GENERAL TAX PLANNING

Intaxication (n.): Euphoria at getting a tax refund, which lasts until you realise it was your money to start with.

The main personal taxes

The following are the main taxes (and rates for 2014–2015) as they affect UK-domiciled and resident individuals:

- Income tax – levied on earnings, rental income, royalties, interest and dividends at rates between 20% and 45%.

- Value added tax (VAT) – levied on purchase of most goods and services, mainly at a rate of 20%.

- Capital gains tax (CGT) – levied on gains arising on disposal of assets in one’s lifetime at either 18% or 28% depending on the income tax rate paid, although the rate is 10% for gains of up to £10 million arising from the sale of certain business interests and assets.

- Stamp duty and Stamp duty land tax (SDLT) – levied on most transactions involving the purchase of equities at a flat rate of 0.50% and transactions involving the purchase and sale of land and property at rates between 1% and 7% (15% where property is purchased by certain ‘non-natural persons’).

- Inheritance tax (IHT) – a flat rate of 40% levied on the death of a UK-domiciled individual (or a non-UK-domiciled individual who has become ‘deemed’ domiciled) on worldwide assets above £325,000 if not left to a surviving spouse/civil partner or charity/political party (36% where at least 10% of the taxable estate is left to charity). Non-UK-domiciled individuals who have neither been classed as ‘deemed’ domiciled nor elected to be treated as UK domiciled are subject to IHT only on most UK assets. A 20% rate is payable in lifetime on gifts to most types of trust above a limit (currently £325,000 every seven years).

Your tax risk profile

Just as we have our own individual investment risk profile we also all have our own tax risk profile. Knowing your tax risk profile is important because it will help you to determine what type of tax planning might be worth considering. Your tax risk profile will depend on a number of factors:

- your desire to save tax – most people understand that they have to pay a fair share of tax, although the top 1% of taxpayers pay nearly a third of all income tax1

- your need to save tax – what difference saving tax will make to you and/or your wider family

- your capacity to understand – being successful and creating wealth doesn’t mean that you are necessarily able to understand complex planning ideas

- your feelings about raising your tax profile – the taxman uses a range of profiling techniques for taxpayers based on information gained from tax returns, land registry and various other data sources. Certain transactions and disclosures might increase your chances of an enquiry

- whether or not you invest in professional and personalised advice – employing a professional tax adviser can be a good ‘investment’, both in terms of avoiding pitfalls and securing tax savings many times the fee paid.

There are different degrees of tax planning, ranging from simple and tested through to highly aggressive and contentious:

- low tax risk – standard planning that is non-contentious such as making a pension contribution, offsetting losses against gains, using an investment bond to defer tax on gains, and using a limited company to control personal taxable income

- high tax risk – this includes aggressively marketed tax schemes that aim to achieve a tax saving. Examples of previous planning that would have fallen within this definition include double trust IOU home schemes – to achieve an inheritance tax saving, employee benefit trusts that used a sub-trust to obtain a corporation tax deduction, and certain qualifying recognised overseas pension schemes that offered the ability to give access to a 100% tax-free lump sum from UK-sourced pension funds.

Attacking aggressive tax planning

HMRC estimates that the difference between the tax it receives and the tax it would have received as ‘officially intended’ is in the region of £35 billion.2 Although illegal evasion and criminal activity represent the biggest element of this, a significant amount (c. £2 billion) relates to ‘avoidance’ and ‘legal interpretation’. To counteract this loss of tax, a range of new rules and obligations has been introduced over the past decade.

Disclosure of Tax Avoidance Scheme (DoTAS)

Since 2004 promoters of tax ‘schemes’ to UK residents which meet certain conditions are required to notify HMRC of the existence of such schemes by quoting a Disclosure of Tax Avoidance Scheme number. There are high penalties for non-disclosure and the stated policy objective is to dissuade promotion and use of arrangements deemed aggressive and motivated mainly or partly by a tax advantage that Parliament did not intend. The taxpayer is then obliged to notify HMRC of their use of the scheme by disclosure of the DoTAS number on their self-assessment tax form. HMRC has taken an increasingly robust approach to challenging a significant number of arrangements that have been notified to them under DoTAS, and it has been claimed that it has been successful in about 80% of tax-avoidance cases.3

General Anti-Abuse Rule (GAAR)

In July 2013 the UK also introduced a General Anti-Abuse Rule (GAAR) to give HMRC wider powers to attack those arrangements it believes are abusive and to discourage taxpayers from using such arrangements. While it is too early to tell how effective the GAAR has been, you need to think carefully about how vulnerable to attack would be any tax planning you undertake. If the arrangement hasn’t been specifically sanctioned by legislation and represents an interpretation or an exploitation of a loophole, you need to be ready for challenge by HMRC. Remember that in attacking any tax planning, HMRC is spending taxpayers’ money and it has much deeper pockets than its ‘customers’.

