CDS might want to hedge against deteriorating credit conditions in that country by buying protection on Italian banks. This example has important consequences, as it implies that market participants might purchase protection on credits to which they have no direct exposure. And this, in turn, means that the amount of CDS outstanding on particular credits might exceed their outstanding debt. Back to the example, if many market participants want to hedge financial risk in Italy, the amount of CDS protection bought on Italian banks could exceed the amount of Italian bank debt outstanding.

A recent study puts the global outstanding notional amount of CDS at $9.4 trillion, split 62% in index CDS and 38% in single‐name CDS. Notional amounts are misleading indicators of outstanding risk, however, for the same reasons that apply to interest rate swaps, which are discussed in Chapter 13. Net notional outstanding then, from the same study, which nets each entity's long and short positions, is only $1.5 trillion, with two‐thirds of that in index CDS and one‐third in single‐name CDS. CDX.NA.IG and iTraxx Europe account for about 70% of traded index amounts, and the top five aforementioned CDS contracts account for more than 90% of index activity. With respect to the single‐name market, about 800 distinct names are referenced in each quarter of trading, but only about 550 of those names are referenced in every quarter. This implies that the single‐name market consists of a core group of names that are traded consistently over time and other names that trade when interest is high in their particular credit situations.13

14.6 CDS UPFRONT AMOUNTS

Before the financial crisis of 2007–2009, CDS traded like interest rate swaps; that is, the coupon changed every moment with market conditions, and standard maturities were fixed terms from the settlement date. For example, buying $1 million notional of five‐year CDS on Genworth at a spread of 558.92 basis points on August 16, 2006, was a commitment to pay $55,892 annually in exchange for compensation in the event of a Genworth default through August 16, 2011. Consequently, as is still true for interest rate swaps today (see Chapter 13), unwinding CDS trades was relatively difficult. For example, to unwind the CDS just described after one month, a trader would most like to sell protection at a fee of 558.92 basis points through August 16, 2011. But at the time of the unwind, on September 16, 2006, the most liquid or on‐the‐run five‐year CDS would mature on September 16, 2011, and might carry a spread of 490 basis points. The trader, therefore, would have to incur relatively high transaction costs to unwind the existing CDS, or would have to sell protection through the on‐the‐run CDS and manage the maturity and spread mismatch between the original and the hedging CDS.

Since the financial crisis, as part of a broader push by regulators to improve operations in this market, CDS have become more standardized. First, maturity dates are limited to pseudo‐IMM (international money market) dates, that is, the 20th days of March, June, September, or December. Thus, for example, all five‐year contracts traded between June 21, 2021, and September 20, 2021, mature on September 20, 2021; all five‐year contracts traded between September 21, 2021, and December 20, 2021, mature on December 20, 2021; etc. Second, all contracts have annual coupons of either 100 or 500 basis points, with a market determined upfront amount to compensate for the difference between the market CDS spread and the standardized coupon. Upfront amounts are described in greater detail later, but, for the present, note how these two changes in market conventions simplify the unwind of CDS. Buying a $1 million five‐year CDS on Genworth on August 16, 2021, at a spread of 558.92 actually requires making annual payments of 500 basis points or $50,000, and – as shown next – an upfront payment of $23,190. Furthermore, the contract matures on September 20, 2021. Therefore, to unwind this contract after one month, the trader can sell a still on‐the‐run CDS, that is, a CDS with a coupon of 500 basis points that matures on September 20, 2021, which exactly offsets the future cash flows of the original CDS.14 If the market upfront payment fell over the month to $13,000, then the trader suffers a loss of $10,190 relative to the original purchase price. Unwinding the contract after more time has passed can be more difficult, because the on‐the‐run contract may have changed, but some liquidity is likely still available: many market participants likely traded Genworth CDS between June 21, 2021, and September 20, 2021, and, therefore, have contracts with a coupon of 500 basis points and a maturity of September 20, 2021.

