CHAPTER 9

INVENTORIES

After completing this chapter, you will be able to do the following:

- Distinguish between costs included in inventories and costs recognized as expenses in the period in which they are incurred.

- Describe different inventory valuation methods (cost formulas).

- Calculate and compare cost of sales, gross profit, and ending inventory using different inventory valuation methods and using periodic and perpetual inventory systems.

- Calculate and explain effects of inflation and deflation of inventory costs on the financial statements and ratios of companies that use different inventory valuation methods (cost formulas or cost flow assumptions).

- Explain LIFO reserve and LIFO liquidation and their effects on financial statements and ratios.

- Convert a company’s reported financial statements from LIFO to FIFO for purposes of comparison.

- Describe implications of valuing inventory at net realizable value for financial statements and ratios.

- Describe the financial statement presentation of and disclosures relating to inventories.

- Explain issues that analysts should consider when examining a company’s inventory disclosures and other sources of information.

- Analyze and compare the financial statements and ratios of companies, including those that use different inventory valuation methods.

Merchandising and manufacturing companies generate revenues and profits through the sale of inventory. Further, inventory may represent a significant asset on these companies’ balance sheets. Merchandisers (wholesalers and retailers) purchase inventory, ready for sale, from manufacturers and thus account for only one type of inventory—finished goods inventory. Manufacturers, however, purchase raw materials from suppliers and then add value by transforming the raw materials into finished goods. They typically classify inventory into three different categories:1 raw materials, work in progress,2 and finished goods. Work-in-progress inventories have started the conversion process from raw materials but are not yet finished goods ready for sale. Manufacturers may report either the separate carrying amounts of their raw materials, work-in-progress, and finished goods inventories on the balance sheet or simply the total inventory amount. If the latter approach is used, the company must then disclose the carrying amounts of its raw materials, work-in-progress, and finished goods inventories in a footnote to the financial statements.

Inventories and cost of sales (cost of goods sold)3 are significant items in the financial statements of many companies. Comparing the performance of these companies is challenging because of the allowable choices for valuing inventories: Differences in the choice of inventory valuation method can result in significantly different amounts being assigned to inventory and cost of sales. Financial statement analysis would be much easier if all companies used the same inventory valuation method or if inventory price levels remained constant over time. If there was no inflation or deflation with respect to inventory costs and thus unit costs were unchanged, the choice of inventory valuation method would be irrelevant. However, inventory price levels typically do change over time.

International Financial Reporting Standards (IFRS) permit the assignment of inventory costs (costs of goods available for sale) to inventories and cost of sales by three cost formulas: specific identification, first-in, first-out (FIFO), and weighted average cost.4 U.S. generally accepted accounting principles (U.S. GAAP) allow the same three inventory valuation methods, referred to as cost flow assumptions in U.S. GAAP, but also include a fourth method called last-in, first-out (LIFO).5 The choice of inventory valuation method affects the allocation of the cost of goods available for sale to ending inventory and cost of sales. Analysts must understand the various inventory valuation methods and the related impact on financial statements and financial ratios in order to evaluate a company’s performance over time and relative to industry peers. The company’s financial statements and related notes provide important information that the analyst can use in assessing the impact of the choice of inventory valuation method on financial statements and financial ratios.

This reading is organized as follows: Section 2 discusses the costs that are included in inventory and the costs that are recognized as expenses in the period in which they are incurred. Section 3 describes inventory valuation methods and compares the measurement of ending inventory, cost of sales and gross profit under each method, and when using periodic versus perpetual inventory systems. Section 4 describes the LIFO method, LIFO reserve, and effects of LIFO liquidations, and demonstrates the adjustments required to compare a company that uses LIFO with one that uses FIFO. Section 5 describes the financial statement effects of a change in inventory valuation method. Section 6 discusses the measurement and reporting of inventory when its value changes. Section 7 describes the presentation of inventories on the financial statements and related disclosures, discusses inventory ratios and their interpretation, and shows examples of financial analysis with respect to inventories. A summary and practice problems conclude the reading.

