THE ROLE OF INSURANCE

‘Buy enough insurance for what can go wrong, so you can invest for what can go right.’

Nick Murray, financial commentator, author and speaker

The extent to which you need insurance will depend on a number of factors personal to you, including available financial resources, lifestyle spending, financial commitments and family health history. Perhaps a more important factor is your view on insurance and whether it is a good use of the family wealth to either insure or not insure and fund the consequences yourself (self-insuring). In addition, in the case of inheritance tax, much will depend on your views on wealth succession and whether you are concerned to replace any wealth lost to the state in tax upon your demise.

In the context of your wealth plan, there are six possible uses of insurance:

- To protect against loss or damage to material assets such as property, vehicles and possessions using general insurance (GI).

- To protect against unforeseen but financially significant expenditure on healthcare and/or long-term care using private medical (PMI) and long-term care insurance (LTC) respectively.

- To protect against the loss of earned income as a result of being unable to work due to ill health using permanent health insurance (PHI).

- To provide protection for your surviving family or business against a known liability such as a mortgage, business loan or business buyout that may be called in following your death or critical illness/permanent disability.

- To protect against outliving your pension resources by transferring investment and longevity (living longer than average) risk to an insurance company through the purchase of a traditional or limited-term annuity.

- To replace the value of your estate that would be lost to inheritance tax (IHT) following death through the use of either whole-of-life insurance or seven-year level or decreasing-term insurance.

Insuring property and possessions

Most people under-insure their property and physical possessions, because they underestimate the true replacement costs at the outset and/or because they fail to update it against inflation. While price is often a major factor in choosing general insurance, it really should be only one factor. While none of us expects to have to call out the fire service, if we do so we want to know that they haven’t gone for the cheapest fire engine that fails to start when they get our call! General insurance is the same in the sense that if you need to claim you don’t want to find that the small print excludes your claim and/or getting paid out takes you ages (not to mention wasted hours dealing with the claims department).

Higher-value homes, cars and possessions need to be covered by insurers that understand and specialise in providing such cover. I recommend using the services of a reputable and experienced general insurance adviser to assess general insurance coverage needs. A good adviser will be happy to visit you at your home and carry out a proper assessment of your needs and suggest a comprehensive solution. You’d be amazed at the real cost of replacing the contents of even a modestly furnished home and wardrobe.

A number of insurers in the higher-value market can provide a single insurance policy that covers all property (including second homes and rental properties), vehicles (including family members and staff) and travel insurance (including business travel and winter sports). I can say from personal experience that having one policy to cover these risks is much easier to administer and ensures nothing ‘slips through the gaps’. See Figure 13.1.

Insuring against ill health

Private healthcare

While the National Health Service (NHS) provides comprehensive and generally good-quality healthcare, particularly for acute conditions, many families like the choice, flexibility and speed associated with private healthcare. While it is perfectly possible to pay for private healthcare as it is needed, whether or not this is viable will very much depend on the level of your financial resources, your expected quality of health throughout your lifetime and the treatment required.

Figure 13.1 Combined high-value general insurance policy

For most people it will be preferable to put in place some form of PMI to protect against large medical costs and, as a result, protect the family wealth. The problem with PMI is that it becomes quite expensive as you get older, given the higher risk of claims arising. There are several ways that you can minimise the cost of PMI, including having a high excess, accepting a restricted choice of hospitals, restricting certain medical conditions, and the last and probably most popular option being able to restrict private healthcare provision to instances in which care could not be provided by the NHS within a specified time period, typically six weeks.

Certain long-term health conditions are not treated by the NHS where the primary need is not nursing care. If you live in England or Wales you will be required to pay for any long-term care, whether this is in your own home or a residential care home. Long-term care is most likely to be required in older age and certain health conditions, which are not necessarily life-threatening, can last for many years, causing a serious drain on the family wealth. Long-term care is covered in more detail in Chapter 19.

Care fees

Long-term care insurance (LTCI) is similar to PMI in that it pays some or all of the costs of care but only if the insured is unable to perform a number of ‘activities of daily living’ (ADLs) or is permanently cognitively impaired (senile). ADLs include washing, moving, dressing, feeding, using the toilet and getting in and out of bed, and it is usual for the policy to require the policyholder to fail at least two, but more often three, of these before a claim will be paid. LTCI will continue to pay a claim until either recovery or death.

