SINGLE-PREMIUM INVESTMENT BONDS

‘Non-qualifying life insurance policies can also have tax advantages.’

Money Advice Service1

Investment bonds are single-premium life insurance policies issued by either a UK (onshore) or overseas (offshore) life assurance company. While the policy usually pays a slightly higher amount than the policy value on the death of the bond life assured, this is usually very small (typically 1% of the value).

Capital gains arising within an onshore bond will be subject to the life company’s tax rate (currently 20%) after allowing for indexation relief and expenses. Gains arising within an offshore bond will be exempt from tax. UK dividends received inside a UK life fund bear no further tax and the investor has no tax liability on reinvested dividends either. Under an offshore bond the dividends will be received and no further tax will be payable, but there will be no reclamation of the tax credit either.

Foreign dividends will be subject to tax inside a UK life fund but typically not inside an offshore bond. In practice, however, the average yield on foreign equities and funds tends to be comparatively low and in any event, there are often non-reclaimable withholding taxes applied before receipt. The terms of any relevant double tax treaty may be helpful where the withholding tax is reclaimable.

Interest received by a UK life fund will be taxed at 20% – the life company tax rate. Interest received inside an offshore bond will not be subject to tax and the benefits of almost gross roll-up will be most keenly seen in connection with interest-bearing assets.

Unlike collective funds, on which the investor suffers income tax on dividends and interest on an arising basis and capital gains tax on eventual encashment, the tax treatment of an investment bond means that the investor potentially pays income tax upon encashment, on any gain, whether arising from accumulated interest, dividends or capital gains. This gives the investor a fair degree of flexibility over the timing of such liability, although with the disadvantage, for higher and additional-rate taxpayers, that the income tax rate payable may be higher than the highest capital gains tax rate of 28% at the time of writing.

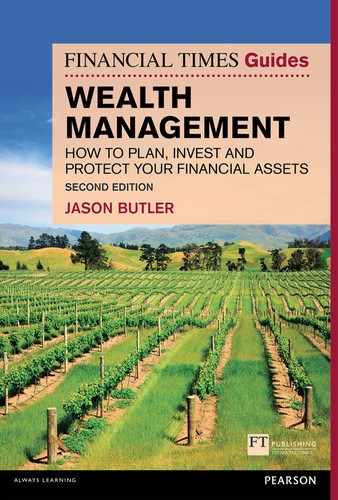

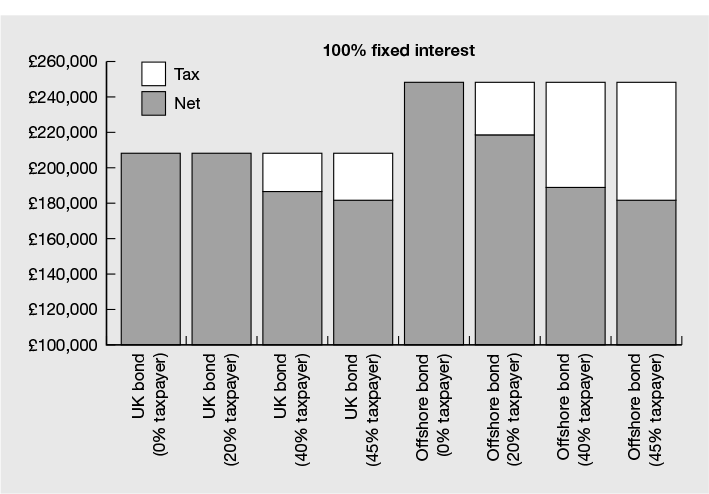

With an onshore bond, because the taxable return is assumed already to have borne basic rate tax at 20%, there is no further tax liability upon encashment for nil and basic-rate taxpayers. The whole net gain arising on encashment is added to the investor’s other taxable income arising in the same tax year and subject to a further 20% income tax for a higher rate and 25% for an additional-rate taxpayer. With an offshore bond the gross gain will be taxed at nil, 20%, 40% or 45% for nil, basic, higher and additional-rate taxpayers respectively. Figures 15.1, 15.2 and 15.3 show the projected values of a UK and offshore bond both before and after encashment for different taxpayers.