Under IFRS, the costs to include in inventories are “all costs of purchase, costs of conversion, and other costs incurred in bringing the inventories to their present location and condition.”6 The costs of purchase include the purchase price, import and tax-related duties, transport, insurance during transport, handling, and other costs directly attributable to the acquisition of finished goods, materials, and services. Trade discounts, rebates, and similar items reduce the price paid and the costs of purchase. The costs of conversion include costs directly related to the units produced, such as direct labor, and fixed and variable overhead costs.7 Including these product-related costs in inventory (i.e., as an asset) means that they will not be recognized as an expense (i.e., as cost of sales) on the income statement until the inventory is sold. U.S. GAAP provide a similar description of the costs to be included in inventory.8

Both IFRS and U.S. GAAP exclude the following costs from inventory: abnormal costs incurred as a result of waste of materials, labor or other production conversion inputs, any storage costs (unless required as part of the production process), and all administrative overhead and selling costs. These excluded costs are treated as expenses and recognized on the income statement in the period in which they are incurred. Including costs in inventory defers their recognition as an expense on the income statement until the inventory is sold. Therefore, including costs in inventory that should be expensed will overstate profitability on the income statement (because of the inappropriate deferral of cost recognition) and create an overstated inventory value on the balance sheet.

EXAMPLE 9-1 Treatment of Inventory-Related Costs

Acme Enterprises, a hypothetical company that prepares its financial statements in accordance with IFRS, manufactures tables. In 2009, the factory produced 900,000 finished tables and scrapped 1,000 tables. For the finished tables, raw material costs were €9 million, direct labor conversion costs were €18 million, and production overhead costs were €1.8 million. The 1,000 scrapped tables (attributable to abnormal waste) had a total production cost of €30,000 (€10,000 raw material costs and €20,000 conversion costs; these costs are not included in the €9 million raw material and €19.8 million total conversion costs of the finished tables). During the year, Acme spent €1 million for freight delivery charges on raw materials and €500,000 for storing finished goods inventory. Acme does not have any work-in-progress inventory at the end of the year.

1. What costs should be included in inventory in 2009?

2. What costs should be expensed in 2009?

Solution to 1: Total inventory costs for 2009 are as follows:

| Raw materials | €9,000,000 |

| Direct labor | 18,000,000 |

| Production overhead | 1,800,000 |

| Transportation for raw materials | 1,000,000 |

| Total inventory costs | €29,800,000 |

Solution to 2: Total costs that should be expensed (not included in inventory) are as follows:

| Abnormal waste | €30,000 |

| Storage of finished goods inventory | 500,000 |

| Total | €530,000 |

3. INVENTORY VALUATION METHODS

Generally, inventory purchase costs and manufacturing conversion costs change over time. As a result, the allocation of total inventory costs (i.e., cost of goods available for sale) between cost of sales on the income statement and inventory on the balance sheet will vary depending on the inventory valuation method used by the company. As mentioned in the introduction, inventory valuation methods are referred to as cost formulas and cost flow assumptions under IFRS and U.S. GAAP, respectively. If the choice of method results in more cost being allocated to cost of sales and less cost being allocated to inventory than would be the case with other methods, the chosen method will cause, in the current year, reported gross profit, net income, and inventory carrying amount to be lower than if alternative methods had been used. Accounting for inventory, and consequently the allocation of costs, thus has a direct impact on financial statements and their comparability.

Both IFRS and U.S. GAAP allow companies to use the following inventory valuation methods: specific identification; first-in, first-out (FIFO); and weighted average cost. U.S. GAAP allow companies to use an additional method: last-in, first-out (LIFO). A company must use the same inventory valuation method for all items that have a similar nature and use. For items with a different nature or use, a different inventory valuation method can be used.9 When items are sold, the carrying amount of the inventory is recognized as an expense (cost of sales) according to the cost formula (cost flow assumption) in use.

Specific identification is used for inventory items that are not ordinarily interchangeable, whereas FIFO, weighted average cost, and LIFO are typically used when there are large numbers of interchangeable items in inventory. Specific identification matches the actual historical costs of the specific inventory items to their physical flow; the costs remain in inventory until the actual identifiable inventory is sold. FIFO, weighted average cost, and LIFO are based on cost flow assumptions. Under these methods, companies must make certain assumptions about which goods are sold and which goods remain in ending inventory. As a result, the allocation of costs to the units sold and to the units in ending inventory can be different from the physical movement of the items.

The choice of inventory valuation method would be largely irrelevant if inventory costs remained constant or relatively constant over time. Given relatively constant prices, the allocation of costs between cost of goods sold and ending inventory would be very similar under each of the four methods. Given changing price levels, however, the choice of inventory valuation method can have a significant impact on the amount of reported cost of sales and inventory. And the reported cost of sales and inventory balances affect other items, such as gross profit, net income, current assets, and total assets.