A short mathematical prelude is needed here before moving to the calculation of upfront amounts. Simple credit risk models assume a constant hazard rate, ![]() , defined such that the probability of default over a short time interval,

, defined such that the probability of default over a short time interval, ![]() years, equals

years, equals ![]() . If the hazard rate is 10% and that time interval is six months, then the probability of default over the six months is 10%/2 or 5%, and the probability of “survival,” meaning no default, is 95%. To survive over a year requires survival over both the first and second six months, which has a probability of

. If the hazard rate is 10% and that time interval is six months, then the probability of default over the six months is 10%/2 or 5%, and the probability of “survival,” meaning no default, is 95%. To survive over a year requires survival over both the first and second six months, which has a probability of ![]() . And this survival probability, in turn, implies that the probability of default over the year, whether in the first or the second six months, is

. And this survival probability, in turn, implies that the probability of default over the year, whether in the first or the second six months, is ![]() , or 9.75%. Note that breaking the one‐year time frame into two six‐month periods makes the probability of survival over the year, 90.25%, greater than 90% (100% minus the annual hazard rate of 10%): with 95% survival over the first six months, only that 95% – not the full 100% – is subject to default over the second six months. Correspondingly, the probability of default over the year, 9.75%, is less than the annual hazard rate of 10%.

, or 9.75%. Note that breaking the one‐year time frame into two six‐month periods makes the probability of survival over the year, 90.25%, greater than 90% (100% minus the annual hazard rate of 10%): with 95% survival over the first six months, only that 95% – not the full 100% – is subject to default over the second six months. Correspondingly, the probability of default over the year, 9.75%, is less than the annual hazard rate of 10%.

More generally, Appendix A14.1 shows that if the hazard rate is applied continuously, then the cumulative survival probability over ![]() years,

years, ![]() , and the cumulative default probability over

, and the cumulative default probability over ![]() years,

years, ![]() , are,

, are,

TABLE 14.10 Calculating the Upfront Amount for 100 Notional Amount of an Annual Pay Five‐Year CDS on Genworth at a Coupon of 500 Basis Points and a CDS Spread of 558.92 Basis Points, as of August 16, 2021. The Recovery Rate Is 40%. Probabilities and the Hazard Rate Are in Percent.

| Discount | Cumulative Survival | Default | |

|---|---|---|---|

| Year | Factor | Probability | Probability |

| 1 | 0.998462 | 91.099 | 8.901 |

| 2 | 0.994257 | 82.991 | 8.109 |

| 3 | 0.985062 | 75.604 | 7.387 |

| 4 | 0.973167 | 68.875 | 6.729 |

| 5 | 0.959797 | 62.744 | 6.130 |

| Hazard Rate | 9.322 | ||

| Value of Fee Leg | 21.995 | ||

| Value of Contingent Leg | 21.995 | ||

| Upfront Amount | 2.319 | ||

To illustrate the use of these equations with the same annual hazard rate of 10%, the cumulative survival probability over four years is ![]() , and the cumulative default probability is one minus that, or 33.0%. Note again that, because of the compounding of survival probabilities over many short time intervals, the four‐year survival rate of 67.0% is significantly greater than one minus four years at 10%, or 60%, and, correspondingly, the four‐year default rate of 33.0% is significantly less than 40%.

, and the cumulative default probability is one minus that, or 33.0%. Note again that, because of the compounding of survival probabilities over many short time intervals, the four‐year survival rate of 67.0% is significantly greater than one minus four years at 10%, or 60%, and, correspondingly, the four‐year default rate of 33.0% is significantly less than 40%.

Appendix A14.2 gives general, algebraic formulae for the market convention of calculating a CDS upfront amount given a quoted CDS spread. The text, however, continues with an example described in Table 14.10: 100 notional amount of a five‐year Genworth CDS as of August 16, 2021. The CDS coupon is 500 basis points; the market CDS spread is 558.92 basis points; and the assumed recovery rate is 40%.15 For simplicity, it is assumed that premium payments are annual (instead of quarterly).

