CHAPTER 17

Software Business Models

The business model disruption framework as it applies to software has multiple layers: Platforms have changed and are changing; enterprise and personal computing markets differ significantly; and the division of labor among operating systems, network services, and application software is also in flux. For our purposes, let's look at the case of Microsoft, insofar as it was a dominant player in software markets through most of the 1990s. How did Internet-related events and trends disrupt its business model?

Incumbent Model Pre-2000

Back when investors were looking for “the next Microsoft,” they held certain assumptions about what a highly successful software company looked like.

Customer Value Proposition

The value proposition for Windows in the 1990s was compelling: If you want to do any of the many wonderful things computers can allow you to do, we are the only game in town. Apple was a niche provider with tiny market share and high prices because of the proprietary hardware-software relationship. For a time, IBM's OS/2 operating system had some technical advantages over Windows, but IBM never established the application ecosystem that would make its OS competitive. No other platforms were credible after the semihobbyist and cult brands of the 1980s, such as Amiga, were sufficiently marginalized.

Once you bought a computer with the Windows OS, by 1995 there were no real alternatives for office productivity applications. In this complementary market, MS Office became the default choice, for both PCs and Macs, where it held even higher market share than on the PC. (On the PC at the time, WordPerfect still had pockets of loyal customers—in law firms, for example.)

Software was available on various types of plastic discs and was sold as a tangible product directly to the user (or her employer). As product companies, software vendors cared about software functionality and performance; data as they were generated or managed by the application fell out of scope. Both desktop and laptop computers were used sitting still, plugged into a hard-wired network when they were near the correct wall jack.

Profit Formula

Software platform leadership requires the development of mechanisms for user lock-in and network effects. Word processing programs stand as an obvious example, where switching is hard and expensive once you learn to use a package, and it makes sense to be on the same product as all of your coworkers if document sharing is a priority.

Software upgrade cycles delivered sustained profitability: That locked-in user base eventually had to buy the new, improved version, particularly after support was withdrawn or new functionality (for example, Wi-Fi in which 802.11A didn't work with 802.11B) was not backward compatible. Upgrades delivered a major revenue infusion to the software seller and perhaps the wider ecosystem.

For both OSs and applications, preventing digital copying of the assets was essential to maintaining pricing power. (See Chapter 4).

Technical support costs had to be kept low or, ideally, turned into a profit center.

Key Resources

Microsoft sold software to large customer bases one consumer or one business at a time. This reality of the market implies effective management of brand, retail channels, and enterprise sales forces. Retail channels such as CompUSA, Computer City, Micro Center, and others were important points of contact (and both formal and informal training) between the big hardware and software brands and the customer. Dell's direct model grew in influence through the 1990s but did not triumph until later.

An enthusiast magazine community helped users overcome their fear of ignorance in the face of complex language, purchase criteria, and user experience. These magazines, while not belonging to Microsoft, performed important functions: The implicit user question, Which computer should I buy?, was always answered by “a machine running Windows,” marginalizing the differences between, say, Toshiba and Gateway.

Strong technical teams matter: Once functionality is specified early (by market-facing product teams) in the new product development cycle, it must be hard-coded into the package. At Microsoft, feature inclusion apparently mattered more than security, stability, or reliability, but switching costs were sufficiently high, and alternatives scarce, that those drawbacks had few consequences for market share.

Key Processes

Software development was clearly essential to Microsoft's growth and continued market power. One challenge grew out of the fact of the sheer size of the code base: The Vista operating system reportedly contained 50 million lines of code. Achieving usability, debugging, consistent security architectures, and performance tuning at that scale is difficult or even impossible.

As a platform play in a heterogeneous ecosystem, Microsoft had to maintain working relationships with a wide variety of firms and organizations. Standards bodies and other forms of intercompany relationship building had to be managed to ensure the success of interoperability, brand consistency, investment effectiveness, and other objectives. Industry analysts (such as IDC) had to be kept abreast of the status of the platform; consumer product branding was insufficient to ensure enterprise adoption, particularly of server and development environments.

As big as Microsoft was (and remains), it could not address all the particular uses to which the software would be put. Building, certifying, and nurturing an independent software developer community helped put Windows systems into small businesses, corporate environments, schools, and other institutions. Developers, in turn, required tools, templates, frameworks, education, marketing materials, and many other forms of support in order to be effective.

Business Model Disruption after 1998

Whether one looks at Google—a clear challenger to Microsoft's dominance—or at Apple, Facebook, or Linux (not a company at all), many of the assumptions about the Microsoft model no longer hold true. Greatness in software now requires a lot of the old-world programming skills and positioning, plus a healthy dose of some new elements.