Figure 15.1 Projected values of onshore and offshore investment bonds – 100% fixed interest

Figure 15.2 Projected values of onshore and offshore investment bonds – 50% fixed interest/50% global equities

Figure 15.3 Projected values of onshore and offshore investment bonds – 100% global equities

If, however, the investor is a basic-rate taxpayer before the bond gain is added to their other taxable income, but becomes a higher/additional-rate taxpayer once the gain is added, the gain will be subject to what is known as ‘top slicing’ relief (see Figure 15.4). This means that the total gain arising on encashment is divided by the number of policy years to determine the ‘sliced’ gain.

The sliced gain is then added to the investor’s other taxable income to determine whether it still exceeds the higher-rate income tax threshold. To the extent that each slice does exceed the higher-rate tax threshold, an onshore bond will be taxed at 20/25% on the net gain for each ‘slice’ above the threshold. An offshore bond will be taxed at nil/20% on the amount of each slice that falls below the personal allowance/threshold for higher-rate tax and 40/45% to the extent that it exceeds it.

Figure 15.4 Top slicing relief

Example

Trevor originally invested £100,000 in a UK investment bond, which he has held for exactly 12 years. The value of the bond is currently £150,000 and Trevor has made no previous withdrawals. Trevor has £5,000 of his basic-rate income tax band available, due to taxable income from his employment and savings. He decides to encash the bond and as a result crystallises the £50,000 gain.

Because the gain exceeds the higher-rate income tax threshold, the £50,000 gain is divided by the 12 years that Trevor has owned the bond, to create a ‘top slice’ of £4,166.67 (£50,000/12). Because the sliced gain falls entirely within Trevor’s unused basic-rate income tax band, no further income tax is payable.

Tax deferral

Personal income tax is payable only on investment returns arising within an investment bond when what is known as a ‘chargeable event’ occurs, which is:

- full encashment

- the death of all lives assured on the bond

- partial encashment that exceeds 5% p.a. of the original investment (the allowance is cumulative)

- assignment for money or money’s worth.

When the bond is eventually encashed, any previous withdrawals that have not been taxed will be added back to work out the amount of taxable gain. However, this is where another feature, called assignment, becomes useful (see Figure 15.5).

Figure 15.5 Deferring or avoiding tax on gains via assignment.

Source: Bloomsbury Wealth Management.

A transfer of shares or collective funds, by way of gift to a third party other than a spouse or civil partner, will give rise to capital gains tax unless it is to trustees and an election is made to ‘hold over’ the gain to the trustees. All or some of the segments of a bond, in contrast, may be assigned to a third party as a gift and there is no immediate tax charge on any gain. The gain is also gifted to the recipient and becomes subject to their own tax position.

In effect, the new owner takes on the base cost of the bond and any subsequent tax liability is assessed against them, not the original owner, when a future chargeable event occurs. The new bond owner could also, at some stage in the future, assign the bond to another person or to trustees and obtain further deferral of income tax.

Assignment makes a lot of sense if the new owner is someone who would be able to crystallise the gain within their personal allowance. In addition, from the 2015–2016 tax year, the first £5,000 of savings income is tax free where the individual has other non-savings income below the personal allowance. This means that potentially up to £15,500 of bond gains could be crystallised each tax year by someone to whom an investment bond had been assigned, perhaps while they are at university.

Assignment also works well if the person to whom the bond is being assigned qualifies as a non-UK resident in the tax year of encashment and their country of residence does not seek to tax (or taxes at a lower rate than the UK) the eventual gain arising. The new Statutory Residence Test makes it harder for a long-term UK resident to lose their UK tax status. It takes five full tax years of non-residence for a previously UK-resident individual2 to avoid income tax on gains arising from a chargeable event on an offshore investment bond acquired while a UK resident. If you realise gains (or cause any chargeable event) by encashing an investment bond while non-UK resident, but subsequently become UK resident within five years of leaving the UK, any realised gains will be retrospectively subject to UK income tax. Chapter 14 has a simplified flowchart to help you determine whether you are UK resident or not, but bear in mind that the rules are complex and you should take advice on your individual circumstances.

A warning on adviser charges

Since 6 April 2013, if you pay financial advice fees by way of a deduction from your bond, this sum counts as a withdrawal for the purposes of the 5% p.a. tax-deferred allowance. Thus, an adviser charge of, say, 1% p.a. of the fund value will mean that your tax-deferred withdrawal allowance will be progressively reduced each year. This is because your withdrawal allowance is based on the original investment, whereas typically the adviser charge is based on the (hopefully increasing) fund value. Discretionary investment manager fees are treated as an expense of the bond provider and as such are not treated as a withdrawal for the purposes of determining your 5% annual tax-deferred withdrawal allowance.