There are relatively few providers active in the LTC market, compared with other types of insurance, but those that are have a lot of experience and useful products. The only current LTCI policy available in the UK market is a care fees annuity – this is designed for those who need care immediately or on a deferred basis and wish to pay a single lump sum to pass the long-term liability for funding care costs to an insurance company. As with all annuities, those who live beyond the average will be better off and those who don’t will be worse off. An immediate or deferred care annuity can be useful if it is essential to have certainty about being able to afford the cost of care but financial resources are limited. However, this still doesn’t mean that all future care costs will be covered, particularly if care costs rise faster than the escalation factor (if any) added to the policy.

Critical illness

Critical illness (CI) insurance, originally known as ‘dread disease’ insurance, pays a lump sum on the diagnosis of any one of a range of serious illnesses or possibly in the event of suffering a permanent and total disability (PTD). However, it’s important to note that some types of cancer are not covered and to make a claim for some illnesses, such as a stroke, you need to have permanent symptoms. For other conditions, such as a heart attack, the illness must be of a specified severity. Examples of conditions on which a valid claim would be paid are shown below:

Alzheimer’s disease before age 65 – resulting in permanent symptoms.

Aorta graft surgery – for disease and trauma.

Aplastic anaemia – resulting in permanent symptoms.

Bacterial meningitis – resulting in permanent symptoms.

Benign brain tumour – resulting in permanent symptoms.

Benign spinal cord tumour.

Blindness – permanent and irreversible.

Cancer – excluding less advanced cases.

Carcinoma in situ of the breast – requiring mastectomy or lumpectomy.

Carcinoma in situ of the testicle – requiring surgery to remove one or both testicles.

Carcinoma in situ – urinary bladder.

Cardiomyopathy.

Cerebral aneurysm – treated by craniotomy or endovascular repair.

Coma – resulting in permanent symptoms.

Coronary artery bypass grafts – with surgery to divide the breastbone (a payment is available to pay for surgery after being placed on an NHS waiting list).

Creutzfeldt-Jakob Disease (CJD) – requiring continuous assistance.

Deafness – permanent and irreversible.

Encephalitis.

Heart attack – of specified severity.

Heart-valve replacement or repair – with surgery to divide the breastbone.

HIV caught from a blood transfusion, by physical assault or at work.

Kidney failure – requiring dialysis.

Liver failure – end stage.

Loss of independent existence – resulting in permanent symptoms.

Loss of hands or feet – permanent physical severance.

Loss of speech – permanent and irreversible.

Major organ transplant.

Motor neurone disease – resulting in permanent symptoms.

Multiple sclerosis – with persisting symptoms.

Multiple system atrophy – resulting in progressive and permanent symptoms.

Non-malignant pituitary adenoma with specified treatment.

Open heart surgery – with surgery to divide the breast bone.

Paralysis of limbs – total and irreversible.

Parkinson’s disease before age 65 – resulting in permanent symptoms.

Pneumonectomy – for disease or trauma.

Pre-senile dementia before age 65 – resulting in permanent symptoms.

Primary pulmonary arterial hypertension – resulting in permanent symptoms.

Progressive supranuclear palsy.

Prostate cancer low-grade.

Pulmonary artery surgery – with surgery to divide the breastbone.

Removal of an eyeball as a result of injury or disease – permanent physical severance.

Severe lung disease/respiratory failure – of specified severity.

Stroke – resulting in permanent symptoms.

Systemic lupus erythematosus – of specified severity.

Terminal illness.

Third-degree burns – covering 20% of the body’s surface area or 50% of the face’s surface area.

Total permanent disability – unable before age 65 to look after yourself ever again.

Traumatic head injury – resulting in permanent symptoms.

This list of conditions, provided by Zurich Assurance Ltd (one of the largest critical illness insurers in the UK), is not a standard offering across all policies and providers – the list will vary in number and interpretation of each illness depending on the provider.

