MINIMISING PORTFOLIO TAXATION

‘An income tax form is like a laundry list – either way you lose your shirt.’

Fred Allen, American comedian

If your investment capital is not held in a tax-free or tax-deferred account such as an individual savings account (ISA), self-invested personal pension (SIPP), small self-administered scheme (SSAS) or offshore portfolio bond (OPB), then tax will be due on interest, dividends and capital gains to the extent that they exceed your individual personal allowance and gains exemption.

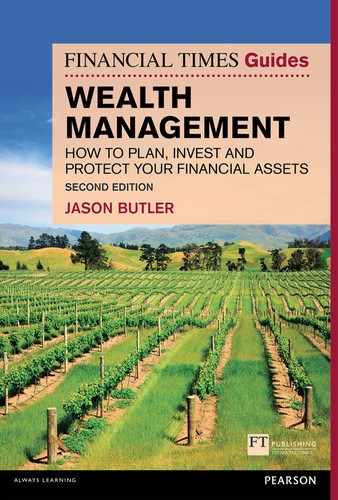

To determine whether total capital gains are taxable you need to first deduct all capital losses arising within the same tax year. Net capital gains in excess of the annual exemption can also be reduced by offsetting any carried forward losses available from previous tax years. Any net gains remaining, which exceed the annual exemption, are then taxed at either 18% or 28% depending on whether or not there is any unused basic-rate income tax band available.

Claiming losses

Losses relating to tax years prior to 1996/97 don’t have a time limit for claim and can be claimed when you need to use them. For losses that arose in the 1996/97 tax year or later, you must have first submitted a claim to HMRC via your self-assessment tax return or, if you don’t complete one of those, by writing to HMRC, within a time limit. The time limits are as follows:

Please note that carried forward losses must be used where there are taxable gains. You can’t decide not to use them because, for example, you’d rather pay capital gains tax at 10% on gains subject to entrepreneurs’ relief and ‘save’ the carried forward losses for use against future gains that might be subject to higher rates of tax.

Capital gains – the 30-day rule

If you crystallise a capital gain by selling and then immediately repurchasing an investment – what used to be called bed-and-breakfasting – it will be treated as having no effect for CGT purposes. However, there are other ways of achieving similar results:

- Bed-and-ISA: you can sell an investment, e.g. shares in an open-ended investment company, and buy it back immediately within an ISA. For 2014/15 the maximum ISA investment is £15,000.

- Bed-and-SIPP: this is a similar process to bed-and-ISA, but the cash realised is used to make a contribution to a SIPP or any other suitable pension plan. The reinvestment is then made within the pension. This approach has the added benefit of income tax relief on the contribution and may also offer a higher reinvestment ceiling than an ISA, depending on your earned income and other pension contributions.

- Bed-and-spouse: you can sell an investment and your spouse can buy the same investment without falling foul of the 30-day rule. However, you cannot sell your investment to your spouse – the two transactions must be made separately through the market.

- Bed-and-something-very-similar: the growing number of funds that track UK and international stock market indices has created an opportunity to replicate the tax benefit of the old bed-and-breakfast strategy. For example, if you hold the ABC UK FTSE All-Share unit trust, you could sell it and immediately reinvest in the XYZ FTSE All-Share Exchange Traded Fund. Your underlying investment – shares in the constituents of the FTSE All-Share Index – will not alter but, because the fund entity (not necessarily the fund provider) has changed, you will escape the 30-day rule.

While your total taxable income now determines the rate of CGT you pay, capital gains do not impact on the amount of income tax you pay. Therefore, it is now important to carefully manage taxable income, as far as possible, to allow any taxable capital gains to benefit from the lower 18% tax rate, to the extent that taxable capital gains fall below the higher-rate income tax threshold of circa £32,000 in excess of the personal income tax allowance.

The way that investments are taxed can have a significant impact on overall returns. This is particularly relevant where the differential between income tax and CGT is wide, with the top rate of income tax currently 45% (the effective rate is 60% for income between £100,000 and £120,000), compared with CGT of up to 28%.

Understanding the composition of portfolio returns – interest, dividends or capital gains – helps us to consider how the returns will be taxed using different tax structures. Although there have been major changes to investment taxation over the past few years, for UK-resident and domiciled individuals these apply at the investor level, not the tax wrapper level, and relate to the income and CGT arising. All companies (including UK life insurers) continue to be taxed under the existing rules and as such will qualify for indexation allowance on capital gains.

