THE ROLE OF GUIDANCE AND ADVICE

‘The investor’s chief problem, and even his worst enemy, is likely to be himself.’

Benjamin Graham, legendary US investor

You probably derive much of your financial knowledge from what you read, hear or see in newspapers, magazines, websites, television and books. The internet gives us fast access to vast amounts of material, whether that is video on demand, discussion forums, social networks or knowledge archives. However, just because there is a lot of information available out there does not mean that it is necessarily accurate, objective or relevant to your situation.

The media is not your friend

The sheer amount of information, vested interests and speed of news, coupled with the huge amount of competition, means that journalists are fighting a losing battle when trying to be helpful, objective and independent in what they communicate to their readers on personal finance issues. Sometimes stories are inspired by real news events and other times by ‘expert’ comment from companies with some form of vested interest. The problem is that in the face of such a continual barrage of often conflicting and sensationalist news and information, the average person finds it hard not to be seduced into taking actions that they may turn out to regret. Even if you’ve decided on your overall planning and investment approach, it is hard not to be knocked off track by the relentless media messages that bombard us on a daily basis.

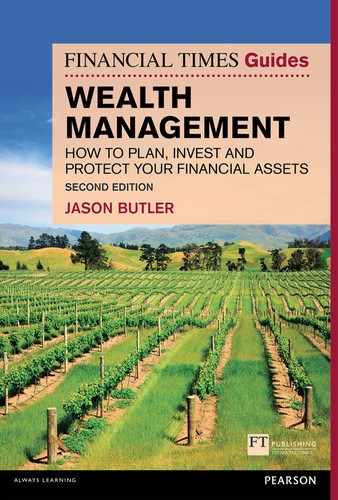

We often overreact to news and ignore the reality of long-term, steady norms. This is normal and totally expected. We place far too much weight on what happened yesterday rather than on what has happened over the past 50 years. The media focuses our attention on the daily movements in the capital value of the stock market. In a sense this fixation on capital values is the investment sizzle, when in fact the investment steak is compound returns. The magic of compounding works away in the background, with dividend/interest and capital gains generated by the portfolio reinvested to create more income and more capital gains. Compounding has been described as the eighth wonder of the world and it is rarely understood what a powerful impact it has on investment returns (see Figure 4.1).

Figure 4.1 The power of compounding

The financial services marketing machine

There is a massive marketing machine deployed by the financial services industry, sometimes subtly and sometimes less so, that is seeking your attention for financial products and services. Jack Bogle, the founder of index fund group Vanguard, estimated that in 2000 the amount spent on financial media advertising was at least $1 billion,1 so today it is likely to be much more than that.

Financial services companies make claims, promises and statements that often don’t bear up to scrutiny. The chief problem is that financial companies are seeking to sell their products regardless of whether they are suitable, competitive or value for money. In some cases these products offer a solution to problems that investors never knew they had. I’ll talk about the cost of investment funds in Chapters 10 and 11, but remember that the amount spent on marketing is often in direct inverse relationship to the value being provided. In other words, the more spent on marketing, the higher is likely to be the real cost of the product. Oddly enough, the most profitable products for the provider may not be the best value for money for the investor.

Fund managers have a lot of form when it comes to launching new funds on the back of strong optimism about an asset class, usually following a period of strong performance. For example, at the height of the technology boom in 2000 fund managers were falling over themselves to launch technology funds on the back of tremendous past performance. I remember very well in early 2000 a taxi driver telling me that he was making more money on his investments in technology funds than he was from driving his cab. When taxi drivers start offering investment advice, you really do need to start worrying.

Aberdeen Global Technology was one of the largest technology funds around at the time and it attracted a lot of new money from private investors keen to join the party. Unfortunately the next ten years were not very kind to those investors, with the fund producing –4.49% p.a. compared with the FTSE All-Share index return of 2.93% p.a.2 Although the fund return has since improved, it still managed only 7.67% p.a. compared with the FTSE All-Share Index return of 8.67% p.a.3

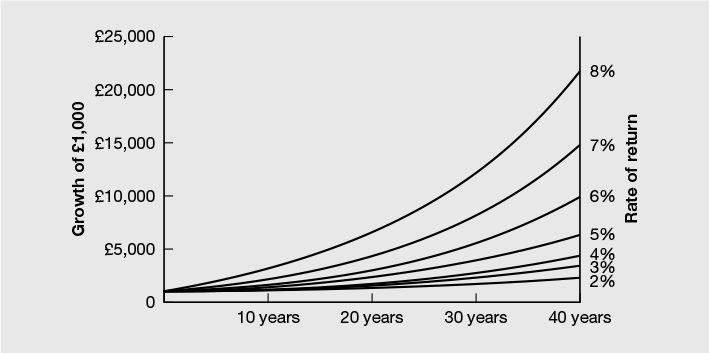

Another great example of active manager hype is that of Jayesh Manek, who was the winner of the Sunday Times Fantasy Fund Manager competition in 1994 and 1995, beating thousands of other entrants and winning £100,000 on each occasion. After initially managing £10 million for well-known investor Sir John Templeton, Manek established the Manek Growth Fund, a unit trust open to public investment. By 2000 he had attracted more than £100 million into the fund, which was up by 160% and worth nearly £300 million. After the tech wreck in 2000 the fund value crashed and since that time the performance of Manek Growth has been truly terrible, as shown in Figure 4.2.

Figure 4.2 Manek Growth – ten-year performance to 31 December 2013

Source: Data sourced from Morningstar, Office for National Statistics.