Accelerated tax payments

At the time of writing, the government had announced its intention to introduce a requirement for taxpayers to pay on account any disputed tax relating to:

| a | an avoidance scheme that is the same or similar to one that has been defeated through litigation with another taxpayer |

| b | schemes that have been disclosed under DoTAS or |

| c | schemes that have been counteracted under the GAAR. |

Once the formal notification is given by HMRC, together with a request for the accelerated payment, the taxpayer will have 90 days to pay the tax in dispute. This won’t affect the taxpayer’s right to make their case through the tribunal process, but it does mean that there will be no cashflow advantage to the taxpayer in the meantime. If the taxpayer wins their case, HMRC will repay the tax, together with interest.

Capped income tax reliefs

Since 6 April 2013 there is a limit on the amount of tax relief that a taxpayer can claim against income tax as a result of losses, set at the greater of £50,000 or 25% of the individual’s total annual income liable to income tax. Total income is adjusted to include an individual’s charitable donations made via payroll giving and to exclude pension contributions, to create a level playing field between those whose deductions are made before they pay income tax and those whose deductions are made after tax.

The tax relief limit does not apply to:

- losses offset against profits from the same trade or property business

- losses attributable to overlap relief and Business Premises Renovation Allowances (BPRA) investment

- gifts to charity

- tax-relievable investments that are already capped, such as registered pensions, enterprise investment schemes (EIS), venture capital trusts (VCTs), Seed EIS (SEIS) and social impact investments.

Losses4 that are subject to the limit include:

- qualifying loan interest – which relates to loans to buy an interest in certain types of company or to invest in a partnership

- total losses arising on shares bought at issue

- losses arising in the early years of a new business where those losses are being claimed against income arising from that business

- claims relating to property capital allowances and agricultural expenditure.

Some limited losses may be carried forward for future use, whereas others, such as qualifying loan interest, may not, so make sure that you claim loan interest first and carry forward other losses to relieve against future income.

Tax planning principles

There are a number of basic principles that you need to be aware of to minimise taxation.

- Know your personal allowances – this is the amount you can earn or capital gains that you can realise without paying tax.

- Know your income tax band – official figures show that the number of higher-rate taxpayers in the UK has almost doubled since 1998/99.5

- Take action – make use of tax-efficient savings schemes, allowances and reliefs.

- Deferring tax – even if you can’t avoid tax, deferring when you have to pay it can enable you to generate additional returns in the meantime.

- Integrated planning – your spending, earning, investing and lifestyle decisions all need to be taken into account to determine how best to minimise taxation.

- Too good to be true – if something looks too good to be true it probably is.

- Know what you are doing – if you don’t understand it (having at least tried to), then don’t do it.

- Tax schemes – be wary of expensive tax schemes with large up-front fees from organisations with which you have no existing relationship and that require a DoTAS number to be entered on your tax return.

- Be wary of any arrangement that involves overseas entities or structures and/or that passes through several entities before ending in a final structure, as your money usually feeds many hungry mouths.

- Nothing is certain – remember that the rules can and do change, although retrospective changes are the exception and not the rule.

- Your residence status affects your liability to most UK taxes except inheritance tax, so bear in mind the rules that determine this because they changed a few years ago (see later in this chapter).

- Tax isn’t everything – be careful not to let the tax tail wag the lifestyle planning dog. Moving abroad, for example, might help you to avoid tax but might have an adverse effect on your family and other personal relationships.

Practical ways of saving tax

For the rest of this chapter I’m going to set out a range of tax planning ideas so that you can check to see you are taking advantage of all the key tactics. I have not included any planning that is a ‘scheme’ or that one could view as ‘aggressive’. That being said, you must always bear in mind that what is acceptable to the tax authorities today may well be unacceptable to them in the future. HMRC has been given significant targets to reduce the tax gap and substantial funding to achieve this by tackling tax-avoidance activities.

Closing interest deposit accounts

These are deposit accounts (usually offshore) that pay interest when you close the account and thus no tax liability can arise until then. Such accounts are useful if you want to avoid incurring taxable interest on cash until a future date, perhaps because you will then have your basic-rate income tax band available, you might have allowable capital allowances to offset or you might then be non-UK resident. If you are UK resident but non-UK domiciled, you could time the closure of an offshore account, and the addition of the accrued interest, to a tax year when you also pay the remittance basis charge, if this would be cheaper than paying UK income tax on the interest earned.