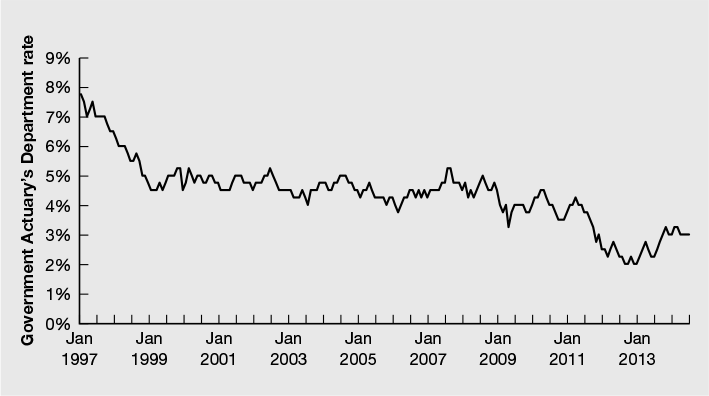

Sometimes CI and/or PTD benefit can be provided in addition to or in advance of normal life insurance via a single protection policy. Alternatively, CI/PTD can be provided as standalone cover. The cost of CI/PTD cover has risen quite sharply over the past ten years, and it becomes particularly expensive for those over the age of 45 and/or smokers, due to the increased risk of a claim arising. Whether or not you need CI/PTD cover depends on a number of factors, including the quality-of-life implications that would arise in the event of you suffering a serious illness or permanent disability. CI/PTD cover is a ‘nice to have’ once you’ve sorted out other insurance cover. Table 13.1 gives an example of the kinds of costs you could expect for £100,000 of cover.

Table 13.1 Illustrative cost of £100,000 CI/PTD cover – annual premiums

| Age at outset | CI only | CI + PTD |

| 30 | £228.47 | £238.16 |

| 35 | £293.95 | £306.87 |

| 40 | £381.76 | £399.70 |

| 45 | £544.84 | £570.67 |

| 50 | £749.53 | £786.94 |

| 55 | £947.77 | £996.48 |

Source: IRESS Exchange Comparison Services, May 2014 non-smoker, to age 60, class 1 occupation, non-smoker.

Insuring against loss of income

Permanent health insurance is neither permanent nor health insurance (which may explain why it is also referred to as income protection insurance) but provides a regular tax-free (as long as it is an individual and not a group policy) income if you are unable to work until recovery, death or the retirement age selected at the outset. The benefit is paid after a deferred period, which can be between 1 and 12 months, and is selected when the policy is established. Generally, the longer the deferred period and the earlier the retirement age, the cheaper the cover will be. Premiums are either guaranteed throughout the policy term or subject to review periodically, with guaranteed premiums being more expensive at the outset. It is also possible to have the income benefit increasing before and/or during a claim to provide some inflation protection. Table 13.2 illustrates the possible cost of £10,000 annual PHI cover.

Table 13.2 Illustrative cost of £10,000 pa PHI cover – annual premiums

| Age at outset | 3 months deferred | 6 months deferred |

| 30 | £74.08 | £68.02 |

| 35 | £85.08 | £75.79 |

| 40 | £102.80 | £86.30 |

| 45 | £130.72 | £104.09 |

| 50 | £174.37 | £142.37 |

Source: IRESS Exchange Comparison Services, May 2014 non-smoker, to age 60, class 1 occupation, own occupation work definition, non-smoker.

The basis on which benefits will be paid will also depend on the definition used to describe incapacity. Incapacity can be described as unable to perform:

- ‘any occupation’

- ‘any occupation for which you are suited or trained’

- ‘your own occupation’.

The first definition is the widest and means that you can’t do any work, whereas the last is the narrowest and means that if you can’t do the job you were doing prior to the incapacity, the claim will be paid. If you have a very skilled or specialist occupation, ‘own’ occupation is preferable, but it is more expensive.