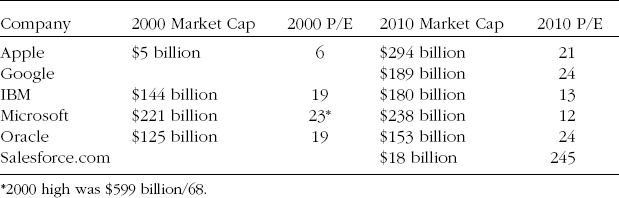

To set some context, Table 17.1 looks at some familiar companies listed by market capitalization and price/earnings (P/E) ratio as of late 2010 compared to 10 years before, at the end of 2000.

Note that Salesforce, the exemplar of software as a service, is valued at 20 times Microsoft's P/E ratio. Microsoft's market capitalization, meanwhile, grew less than 8% in a decade. In addition, as of 1998, anyone looking for “the next Microsoft” probably would not have looked to Viacom or Disney as models. And for good reason: The role of “pushed” content remains in transition more than a decade later. Yet so-called shrinkwrap business models emphasizing software as a physical product often sold by the number of users or “seats” are in rapid decline while the core of the media-industry model—the packaging of audiences for sale to advertisers—is fueling growth at Google, presenting both technical and cultural challenges at Yahoo!, being rewritten at Facebook, and the source of deep concern among Microsoft's top leadership.1

The changing of the guard is further emphasized by Microsoft's recent experience with old-school software, its Vista operating system. The product shipped three years late, with a stripped-down feature set, and effectively cost several senior executives their jobs. It never sold in large numbers, in part because enterprise buyers refused the trade-offs of cost, risk, and performance that it offered. Windows 7 sold better but garners little press recognition or industry buzz: It has many attributes of a utility or an appliance, while strong market presence and growth are the hallmarks of Facebook, Apple, and, in mobile particularly, Google. In contrast, Microsoft's mobile software platform has yet to generate momentum, although the company's landmark alliance with Nokia will certainly bear watching here.

What are the emerging dynamics for software dominance? Compared to the standards for success circa 1997, a few factors have been inverted while most still hold true, albeit with a twist.

TABLE 17.1 Selected Technology Companies' Market Capitalization and P/E Ratio

Product versus Service

In the majority of cases, nobody wants a product for what it is. (Diamonds and other luxury goods are obvious exceptions.) Rather, we want the capabilities delivered by the product: Knives slice food, cars provide transportation, and cameras deliver memories. When people buy software for what it does, there are numerous advantages to not owning seat licenses (particularly unutilized ones), physical artifacts such as discs or manuals, physical server hardware, physical data centers, or even physical storage. At the enterprise level, Microsoft has not suffered as directly from the presence of Salesforce.com as have Oracle and SAP, but the Salesforce model is helping people change their mind-sets: Recall that a business model is in large measure a cognitive commitment rather than a written document or legal status. At the personal level, Google's search, applications, maps, and mail/storage prove their utility daily to tens of millions of users. Software as a product is getting to be a more difficult sell.

The conception of software as a service rather than a product was advanced by the open-source community in the late 1990s. Understanding the difference between the use value and the sales value of software, particularly for custom enterprise applications, helped provide intellectual legitimacy for Apache, Linux, and others. As Eric Raymond, the author of the open-source manifesto The Cathedral and the Bazaar, put it, “[S]oftware is largely a service industry operating under the persistent but unfounded delusion that it is a manufacturing industry.”2

Platforms

Rather than developing for UNIX, Windows, Mac OS, Symbian, set-top boxes, and a variety of other OSs, Google and Amazon have led the way toward development of services for the Internet as a platform. Among other things, this stance greatly simplifies product distribution: The differences between today's Google Maps and a 1998 version of Rand McNally's Windows package are striking. Every time a new road was paved, or interstate exits were renamed, or a pedestrian mall was built, millions of CDs became obsolete. In contrast, Google (or NAVTEQ or whatever) makes one change to the base map and every subsequent query will be addressed with accurate information.

Getting the platform right still matters, but the definition of the term is changing from local to virtual, solitary to distributed, and product to environment. Furthermore, platform heterogeneity is a reality: Mobile devices and PCs, tablets and set-top boxes, and even automobiles are semiintegrated, so user identities, data, and preferences must move seamlessly back and forth. Google runs across platforms, following the user, perhaps better than any major software vendor, while Microsoft remains heavily desktop-centric, not to mention Microsoft-centric.