3.1. Specific Identification

The specific identification method is used for inventory items that are not ordinarily interchangeable and for goods that have been produced and segregated for specific projects. This method is also commonly used for expensive goods that are uniquely identifiable, such as precious gemstones. Under this method, the cost of sales and the cost of ending inventory reflect the actual costs incurred to purchase (or manufacture) the items specifically identified as sold and the items specifically identified as remaining in inventory. Therefore, this method matches the physical flow of the specific items sold and remaining in inventory to their actual cost.

3.2. First-In, First-Out (FIFO)

FIFO assumes that the oldest goods purchased (or manufactured) are sold first and the newest goods purchased (or manufactured) remain in ending inventory. In other words, the first units included in inventory are assumed to be the first units sold from inventory. Therefore, cost of sales reflects the cost of goods in beginning inventory plus the cost of items purchased (or manufactured) earliest in the accounting period, and the value of ending inventory reflects the costs of goods purchased (or manufactured) more recently. In periods of rising prices, the costs assigned to the units in ending inventory are higher than the costs assigned to the units sold. Conversely, in periods of declining prices, the costs assigned to the units in ending inventory are lower than the costs assigned to the units sold.

3.3. Weighted Average Cost

Weighted average cost assigns the average cost of the goods available for sale (beginning inventory plus purchase, conversion, and other costs) during the accounting period to the units that are sold as well as to the units in ending inventory. In an accounting period, the weighted average cost per unit is calculated as the total cost of the units available for sale divided by the total number of units available for sale in the period (Total cost of goods available for sale/Total units available for sale).

3.4. Last-In, First-Out (LIFO)

LIFO is permitted only under U.S. GAAP. This method assumes that the newest goods purchased (or manufactured) are sold first and the oldest goods purchased (or manufactured), including beginning inventory, remain in ending inventory. In other words, the last units included in inventory are assumed to be the first units sold from inventory. Therefore, cost of sales reflects the cost of goods purchased (or manufactured) more recently, and the value of ending inventory reflects the cost of older goods. In periods of rising prices, the costs assigned to the units in ending inventory are lower than the costs assigned to the units sold. Conversely, in periods of declining prices, the costs assigned to the units in ending inventory are higher than the costs assigned to the units sold.

3.5. Calculation of Cost of Sales, Gross Profit, and Ending Inventory

In periods of changing prices, the allocation of total inventory costs (i.e., cost of goods available for sale) between cost of sales on the income statement and inventory on the balance sheet will vary depending on the inventory valuation method used by the company. The following example illustrates how cost of sales, gross profit, and ending inventory differ based on the choice of inventory valuation method.

EXAMPLE 9-2 Inventory Cost Flow Illustration for the Specific Identification, Weighted Average Cost, FIFO, and LIFO Methods

Global Sales, Inc. (GSI) is a hypothetical distributor of consumer products, including bars of violet essence soap. The soap is sold by the kilogram. GSI began operations in 2009, during which it purchased and received initially 100,000 kg of soap at 110 yuan/kg, then 200,000 kg of soap at 100 yuan/kg, and finally 300,000 kg of soap at 90 yuan/kg. GSI sold 520,000 kg of soap at 240 yuan/kg. GSI stores its soap in its warehouse so that soap from each shipment received is readily identifiable. During 2009, the entire 100,000 kg from the first shipment received, 180,000 kg of the second shipment received, and 240,000 kg of the final shipment received was sent to customers. Answers to the following questions should be rounded to the nearest 1,000 yuan.

1. What are the reported cost of sales, gross profit, and ending inventory balances for 2009 under the specific identification method?

2. What are the reported cost of sales, gross profit, and ending inventory balances for 2009 under the weighted average cost method?

3. What are the reported cost of sales, gross profit, and ending inventory balances for 2009 under the FIFO method?

4. What are the reported cost of sales, gross profit, and ending inventory balances for 2009 under the LIFO method?

Solution to 1: Under the specific identification method, the physical flow of the specific inventory items sold is matched to their actual cost.