The basic idea behind the market convention is as follows. First, find the hazard rate that makes the Genworth CDS “fair” in the sense that the expected discounted value of paying for protection with the CDS spread – here 558.92 basis points per year – is equal to the expected discounted value of receiving compensation in the event of default – here ![]() . This hazard rate turns out to be 9.322%. Second, using that hazard rate, find the expected discounted value to the protection buyer of paying the actual CDS coupon – here 500 basis points – instead of the CDS spread of 558.92 basis points. That value turns out to be 2.319. Hence, to buy 100 face amount of Genworth protection at a coupon of 500 basis points, when the CDS spread is actually 558.92, the protection buyer has to pay an additional 2.319 upfront.

. This hazard rate turns out to be 9.322%. Second, using that hazard rate, find the expected discounted value to the protection buyer of paying the actual CDS coupon – here 500 basis points – instead of the CDS spread of 558.92 basis points. That value turns out to be 2.319. Hence, to buy 100 face amount of Genworth protection at a coupon of 500 basis points, when the CDS spread is actually 558.92, the protection buyer has to pay an additional 2.319 upfront.

The first column of Table 14.10 lists the years of the five annual payments. The second column gives the discount factors from the LIBOR swap curve as of the pricing date. The third and fourth columns give the cumulative survival and default probabilities at the end of each year, computed with Equations (14.4) and (14.5) and a hazard rate of 9.322%. This hazard rate is shown in the table, and its derivation is given presently.

Like all CDS, the Genworth CDS in the example can be described as having two legs: a fee leg and a contingent leg. The fee leg comprises the payments of the premium from the buyer to the seller of protection. At the end of any year in which there has not been a default, the buyer in the current calculation has to pay the CDS spread of 558.92 basis points on the 100 notional amount, or 5.5892. If there is a default over the year, then the buyer has to pay the accrued coupon from the start of the year to the time of default. If, for example, the default occurred after three months, or one‐quarter of a year, the buyer would have to pay one‐fourth of the coupon, or 1.3973; if the default occurred in the middle of the year, the buyer would have to pay 2.7946. For simplicity, however, the market convention for calculating upfront amounts assumes accrual for half the period, or, in this example, for half of the year. (This assumption has less impact on the calculations in practice, because coupons are actually paid quarterly.)

Continuing with the example, then, the buyer's payment on the fee leg at the end of the first year is 5.5892 if there is no default over the year, and 2.7946 if there is. The probability of these two contingencies are reported in the table as 91.099% and 8.901%, respectively. Hence, the expected present value of this payment is,

Analogous calculations can be repeated for each of the next four years, using the appropriate survival and default probabilities and discount factors. Then, summing the results gives the present value of the fee leg, reported in Table 14.10, as 21.995.

TABLE 14.11 Calculating the Expected Discounted Value of 100 Face Amount of an Annual Pay Five‐Year 5% Genworth Bond as of August 16, 2021, at a Hazard Rate of 9.322% and a Recovery Rate of 40%.

| Expected PV Coupon | Expected PV Principal | |||

|---|---|---|---|---|

| Year | Default | No Default | Default | No Default |

| 1 | 0.222 | 4.548 | 3.555 | |

| 2 | 0.202 | 4.126 | 3.225 | |

| 3 | 0.182 | 3.724 | 2.911 | |

| 4 | 0.164 | 3.351 | 2.620 | |

| 5 | 0.147 | 3.011 | 2.354 | 60.222 |

| Total | 0.916 | 18.760 | 14.663 | 60.222 |

| Bond Price | 94.561 | |||

With respect to the contingent leg, the seller of protection pays the buyer 60 in any year that Genworth experiences a default. The expected discounted value of that contingent payment in the third year, for example, is,

Performing this calculation for each of the five years and summing the results gives the present value of the contingent leg, reported in Table 14.10, as 21.995.

Because the discounted expected values of the fee and contingent legs are equal, the hazard rate of 9.322% correctly reflects the market CDS spread of 558.92 basis points. Solving for this hazard rate in the first place requires iterating through the calculations just described. For example, after setting up the calculations in Table 14.10 as an Excel spreadsheet, the built‐in solver can be used to find the hazard rate that results in equal values for the fee and contingent legs.