PHI is arguably one of the most underused types of policy, for reasons that have been attributed to the perceived time taken to underwrite benefits, complexity and a lack of awareness by individuals of the likelihood of needing to make a claim. Nevertheless, if you are dependent on earnings for your current and future lifestyle, it is the only insurance that can provide prolonged protection against their loss. While the UK consumer organisation Which? states that income protection is must-have insurance for most working adults,1 apparently twice as many people choose to insure their pet or mobile phone instead.2 Official 2013 statistics showed that 2.56 million people were claiming illness- or injury-related benefits from the government and, of those, 2.08 million people had been off work and claiming illness-related benefits for more than six months.3 In 2011/12 in the UK 27 million working days were lost due to illness and injury and 212,000 injuries led to a three-day or longer absence.4

If you have income protection provided for you via your employment then the premiums paid by your employer will not be a taxable benefit in kind. However, if you make a valid claim under the policy, the benefit will be payable to you via the PAYE system and taxed as normal salary. Long-term claims are usually paid directly by the insurer, but they will still be taxed at source via the PAYE system.

If you are already financially independent but still generating income from employment or self-employment, there is no need for you to worry about insuring against the loss of that income in the event of ill health or disability. However, if you are using that income to make regular gifts to a family trust or one or more individuals, and you want to continue that in the event of ill health, or if you are not quite financially independent and are relying on future earned income to add to your financial resources, then insuring against loss of income should be a priority.

Insuring against liabilities arising on death

If you have not reached financial independence and have dependants, you will probably need life insurance to provide the financial resources that would not be generated following your death. If you are already financially independent, whether or not you are still working, there are also several situations in which life insurance might be required as part of your overall wealth plan, such as child maintenance obligations and/or covering any inheritance tax liability.

Family income benefit

Family income benefit (FIB) is a special type of life policy that provides regular payments (free of income tax) in the event of the policyholder’s death until the end of the policy term. In effect it is like life insurance in instalments. An FIB policy is likely to be cheaper than a term insurance or whole-of-life policy with the same term and total benefit level. This is because the insurer’s risk gradually reduces as the policy progresses. For example, with a 20-year level-term policy of £500,000, if the insured died after 19 years and 330 days, the insurer would still have to pay out £500,000. With an FIB policy with £25,000 of annual benefit (a potential total payout of £500,000), if the insured died after 19 years and 330 days, the insurer would pay out only about £2,000, being 1/240th of the total initial benefit. Another benefit of FIB cover is that it avoids the need to have to invest funds to generate an income and therefore keeps things simple at what may be a very difficult time. Some policies allow future benefits to be paid as a discounted lump sum if necessary. Figure 13.2 gives an idea of how an FIB policy works while Table 13.3 illustrates the annual costs of FIB cover.

Figure 13.2 How a family income benefit policy works

FIB offers very good value protection for those people still earning income and who want to replace it in the event of their death and where they do not want, or have insufficient resources, to self-insure. However, even if you are financially independent FIB might still be useful as part of an overall estate plan, particularly if you have agreed to fund the education of family or friends or have other regular financial commitments, such as child maintenance payments, that you would like to continue in the event of your death. In this scenario an FIB policy provides a simple and targeted solution. Please note that to avoid inheritance tax it is usually advisable to assign life policies into a flexible trust. In Chapter 21 I explain the main types of trusts and their application.

Table 13.3 Illustrative cost of FIB cover – annual premiums

Source: IRESS Exchange Comparison Services, May 2014 non-smoker, class 1 occupation, non-smoker.

Term policy

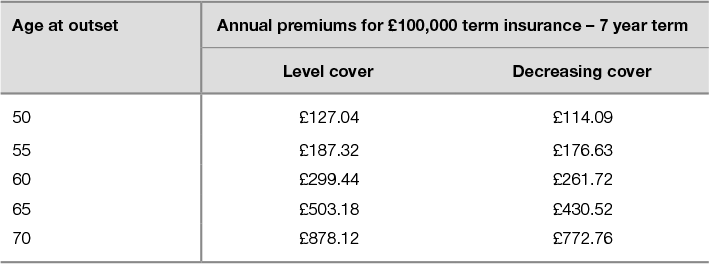

Another type of life assurance policy is a term protection policy. This type of policy has a set term of between 1 month and as long as 40 years, during which a lump sum (whether that is level, decreasing or increasing) would be paid out upon your death providing that the premiums are paid on time. The policy never accrues a value unless a claim is paid and premiums can be guaranteed to remain the same throughout the term. Alternatively, for a lower initial level of premium, future premiums can be subject to adjustment if the insurance company’s rates change. Table 13.4 illustrates the cost of term insurance.