When it comes to promoting their funds, fund managers are usually highly selective about what they show. They typically show those funds that have outperformed the particular measure they select while saying nothing about their underperforming funds. Often they quote a very short-term track record (three years is common) of one of their ‘star’ managers or their five-year, top-quartile-performing flagship fund. The media also gets sucked into quoting this highly selective past performance data as part of a story or feature on investing trends, often based on press releases originated by smart people in public relations firms. I know from experience that many journalists want to write about ‘noise’ rather than the boring reality that investing and financial decision making should be dull to be successful. ‘Buy and hold’ doesn’t have the same ring about it as ‘The next big thing is …’.

Average investors and markets

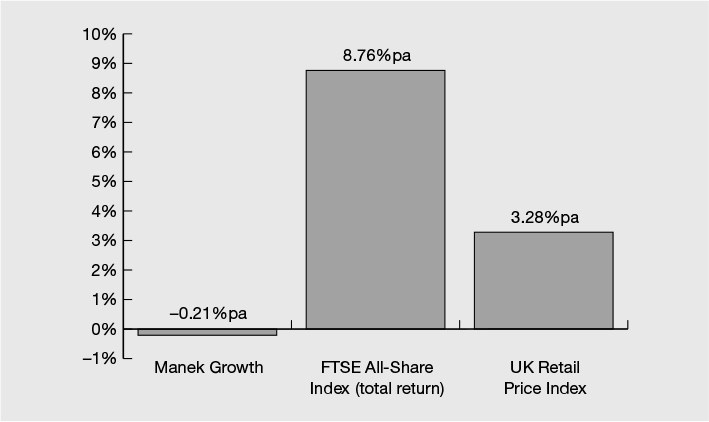

As I explained in Chapter 2, the academic research tells us that investors rarely obtain anything like the returns the funds in which they are invested achieve. This is because the average investor flits from fund to fund based on the prevailing messages they pick up from the media and the financial services industry – ‘this time it’s different’. There is a powerful and very natural human tendency to want to do something in the face of adversity or if others are apparently doing better (investment wise) than you. A long-running US-based study carries out an analysis each year into the impact of investor behaviour on the returns that they achieve.4 As you can see from Figure 4.3 the average investor doesn’t get much of the returns that are there for the taking if only they could stay the course.

Figure 4.3 Investor returns compared with fund returns

Source: Data from DALBAR (2014) Quantitative Analysis of Investor Behavior (QAIB).

Over the 20-year period to the end of 2013 it seems that the average US equity investor achieved a return of 4.2% p.a. less than the main US stock market index and the average US bond investor achieved a return of 5% p.a. less than the main US bond index. Although the average equity investor did beat inflation, the average bond investor actually lost money in relation to inflation. This is nothing to do with fund manager competence or costs but poor discipline on the part of investors.

‘Investors should remember that excitement and expenses are their enemies.’

Warren Buffett, Chairman, Berkshire Hathaway Corporation

Responding to changing economic conditions

In his lecture on what investors could learn from the stock market crash of 2008–2009, Charles Ellis put it like this:

‘People often like to say, well, there’s a great powerful experience in this terrible financial crisis, are there lessons to be learned? The answer of course is “yes”, but be careful you don’t learn too much because it’s a very unusual experience that we went through and most people will never go through anything like that again. So, you don’t want to be so well prepared to go through it again that you lose the chance to have positive experiences for the more normal part of life.

But, you really should pay attention to what was it about the experience of the crisis that really was shaking your confidence and might have caused you, or people like you, to do something that would have been horrible in the long run. Give you a good example: anybody who got so frightened last February or March [2009] that they cleared out their stock investments and put their money into either bonds or cash is someone who took a temporary loss and made a permanent loss. That’s a lesson we all want to learn: don’t allow current experience, no matter how acute, to be disruptive of your long-term planning.

The easiest example for all of us who’ve had teenage children is be very careful that the worst moment of experience with a teenage child does not dominate your behaviour towards that child. Be steady, be calm and in the long run your child will grow up to be a wonderful adult, just like you.’5

Media noise is just that, noise. Don’t confuse the needs of media to sell copy and advertising with what is in your best interests. You wouldn’t measure the distance between your home and place of work with a small ruler, so avoid reacting to short-term, random news. The best antidote to being blown off course might be to work with a decent adviser to develop and stick with a structured financial plan that enables you to make decisions in context with your values and key life goals.