Lock-in

The lock-in aspect still concerns Wall Street analysts, particularly because switching costs can be so low. If I change from Yahoo! Finance to, say, Fidelity's investor workbench, apart from my investment in learning the old interface, there's very little to restrain me from leaving. Tim O'Reilly, who helped formulate the very notion of Web 2.0*, asserts that users should own their data in these sorts of scenarios, but the exceptions to his assertion prove that Web 2.0 is hardly the last word. A person's eBay reputational currency, iTunes preferences, and Facebook profile are neither open nor portable—by design. Google owns search history and mobile search location; Amazon owns search, review, and purchase history; cloud e-mail providers own substantial clues about identity. Data has thus become a new mode of lock-in, joining application compatibility, learning investments, and long-term licensing.

Network Effects

There's no question that successful software still exploits network effects. The more developers who code to a given platform—Facebook, Salesforce, or Google Maps—the more that standard gains authority: Note that none of those aforementioned businesses counts only as a Web site. One of the platform pioneers powerfully illustrates the point perfectly: Amazon once noted in its earnings conference call that it had 265,000 developers signed up to use its Web services, a huge number for a young technology. There are also powerful network effects among users, whether at eBay, MySpace, or such peer-to-peer content distribution services as BitTorrent: The more people who use the service, the more valuable it becomes. Conversely, when people defect in large numbers, the flywheel spins in reverse. Compare that one fact to consumer products, banking, automobiles, or pharmaceuticals, and we are reminded how significantly online dynamics depart from those of widget business or even most of the service sector.

Upgrade (and Therefore Revenue) Cycles

No longer is the objective to leverage a large installed base onto a new version of the product. Google makes money every hour of every day, and apart from acquisitions, we don't expect spikes in its revenues. Indeed, the escape from the cyclicality of product upgrade cycles may not yet be fully appreciated as analysts assess the new breed of software companies. The dependence of shrinkwrap software companies (that sell software as a product) on secondary revenue streams may become problematic: Oracle CEO Larry Ellison noted in an interview with FT that his company was collecting 90% margins on software maintenance.3 Customers can't be, and aren't, happy with those economics, so it is likely only a matter of time until competition and/or customer resistance change the model. SAP's attempt to move into the cloud and “information appliance” markets (where it encounters Sun+Oracle products) will be interesting to watch insofar as it represents a departure from the company's legacy business model.

Selling Software as a Product, One at a Time

Google once reported quarterly revenues that represented a year-over-year improvement of 58%. Did its sales force grow by 60% in a year? Highly doubtful. Although the company offers a few software products a customer can purchase, enterprise search hardware and software, hosted applications, and geographic information system tools amount to mere drops in that $29 billion annual bucket. An important facet of the software as a service trend is that in an increasing number of cases, users don't have the software on their own devices but access a server, the location of which is irrelevant, to get something done. As a result, the customer base (of advertisers) is dramatically smaller than the user base, which delivers favorable sales force performance metrics.

Accordingly, software distribution channels are being completely reinvented: The old goal used to be to get your product onto a shelf and/or catalog page at Computer City, Egghead, and MicroWarehouse. Note that all of those businesses are defunct, another indication of deeper change in the industry. In a related development that sheds further light on a complicated situation, PC Magazine subscriptions and ad pages dropped to the point where it ceased paper publication in 2008.

Retail Channel

Because it owns neither the PC hardware layer nor a content distribution channel, Microsoft is caught in conflicting trends here. Apple's retail stores are a powerful presence for the linked hardware-software platform, bringing in about $10 billion a year. At the same time, the demise of the PC-centric format hit Microsoft particularly hard: Best Buy, with troubles of its own and where PCs are displayed alongside toasters, cannot replicate the capabilities of a CompUSA of years gone by, not to mention an Apple Genius Bar, with its nearly-ideal selling environment. Apple's App Store/iTunes format constitutes yet another competitive front. Finally, online distribution of free applications or services serves as another way that software gets to users.

People Buy Features and Performance

There's a wonderful video that embodies this thinking perfectly: Enter “microsoft ipod” into the YouTube search bar. Microsoft apparently produced this spoof internally, illustrating the trend toward “speeds and feeds” in stark contrast to Apple's aura and powerful design sense. Just run down the standard old-school software questions in regard to Facebook or MapQuest:

- What is the recommended processor?

- How much free disk space is required?

- What is the minimum memory required?

- How many transactions per second can the application handle?

- How fast can the application render/calculate/save/etc.?