Sales = 520,000 × 240 = 124,800,000 yuan

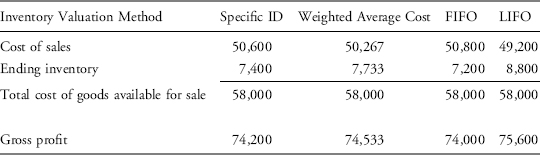

Cost of sales = (100,000 × 110)+(180,000 × 100)+(240,000 × 90) = 50,600,000 yuan

Gross profit = 124,800,000 − 50,600,000 = 74,200,000 yuan

Ending inventory = (20,000 × 100)+(60,000 × 90) = 7,400,000 yuan

Note that in spite of the segregation of inventory within the warehouse, it would be inappropriate to use specific identification for this inventory of interchangeable items. The use of specific identification could potentially result in earnings manipulation through the shipment decision.

Solution to 2: Under the weighted average cost method, costs are allocated to cost of sales and ending inventory by using a weighted average mix of the actual costs incurred for all inventory items. The weighted average cost per unit is determined by dividing the total cost of goods available for sale by the number of units available for sale.

Weighted average cost = [(100,000 × 110)+(200,000 × 100)+(300,000 × 90)]/600,000 = 96.667 yuan/kg

Sales = 520,000 × 240 = 124,800,000 yuan

Cost of sales = 520,000 × 96.667 = 50,267,000 yuan

Gross profit = 124,800,000 − 50,267,000 = 74,533,000 yuan

Ending inventory = 80,000 × 96.667 = 7,733,000 yuan

Solution to 3: Under the FIFO method, the oldest inventory units acquired are assumed to be the first units sold. Ending inventory, therefore, is assumed to consist of those inventory units most recently acquired.

Sales = 520,000 × 240 = 124,800,000 yuan

Cost of sales = (100,000 × 110)+(200,000 × 100)+(220,000 × 90) = 50,800,000 yuan

Gross profit = 124,800,000 − 50,800,000 = 74,000,000 yuan

Ending inventory = 80,000 × 90 = 7,200,000 yuan

Solution to 4: Under the LIFO method, the newest inventory units acquired are assumed to be the first units sold. Ending inventory, therefore, is assumed to consist of the oldest inventory units.

Sales = 520,000 × 240 = 124,800,000 yuan

Cost of sales = (20,000 × 110)+(200,000 × 100)+(300,000 × 90) = 49,200,000 yuan

Gross profit = 124,800,000 − 49,200,000 = 75,600,000 yuan

Ending inventory = 80,000 × 110 = 8,800,000 yuan

The following table (in thousands of yuan) summarizes the cost of sales, the ending inventory, and the cost of goods available for sale that were calculated for each of the four inventory valuation methods. Note that in the first year of operation, the total cost of goods available for sale is the same under all four methods. Subsequently, the cost of goods available for sale will typically differ because beginning inventories will differ. Also shown is the gross profit figure for each of the four methods. Because the cost of a kg of soap declined over the period, LIFO had the highest ending inventory amount, the lowest cost of sales, and the highest gross profit. FIFO had the lowest ending inventory amount, the highest cost of sales, and the lowest gross profit.

3.6. Periodic versus Perpetual Inventory Systems

Companies typically record changes to inventory using either a periodic inventory system or a perpetual inventory system. Under a periodic inventory system, inventory values and costs of sales are determined at the end of an accounting period. Purchases are recorded in a purchases account. The total of purchases and beginning inventory is the amount of goods available for sale during the period. The ending inventory amount is subtracted from the goods available for sale to arrive at the cost of sales. The quantity of goods in ending inventory is usually obtained or verified through a physical count of the units in inventory. Under a perpetual inventory system, inventory values and cost of sales are continuously updated to reflect purchases and sales.

Under either system, the allocation of goods available for sale to cost of sales and ending inventory is the same if the inventory valuation method used is either specific identification or FIFO. This is not generally true for the weighted average cost method. Under a periodic inventory system, the amount of cost of goods available for sale allocated to cost of sales and ending inventory may be quite different using the FIFO method compared to the weighted average cost method. Under a perpetual inventory system, inventory values and cost of sales are continuously updated to reflect purchases and sales. As a result, the amount of cost of goods available for sale allocated to cost of sales and ending inventory is similar under the FIFO and weighted average cost methods. Because of lack of disclosure and the dominance of perpetual inventory systems, analysts typically do not make adjustments when comparing a company using the weighted average cost method with a company using the FIFO method.