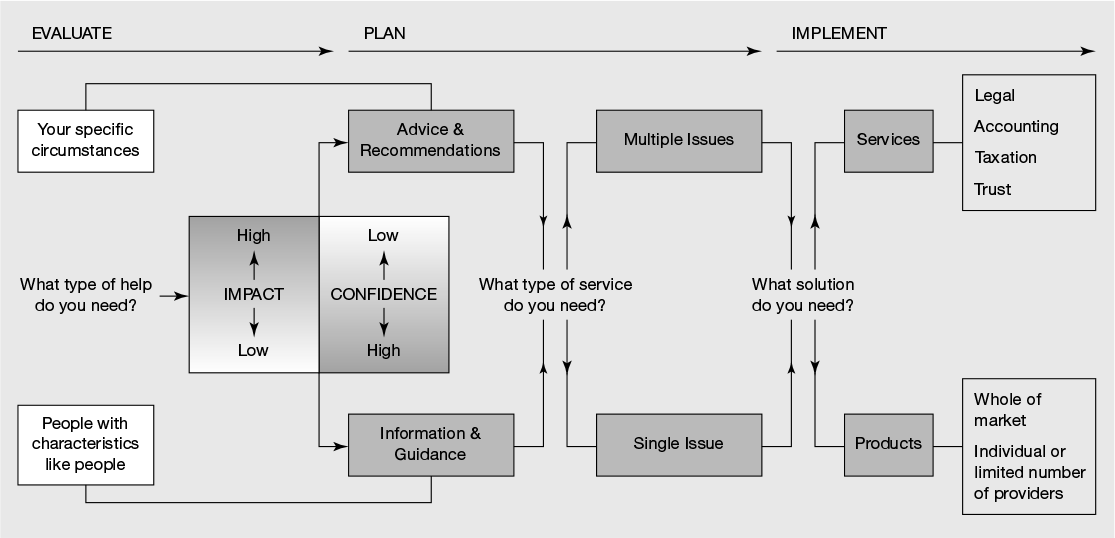

Decide what help you need and would derive value from

There are several factors to consider when working out whether you need assistance with planning, implementing and managing your personal wealth. In no particular order these include:

- your financial personality (propensity, inclination, time, behaviour)

- your confidence in making financial decisions

- the financial impact on your desired lifestyle and other life goals

- the time you have available

- the complexity of your financial and family situation.

Advice

Providing financial advice on investments, pensions, certain insurance contracts and mortgages is highly regulated in the UK and most private individuals are classed as ‘retail’ investors. This means that any firm that provides advice has to follow strict rules in relation to suitability, appropriateness and fair dealing. Because some areas of advice relate to complex and difficult financial issues which can have a big impact on people’s lives, there are various protections in place, including professional indemnity insurance (held by the advice firm), a financial ombudsman service (to adjudicate on complaints) and a compensation scheme funded by a levy of the financial services sector. It is a criminal offence for anyone to offer regulated financial advice without being authorised and regulated to do so.

Financial advice is based on a thorough assessment of your personal situation and is tailored to meet your specific needs. This results in written recommendations which should enable you to achieve your objectives. Such advice can be focused on one specific area, such as protecting your family against your death, but the advice firm is still responsible for pointing out if they think other matters need to be considered. You are perfectly in your rights to reject any suggestions to widen the scope of advice. Alternatively, firms will offer a general advice service which covers your entire situation, whether or not this relates to your specific objectives, and this is often referred to as full-service, comprehensive or holistic advice.

Passporting firms

Some European financial advice firms are regulated and established in one country but provide regulated services to residents in another, under a system known as ‘passporting’. This means that the firm is approved and regulated by the host country’s regulator and is permitted to operate, for example, in the UK as long as they agree to follow the UK’s rules.

My understanding, from speaking to compliance experts, is that no other European financial services regulator is as strict and tough as the UK’s Financial Conduct Authority. There is some evidence of previously UK-regulated advisers moving their business and regulatory authorisation to another European county with a more ‘relaxed’ regulatory approach and then passporting their services back to the UK. Apart from the obvious potential for regulatory arbitrage to arise (where firms seek the easiest regulatory regime), trying to get redress if things go wrong might turn out to be less than easy, particularly if you don’t speak the language. You have been warned!

Guidance

Guidance is where a financial services company provides you with information to enable you to make your own decision, including arranging any financial products. The information is usually based on people like you, but is not specific to your situation. Although there is still protection in relation to financial products being fit for purpose, this does not extend to the suitability of such products for you, so if you have a bad outcome, you will have no protection or redress available to you. Over the past ten years or so, with the proliferation of online DIY investment platforms, new providers of low-cost investment and pension products, and consumer finance websites, some people have confused guidance with advice. For example, an online portfolio service that provides information on investment matters, including which portfolios might be suitable, appears as if it is providing specific and tailored advice.

What help do you need?

If you have relatively simple needs, modest wealth/income, high confidence, the outcome would have a low impact on your wealth and/or have a high interest level and time available, then guidance may well be the best solution for you.

If, however, your needs are complex, you have low confidence, the outcome would have a high impact on your wealth and/or you have little time or interest in personal finances, then you’ll probably need advice that is tailored to your situation.

Frequency of advice

Assuming that advice is the service you need, you also need to decide whether you need an ongoing advice service or not, and if so, the frequency of that service, i.e. yearly, three yearly or a longer interval. If you wish to focus on one particular issue, for example reviewing your pension arrangements, protecting your family in the event of your death, or setting up a tax-favoured investment such as an Enterprise Investment Scheme, you might need one-off advice rather than an ongoing service. However, with more complicated circumstances and substantial wealth, where the financial impact is high (for example, where portfolio and/or pension regular withdrawals need ongoing monitoring), you will probably need and want a more comprehensive and ongoing advice service. Figure 4.4 sets out these choices graphically.

My view is that there are a substantial number of people who are being over-served and overcharged by financial services firms because the firm is providing an ongoing annual service which is not necessary for the person’s situation or not good value for money in relation to the financial outcomes achieved. This has become more apparent since the introduction of the ban on product-based commission incentives to UK advisers in January 2013. These new rules have seen many financial services firms trying to replace commission payments from products with ‘adviser remuneration’ facilitated by deductions from financial products, in return for an ongoing advice ‘service’. I have spoken to many individuals over the past few years who are questioning the value of this ongoing ‘service’ and the amount of fee charged. Sending out periodic valuations and having a one-hour annual meeting is not an advice service, and unless value is being delivered in excess of the advice costs, it doesn’t make sense to use such firms.