The very mention of these former performance criteria in regard to the most successful “applications” of our time highlights the discontinuity between where we are and where we were. It's critically important to note that the path from the PC-resident Lotus Organizer to Basecamp project management or the original Encarta CDs to Wikipedia involved a step-function change rather than evolutionary progression: Incremental improvements to existing products are often insufficient in times of radical innovation.

Hire the Best Technical Team

There's no question that high-caliber architects and developers matter. Look at the arms race among Microsoft, Amazon, Google, and Yahoo! to hire the giants of the industry. At the same time, Facebook is raiding Google for software engineers and managers by the hundreds. In addition, the outside-in dynamic of user-generated content also allows such sites as Twitter or Facebook to thrive. In these kinds of businesses, it's certainly imperative to get top-flight operations and data-center professionals, no question, but these folks are of a different breed compared to the breakthrough innovators of the sort represented by Google's Vint Cerf, Louis Monier (who spent time at AltaVista, eBay, and Google), and Gordon Bell at Microsoft.

The lowering of coordination costs facilitated by the Internet allows smart people to collaborate outside of institutions, as we saw in Chapter 9.4 With a target on its back as the dominant firm of the previous computing regime, Microsoft thus must compete on multiple fronts:

- Apple is proprietary, high margin, and design driven, a hardware+ software and fixed+mobile platform.

- Linux is free, user driven, organically evolving, and robust but ugly.

- Google is network-centric, mobility and geography-aware, with an ad-driven revenue model.

Competitive positioning relative to three such different models of software creation and distribution stands as a truly problematic proposition.

Rows and Columns

While I don't want to oversimplify and assert that value has migrated from nodes to links, the fact remains that the structure of business, personal connections, and information is looking much more like a spiderweb than a library card catalog. As scholarship from Rob Cross at the University of Virginia and others has illustrated, informal networks of personal contacts, once exposed, often explain a corporation better than the explicit titles and responsibilities.5 At the engineering level, the very concept of social networking behind Twitter, Flickr, and Foursquare represents a departure from a conventional relational database mentality. The world as a radial graph is a very different proposition from trying to fit reality into cells in a preordained and fixed database schema.

Looking Ahead

The corporate architectures at Microsoft, Google, and Apple mirror their varying approaches to the market. For roughly a decade Apple's share price included a healthy dose of respect for the management skill of Steve Jobs, in that particular context, to both envision and execute. Conversely, the achievement of Google, with the jury out on the model's staying power, may lie in leadership's balancing of individual brilliance at different layers of the hierarchy with financially realistic corporate objectives. Finally, Microsoft appears to be working hard to define an emerging man agement model as the founding generation hands off to new leaders.

Taken together, these tendencies are reshaping the software business: Programming (as in putting content together on radio or television) has joined programming (as in coding) as a core competency for many kinds of businesses that fall in the gaps between computing and media. The fusion also shakes up conventional media, as we noted earlier. The purely push-based media model, used to advertise things primarily for largely unmeasurable brand impact (unmeasurable at the level of the ad, particularly), is being challenged by viewers and readers who want more participation in both the experience (what used to be called consumption)6 and the process (formerly known as publishing or content creation). As blogs, social networks, and professional content get further jumbled, and as NewsCorp founder Rupert Murdoch seems to be intent on demonstrating, the business models of media, software, gaming, and information transport will continue to become further intermixed.

Notes

1. Ray Ozzie announced himself as Bill Gates's successor as chief software architectat Microsoft with a memo entitled “The Internet Services Disruption,” dated November 9, 2005, www.zdnet.com/blog/web2explorer/page/ray-ozziethe-internet-services-disruption/54.

2. Eric Raymond, “The Magic Cauldron,” http://catb.org/~esr/writings/magiccauldron/.

3. Richard Waters, “Transcript: FT Interview with Larry Ellison,” Financial Times April 18, 2006, www.ft.com/cms/s/2/5f7bdc18-ce85-11da-a032-0000779e2340.html#axzz1QPPGvl3F.

4. Clay Shirky, Here Comes Everybody: The Power of Organizing Without Organizations (New York: Penguin, 2008).

5. Rob Cross, The Hidden Power of Social Networks: Understanding How Work Really Gets Done in Organizations (Boston: Harvard Business School Press, 2004).

6. See, for example, SocialVibe, which explicitly contracts for viewers to watch ads on their time schedule rather than on an interruption model.

*Web 2.0 was a notion revolving around foundational changes from a static, broadcast model for the Web to a more dynamic, people-powered environment; usergenerated content is an essential component of the term. Key examples of the tendency include Flickr, Google Maps, Wikipedia, and Facebook.