Whole life

A whole-of-life policy is designed to provide life cover, usually, until age 99. Premiums can be guaranteed or reviewable. If reviewable, premiums can be set at a lower initial level (usually the first ten years, then at five-yearly intervals), but expect steep increases in the future. The key benefit of this type of policy is that the cover continues as long as you pay the premiums.

Table 13.4 Illustrative annual costs of term insurance

| Age at outset | £100,000 payable on death within 20-year term |

| 30 | £58.64 |

| 35 | £73.22 |

| 40 | £95.39 |

| 45 | £135.61 |

| 50 | £203.07 |

Source: IRESS Exchange Comparison Services, May 2014 non-smoker, class 1 occupation, non-smoker.

Relevant life policy

A relevant life policy (RLP) is essentially a life policy that is taken out by a company, limited liability partnership (LLP) or sole trader for the benefit of an employee. Subject to certain conditions, the premiums will be deductible against corporation tax (or profits in the case of a sole trader or members of a partnership) and not assessed as a benefit in kind for income tax and national insurance purposes against the employee. Partners, LLP members and sole traders are not employees for the purposes of an RLP. If, however, you run your business via a limited company and are also a director, then you are treated as an employee, whether or not you take substantial remuneration. This opens up the possibility of arranging your life insurance through your business and, as a result, lowering the cost substantially compared with a personal policy.

The company, as your ‘employer’, would apply for the RLP and as part of the application process would also complete special RLP trust documentation. The company would therefore be a trustee of the RLP, but it is perfectly acceptable to appoint additional individual trustees such as your spouse. The RLP benefit would be payable if you die before you reach age 75. Other benefits available are in respect of ill health, disablement or death by accident, but these benefits are payable only as long as you are still in employment. In the event of your death, the life policy benefit will be paid by the insurer to the trustees of the RLP. The trustees would have discretion as to who should receive the benefit from the classes of beneficiaries specified in the trust. If you have previously completed a nomination form addressed to the trustees of the RLP trust, this will give a non-binding expression of your wishes to them as to who you would prefer to gain from the death benefits. This is similar to the method of nominating beneficiaries under a registered pension scheme.

Any benefit payable for ill health or disability will be paid in the same way as the death benefit, i.e. to the trustees of the trust. As the employee is one of the trust beneficiaries, the trustees can make the payment either to the employee or to their family. The trustees will need to consider all the circumstances at the relevant time in order to decide who should receive the benefit. There is no statutory maximum amount that may be provided by an RLP. Insurers may have their own commercial maxima and associated underwriting/financial underwriting limits and the sum assured should be reasonable in relation to securing deductibility for premiums paid by the employer under the ‘wholly and exclusively ‘ rules on the provision of benefits under the plan.

There are no other tax implications as long as the life assured is alive. Once the death benefit is paid to the trustees, as the trustees will hold the benefit subject to a discretionary trust, then the normal IHT rules that apply to the taxation of discretionary trusts (the ‘relevant property regime’) will also apply here. This will mean potential periodic and exit tax charges (see Chapter 21).

If the life assured leaves service and takes up a new employment, it may be that the new employer will be prepared to take over payment of the premiums and so keep the cover in force. Otherwise the policy would come to an end.

An RLP in practice

Darren owns a trading business called XYZ Ltd, of which he is also a director. As such he qualifies as an employee of XYZ Ltd and so the company can take out an RLP on his life. Darren takes a salary of £20,000 and regular dividends of £100,000 per annum. After taking into account his existing personal assets and the net value of the business if sold, it is determined that Darren needs life insurance of £2 million to meet his family’s lifetime needs. XYZ Ltd applies for an RLP with ABC Life, which provides the necessary special RLP trust documentation. Because the sum assured is reasonable given Darren’s historic earnings from the company and the RLP trust documentation complies with the RLP rules, the policy meets the ‘wholly and exclusively’ test. This means that the premium will be deductible from XYZ Ltd’s profits for corporation tax purposes.