The stage is now set for calculating the upfront amount such that paying this upfront amount at the initiation of the CDS and then paying a running premium of 500 basis points has the same discounted expected value as paying nothing upfront and then a running premium of 558.92 basis points. As derived previously, the expected discounted value of the fee leg making payments of 5.5892 is 21.995. It follows, then, that the value of payments of the standardized coupon of five in the fee leg is ![]() . Therefore, the required upfront payment is just the difference,

. Therefore, the required upfront payment is just the difference, ![]() , or 2.319: an upfront payment of 2.319 and a running premium of five (which is worth 19.676) has the same value as no upfront payment and a running premium of 5.5892 (which is worth 21.995).

, or 2.319: an upfront payment of 2.319 and a running premium of five (which is worth 19.676) has the same value as no upfront payment and a running premium of 5.5892 (which is worth 21.995).

A moment's reflection reveals that the upfront amount is positive whenever the CDS spread is greater than the standardized coupon. If the market CDS spread of Genworth were 450 on August 16, 2021, then the upfront amount turns out to be ![]() 2.051. Buying protection by receiving 2.051 upfront and paying a running premium of five has the same value as no upfront amount and paying a running premium of 4.50.16

2.051. Buying protection by receiving 2.051 upfront and paying a running premium of five has the same value as no upfront amount and paying a running premium of 4.50.16

This section concludes by emphasizing that the quoting of an upfront amount from a CDS spread is only a convention, like the relationship between price and yield‐to‐maturity. Market participants form their own views on upfront amounts at which they are willing to trade CDS. They may not be willing, for example, to assume a particular recovery rate or that the hazard rate is constant over time. But they all use the accepted market conventions to calculate upfront amounts from a quoted CDS spread or vice versa.

14.7 CDS‐EQUIVALENT BOND SPREAD

The credit spreads defined earlier in the chapter are all measures of bond return assuming no default. An alternative approach, the CDS‐equivalent bond spread, accounts for default and recovery and is computed along the lines of the previous section. The basic idea is to find the hazard rate such that the market price of the bond equals the expected discounted value of its cash flows. Then, the bond's CDS‐equivalent spread is the CDS spread corresponding to that hazard rate. To illustrate, say that the market price of a five‐year, 5% (annual pay) bond on Genworth is 94.561 as of August 16, 2021. It is shown next that the expected discounted value of that bond's cash flows equals that market price if the hazard rate is 9.322%. Furthermore, from Table 14.10, the five‐year CDS spread at a hazard rate of 9.322% is 558.92 basis points. Therefore, the CDS‐equivalent spread of this five‐year, 5% bond is 558.92 basis points. In other words, the credit risk implied by the bond's market price is the same as that implied by a five‐year CDS at a spread of 558.92 basis points. This spread depends on the restrictive assumption that the hazard rate is constant. The calculation of expected discounted values, while seeming to imply risk neutrality, is not as restrictive as it seems: the hazard rate can be considered “risk‐neutral” so that it prices fixed income securities without necessarily reflecting real‐world probabilities. (This distinction is discussed in Chapter 7.)

Appendix A14.4 gives the algebra for calculating the expected discount value of a bond's cash flows given a hazard rate. The text, however, continues with pricing 100 face amount of an annual pay, five‐year, 5% Genworth bond as of August 16, 2021, and the results are summarized in Table 14.11. Because the bond's assumed market price is consistent with a hazard rate of 9.332%, which is the hazard rate in Table 14.10, the cumulative survival and default probabilities from that table can be used here. Also, because the pricing dates are the same, the discount factors from that table can be used here as well.

Along the lines of the previous section, the expected value of a bond's coupon in a given year is half of its value times the probability of default over the year plus its value times the probability of no default over the year. The discounted expected value of the first coupon of the 5% Genworth bond, for example, is as in Equation (14.6), but with the bond coupon of 5.00 replacing the CDS spread payment of 5.5892,

The two components of this coupon's expected discounted value are given in the second and third columns of the first row of Table 14.11. The next rows of the table repeat this calculation for subsequent coupon payments, using the appropriate discount factors, cumulative survival probabilities, and cumulative default probabilities from Table 14.10. Summing the results, the total discounted expected value of the bond's coupons is ![]() .