Use the tax-free savings band

From the 2015–2016 tax year, the starting rate of tax that applies on up to £5,000 of savings income is nil. The nil savings income band is lost if non-savings income (for most people, their pension or wages) exceeds their personal allowance (£10,500 in 2015–2016) plus the £5,000 savings band. This means that up to £15,500 p.a. of interest could potentially be received tax free. As well as interest from cash deposit accounts, this includes income arising from fixed income holdings such as gilts and corporate bonds, and ‘gains’ arising from offshore single-premium investment bonds.

Because an investment bond can be assigned to another person without causing an immediate tax charge, the gain will become assessable to income tax only when the recipient cashes in some or all of the bond. As long as the gain, when added to any other savings and non-savings income, is below £15,500, no tax will be payable. Figure 15.2 in Chapter 15 shows how this could work in practice.

Use other family members’ income tax bands

If your spouse/civil partner doesn’t use their personal income tax allowance or pays a lower rate of income tax than you, consider transferring sufficient savings or investment capital to them to enable any taxable income arising to be taxed at either nil or the lower rate. The transfer must be irrevocable and with tax saving not as the sole motive. Transfers of assets between spouses or civil partners who are living together are exempt from capital gains and as such may be arranged without triggering capital gains tax.

You could extend this concept to using other family members, such as a life ‘partner’, parents, children (aged 18+), brothers or sisters who are not using their full income tax band but share the same household. Make sure that your paperwork is in order, just in case you have to justify or substantiate any transfers.

Make maximum use of tax-free accounts

Make sure that you utilise your and your spouse’s/civil partner’s ISA allowance each tax year. Currently you may each contribute up to £15,000 per tax year to an Individual Savings Account and invest in cash deposits and/or stocks and shares, with all income and gains being tax-free. It is also possible to invest up to £4,000 per annum into a cash or stocks and shares Junior ISA for those under 16, and up to £15,000 p.a. into a cash-only ISA for those aged between 16 and 18.

Use National Savings products

Make use of National Savings Certificates when they are available as these provide tax-free, albeit low, returns (both nominal and index-linked) and security of capital. Premium bonds also provide tax-free returns by way of prize draws each month. Although the average return is usually quite low compared with most deposit accounts, the two top prizes each month are £1 million, so it’s a reasonable choice if you have significant capital to place in low-risk holdings and/or you have other taxable income subject to higher- or additional-rate income tax.

Make a personal contribution to a pension

A personal contribution to a pension scheme is paid net of basic-rate income tax (currently 20%) and has the effect of expanding your basic-rate income tax band accordingly. For example, an £800 contribution would gross up to £1,000 received by the pension fund and your basic rate income tax band would increase accordingly. This means that, to the extent it falls below the threshold at which higher- and additional-rate income tax is payable, taxable income from earnings, savings or investment will be taxed at the basic rate (20%) rather than at the higher (40%) or additional rate (45%).

A pension contribution can also enable you to:

- restore the loss of personal allowance where total taxable income is between £100,000 and £120,000 and obtain effective tax relief of 60% (see the example that follows)

- enable taxable capital gains arising in the same tax year, in excess of the annual exemption of £11,000, to be taxed at 18% rather than 28%, to the extent that such gains fall below the threshold at which higher-rate income tax is payable

- reduce your net adjusted income to below the £60,000 threshold at which child benefit is completely lost, with income below £50,000 enabling the full benefit to be paid

- reduce the amount of income tax payable on taxable gains arising from single-premium investment bonds (see Chapter 13 for more details).

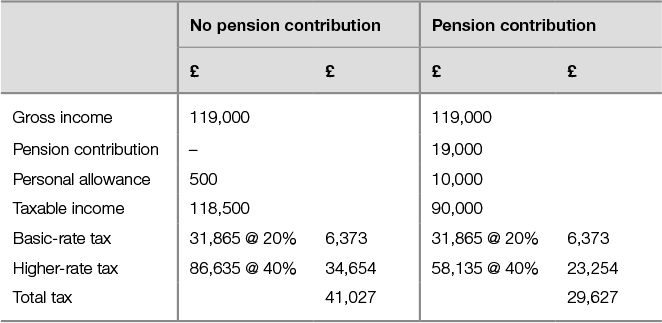

60% income tax relief

In 2014/15 John has income of £119,000, all of which consists of earnings and interest. His current pension contributions are under £20,000. He can thus make an extra £19,000 gross pension contribution without tax penalty because the aggregate contributions of £39,000 would still fall within the £40,000 annual allowance. Depending upon whether he makes the pension contribution, his tax bill would be:

Thus, a gross pension contribution of £19,000 will save John £11,400 in tax, an effective 60% rate of relief.