The key factors that need to be taken into account when considering investment location are as follows:

- use of your personal CGT annual exemption

- whether or not you have any unused basic-rate income tax band

- your need for regular withdrawals to meet expenditure needs

- the amount of periodic rebalancing likely to be necessary to keep your portfolio consistent with your risk profile

- whether or not you have a spouse or civil partner with whom you can share the portfolio taxation options

- whether and to what extent the portfolio is to be held within a trust or pension structure, perhaps as part of other tax planning components

- the ability for CGT to be ‘washed out’ on your death, i.e. extinguished

- the product or tax wrapper charges incurred

- the type of asset held, i.e. deposit, fixed interest, equity income or growth, or real estate investment trust shares

- the type of investment required – some types of investments and funds are not permitted to be held within certain tax structures

- the administrative work and professional costs associated with tax reporting

- the holding period of the portfolio, because compounding works best over the long term

- whether or not you also wish to integrate inheritance tax planning with your investment capital.

The individual savings account (ISA) allowance

This allows a UK resident1 to hold cash, fixed interest or equity investments in a tax-free environment, although withholding tax on dividends may not be reclaimed. The limit is £15,000 per person per tax year for those aged18+, so couples can shield £30,000 p.a. from the taxman if both invest in an ISA. An ISA is most attractive for those who pay higher-rate income tax and who would generate capital gains of more than £11,000 per tax year. Having said that, it is often possible to invest in funds via an ISA at no extra charge, so just from an administration perspective an ISA is likely to be the foundation of your portfolio tax management strategy.

The four main non-pension investment tax wrappers

Beyond ISAs, the four types of tax wrapper most commonly used to hold an investment portfolio are:

- Collective funds held via a nominee account or in own name.

- An onshore investment bond.

- An offshore investment bond.

- A family investment company.

If you have a substantial portfolio, it is likely that a combination of these tax wrappers might be the best solution, but it will be influenced very much by the underlying investment strategy. The tax treatment of each wrapper is set out in Table 16.1.

Collective funds

Onshore open-ended funds and investment companies are exempt from CGT on disposals arising within the fund and generally corporation tax is not payable, provided that income is distributed to investors. At the investor level, a flat CGT rate of 18% or 28% (depending on the investor’s taxable income) is charged on disposals of units or shares in such a fund. CGT is payable only if such realised gains exceed the investor’s annual exemption, after first taking into account any losses arising in the current tax year or those carried forward from previous tax years. Non-, basic-rate and corporate taxpayers receive dividends from equity-based collectives free of any additional tax liability, although withholding tax on those dividends may not be reclaimed. Higher-rate (40%) and additional-rate (45%) taxpayers pay an effective tax of 25% and 30.55% respectively of the net dividend paid.2

Table 16.1 Comparison of tax treatment of main non-pension tax structures

* For a detailed explanation of top slicing relief, please see Chapter 15.

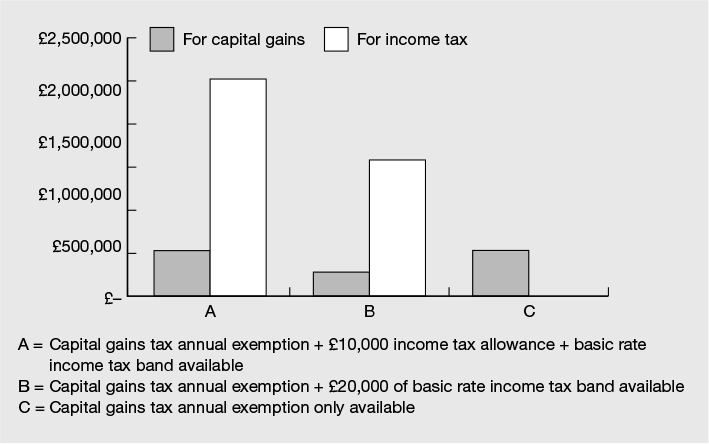

Offshore investment funds are deemed to be either ‘reporting’ or ‘non-reporting’ for tax purposes. A reporting fund declares the income arising within the fund, whether this is paid out to investors or not. The investor is then responsible for paying income tax, at their highest rate, on that reported income. Depending on the nature of the underlying holdings, this income will be taxed as either interest or dividends. When the investor comes to dispose of their holding, any increase or decrease in value is then subject to CGT treatment.

Sometimes, the reported income in a tax year is higher than the income that has been distributed to the investor. If the fund is held in a nominee or other type of investment platform, the investor may mistakenly assume that the tax voucher issued by the nominee or investment administrator is equal to the total income reported by the fund manager. However, unless the investor checks the investment fund’s annual report, they will not know if the reported income is higher than the distributed amount received by the nominee. If you hold reporting funds, either direct or via nominee, you must check the fund’s annual report to make sure that you have declared all reported income, not just what you have received as dividends or that has been detailed in the nominee’s consolidated annual tax report.