Using the LIFO method, the periodic and perpetual inventory systems will generally result in different allocations to cost of sales and ending inventory. Under either a perpetual or periodic inventory system, the use of the LIFO method will generally result in significantly different allocations to cost of sales and ending inventory compared to other inventory valuation methods. When inventory costs are increasing and inventory unit levels are stable or increasing, using the LIFO method will result in higher cost of sales and lower inventory carrying amounts than using the FIFO method. The higher cost of sales under LIFO will result in lower gross profit, operating income, income before taxes, and net income. Income tax expense will be lower under LIFO, causing the company’s net operating cash flow to be higher. On the balance sheet, the lower inventory carrying amount will result in lower reported current assets, working capital, and total assets. Analysts must carefully assess the financial statement implications of the choice of inventory valuation method when comparing companies that use the LIFO method with companies that use the FIFO method.

Example 9-3 illustrates the impact of the choice of system under LIFO.

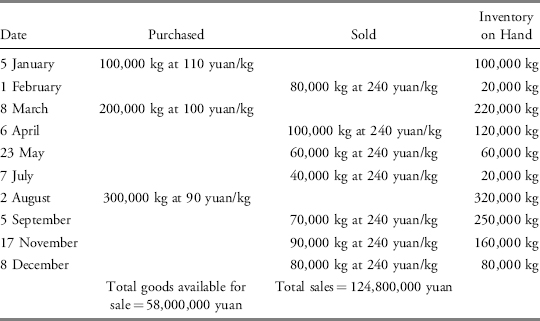

EXAMPLE 9-3 Perpetual versus Periodic Inventory Systems

If GSI (the company in Example 9-2) had used a perpetual inventory system, the timing of purchases and sales would affect the amounts of cost of sales and inventory. Following is a record of the purchases, sales, and quantity of inventory on hand after the transaction in 2009.

The amounts for total goods available for sale and sales are the same under either the perpetual or periodic system in this first year of operation. The carrying amount of the ending inventory, however, may differ because the perpetual system will apply LIFO continuously throughout the year. Under the periodic system, it was assumed that the ending inventory was composed of 80,000 units of the oldest inventory, which cost 110 yuan/kg.

What are the ending inventory, cost of sales, and gross profit amounts using the perpetual system and the LIFO method? How do these compare with the amounts using the periodic system and the LIFO method, as in Example 9-2?

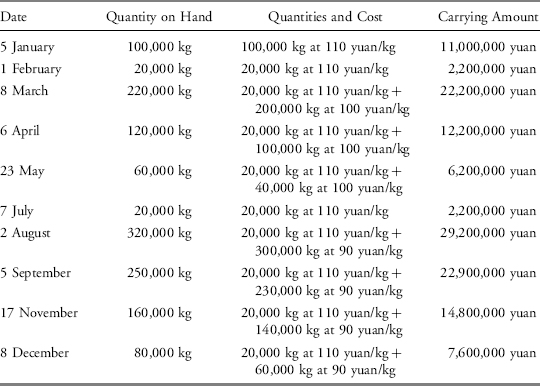

Solution: The carrying amounts of the inventory at the different time points using the perpetual inventory system are as follows:

Perpetual system

Sales = 520,000 × 240 = 124,800,000 yuan

Cost of sales = 58,000,000 − 7,600,000 = 50,400,000 yuan

Gross profit = 124,800,000 − 50,400,000 = 74,400,000 yuan

Ending inventory = 7,600,000 yuan

Periodic system from Example 9-2

Sales = 520,000 × 240 = 124,800,000 yuan

Cost of sales = (20,000 × 110)+(200,000 × 100)+(300,000 × 90) = 49,200,000 yuan

Gross profit = 124,800,000 − 49,200,000 = 75,600,000 yuan

Ending inventory = 80,000 × 110 = 8,800,000 yuan

In this example, the ending inventory amount is lower under the perpetual system because only 20,000 kg of the oldest inventory with the highest cost is assumed to remain in inventory. The cost of sales is higher and the gross profit is lower under the perpetual system compared to the periodic system.

3.7. Comparison of Inventory Valuation Methods

As shown in Example 9-2, the allocation of the total cost of goods available for sale to cost of sales on the income statement and to ending inventory on the balance sheet varies under the different inventory valuation methods. In an environment of declining inventory unit costs and constant or increasing inventory quantities, FIFO (in comparison with weighted average cost or LIFO) will allocate a higher amount of the total cost of goods available for sale to cost of sales on the income statement and a lower amount to ending inventory on the balance sheet. Accordingly, because cost of sales will be higher under FIFO, a company’s gross profit, operating profit, and income before taxes will be lower.