Have your employer make a pension contribution

If you are employed (including by a company owned and controlled by you) your employer could contribute to a pension scheme for you. This could also be funded by you giving up a right to salary or bonus (this is known as salary sacrifice). If salary or bonus is sacrificed in favour of a pension contribution before it has been contractually earned, no income tax or employer’s or employee’s National Insurance contributions will be due. Most employers are prepared to add the National Insurance saving to the contribution on the basis that it costs them no extra than the salary or bonus.

Employer contributions, unlike personal contributions, do not require a corresponding amount of ‘relevant’ earnings to justify the contribution. Employer contributions will be tax exempt as long as they are within your unused annual allowance (including any carried forward from the previous three tax years).

Claim capital allowances on property

It is possible to claim capital allowances on the purchase price of certain types of property, including holiday lets, residential (as long as at some stage it has been let to multiple households at the same time) and commercial property. The allowance you can claim will depend on the type of property and varies between 5% and 30% of the purchase price, which may be offset against taxable income arising in the current, previous or future tax years. Capital allowances are a specialist area of tax and you should take appropriate advice from an expert in this area.

Rent a room in your home when you are away for tax-free income

If you rent a room (or an entire floor) in your home to a lodger you can receive up to £4,250 per annum tax-free (or £2,125 if shared without your partner or someone else). The legislation does not say the room or rooms have to be rented to a lodger staying in your home all year, so it would be perfectly acceptable for you to go away for a long summer break and to rent out your home to someone while you are away.

There are four basic rules you must follow in order to qualify for the relief:

- The room or rooms must be within your ‘only or main residence’.

- The letting must be for living accommodation, not for use as an office, for example.

- The relief is limited to £4,250 gross receipts in the tax year.

- The relief applies to individuals only, not to companies or partnerships (although it does apply where individuals share the income other than as a business arrangement, for example husband and wife).

The ‘only or main residence’ is not the same definition as for capital gains tax relief but a simpler interpretation of where your friends would expect to find you. This means you cannot take advantage of the capital gains tax rules that allow you in certain circumstances to treat a property as being your main residence even though you do not currently live there. You do not have to own the property, although subletting rooms in a rented property would need the landlord’s agreement. The definition of ‘living accommodation’ does not have to mean place of permanent residence. It would be permanent in the case of a lodger, but the law does not specify permanence as a requirement. A holidaymaker living there for only one or two weeks would be perfectly acceptable under the law. If your tax inspector does try to claim you cannot use the relief for temporary lettings or says you cannot let the whole of your home, as then it could not be your ‘only or main residence’, point out that nowhere in the legislation6 does it say your home ceases to be your ‘only or main residence’ when you go on holiday.

Make a gift to charity

Cash donations to registered charities have the effect of expanding your basic-rate income tax band. This provides higher-rate tax relief on any taxable income above the threshold at which higher-rate tax becomes payable. It can also reduce your adjusted net income to below the £60,000 threshold at which child benefit is lost. In addition, it may also allow capital gains to be taxed at 18% rather than 28%.

Gifts of property or investments have the effect of reducing your taxable income, and as such offer the highest personal cashflow benefit for the person making the gift. In this way it may also increase the amount of your surplus annual income for the purposes of making immediately IHT-exempt gifts (see Chapter 20). For a more detailed explanation of the tax treatment of charitable gifts, see Chapter 24 on philanthropy.

Become a non-UK tax resident

Income

If you become a non-UK resident then no UK income tax is usually payable on income arising while you are non-resident. It is usually best to avoid holding UK shares or equity funds that generate income while you are a non-UK resident, due to the imposition of unreclaimable withholding tax.

Chargeable event gains from bonds

Gains arising on life insurance investment bonds are treated as income for tax purposes when a chargeable event occurs and this offers two potential planning opportunities for non-UK resident investors.

First, an investor who has been non-UK resident for part of the investment period can claim a reduction against the ‘chargeable gain’ when they resume UK residence. This was formally known as ‘time apportionment relief’. The gain calculated can be reduced by the total number of days spent out of the UK as a proportion of the total number of days the investment bond has been held. Previously, only offshore bond gains could be reduced for periods of non-UK residence, but this relief was extended to onshore bonds that commence after 5 April 2013 or existing onshore bonds that are assigned after this date. See Chapter 15 for more details on this tax treatment.