An offshore non-reporting fund is any fund that does not have reporting fund status, usually because it declares neither income arising within the fund nor any capital gains. As such no tax is payable by the investor until the holding is disposed of. If they are a UK-resident and domiciled person then income tax will be paid on the entire uplift in value of their holding, although no allowance is provided for losses against other taxable income. Many ETFs and most alternative investment strategies such as hedge funds and structured products are offered through non-reporting funds. This adverse tax treatment makes non-reporting funds unsuitable for most taxable investors, unless the fund is held within a tax wrapper such as a pension or an offshore bond.

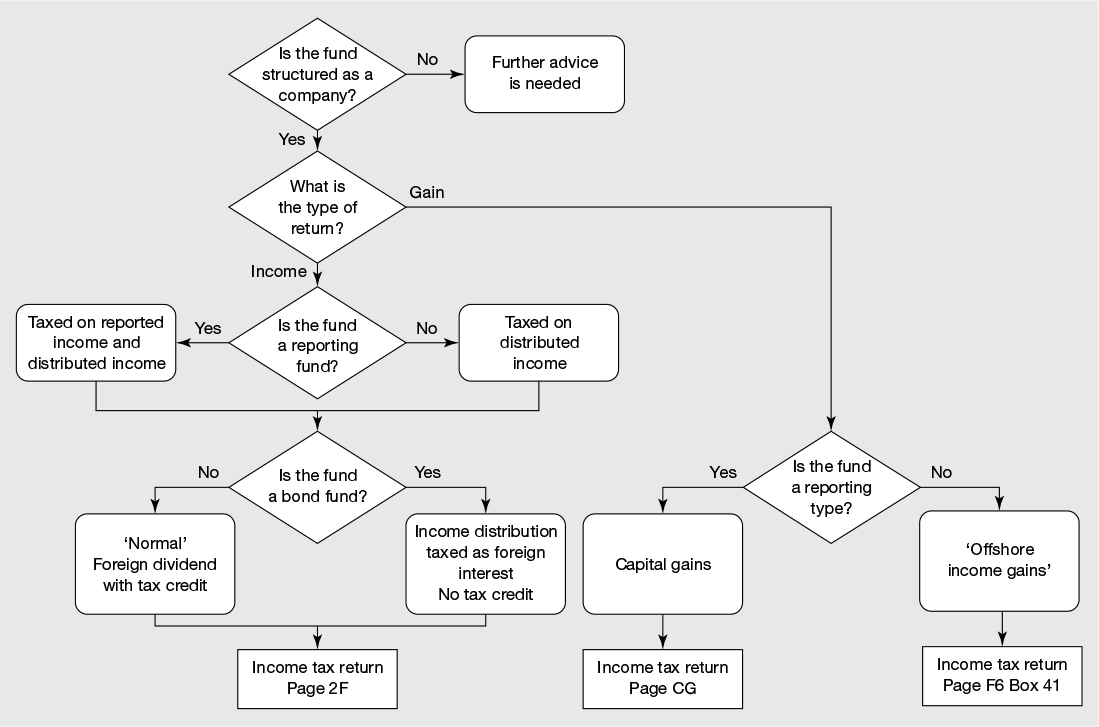

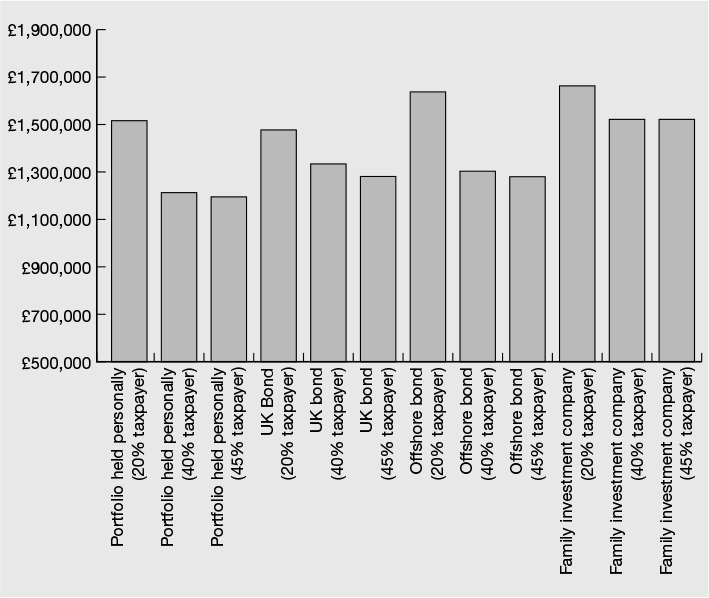

Figure 16.1 shows the optimum value of a taxable investment portfolio, based on three investor tax profiles, depending on how the returns arise.

Figure 16.1 Optimum value of taxable investment portfolio

Investment bonds

We looked at investment bonds in detail in Chapter 15.

Family investment company

Dividend income arising from the company’s investment portfolio would be exempt from further tax, as the withholding tax attaching to dividends is deemed to have settled the corporation tax liability. Interest income would be subject to the main corporation tax rate of 20% (21% until April 2015).