Conversely, in an environment of rising inventory unit costs and constant or increasing inventory quantities, FIFO (in comparison with weighted average cost or LIFO) will allocate a lower amount of the total cost of goods available for sale to cost of sales on the income statement and a higher amount to ending inventory on the balance sheet. Accordingly, because cost of sales will be lower under FIFO, a company’s gross profit, operating profit, and income before taxes will be higher.

The carrying amount of inventories under FIFO will more closely reflect current replacement values because inventories are assumed to consist of the most recently purchased items. The cost of sales under LIFO will more closely reflect current replacement value. LIFO ending inventory amounts are typically not reflective of current replacement value because the ending inventory is assumed to be the oldest inventory and costs are allocated accordingly. Example 9-4 illustrates the different results obtained by using either the FIFO or LIFO methods to account for inventory.

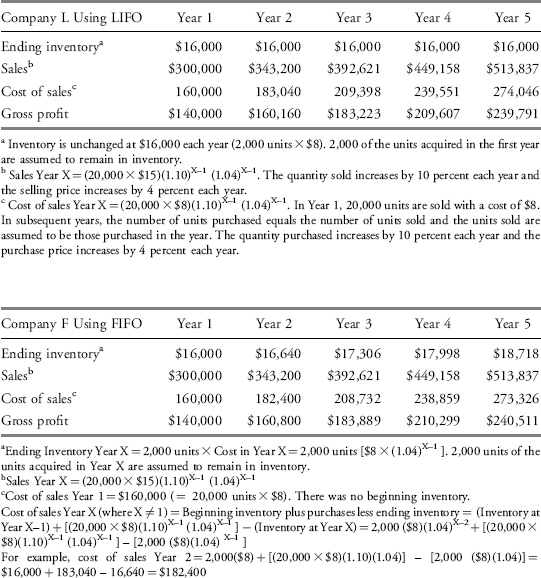

EXAMPLE 9-4 Impact of Inflation Using LIFO Compared to FIFO

Company L and Company F are identical in all respects except that Company L uses the LIFO method and Company F uses the FIFO method. Each company has been in business for five years and maintains a base inventory of 2,000 units each year. Each year, except the first year, the number of units purchased equaled the number of units sold. Over the five year period, unit sales increased 10 percent each year and the unit purchase and selling prices increased at the beginning of each year to reflect inflation of 4 percent per year. In the first year, 20,000 units were sold at a price of $15.00 per unit and the unit purchase price was $8.00.

1. What was the end of year inventory, sales, cost of sales, and gross profit for each company for each of the five years?

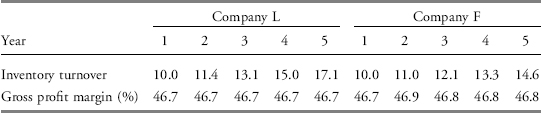

2. Compare the inventory turnover ratios (based on ending inventory carrying amounts) and gross profit margins over the five year period and between companies.

Note that if the company sold more units than it purchased in a year, inventory would decrease. This is referred to as LIFO liquidation. The cost of sales of the units sold in excess of those purchased would reflect the inventory carrying amount. In this example, each unit sold in excess of those purchased would have a cost of sales of $8 and a higher gross profit.

Solution 1:

Solution to 2:

Inventory turnover ratio = Cost of sales ÷ Ending inventory. The inventory turnover ratio increased each year for both companies because the units sold increased, whereas the units in ending inventory remained unchanged. The increase in the inventory turnover ratio is higher for Company L because Company L’s cost of sales is increasing for inflation but the inventory carrying amount is unaffected by inflation. It might appear that a company using the LIFO method manages its inventory more effectively, but this is deceptive. Both companies have identical quantities and prices of purchases and sales and only differ in the inventory valuation method used.

Gross profit margin = Gross profit ÷ Sales. The gross profit margin is stable under LIFO because both sales and cost of sales increase at the same rate of inflation. The gross profit margin is slightly higher under the FIFO method after the first year because a proportion of the cost of sales reflects an older purchase price.

In the United States, the LIFO method is widely used (approximately 36 percent of U.S. companies use the LIFO method). The potential income tax savings are a benefit of using the LIFO method when inventory costs are increasing. The higher cash flows due to lower income taxes may make the company more valuable because the value of a company is based on the present value of its future cash flows. Under the “LIFO conformity rule,” the U.S. tax code requires that companies using the LIFO method for tax purposes must also use the LIFO method for financial reporting. Under the LIFO method, ending inventory is assumed to consist of those units that have been held the longest. This generally results in ending inventories with carrying amounts lower than current replacement costs because inventory costs typically increase over time. Cost of sales will more closely reflect current replacement costs.