Financial advice or financial planning?

The term ‘advice’ has a specific regulatory meaning in the UK. Over the past 25 years or so the regulatory regime has defined advice in relation to the arranging of financial products but not the actual advice process itself. This is starting to change, but most regulations and rules are still couched in terms of someone needing a financial product. As a consequence there are some areas of advice that are not regulated and/or not subject to the commission ban, such as financial planning, tax planning, trusts, wills and certain life and disability products which do not acquire a surrender value.

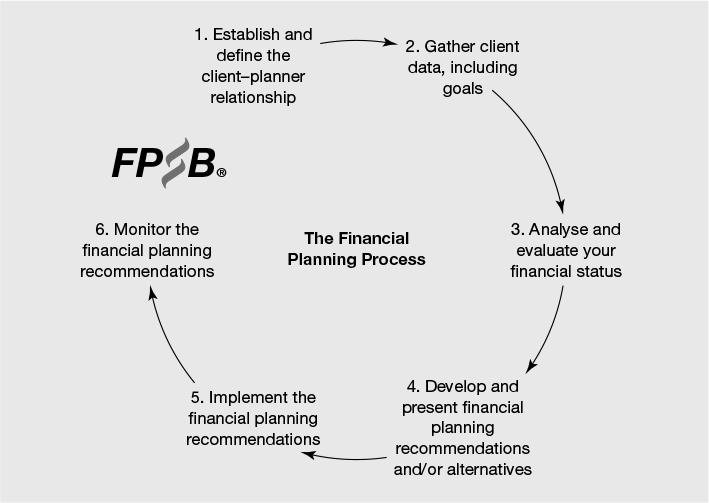

About 40 years ago financial advisers in the United States developed a six-step process for personal financial planning, which provided a comprehensive, structured and consistent framework that professionals could use with their clients to help them achieve their life objectives (see Figure 4.5).

Experience and professional qualifications

Since January 2013 all individuals who provide UK-regulated investment and financial advice to individuals must have attained a level of professional qualification equivalent to that of the first year of a degree course. In reality, a number of areas of advice, such as pension transfers, have always required higher levels of qualification, but the new standard will apply across the board to insurance salespeople, bank advisers, financial advisers, stockbrokers and private bankers.

Figure 4.5 The six-step financial planning process

Source: Financial Planning Standards Board ltd. Copyright © 2014, Financial Planning Standards Board Ltd. All rights reserved.

Table 4.1 illustrates the levels of different types of designations and where they sit on the educational ladder, to give you an idea of the quality and difficulty required in attaining different levels of qualification. The Certified Financial Planner (CFP) accreditation is awarded to individuals who pass a rigorous financial planning case study assessment, in addition to possessing the necessary technical examination standards required by the regulator. This ability to apply technical knowledge to a given client situation makes the CFP a good standard by which to determine whether a professional adviser has the relevant skills and knowledge to provide high-quality advice. Today there are over 153,000 practitioners around the world who hold the CFP accreditation.6

In 2011, the Institute of Financial Planning (IFP), which administers the CFP accreditation in the UK, launched an Accredited Financial Planning Firm™ designation and register. To be awarded Accredited status firms have to:

Table 4.1 Summary of financial services qualifications

| Academic | Level | Vocational |

| PhD/CFA | 7 | Diploma in Wealth Management (CISI) Diploma for Chartered Banker (CCN) Chartered Financial Analyst (CFA Institute) |

| MSc/MA/MBA | 6 | Chartered Financial Planner (CII) Advanced Diploma in Financial Planning (CII) Chartered Wealth Manager (CISI) Certified Financial Planner (IFP) |

| BSc/BA | 5 | |

| 1st year foundation degree | 4 | Diploma in Accounting & Business (ACCA) Diploma in Accounting (AAT) Diploma in Regulated Financial Planning (CII) Diploma in Investment Advice (CISI) Investment Management Certificate (new, CFA Institute) Certificate in Paraplanning (IFP) |

| International Baccalaureate | 3–4 | Certificate in Investment Management |

| A Level/City & Guilds | 3 | Certificate for Finanical Advisers (IFS) Certificate in Financial Planning (CII) Diploma in Financial Services (Chartered Banker) (CCN) |

| AS Level | 2–3 | NVQ in Retail Financial Services |

| GCSE | 1–2 | Foundation Certificate in Personal Finance Award in Personal Financial Planning |

- meet the IFP’s strict criteria for the delivery of a comprehensive financial planning service

- have easy-to-understand propositions, transparent charges and a clear investment philosophy

- have demonstrated their commitment to a professional code of ethics and practice standards

- ensure that their financial planning service is delivered by highly qualified practitioners

- have the ability to help you develop an effective plan to achieve your goals in life.

The Institute assesses all firms on an annual basis to ensure that they continue to meet the highest standards of professional practice. Accredited firms can be found in most regions of the UK, and I strongly recommend that you include at least one Accredited Financial Planning Firm on your advice firm shortlist.

Wealth management

The term ‘wealth management’ has become more prevalent over the past 15 years, but not all firms that profess to provide it offer the same service. A lot of stockbrokers and investment managers call themselves wealth managers when they focus only on the investment assets and have limited understanding of tax and legal issues and no concept of financial planning. Some restricted financial advisers, with limited investment or tax knowledge, focus more on advising and arranging tax wrappers such as self-invested personal pensions (SIPPs) and insurance bonds. Some financial planners focus purely on the overall plan and do not provide investment services. A comprehensive wealth management service should comprise the various different disciplines and areas that go to make up a proper wealth plan.