Second, if the bond is encashed when the investor is long-term non-UK resident, any gain will not be subject to UK income tax, although it may be taxable in the investor’s country of residence. Do note, however, that anti-avoidance rules introduced in 2013 mean that chargeable event gains arising on an investment bond during a temporary period of non-residence will be taxable on the individual’s return. This will be similar to the current CGT rule and will apply where an individual:

- has been resident in the UK for a period of at least four of the last seven tax years, and

- becomes UK-resident again within five years of leaving.

Capital gains

If you have assets that you acquired while a UK resident and on which you crystallise a capital gain after you become a non-UK resident, you must remain a non-UK resident for at least five years to avoid capital gains becoming payable retrospectively. If you acquire an asset after you have become a non-UK resident, you may crystallise any capital gains while you remain a non-UK resident and you will usually avoid UK capital gains tax, even if you return to the UK within five years of leaving.7 An exception to this rule is expected (at the time of writing) to apply from 6 April 2015 for non-UK residents who dispose of UK residential property. Gains apportioned to the period from that date will be subject to tax, regardless of residence status.

The UK, in line with many countries around the world, now has a Statutory Residence Test, which is designed to give taxpayers more certainty about their residence status and what they need to do to ensure that they are non-UK resident. In broad terms, if you’ve never been UK resident then it is now harder to become tax resident, whereas if you have been UK resident it is now harder to lose that status. Figure 14.1 gives more information on residence, but bear in mind that if your circumstances are complicated, you should seek specialist tax advice on your status.

Offset trading losses against income

Business trading losses incurred personally,8 whether as a sole trader or as a partner or member of an LLP, can be claimed against your other income, from whatever source, in the same year as the loss or the preceding year. Loss relief can similarly be claimed against capital gains, which is likely to be more useful now that the top rate of capital gains tax is 28%.

Trading losses arising in the first four years of a new business may be offset against taxable income going back up to three years on a first in and last out basis. While making losses is not to be welcomed, getting the taxman to help you will at least soften the blow. This illustrates a key benefit of using an LLP as the primary structure for an early-stage business that incurs initial losses, if you have other income subject to the higher or additional income tax rate. Do note, however, that this type of loss relief is restricted to the higher of £50,000 or 25% of your total taxable income each tax year.

Invest in a VCT, an EIS or a Seed EIS

Although traditionally these were high-risk investments, a number of VCT and EIS providers now issue lower-risk funds that invest in cash-generative trades, where the objective is to return the original capital invested through an orderly wind-up and distribution of cash after a set number of years. A SEIS provides more generous tax benefits but is generally much more risky due to the fact that it invests in very small start-up ventures.

VCT

Up to £200,000 may be invested in a VCT each tax year, with income tax relief of up to 30%, subject to holding the shares for five years. Dividends and capital gains are tax free.

EIS

Up to £1 million may be invested in a qualifying EIS each tax year (and a further £1 million can be carried back to the previous tax year), with income tax relief of up to 30%, subject to holding the shares for three years. The income tax relief is limited to the extent of your tax liability and if you make a loss from an EIS, in excess of the initial income tax relief, this may be offset against other taxable income in the tax year of loss and/or carried back to the preceding tax year. Any subsequent capital gains are tax-free, and for this reason it is rare for the EIS to pay dividends that would be taxable. However, unlike a VCT, any future losses in excess of the initial income tax relief are allowable as a deduction against other taxable income.

A lower-risk EIS, which returns just your initial investment, can offer a highly attractive return, purely on account of the initial tax relief. Figure 14.2 sets out the projected internal rate of return from an EIS based on a number of scenarios. The breakeven point for you to be no worse off is realising 70p for every 100p invested if you can’t offset the loss against other taxable income, or 42p if you can (at the rate of 40%).

Figure 14.2 Internal rate of return from range of EIS outcomes

SEIS

Up to £100,000 can be invested into small start-up companies each tax year (and a further £100,000 can be carried back to the previous tax year), with income tax relief of up to 50%, subject to holding the shares for three years. In addition, other taxable capital gains may be reinvested into a SEIS and 50% of this amount will be permanently exempt from tax when the SEIS is eventually realised. Gains arising in the previous tax year also qualify for this treatment. SEIS are unlikely to appeal to many investors due to the extremely high-risk nature of the types of businesses that would qualify for investment. However, if you have a friend or relative who wants to start up a business that qualifies as a SEIS, the tax reliefs will reduce the effective cost.

Table 14.1 compares the main features of VCTs, EIS and SEIS.

