APPENDIX TO CHAPTER 8

Expectations, Risk Premium, Convexity and the Shape of the Term Structure

This appendix proves Equation (8.18) along the lines of Ingersoll (1987).1 Assume that ![]() , the single, instantaneous rate factor, follows the process,

, the single, instantaneous rate factor, follows the process,

Let ![]() be the full price of some security that depends on

be the full price of some security that depends on ![]() and time. Then, by Ito's lemma,

and time. Then, by Ito's lemma,

where ![]() ,

, ![]() , and

, and ![]() denote the partial first derivatives with respect to

denote the partial first derivatives with respect to ![]() and

and ![]() and the second partial derivative with respect to

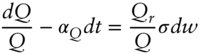

and the second partial derivative with respect to ![]() . Dividing both sides of (A8.2) by

. Dividing both sides of (A8.2) by ![]() , taking expectations, and defining

, taking expectations, and defining ![]() to be the expected return of the security,

to be the expected return of the security,

Combining (A8.1), (A8.2), and (A8.3),

Because Equation (A8.4) applies to any security, it also applies to some other security ![]() ,

,

Now consider the strategy of investing one unit of currency in security ![]() and

and ![]() in security

in security ![]() . From Equations (A8.4) and (A8.5), the return on this portfolio is,

. From Equations (A8.4) and (A8.5), the return on this portfolio is,

Note that terms with the random variable ![]() have fallen out of Equation (A8.6). This particular portfolio is chosen, in fact, so as to hedge completely the risk of

have fallen out of Equation (A8.6). This particular portfolio is chosen, in fact, so as to hedge completely the risk of ![]() with

with ![]() . In any case, because the portfolio has no risk, it must earn the instantaneous rate,

. In any case, because the portfolio has no risk, it must earn the instantaneous rate, ![]() ,

,

Rearranging terms,

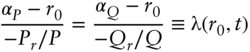

Equation (A8.8) says that the expected return of any security above the instantaneous rate divided by its duration with respect to that rate must equal some function ![]() . This function cannot depend on any characteristic of the security, because (A8.8) is true for all securities. The function may depend, however, on the interest rate factor and time. Rewriting Equation (A8.8), for any security

. This function cannot depend on any characteristic of the security, because (A8.8) is true for all securities. The function may depend, however, on the interest rate factor and time. Rewriting Equation (A8.8), for any security ![]() ,

,

NOTE

- 1 Ingersoll, J. (1987), Theory of Financial Decision Making, Rowman & Littlefield.