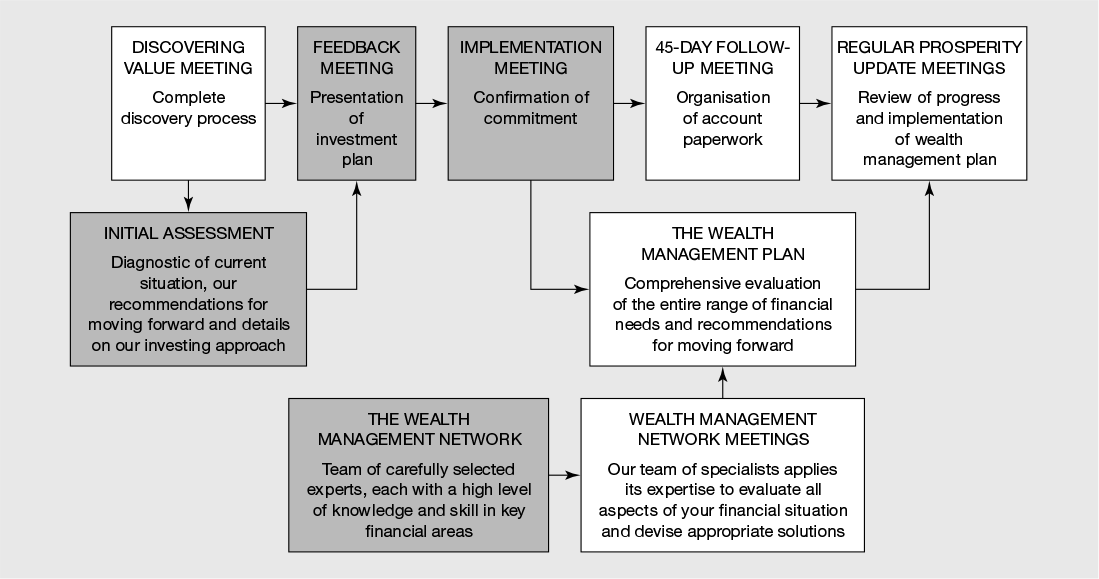

A typical comprehensive wealth management consulting process is illustrated in Figure 4.6. While every firm will have its own approach and processes, this will give you an idea of the type of approach to look for. A firm that cannot explain its process is unlikely to deliver a slick and professional service.

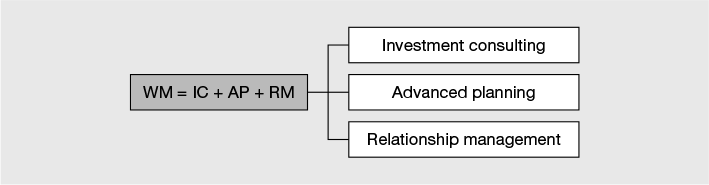

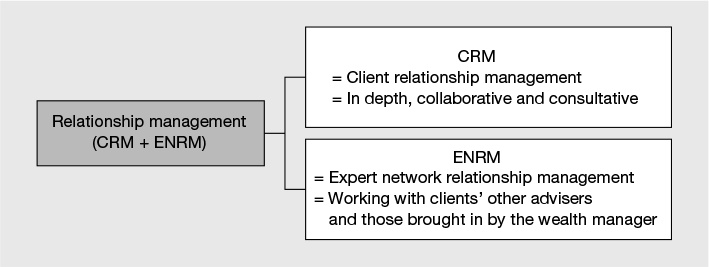

As illustrated in Figure 4.7, this service should comprise three key elements: investment consulting, advanced planning and relationship management.

Investment consulting is the process of devising, maintaining and periodically updating an appropriate investment strategy or strategies that reflect your risk profile and other preferences, based on what empirical evidence suggests is the most effective approach.

Figure 4.7 Key elements of a comprehensive wealth management service

Source: CEG Worldwide.

Relationship management (see Figure 4.8) is the ongoing process of ensuring that all advice is complementary and appropriate and action in one area of your wealth planning does not impact negatively on another. If you have existing advisers, for example a tax adviser, then your wealth manager must have both a process and the inclination to engage those other advisers in the wealth management process.

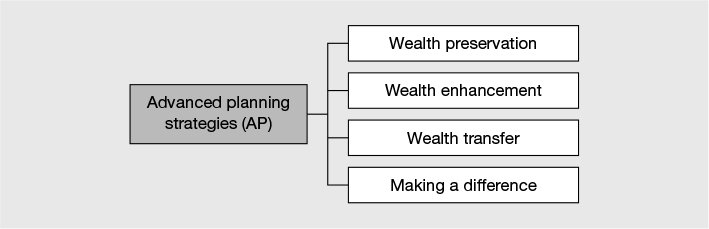

The advanced planning component comprises four strategic areas of wealth enhancement, transfer and protection as well as charitable planning (see Figure 4.9). Each of these strategies usually involves several tactics that enable sophisticated wealth planning to be carried out and will usually be set out in a wealth management plan.

Figure 4.9 Key elements of a wealth management plan

Source: CEG Worldwide.