On the basis that the company’s corporation tax rate is 20%, the cost of this policy when compared with arranging the same one personally funded from after-tax income would be as shown in Table 13.5. The annual cost differential in this example would be £1,333. Larger policies would generate even higher savings.

Table 13.5 Comparison of personal policy and relevant life policy

| Personal | RLP | |

| Gross profit | £3,333 | £2,000 |

| RLP premium | Nil | £2,000 |

| Corporation tax @ 20% | –£667 | Nil |

| Net dividend as paid | £2,666 | Nil |

| Income tax @ 25% of net dividend | –£667 | Nil |

| Net cash available | £2,000 | N/A |

| Effective cost | £5,555 | £2,000 |

Note: these figures are purely to illustrate the cost differential between a personally funded policy and a company funded RLP. Actual cost will vary depending on age, benefit level, premium frequency and underwriting status.

In summary, an RLP offers the following benefits to employees (including controlling directors):

- tax relief on the premiums for the employer, subject to satisfying the ‘wholly and exclusively’ test

- no assessment of premiums on the employee as a benefit in kind

- premiums not taken into account in determining the available annual allowance for registered pensions

- no assessment for the purpose of employer or employee National Insurance contributions

- benefits arise free of income tax and inheritance tax

- benefits do not count towards the lifetime allowance for pension purposes.

If you qualify as an employee and need life insurance protection, then a relevant life policy is likely to be the most cost- and tax-efficient way of providing cover. It is also likely to be most cost-effective to arrange the policy on nil-commission terms and pay a fixed fee for advice and arrangement.

Loan protection

If you have any personal or business borrowing, check the position in the event of your death. Some loans have a clause that requires the loan to be repaid if the principal borrower or director dies. It is usually a better use of the family’s or business’s money to pay insurance premiums than to be scrambling around for cash to pay the bank at such times. Also check that you are getting good value for money as insurance offered by banks and other lenders is rarely the best value, particularly for large policies. The cost of life insurance has fallen a lot in the past ten years as life expectancy has increased. A term protection-only policy is usually the right type of policy in this situation.

Business protection

If you are a partner or one of several shareholders in an unquoted business, you need to ensure that your business or co-business owners have the means to fund any buyout of your share in the event of your death. There are two components to this planning: the agreement to buy and sell and the insurance or financial means to fund the transaction. A double-option agreement (which allows either party to enforce it) is usual in the case of individuals, giving both sides the option to buy/sell and a life assurance policy to fund some or all of the buyout, without impairing the retention of business or agricultural property relief against IHT on the business assets – see Figure 13.3.

Figure 13.3 Business protection and double option agreement

The life policy can either be owned by the other business owners or by you and written in a special business trust for their benefit. You need to make sure that you have similar agreements and policies for your other co-owners. Where the company is to be the buyer of your shares in the event of your death, the life policy will be taken out by the company and the company’s articles of association need to be checked to ensure that the company is permitted to buy its own shares. Term protection or whole-of-life is suitable to provide this cover, but they have different tax treatments on premiums and benefits. This is a complex area and specialist advice is required to ensure that things are structured correctly and the most beneficial tax treatment is secured.

Insuring against living too long

A traditional pension annuity is an insurance policy that allows you to exchange pension capital for a specified and usually guaranteed income throughout life. The life company usually prices an annuity based on four factors: general yields from long-term, fixed interest securities, life expectancy, administration costs and profit margin. Those annuitants who die earlier than the average subsidise those who live longer than average. Therefore those who do best from annuities are those who live the longest. The problem is that none of us knows exactly when we are going to die and so annuities are a bit of a lucky dip.

Henry Allingham is an extreme example of when buying an annuity with a pension fund can turn out to be a good choice. A veteran of the First World War, Henry died in 2010 at the age of 113, having received income from the pension annuity he purchased in 1962, aged 65, for 48 years. It was the insurance company that took the risk that Henry would live too long, which turned out to be a good deal for Henry and not such a good one for the annuity provider. Figure 13.4 shows average life expectancy for various age groups.