If the purchase prices (purchase costs) or production costs of inventory are increasing, the income statement consequences of using the LIFO method compared to other methods will include higher cost of sales, and lower gross profit, operating profit, income tax expense, and net income. The balance sheet consequences include lower ending inventory, working capital, total assets, retained earnings, and shareholders’ equity. The lower income tax paid will result in higher net cash flow from operating activities. Some of the financial ratio effects are a lower current ratio, higher debt-to-equity ratios, and lower profitability ratios.

If the purchase prices or production costs of inventory are decreasing, it is unlikely that a company will use the LIFO method for tax purposes (and therefore for financial reporting purposes due to the LIFO conformity rule) because this will result in lower cost of sales, and higher taxable income and income taxes. However, if the company had elected to use the LIFO method and cannot justify changing the inventory valuation method for tax and financial reporting purposes when inventory costs begin to decrease, the income statement, balance sheet, and ratio effects will be opposite to the effects during a period of increasing costs.

The U.S. Securities Exchange Commission (SEC) has proposed the full adoption of IFRS by all U.S. reporting companies beginning in 2014. An important consequence of this proposal would be the complete elimination of the LIFO inventory method for financial reporting and, due to the LIFO conformity rule, tax reporting by U.S. companies. As a consequence of the restatement of financial statements to the FIFO or weighted average cost method, significant immediate income tax liabilities may arise in the year of transition from the LIFO method to either the FIFO or weighted average cost method.

4.1. LIFO Reserve

For companies using the LIFO method, U.S. GAAP requires disclosure, in the notes to the financial statements or on the balance sheet, of the amount of the LIFO reserve. The LIFO reserve is the difference between the reported LIFO inventory carrying amount and the inventory amount that would have been reported if the FIFO method had been used (in other words, the FIFO inventory value less the LIFO inventory value). The disclosure provides the information that analysts need to adjust a company’s cost of sales (cost of goods sold) and ending inventory balance based on the LIFO method, to the FIFO method.

To compare companies using LIFO with companies not using LIFO, inventory is adjusted by adding the disclosed LIFO reserve to the inventory balance that is reported on the balance sheet. The reported inventory balance, using LIFO, plus the LIFO reserve equals the inventory that would have been reported under FIFO. Cost of sales is adjusted by subtracting the increase in the LIFO reserve during the period from the cost of sales amount that is reported on the income statement. If the LIFO reserve has declined during the period,10 the decrease in the reserve is added to the cost of sales amount that is reported on the income statement. The LIFO reserve disclosure can be used to adjust the financial statements of a U.S. company using the LIFO method to make them comparable with a similar company using the FIFO method.