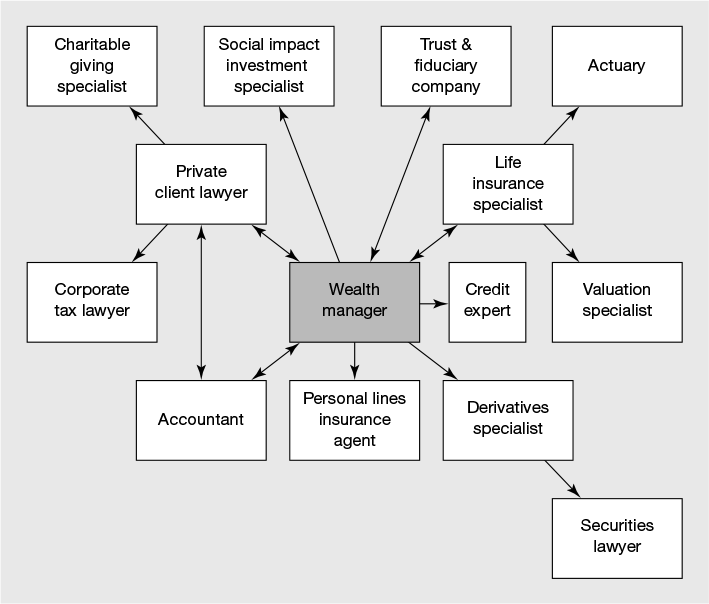

The expert network

A good wealth manager will have knowledge of you and your family and a broad understanding of strategies and tactics that you may need to adopt to achieve your goals. However, due to the sheer complexity of the financial and tax environment in which we live, it is unlikely that any wealth manager can be expert in all areas. Sometimes larger firms have different departments and seek to offer a ‘one-stop shop’, while others have a panel of outside experts in different disciplines on which they can call to provide focused advice and service as necessary (see Figure 4.10).

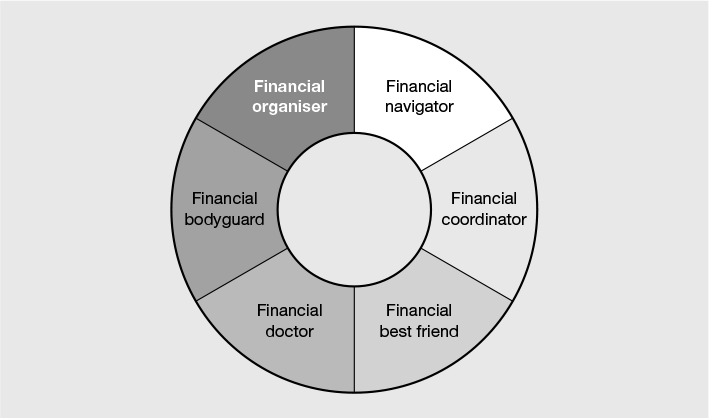

Many years ago I saw a presentation in the United States that explained the key roles a good financial adviser performs as part of a long-term professional client relationship and these are shown in Figure 4.11.

The financial navigator

As we saw in Chapter 1, knowing what’s important to you, where you are going and why are the keys to successful planning. A good adviser will make sure that you are clear about your goals and that such goals are true to your values. They will also help you to resolve any mismatches between what you want to achieve and what is possible, as well as determining alternative strategies and associated tactics.

The financial coordinator

A good wealth plan for most people will include a number of different elements, such as investment, tax, legal aspects and insurance. Particularly if you have more complex needs and larger amounts of wealth, you will need to use the services of a number of professionals, each with specialist knowledge and skills in different disciplines. The danger is that the overall advice can be fragmented, more expensive than it need be and quite often not as effective as it could be.

A good wealth manager will help to coordinate the advice of these professionals to ensure that the constituent parts ‘fit’ together to form a bespoke and comprehensive solution. Often there needs to be a series of discussions and communication between, say, a trust specialist, a lawyer and a tax adviser, to ensure that any solutions ‘fit’ together. The wealth manager will understand the context of the family’s overall financial position and objectives and ask the necessary questions so that, when a solution or shortlist of solutions is presented to you, all the technical analysis and evaluation has been completed.

The financial best friend

The best financial advisers and wealth managers are people who are also there for you in difficult times to provide moral support and can help you deal with opportunities, threats and life events. Sometimes you might want a sounding board, even if you think you know the answer to the question, to give you more confidence that you are making a good decision.

The following are typical of the range of issues that clients have shared with me over the years:

- whether to accept the remuneration package in a new job

- how to deal with aged parents’ care needs

- whether to buy a new home

- how to teach children the value of money

- whether to make a gift of capital or to lend it

- whether to invest in a friend’s or relative’s business venture

- whether to retrain for a completely different career

- how best to determine a fair value for selling the family home to a close friend.

More often than not I didn’t offer a solution as the clients came up with the answers themselves, but they found it helpful to share the issues with someone outside the family whom they trusted. As they say, a problem shared is a problem halved. A good adviser will also play devil’s advocate when you have suggested a goal, value, preference or tactic, to ensure that you’ve really thought things through. They will also hold you to account in relation to the financial planning policies that you have created in your plan.

The financial doctor

Just like the medical doctor who knows your family well and can be trusted to keep confidences, a good adviser develops a deep understanding of you and your family over many years. Sometimes relationships are not always what they seem and it can take time to uncover subtle but important information. For example, some adult children might be reckless spendthrifts with a trail of broken relationships, while others might be hard workers who value wealth and are in a stable relationship. There might be stepchildren to whom the individual is closer than birth children who don’t keep in touch.

A life partner who has never made important financial decisions will usually welcome the support and guidance of an adviser who is familiar with the family’s wealth plan and the various components, in the event of their partner dying or becoming seriously ill. It can take several years to get to know a family and its dynamics and to uncover the various issues, and this takes investment in time and emotional energy on the part of the adviser. The more your wealth adviser gets to know you as a person, the more that trust and empathy will develop.