.

With respect to principal, if there is a default in any year, then the principal received is the face amount times the recovery rate. The discounted expected value of principal received in the third year, for example, is the three‐year discount factor times the probability of default in year three times the recovery on 100 face amount,

which is the value given in the fourth column, third row, of Table 14.11. (Note that, in Equation (14.9), the bondholder receives 40, while in Equation (14.7), the buyer of protection receives a default compensation of 60.) The table uses the equivalents of Equation (14.9) to calculate the rest of the fourth column.

If there is no default up to and including maturity, the bond pays its full principal amount. The expected discounted value of this cash flow is,

and is given in the year five row and in the rightmost column of Table 14.11.

Finally, adding together the four components of the bond's expected discounted value from the table, the bond's price is 94.561. Hence, because the bond is fairly priced using a hazard rate of 9.322%, and because that hazard rate corresponds to a CDS spread of 558.92 basis points (from the previous section), this bond's CDS equivalent spread is 558.92 basis points.

This section now compares the CDS‐equivalent bond spread just explained with the bond spread discussed already. First, Appendix A14.3 shows that the CDS spread is approximately equal to the hazard rate times one minus the recovery rate. Mathematically, letting ![]() denote the CDS spread; letting

denote the CDS spread; letting ![]() denote the hazard rate, as before; and letting

denote the hazard rate, as before; and letting ![]() denote the recovery rate,

denote the recovery rate,

In the context of Table 14.10, for example, the approximation predicts a CDS spread of 9.322% times (1 − 40%), or 559.32 basis points, while the actual spread is a very close 558.92 basis points.

Second, Appendix A14.5 shows that,

where ![]() is the bond spread, and

is the bond spread, and ![]() is the recovery rate as a percentage of market value. To this point the chapter has assumed par recovery, that is, bond recovery rates are best modeled as a fixed percentage of face amount. Market recovery, by contrast, which is used to derive Equation (14.12), assumes that recovery is a fixed percentage of market value. Say that two bonds were sold by the same issuer with the same seniority, but one of the bonds has a much longer maturity and trades at a larger price discount or premium, depending on the level of rates and spreads. In the event of default, will the two bonds recover the same amount – as assumed by par recovery – or will the longer‐term bond's recovery reflect its greater discount or premium – as assumed by market recovery? Par recovery is the more common assumption and is better supported by empirical evidence.17

is the recovery rate as a percentage of market value. To this point the chapter has assumed par recovery, that is, bond recovery rates are best modeled as a fixed percentage of face amount. Market recovery, by contrast, which is used to derive Equation (14.12), assumes that recovery is a fixed percentage of market value. Say that two bonds were sold by the same issuer with the same seniority, but one of the bonds has a much longer maturity and trades at a larger price discount or premium, depending on the level of rates and spreads. In the event of default, will the two bonds recover the same amount – as assumed by par recovery – or will the longer‐term bond's recovery reflect its greater discount or premium – as assumed by market recovery? Par recovery is the more common assumption and is better supported by empirical evidence.17

In short, CDS and bond spreads are not equivalent, and the consensus in favor of the par recovery assumptions argues in favor of preferring the CDS spread. Furthermore, at high hazard rates and low bond prices, the CDS spread is significantly greater than the bond spread. To illustrate, recall from Tables 14.10 and 14.11 that the five‐year 5% Genworth bond, at a hazard rate of 9.322% and a price of 94.561, has a CDS spread of 559 basis points. From the data in these tables, it can also be computed that its bond spread is a similar 551 basis points.18 However, if the hazard rate is a much higher 16.70%, then the bond price is 80.688; the CDS spread is 1,000 basis points; and the bond spread is a much lower 932 basis points. (These computations are also left as an exercise for the reader.) Intuitively, by assuming too low a recovery for discount bonds, bond spreads have to be lower to reproduce seemingly high market prices.

14.8 CDS‐BOND BASIS

Credit risk today is traded in both the corporate debt market and in the CDS market. It is natural to ask, therefore, whether a particular credit trades at the same price in both markets or is cheaper in one market than the other. If the latter, then there might be relative value trading opportunities to buy in one market and sell in the other.