For CGT purposes, the acquisition cost of the company’s holdings would benefit from indexation allowance, which removes any inflationary gains arising. Any indexed gains realised within the portfolio would be subject to corporation tax of 20% (21% until April 2015). Care is required where the company holds large amounts of cash and fixed interest investments, as special rules called ‘loan relationship’ might cause unnecessary additional annual tax charges.

Although CGT, currently up to 28%, would be charged on the ultimate disposal of the FIC shares, this may not be for many years, if ever. If the shares in the FIC are held at death, then no CGT will be payable by the estate. In the meantime, the FIC would enable the family to accumulate wealth net of relatively low tax rates, compared with up to 27.5% on dividend income and 28% on unindexed gains arising if held personally (indexation allowance was abolished many years ago for personally owned investments).

Side by side

The balance between capital gains and reinvested income can have a big effect on the relative merits of the available investment tax wrappers, as well as the investor’s rate of tax paid on encashment of the portfolio (if that ever happens in practice). In addition, the charges associated with setting up and maintaining the tax wrapper can have a significant impact.

Figure 16.3 Projected portfolio values – 100% fixed interest

Asset class returns are based on those set out in Figure 3.3 of chapter 3.

Figures 16.3 to 16.5 show different investment strategies held via the main tax wrappers. The projected terminal values net of tax vary considerably. A point to bear in mind is the probability of actually paying the tax shown in the examples. A transfer of directly held funds by way of gift to a third party other than a spouse or civil partner will give rise to CGT unless it is to trustees and an election is made to ‘hold over’ the gain to the trustees. However, it may be possible to gift some shares with different rights, before any gains have accrued.

Figure 16.4 Projected portfolio values – 50% fixed interest, 50% equity

Asset class returns are based on those set out in Figure 3.3 of chapter 3.

An investment bond, in contrast, may be assigned to a third party as a gift and there is no immediate tax charge on any latent gain. The gain is also gifted to the recipient and subject to their own tax position on eventual encashment. It may be that you are a higher-rate taxpayer during some or all of the holding period of the portfolio but become a basic-rate taxpayer prior to encashment. This is where careful management of your taxable income, such as controlling how much income you withdraw from your pension fund, can have a big impact. If you or a person who receives assignment of some or all of the bond as a gift crystallises the gain when they are non-UK resident, they may avoid UK income tax completely.

Figure 16.5 Projected portfolio values – 100% equities

Asset class returns are based on those set out in Figure 3.3 of chapter 3.

A family investment company funded substantially by way of a loan could provide tax-free cash to the original investor through loan repayments, rather than being subject to higher-rate tax as would be the case had dividends been taken. An investment bond can provide tax-deferred withdrawals of 5% p.a. of the original investment.

No silver bullet

Given the many variables to take into account and the inherent uncertainties with regard to the future (e.g. in respect of actual performance, individual investor tax rates and what the tax system will look like), you need to bear in mind that there is an element of risk in choosing how best to hold investments from a tax perspective, given that the assumptions used are highly likely to turn out to be wrong. Asset allocation is the way investors minimise investment risk (for what will always be an uncertain future) by diversifying across different asset classes. This principle of ‘spreading’ or ‘allocation’ can also be applied in connection with tax wrapper selection where there is some uncertainty as to the future. Where this uncertainty could make a decision made on an ‘all or nothing’ basis the wrong one, it may make sense to diminish this risk by spreading investments across appropriate investment wrappers.

In addition to pensions and ISAs, it may be most appropriate to ensure that low-yield investments are held directly and high-yield funds held within investment bonds. For portfolios that include a mix of equity and fixed interest holdings it will be important to strike a balance and so across a whole portfolio one could see (subject to control of charges and unnecessary complexity) a range of wrappers being selected. It is also worth bearing in mind the need to rebalance the portfolio in the future. This would entail moving capital between different asset classes in order to maintain the required risk exposure, which can be compromised if each asset class is held within a different wrapper type. Choosing the right tax wrapper(s) needs careful analysis of the facts and your likely future circumstances.

1 You must be UK resident at the time that you invest capital into an ISA, but you are permitted to retain the account and its UK-tax-exempt status if you become non-UK resident. The ISA may be taxable in your new country of residence.

2 Dividends come with a non-reclaimable tax credit equal to 1/9th of the net dividend paid. So a £9 dividend would come with a £1 notional tax credit, making the gross dividend £10. The non-taxpayer cannot reclaim the notional tax credit, whereas it settles the liability of the basic-rate taxpayer. The higher-rate and additional-rate taxpayer, meanwhile, is required to pay 22.5/27.5% respectively of the grossed-up dividend not represented by the notional tax credit. This is equivalent to 25/30.55% respectively of the net dividend paid.