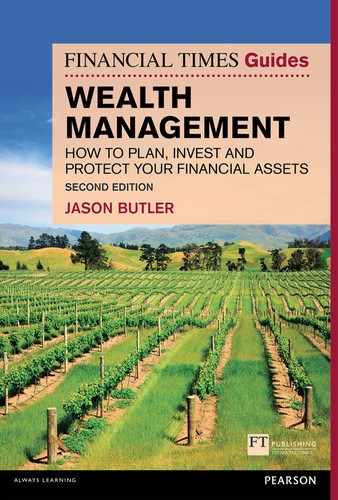

While they do provide certainty, traditional annuities lack flexibility and may be poor value for money if you die early or annuity rates improve in the future. As illustrated in Figure 13.5, annuity rates have actually been falling over the past few decades, mainly due to a fall in the yields available from long-term gilts and improving life expectancy. Whether this trend will continue is debatable, particularly if long-term interest rates rise in the future. As a general principle, it doesn’t make sense to take longevity risk (i.e. the risk of living too long) and you should look to start purchasing an annuity or a series of annuities over time between the ages of 70 and 80 at the latest. We discuss the options for taking pension plan benefits in Chapter 18, where you will find a fuller explanation of the key factors that will influence your decision on whether or not, or the extent to which, you should buy a pension annuity with your pension pot.

Figure 13.4 Life expectancy at different ages

Source: Office for National Statistics. Period expectation of life: based on unsmoothed calendar year mortality rates from 1981 to 2012 and projected mortality rates from the 2012-based national population projections.

Figure 13.5 Historic annuity rates

Source: Scottish Life based on GAD tables.

Inheritance tax (IHT)

If you have an inheritance tax liability, which you can’t or don’t want to carry out any planning to reduce or avoid, or perhaps you’ve done as much planning as is practical or with which you are comfortable but you are concerned about the loss of your family’s wealth to the Exchequer, you may want to consider the role of life insurance. Sometimes it is a better use of family money to buy life insurance equal to some or all of the IHT liability. While paying insurance is in effect the same thing as paying some of the IHT in advance, it does have the benefit, for those in reasonable health, of being simple and allows you to retain maximum flexibility and control over your wealth.

Table 13.6 illustrates the total cost of guaranteed whole-of-life insurance for different amounts of cover at various ages. A joint whole-of-life policy is usually the most competitive policy for couples, but single people might find a term policy better value. In any case the cost of the insurance is likely to be much less than the tax liability, in some cases a lot less. Insurance is not a panacea to IHT planning, but as one of a range of possible solutions it is worthy of consideration.

Table 13.6 Illustrative cost of £1 million long-term life cover – annual premiums

| Age at outset | Whole-of-life policy to age 99 |

| 55 | £8,375.28 |

| 60 | £11,844.96 |

| 65 | £17,756.04 |

| 70 | £29,674.80 |

| 75 | £43,473.25 |

Source: IRESS Exchange Comparison Services, May 2014 non-smoker.

If you’ve made an outright gift for which you need to survive seven years before it falls out of your estate, you may be concerned about the IHT liability that might arise should you not survive the required seven years. In this scenario a short-term life policy can be effected, with the cover equal to the tax liability. The policy, known as a gift inter vivos (‘in life’), can be on either a level or a decreasing basis, depending on whether your nil-rate band is available (see Table 13.7). The policy is written subject to a trust to ensure that the benefit would remain outside your estate and be available to your beneficiaries. There are only a few insurers active in this market and the costs don’t seem to be significantly different for those in good health, although if you have a health condition it is probably worth making multiple, simultaneous applications (any medical examination required can usually be done once and the results shared between insurers) to see which provider offers the best terms.

Table 13.7 Illustrative cost of £100,000 gift inter-vivos life cover

Source: IRESS Exchange Comparison Services, May 2014 non-smoker.

Buying any insurance involves a known cost in return for transferring a risk to an insurance company. In the context of wealth planning the key issue is whether the cost of insurance is a better use of family wealth compared with accepting the possibility of a high-impact but very low-probability risk.

1 www.which.co.uk/money/insurance/reviews-ns/income-protection/

2 Think Tank Demos (2013) ‘Financial protection’, April.

3 Department for Work and Pensions, March 2013.

4 Health and Safety Executive Annual Statistics 2011/12.