Table 14.12 sets the stage with a simplified relationship between selling CDS protection on a particular credit and buying a bond of that same credit, financed in the repo market.19 The table is a simplification by assuming that i) the CDS contract has an upfront payment of zero, that is, the CDS coupon equals the CDS spread; ii) the corporate bond is priced at par; and iii) the CDS and the underlying bond mature on the same date. Under these assumptions, the table shows that selling CDS protection is equivalent to buying a bond and financing its purchase with term repo to the bond's maturity. More specifically, the cash flows from selling 100 notional of CDS are: zero today; the spread ![]() on 100 until the earlier of default or maturity;

on 100 until the earlier of default or maturity; ![]() if and when the bond defaults; and zero if the bond matures without a default. The cash flows from buying 100 face amount of the bond at a price of par are

if and when the bond defaults; and zero if the bond matures without a default. The cash flows from buying 100 face amount of the bond at a price of par are ![]() 100 today; the coupon rate

100 today; the coupon rate ![]() on the face amount to the earlier of default or maturity;

on the face amount to the earlier of default or maturity; ![]() if and when the bond defaults; and 100 if the bond matures without a default. Finally, the cash flows from borrowing the bond's purchase price through repo are 100 today;

if and when the bond defaults; and 100 if the bond matures without a default. Finally, the cash flows from borrowing the bond's purchase price through repo are 100 today; ![]() on 100 until the earlier of default or maturity; and

on 100 until the earlier of default or maturity; and ![]() 100 at the earlier of default or maturity. (To clarify these repo cash flows, note that, if a bond defaults, the borrower has to unwind the repo position by paying off the 100 loan amount, which then ends interest payments on the loan.) Finally, adding the cash flows from purchasing the bond and selling the repo gives the “Total” row, which exactly matches the cash flows of selling CDS protection so long as

100 at the earlier of default or maturity. (To clarify these repo cash flows, note that, if a bond defaults, the borrower has to unwind the repo position by paying off the 100 loan amount, which then ends interest payments on the loan.) Finally, adding the cash flows from purchasing the bond and selling the repo gives the “Total” row, which exactly matches the cash flows of selling CDS protection so long as ![]() .

.

TABLE 14.12 A Simplified Arbitrage Relationship Between Selling Protection on a Credit and Buying a Bond on That Same Credit, Financed by Repo.

| Today | Interim (%) | Default | Maturity/No Default | |

|---|---|---|---|---|

| Sell CDS Protection | 0 | 0 | ||

| Buy Par Bond | 100 | |||

| Sell Repo | 100 | |||

| Total | 0 | 0 |

The CDS‐bond basis refers to the difference between the CDS spread and some measure of the bond's spread over riskless rates. In the simplified setting of Table 14.12, where the bond spread is the difference between the par coupon and the matching‐term repo rate, the CDS‐bond basis is ![]() . If the basis is positive, then

. If the basis is positive, then ![]() , which means that the bond is rich, or that it has a low spread relative to the CDS spread. Put another way, selling CDS protection earns more than buying the bond. If the basis is negative, then

, which means that the bond is rich, or that it has a low spread relative to the CDS spread. Put another way, selling CDS protection earns more than buying the bond. If the basis is negative, then ![]() , which means that the bond is cheap relative to the CDS spread, and that buying the bond earns more than selling CDS protection. In either case, when the basis is not zero, an arbitrage opportunity is available. If positive, execute a positive basis trade, that is, sell protection, short the bond, and buy the repo, to lock in

, which means that the bond is cheap relative to the CDS spread, and that buying the bond earns more than selling CDS protection. In either case, when the basis is not zero, an arbitrage opportunity is available. If positive, execute a positive basis trade, that is, sell protection, short the bond, and buy the repo, to lock in ![]() per period until the earlier of default or maturity. And if the basis is negative, execute a negative basis trade, that is, buy protection, buy the bond, and sell the repo, to lock in

per period until the earlier of default or maturity. And if the basis is negative, execute a negative basis trade, that is, buy protection, buy the bond, and sell the repo, to lock in ![]() per period.

per period.