Practical application

Instead of holding an investment portfolio in your own name, you could hold it via an investment bond. As well as minimal or no tax arising within the bond, this leaves your personal income tax allowance, basic-rate band and capital gains tax exemption available to minimise taxation on other assets you may own. In the meantime you may withdraw the investment returns arising (up to 5% p.a. of the amount invested) without immediate tax. This could mean a substantial uplift in yearly cashflow and/or a lowering of tax on personally held assets.

Dividend income

The main problem with dividends, whether via direct holdings or from an investment fund, is the significant tax liability that higher-rate and additional-rate taxpayers incur, even if they accumulate the income. A 40% taxpayer will pay 25% and an additional-rate taxpayer will pay 30.55% on the net dividend received. This is where using a UK single-premium investment bond might be useful, as part of a balanced portfolio tax-planning strategy. Investment bonds come in two forms: self-select and restricted. The self-select version allows you, or the investment manager you appoint, to choose from a very wide range the investment funds or securities that you wish to use.

Dividend income received within a UK insurance company bond does not suffer corporation tax, having received an internal tax credit of 10% on the dividend. Therefore the compounded returns, particularly over very long time periods, will be greater than if a higher or additional-rate taxpayer received the dividends personally. The accumulated dividend income will eventually be taxed on the policyholder if they are a higher or additional-rate taxpayer on encashment but at a lower rate than you might think.

Consider Peter, a higher-rate taxpayer, who invests £1 million in a portfolio of equities that produces a high dividend yield of 4.5% net. As a higher-rate taxpayer he will pay the following income tax on these dividends:

This compares with no tax on the net dividends received inside the wrapper of the bond.

Disregarding the benefits of compounding returns subject to lower tax within the bond, let’s assume that Peter encashes the bond after one year’s ownership. Although this isn’t likely, it allows us to make a clear comparison with the taxation position if held personally. Peter will pay income tax on the accumulated gain at 25% as follows:

| Chargeable event gain | = | £45,000 | |

| Additional-rate income tax @ 25% | = | (£11,250) | |

| Net gain in Peter’s hands | = | £33,750 | |

| Increase in return to Peter | = | £ 2,500 | (+8%) |

Peter retains 8% more of the dividend via the bond because the gain on the bond is not grossed up as it is with the direct receipt of a dividend and he is given credit for the bond having paid basic-rate tax already, when in fact the dividend tax credit was only 10%. In addition, the higher net dividends retained within the bond will compound each year to increase the terminal value of the portfolio still further.

Additional tax benefits of a single-premium bond include:

- facility to withdraw up to 5% p.a. (cumulative) of the original investment, tax-deferred

- may allow other taxable income to be brought below the £150,000 additional-rate threshold

- may allow personal allowance to be partially or fully reinstated if taxable income is below £120,000

- may bring adjusted net income below £60,000 and so reduce or avoid the child benefit tax charge

- one or more segments could be assigned to a basic-rate taxpayer before encashment, to avoid additional income tax arising on the gain

- if encashment arises when the policyholder qualifies as non-UK resident, no UK income tax liability will arise

- potential to reduce tax on encashment if the policyholder, before encashment, has any unused basic-rate income tax band.

A UK insurance bond can be cost-effective at any level from £100,000 upwards, but clearly the larger the investment and resulting yield, the bigger the benefits. Although the use of an investment bond is not a panacea to the problems of high taxation, as part of a balanced tax wrapper allocation strategy, and subject to the impact of charges, it could offer valuable benefits.

Using with trusts

Because investment bonds are deemed, for tax purposes, to be non-income producing and it is possible to choose when gains are taxed, they are particularly useful for trustees of discretionary trusts to use to hold investment capital on which they would otherwise pay income and capital gains tax at the higher rate. For example, you could set up a trust (under which the settlor is excluded from benefit) and then loan your capital to the trustees so that they can invest in an investment bond. The trustees could then repay you over a period of time using the 5% tax-deferred withdrawal facility to avoid an immediate income tax charge. See Figure 15.6.

Figure 15.6 Gift and loan arrangement with an investment bond

Source: Bloomsbury Wealth Management.