Invest in a social impact investment

Social impact investments provide tax benefits that are virtually the same as EIS. However, because the return is primarily by way of positive outcomes for society, the investment return to you as an investor is likely to be minimal, if any. If you pay income tax, have other taxable capital gains subject to 28% tax, have maximised all the other non-aggressive planning options (or don’t wish to) and are interested in making a difference to society instead of or in addition to any charitable giving, this could be an interesting addition to your plan. The following example shows that an internal rate of return of over 25% p.a. is possible with just a return of capital.

Social impact investing – an example

Sally has paid income tax for several years, up to and including the 2015–2016 tax year, of just over £15,000 per year. In the 2015–2016 tax year she also realised taxable capital gains (i.e. in excess of her capital gains tax exemption) of £100,000 from selling a rental property. Because she has no basic-rate income tax band, it having been used up by her taxable income, the tax would be due on the gains of £28,000 (£100,000 × 28%). Sally is interested in backing a broad range of social impact activities.

Sally invests £100,000 into the Make It Better social impact bond on 1 April 2016, (i.e. the 2015–2016 tax year) and elects to carry back £50,000 of this to the 2014–2015 tax year. In addition, she applies to hold over the capital gain arising from the property sale.

On 5 April 2019 (i.e. 2018–2019 tax year) Sally encashes half the bond to receive half her original capital. She then encashes the other half on 6 April 2019 (i.e. 2019–2020 tax year). She has her full capital gains tax exemption available in both 2018–2019 and 2019–2020. Because she has retired, she also has £20,000 of her basic-rate income tax band available in both 2018–2019 and 2019–2020.

Based on the projected cashflows the internal rate of return is 25.2% p.a.

Employing family

If you run your own business and have a lower tax-paying spouse/civil partner or other family member, you might consider employing them in your business. As long as you pay them below the thresholds at which income tax and National Insurance are payable (about £8,000 per annum should be fine), no tax will be payable, but valuable state benefits will be accrued. Make sure, however, that they actually do sufficient work to justify the income and that the rate is not less than the national minimum wage.

If you find that you need to cut expenses in a few years’ time you could, of course, make these family members redundant and choose to pay them a non-contractual termination payment. Currently this is tax deductible for the employer and up to £30,000 is tax-free to the employee. If the termination of family employees happens to coincide with when they need a deposit for a new home, it might just work out nicely for all concerned.

Share the business

You might also give your spouse/civil partner, and possibly your children, shares in your company or partnership so that profits can be distributed to them. Although the shares need to have full voting rights, you could restrict these to a very small amount and you could then pay higher proportionate dividends to those shares. Do be careful if your business is already worth a lot, and avoid giving your children (or the bare trustee who will own the shares for a minor child) any cash used to subscribe for the shares, and make sure you take proper tax advice.9

Turn your investment property portfolio into a trading business

If you own property as part of a trading activity there are several tax advantages:

- Losses can be relieved against other income.

- Unrealised losses can be relieved against income.

- Rollover relief on capital gains arising from sale of fixed assets used for the trade.

- Tax of only 10% on the sale or wind-up of a company.

- The value should qualify for business property relief and as such be exempt from inheritance tax (see Chapters 20, 21 and 22).

Turn your hobby into a business

You’d be surprised how many hobbies could be turned into a trading business:

- travel – travel writer or reviewer, TV/film location scout

- country home – smallholding/farming business

- music – music label, promoter, reviewer, performer

- flying – teaching, transporting, fun flights

- history – lecturing and writing on historic matters

- cars – provide classic/high-value cars for hire to weddings, film production companies and other suitable hirers.

A business must be commercial and run with a view to making a profit, so you’ll need to create a business plan setting out your aims and trading activities. Assuming that the commercial intention is clearly established, most of your setup and running costs will be tax deductible against your other taxable income. Don’t forget that in the first four years of a trade you can carry back trading losses up to three years prior to the year of loss. A travel business, for example, will clearly involve flights, accommodation, travel and subsistence, a laptop computer, smart phone and stationery, so it’s nice to know that the taxman will be helping towards these costs.

Invest in commercial woodland

Whether you invest via a fund, a syndicate or directly on your own, woodland that is managed commercially benefits from several tax advantages, including:

- income arising from the trade is exempt from income or corporation tax

- capital gains arising from the sale of trees (not the land) are exempt from tax

- other taxable capital gains may be deferred by being reinvested into woodland

- the value is exempt from inheritance tax after two years’ ownership.