Crucial to these arbitrage arguments is that the term of the repo equal the maturity of the bond and the CDS. In a negative basis trade, for example, selling overnight – rather than term – repo exposes a trader to financing risk: the overnight repo rate might increase dramatically or repo funding might be withdrawn completely, either because the bond's creditworthiness has deteriorated, because general financing supply has tightened, or because the trader's own credit has come under stress. In any of these scenarios, the trader might very well be forced to unwind the position at a loss, that is, when the bond has become even cheaper relative to CDS. Similarly, in executing a positive basis trade with overnight repo, the financing risk is not being able to continue to borrow the bonds in order to maintain the short position.

In practice, because there is no market for very long‐term corporate repo, it is nearly impossible to execute a basis trade without bearing financing risk. Therefore, despite arbitrage arguments like Table 14.12, there is a fundamental difference between CDS and levered bond positions: CDS positions have implicit financing to maturity, while levered bond positions are inherently subject to financing risk.

Outside the simplified setting of Table 14.12, market participants compute the CDS‐bond basis using different measures of a bond's spread, like yield spread, bond spread, asset swap spread, and CDS‐equivalent bond spread. The advantages and disadvantages of each of these is discussed previously, but all of these measures can be misleading in the context of the CDS‐bond basis. Without a term‐repo rate, any measure of the basis ignores the financing risk in a CDS versus levered bond arbitrage trade.

A lot of money was lost in negative basis trades through the financial crisis of 2007–2009. As funding conditions became more difficult, CDS‐bond bases moved negative, reflecting the difficulty of going long credit risk with levered bond positions relative to selling CDS protections. Some traders, however, saw these negative bases as trading opportunities, which turned into nightmares as funding conditions deteriorated even further. Over the crisis, in fact, the investment‐grade index CDS‐bond basis fell from about zero to negative 250 basis points.

Figure 14.6 shows the CDS‐bond basis for French and Italian government bonds from January 2006 to October 2021. The basis is defined here as the difference between the five‐year CDS spread and the five‐year government bond yield spread over Germany. By way of economic backdrop, the European sovereign debt crisis ran from the end of 2009 to 2012, during which time the finances of both banks and governments in the so‐called “peripheral” countries (e.g., Greece, Italy, Portugal, and Spain) came under pressure. Later, in the fall 2018, European Union and Italian government officials squabbled over Italy's proposed budget, which did not comply with existing fiscal rules. The figure shows that the sovereign Italian CDS‐bond basis became significantly negative during both of these stressful periods. As in the financial crisis of 2007–2009, repo lenders became reluctant to fund Italian government bonds, pushing up their spreads and pushing their CDS‐bond basis into negative territory. In fact – though not shown in the figure – spreads of Italian to German government bonds rose to over 600 basis points during the sovereign debt crisis, and to nearly 300 basis points during the budget standoff. By contrast, French government credit exhibited a positive CDS‐bond basis during the sovereign debt crisis. French over German spreads did rise to a peak of about 100 basis points at that time, but the bigger story was the difficulty of borrowing and shorting French government bonds, at least in part because the European Central Bank was aggressively buying European sovereign debt. In any case, the resulting upward pressure on French government bond prices resulted in a significantly positive CDS‐bond basis.20 Finally, more recently, funding stresses during the COVID pandemic and economic shutdowns drove both Italian and French government CDS‐bond bases somewhat negative.

FIGURE 14.6 CDS‐Bond Basis for French and Italian Sovereign Debt, January 2006 to October 2021.

14.9 HAZARD‐ADJUSTED DURATION AND DV01

The durations of bonds with credit risk are often calculated along the lines of Chapter 4, that is, cash flows are assumed to be paid on schedule, but are discounted at higher rates, typically at benchmark rates plus a credit spread or a term structure of credit spreads. Calculated this way, however, duration can be misleading for bonds with significant credit risk. For these bonds, expected cash flows are much earlier than scheduled cash flows and, consequently, their durations are correspondingly shorter.