The financial bodyguard

Poor products and services, the constant barrage of media ‘noise’ and human emotions can conspire to mean sometimes you will need protecting from people, products and services that are not good for your wealth. The role of financial body-guard is not always one that you might associate with a good financial adviser, particularly if you have used transaction-based firms such as private banks, insurance salespeople or brokers who are reliant on commission from product sales. ‘Bodyguard’ is, however, a key role provided by advisers who do not represent or are not in any way tied to a product provider and whose remuneration is paid directly by you through pre-agreed fees.

The financial organiser

Being well organised means knowing what financial assets you own and why you own them. Knowing the location of important paperwork like legal papers and ownership certificates is also essential. A good adviser can help you to make sense of what you have and, where possible, simplify and rationalise things so that you have as few moving parts as possible. Minimising paperwork, information and other administrative tasks is the key to being well organised. The more organised you feel, the more confidence you will have about your wealth. The more confidence you have, the better your decision making will be and the more you’ll enjoy life.

Keeping a good audit trail to substantiate certain financial planning strategies and solutions is another key discipline with which the better advisory firms will help you. For example, a useful but under-used inheritance tax planning technique is to make regular gifts out of surplus income. As long as various conditions are met, the amount gifted falls out of the inheritance tax planning net immediately. A key element necessary to prove to the tax authorities that you have met the conditions for the tax exemption is to have copies of an exchange of letters recording gifts made, including dates and names. A decent firm will help you to maintain the necessary records.

Planning and advice fees and value

There are numerous ways that financial planners and wealth managers charge for their services:

- fixed initial and service fees

- hourly charge

- percentage of assets invested

- proportion of tax saved

- product commissions received on non-regulated tax shelters, and insurance products.

Sometimes these charging methods are combined. The key point is to know what you are paying and why. Regardless of what the rules say and no matter how convenient it might be, I think you should agree the fees for the advice and services you use and pay them yourself, and ideally avoid paying them by way of deductions from financial products. An adviser who agrees and charges explicit fees rather than relying on payments from transactions or from product deductions has less of a conflict of interests in the advice that they give. It is also easier for you to determine whether or not those fees have been good value for money.

Many private banks and certain restricted financial advisers use their organisation’s own products and funds, which are often more expensive than would be the case if you used an independent adviser, whether they agree an explicit fee for planning services or not. The more complicated the product or solution, the more likely it is to be expensive and to have high fees and costs. Some ‘advisers’, who do not charge stand-alone advice fees, insist on being paid by way of adviser charge deducted from investment products. This is a bit like your doctor earning a commission every time he prescribes you drugs; in such a situation you can expect most diagnoses to need medication.

If you use a good wealth manager then you should expect to pay a fixed planning fee for the initial work and this will vary depending on the complexity and value of your wealth, as well as the breadth and depth of the firm’s professional staff. Ongoing management fees should relate to the ongoing value being delivered, as well as the degree of responsibility assumed and services provided by the wealth manager, so make sure you know what you are paying, what you are getting for those fees and that you have a means of assessing value for money.

Management fees are high and still rising

By Emma Dunkley

Despite mounting pressure on the financial services industry for greater transparency over fees and lower costs for investing, the charging structures of many wealth managers are still far from clear. Yet, although more investors are starting to pay more attention to charges, few wealth managers are taking decisive action to clarify or reduce them.

Most firms still apply ad valorem charges, levying a fee based on a percentage of assets under management, which means that costs increase as the value of assets under management grows. Some offset the impact with tiered fee structures, whereby the level of the ad valorem charge reduces as assets rise, but few firms apply a flat, fixed fee, which investors argue is a more transparent charging structure.

Gina Miller, founding partner of SCM Private, who spearheads the True and Fair Campaign on fees, says about 70 per cent of an investor’s real return can be eaten by charges. The average wealth management charge, including the cost of the investments, amounts to 3.24 per cent a year.

But transaction costs incurred by the wealth firm and fund managers, which are often undisclosed, come to an average of 0.41 per cent a year, Ms Miller adds. That takes the total to an average 3.65 per cent a year – compared to an average real annual return on equities of 5.2 per cent. Transaction charges vary widely; some groups include them in the overall cost of management, others charge them at a flat-rate cost, such as £25 or £35, others charge a percentage transaction fee (which can be as high as 1.65 per cent) and there are often “settlement” or “compliance” charges on top.

Upfront charges can inflate that still further in the early years. Research by Numis Securities reveals that wealth managers charge as much as 7.5 per cent a year in some cases. An investor with £120,000 invested across funds, shares, investment trusts and exchange traded funds, split across a pension, investment account and individual savings account, could pay up to £8,970 in fees to St James’s Place in the first year, according to Numis. The same portfolio at Barclays Wealth Advisory would cost £5,475 a year on a portfolio of £120,000. The Hargreaves Lansdown Portfolio Management Service charges £1,462 a year.

St James’s Place pointed out that the charge includes the initial and ongoing cost of advice, which is not typically included in figures from other wealth managers. The figure also accounts for the charge for exiting the investment in the first year, which few investors would do.

Nonetheless, the research by Numis and others reveals the wide discrepancy in fees and how difficult they are to ascertain. Ms Miller says investors often believe the “annual management charge” represents the total cost. “Unless there’s a standard method with all the explicit and implicit charges updated on an annual basis, there’s no chance of understanding it,” she says.