Become an owner in your friend’s or relative’s business

If you want to provide some financial assistance to a friend or relative, from a tax perspective it is likely to be more effective if you become a general partner or limited liability partner, rather than loaning them money. Any losses arising will be allowable against other taxable income (subject to limits), but as and when you want your capital back, this can be done without any tax implication as it will be treated as a repayment of your capital account. In addition, after two years your holding will qualify (as long as the business is not carrying out an excluded activity) for inheritance tax exemption under business property relief.

If your friend or relative’s business is a limited company, make sure that you subscribe for new shares, not buying existing ones from existing shareholders. This is because only new shares qualify for income loss relief in the event that the company goes bust with no value.

Turn a second home or investment property into a furnished holiday letting property

Losses arising from a furnished holiday let (FHL) property, including those arising from mortgage interest, are allowable against the same FHL income. The FHL business could include several FHL properties held as a sole trader or within a limited liability partnership structure. The eligibility rules for a property to qualify as an FHL have been toughened up over the past few years. The property must be available for letting for at least 210 days/30 weeks (increased from 140 days/20 weeks) and must be actually let for at least 105 days/15 weeks (increased from 70 days/10 weeks) of the tax year. It should be noted that the tax treatment of FHLs applies to property situated anywhere in the European Economic Area (EEA).

Interest on a new mortgage taken against the FHL property will usually qualify as deductible against current and future FHL income as long as the loan is equal to or less than the original purchase price plus the cost of any improvements made since then and any profits are retained in the FHL business. It may be possible to claim capital allowances on certain aspects of the property, such as furniture and plant and machinery, and in some cases this can amount to as much as 15% of the property value. The availability of capital allowances on an FHL property depends on when it first qualified as an FHL based on the current eligibility rules referred to earlier.

Another point worth remembering is that all taxable earnings arising from an FHL qualify as relevant income for pension contribution purposes. Therefore, provided that you have sufficient unused pension annual and lifetime allowance, you could make a contribution and obtain tax relief at your highest rate. If only one of you has unused pension lifetime allowance but you own the FHL jointly, there is nothing to stop you from allocating the bulk of the profits to the one who has unused pension lifetime allowance so they can make the pension contribution.

Any capital gains arising on disposal of an FHL should qualify for entrepreneurs’ relief. As such, as long as total gains from business holdings have not exceeded £10 million in your lifetime, the taxable gain on an FHL will be subject to only 10% tax. Alternatively, you might be able to apply for Business Asset Rollover relief, if you reinvest the proceeds of one FHL into another FHL (although it could be another non-FHL business asset). An FHL may qualify for exemption from inheritance tax, providing that it is treated as ‘trading’ rather than being held as purely an investment. The more actively you are involved in managing an FHL, the more likely you are to secure IHT exemption.

Minimising capital gains tax

- Use your annual exemption to crystallise gains (£11,000 in 2014–2015 and £11,100 in 2015–2016).

- Hold capital growth assets within an ISA (up to £15,000 per tax year).

- If your gains exceed the capital gains tax exemption each tax year, consider crystallising sufficient losses to offset those excess gains.

- Make an irrevocable transfer of assets to your spouse/civil partner prior to realising capital gains if they are a non/basic-rate taxpayer and as such would pay tax at 18% rather than 28% and/or they would fall within their unused annual capital gains tax exemption.

- Make a pension contribution and/or a charitable gift. This will expand your basic-rate income tax band, so that taxable capital gains are taxed at 18% rather than 28%, to the extent that the gains fall within the unused basic-rate income tax band.

- Gift property and/or investments to a charity to reduce your taxable income to enable you to have gains taxed at 18%, to the extent that they fall within the unused basic-rate income tax band (c. £42,000 with personal allowance).

- If you do crystallise some capital gains, be careful about also realising losses before 6 April. Capital losses made in a tax year first have to be offset against gains made in the same tax year, with any extra losses carried forward to offset against gains arising in future years. If your gains alone would have been within your annual exemption, the losses are effectively wasted. Losses arising from previous tax years may continue to be carried forward indefinitely until taxable gains arise.

- Become non-UK resident before realising taxable gains, but remember to remain so for five years.

- Consider reinvesting the taxable gain into a qualifying trading investment, such as a lower-risk EIS or commercial woodland (or fund).

- Set up your own EIS company that carries out a qualifying trade (specialist advisers can help you with this), funded by reinvestment of other taxable capital gains to defer paying tax. As long as you aren’t claiming income tax relief you can own 100% (not just 30%) of the shares and after three years you can change the trade to any activity (including becoming a family investment company) without the deferred capital gains becoming chargeable (see Chapter 22).

- Hold the asset until you die, as CGT is washed out on death.