Bespoke investments

Some offshore bonds provide the option of what is known as an ‘internal linked fund’ (ILF) (see Figure 15.7). An ILF can often be considered as an alternative to, or in addition to, a personalised open-ended investment company. An ILF must fulfil certain statutory criteria, which include the requirement that the fund be available to investors at large or to a class of investors, membership of which is determined by the insurer. If the option to invest in the fund is available to a class, that option must also appear in the insurer’s marketing material.

ILFs can provide access to a variety of assets that could otherwise render an investment bond as ‘highly personalised’ for income tax purposes. Highly personalised bonds suffer an annual income tax charge of 15% of the bond’s value, regardless of returns, so you need to avoid this treatment at all costs. Alternative assets such as hedge funds, shares, gilts and derivatives can be included in an ILF’s investment portfolio without triggering the personalised bond tax charge.

Each ILF must be managed by a discretionary investment manager, appointed by the insurer, although the policyholder can pick their preferred manager. The insurer monitors future performance against the agreed strategy, benchmark and objectives.

Figure 15.7 Internal linked fund option

Source: Bloomsbury Wealth Management.

Offshore bonds sold outside the UK

Many high-earning UK expatriates buy non-UK investment bonds that would be classed as highly personalised in the UK. While the investor remains non-UK tax resident, this is not a problem. However, to avoid the 15% annual tax charge arising on the bond when the investor becomes UK-tax resident, either the policy needs to be endorsed to restrict the offending investment options so that it would not be classed as highly personalised, or the bond will need to be encashed before the investor returns to the UK.

Discounted value arrangement

Bonds can also be set up with special conditions that have the effect of immediately reducing the value of the bond for IHT by up to 60%, but that permit the investor to retain access to as much as 10% p.a. of the original investment. See Chapter 22 on non-trust structures for estate planning application.

Accumulation and maintenance (A&M) plan

Another type of offshore bond has special policy conditions that restrict the right to encash to a date or dates in the future and then gift this to younger generations. This allows you to make a potentially exempt transfer for IHT purposes, while restricting when the new owners can access the funds and avoiding the hassle and tax complication of a trust.

You would invest into a specially modified offshore insurance bond, with a wide choice of investments, which you then assign as an outright gift to your chosen beneficiary or beneficiaries. The policy conditions are such that the surrender value of the bond is suppressed until a future date stipulated by you at the outset, to coincide with the age that you feel comfortable with the beneficiary or beneficiaries having access to the bond. This solution is ideal where you wish to make an outright gift now but want to avoid the recipient gaining access at a young age and either do not want, or are unable, to gift to a discretionary trust (because you have already made a gift to trust to the nil-rate band within the past seven years). See Chapter 22 for a more detailed explanation of this structure.

Private placement life assurance

Another version of investment bond is called private placement life assurance (PPLA). This allows the policyholder to obtain life cover, either on top of (additional cover) or instead of (integrated cover) the bond’s surrender value. The cost of the life insurance is deducted from the bond but does not count towards the 5% tax-deferred withdrawal allowance and enables this to be funded from tax-free returns. Table 15.1 shows both types of cover for a £2 million PPLA bond.

Table 15.1 Private placement life assurance bond

| Premium | Integrated cover | Additional cover |

| Life cover | £10m | £10m + surrender value |

| Projected encashment value – 20 yrs @ 5% pa growth | £2.5m | £2.2m |

Source: Bloomsbury Wealth Management.

It is possible to arrange the policy in trust. This is achieved via a loan of capital to trustees who then invest in the bond. The loaned amount will remain in the donor’s estate but the life cover will not.

Non-UK domiciled individuals

An investment bond that is funded by clean capital (i.e. that does not contain accrued income) allows a UK resident but non-UK domiciled individual to avoid having to pay the £30,000/£50,000 p.a. remittance basis charge, and as such benefit from use of their personal income tax allowance and capital gains tax exemption in respect of UK income and gains. This is because the bond is deemed to be non-income producing and as such not subject to UK income tax. Annual withdrawals of up to 5% of the original amount invested may also be remitted to the UK without tax charge.

Whether the current well-established tax treatment of investment bonds will continue is anyone’s guess, but, if it doesn’t, having all investment returns classed as income rather than capital gains might turn out to be rather expensive. For this reason, it probably makes sense to avoid holding your entire portfolio in an investment bond.

1 www.moneyadviceservice.org.uk/en/articles/tax-and-qualifying-life-insurance-products

2 For this purpose UK residence means having been UK resident in at least four of the last seven tax years.