Wealth managers say they are working towards a model of greater transparency. Last year, Rathbones and Quilter Cheviot joined forces to create a standard methodology for calculating total account costs, expressed as an annual percentage. And European regulation coming into force in the next few years should drive wealth managers towards improving their overall charging structures.

Aside from the lack of transparency over fees, investors are also concerned that charges are rising, rather than coming down. “We’ve noticed that a number of people are paying very high annual fees via discretionary investment services,” says Justin Modray, founder of financial advice site Candid Money. Investors typically pay more than 1 per cent for the wealth manager’s service plus fees for the underlying funds of about 2 per cent a year – often on hundreds of thousands of pounds.

![]()

Source: Dunkley, E. (2014) Management fees are high and still rising, Financial Times, 21 June

© The Financial Times Limited 2014. All Rights Reserved.

Vanguard, the mutual low-cost investment fund company, sets out how it sees good financial advisers delivering value, which it describes as ‘adviser alpha’, and it isn’t related to beating investment markets:

‘A more pragmatic answer for both parties might be “better than investors would likely do if they didn’t work with a professional adviser”. In this framework, an adviser as alpha (i.e. added value) is more aptly demonstrated by his or her ability to effectively act as a wealth manager, financial planner and behavioural coach – providing discipline and reason to clients who are often undisciplined and emotional – than by efforts to beat the market. … On their own, investors often lack both understanding and discipline, allowing themselves to be swayed by headlines and advertisements surrounding the “investment du jour” – and thus often achieving wealth destruction rather than creation. In the adviser as alpha framework we’ve described, the adviser becomes an even more important factor in the client–adviser relationship, because the greatest obstacle to clients’ long-term investment success is likely to be themselves.’7

Until now gamma has been the term that academics used to describe the degree to which an investor is risk averse. Recently two academics redefined gamma as a measure of the additional expected retirement income achieved by an investor from making more intelligent financial planning decisions.8

In summary, these financial decisions relate to five main areas:

- A total wealth framework (or plan) to determine the optimal asset allocation strategy.

- A dynamic regular portfolio withdrawal strategy.

- Incorporating guaranteed-income products (i.e. annuities) as necessary.

- Tax-efficient investment allocation and withdrawal decisions.

- Optimising the portfolio to take into account risks such as those from inflation and currency movements which would impact on achieving different goals.

A significant proportion of investors will want and/or need to take ongoing advice from a professional financial adviser to make these good decisions. Financial advice is not free and it’s natural to wish to avoid incurring costs for something where the value is not clear. The academics have, however, calculated the value of getting these decisions right in terms of additional retirement income, which they calculate to be 22% more income, equivalent to 1.59% p.a. average additional return.

The majority of UK-regulated financial advisers are highly qualified, knowledgeable and professional. While advice fees are a cost, the value that you and your family should receive, in the form of a better financial outcome, should make the cost pale into insignificance in the long run.

Adviser checklist

The checklist below lists questions to ask a prospective adviser. Sources of good advice can be found in the useful websites and further reading section at the end of the book.

Checklist

Full-service advice firm – due diligence

- Do you provide structured financial planning as the core service before offering investments or other services?

- Do you offer a transparent ‘fee for service’ charging structure that is not linked to the arrangement of products or investments?

- Do you offer products, funds and financial solutions from the whole marketplace or do you offer only a restricted range from a few companies?

- Do you have experience of dealing with people like me in terms of personality, family situation, level of wealth and wealth issues?

- Do you and your colleagues hold advanced-level professional financial advice qualifications and, if so, what are these?

- What arrangements do you have to bring in expertise from outside your firm if needed, such as legal or tax planning, and how is this integrated into your own service?

- Do you ever receive sales commissions from any source (e.g. insurance products or introducer fees from other professionals) and, if so, will you rebate this either back into the product or directly to me?

- What is your investment philosophy and do you have a comprehensive document that sets out your approach and rationale?

- How are the professional staff in your firm remunerated?

- Would you be able to allow me to speak to one of your clients in a similar situation to myself before committing to using you?

- Could you show me example outputs of your written work, including the financial plan, so I can have an idea of what to expect?

- How many meetings and discussions can I expect to formulate the initial strategy and how long is this likely to take?

- What is the minimum commitment required from me in terms of time and fees?

- What level of resources does your firm have in terms of financial planning, investment and tax expertise?

- Who are the actual people with whom I and my family will be dealing on a day-to-day basis?

- If something goes wrong with the service or your advice, to whom do I complain?

- What are the key financial results for your company in terms of balance sheet strength, revenue and profits?

- Do you think I am the type of customer you are looking for and could service well?

1 Bogle, J. (2007) The Little Book of Common Sense Investing, Wiley.

2 Data source: Morningstar, FTSE, ONS ten-year performance to 31.12.2010.

3 Data source: Morningstar, FTSE, ONS ten-year performance to 31.12.2013.

4 Dalbar Inc., Quantitative Analysis in Investor Behaviour 2014.

5 Transcript of video interview with respected investment expert and author Charles Ellis on investment fundamentals: www.vanguard.co.uk/uk/portal/Library/interviews--video-ellis.jsp

6 Source: www.fpsb.org/ as at April 2014.

7 Bennyhoff, D.G. and Kinniry, F.M. (2010) ‘The adviser as Alpha: Insights from the US market’, Vanguard White paper, December.

8 Blanchett, D. and Kaplan, P. (2012) ‘Alpha, beta, and now … gamma’, Morningstar White paper.