Trading assets

Subject to the normal caveats about risk and liquidity, consider investing in a trading business so that disposal of the business would be eligible for entrepreneurs’ relief, giving CGT at 10% on up to £10 million of gain. The main requirement is that the business must be trading and you have owned your stake for at least 12 months. In the case of a limited company you must be an employee (not necessarily full time) or officer of the company (i.e. a director but not necessarily paid) with at least 5% of the ordinary share capital and voting rights.

Business profit entity

Choose your business entity and method of profit extraction carefully. The choice is between sole trader, general partnership, limited liability partnership and limited company (UK or overseas) and each has a different tax effect. Don’t assume that a limited company is the correct choice because this effectively creates an artificial tax barrier around profits and assets that can reduce flexibility. An LLP structure is transparent for tax purposes but does mean you can end up paying income tax on profits retained for use by the business.

Limited company directors – salary/bonus or dividends?

Unless you are a non-taxpayer or have losses that you are permitted to offset against income, a dividend usually provides a shareholding director with the highest net-of-tax cash. Bear in mind, however, that dividends won’t contribute anything towards your state pension and other National Insurance contribution-based benefits. Table 14.2 shows the tax cost of extracting cash as salary/bonus or dividends for a basic-rate and higher-rate taxpayer.

Table 14.2 Net cash from salary/bonus or dividends for basic and higher-rate taxpayer

The need for professional advice

The UK tax system is intricate and constantly changing, so your planning needs to be reviewed regularly in the light of the applicable rules and legislation. Depending on the magnitude of your wealth and how complex your affairs are, you may need to employ a tax adviser. Minimising tax usually requires a coordinated approach and a mixture of planning tactics. This has never been more so than in today’s taxation environment.

A common mistake is to confuse having an accountant with having a tax adviser. The majority of accountants are not tax advisers but are, in all truth, better described as tax and accounts compliance experts. A decent accountant will make sure that you prepare your tax information, make the correct disclosures and submit your tax return within the appropriate timescales. Because of their personality traits and business model, a substantial proportion of accountants are keen to preserve their regular fee income arising from tax compliance and audit work. While some do look to provide added-value services such as tax planning, for many it is not their focus and they often see it as a risky activity.

A qualified tax adviser, meanwhile, understands the detail of tax legislation/practice and is constantly seeking out ways to arrange clients’ financial affairs to minimise taxation. A tax adviser’s business model may include a tax compliance service, but many of the best advisers do not get involved in compliance, preferring to work with clients’ existing accountants. The best tax advisers are creative, proactive and generate fee income from delivering real tax savings that repay their fees many times over.

Tax is a complex area and not something that you should approach lightly. HMRC’s current assertive and aggressive approach, together with the demands for tax revenue, is likely to see high-value taxpayers targeted more and more for investigation. It makes sense, therefore, to ensure that you have your tax affairs in good order.

1 HMRC, ‘Income tax liabilities statistics 2011–12 to 2013–14’, Table 2.4, p. 28 states that it is estimated that 28.3% of all income tax in 2013/14 was paid by the top 1% of taxpayers.

2 HMRC, ‘Measuring tax gaps – 2013 edition’, www.hmrc.gov.uk/statistics/tax-gaps/mtg-2013.pdf

3 As reported by Reuters, ‘Britain seeks to take the shine off tax-avoidance schemes’, 19 March 2014.

4 There are several other losses that are included in the cap and these, together with helpful examples, can be found at www.hmrc.gov.uk/budget-updates/march2013/limit-relief-guidance.pdf

5 HMRC, ‘Income tax liabilities statistics 2011–12 to 2013–14’, Table 2.1, p. 21 states that in 1998/99 there were 2.3 million higher-rate taxpayers compared with the estimate of 4.4 million in 2013/14.

6 Section 784 of the Income Tax (Trading & Other Income) Act 2005 dictates exactly how the rent-a-room relief must be applied.

7 Where an asset has been acquired by an individual when non-UK resident, but which is classed as a replacement asset for an asset previously acquired while UK resident, capital gains can become payable on the disposal of the asset acquired while non-UK resident.

8 Where the claimant works in the trading business for less than ten hours per week on average over a six-month period, the trade will be treated as ‘non-active’ and as such any losses arising will be subject to a cap of £25,000 per annum.

9 The Children’s Settlement rule applies where income arises from capital gifted by parents to be held on bare trust for their minor children such that any income arising would be taxed against the parent. It is therefore essential that you take expert tax advice when considering any income tax planning involving minor children. Capital gains arising, however, are still taxed against the child.