EXAMPLE 9-5 Inventory Conversion from LIFO to FIFO

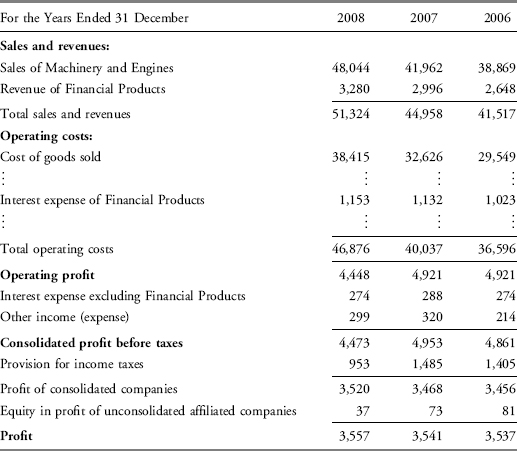

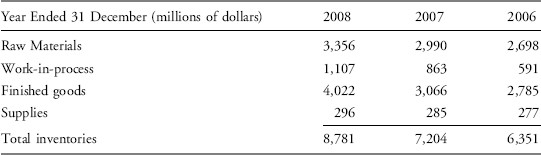

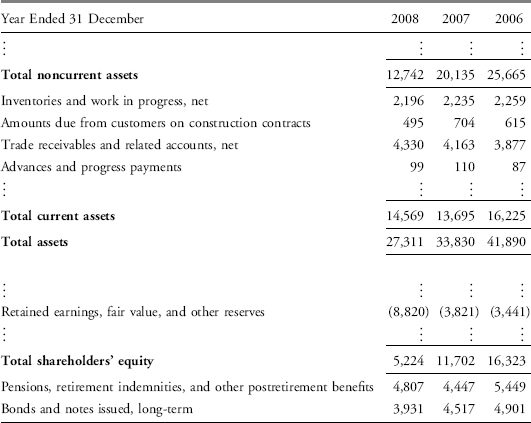

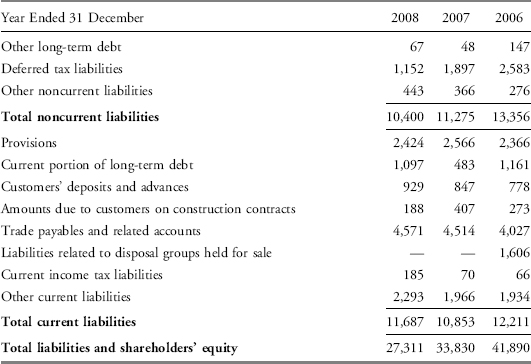

Caterpillar Inc. (NYSE: CAT), based in Peoria, Illinois, USA, is the largest maker of construction and mining equipment, diesel and natural gas engines, and industrial gas turbines in the world. Excerpts from CAT’s consolidated financial statements are shown in Exhibits 9-1 and 9-2; notes pertaining to CAT’s inventories are presented in Exhibit 9-3. Assume tax rates of 20 percent for 2008 and 30 percent for earlier years. The assumed tax rates are based on the provision for taxes as a percentage of consolidated profits before taxes rather than the U.S. corporate statutory tax rate of 35 percent.

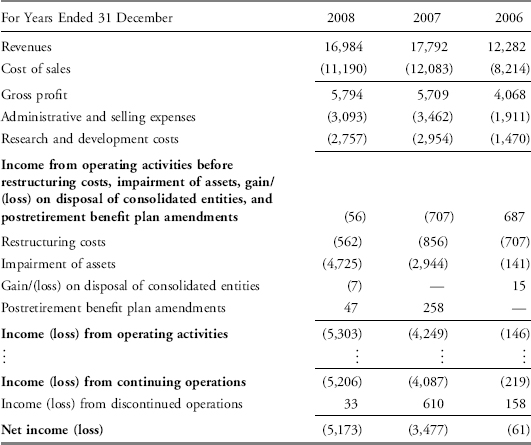

EXHIBIT 9-1 Caterpillar Inc. Consolidated Results of Operation (US$ millions)

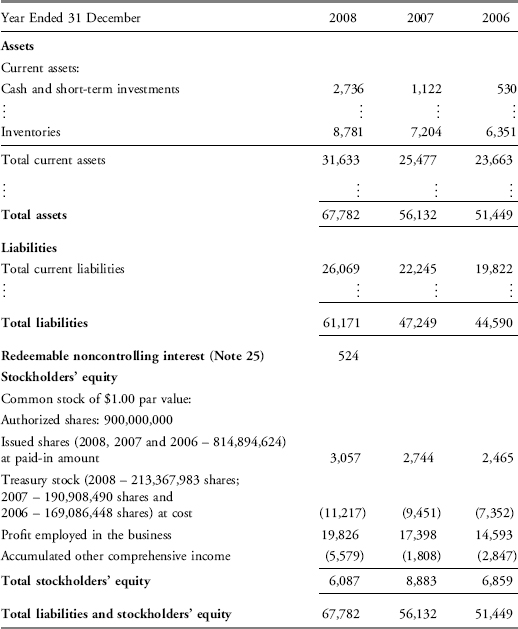

EXHIBIT 9-2 Caterpillar Inc. Consolidated Financial Position (US$ millions)

1. What inventory values would CAT report for 2008, 2007, and 2006 if it had used the FIFO method instead of the LIFO method?

2. What amount would CAT’s cost of goods sold for 2008 and 2007 be if it had used the FIFO method instead of the LIFO method?

3. What net income (profit) would CAT report for 2008 and 2007 if it had used the FIFO method instead of the LIFO method?

4. By what amount would CAT’s 2008 and 2007 net cash flow from operating activities decline if CAT used the FIFO method instead of the LIFO method?

5. What is the cumulative amount of income tax savings that CAT has generated through 2008 by using the LIFO method instead of the FIFO method?

6. What amount would be added to CAT’s retained earnings (profit employed in the business) at 31 December 2008 if CAT had used the FIFO method instead of the LIFO method?

7. What would be the change in Cat’s cash balance if CAT had used the FIFO method instead of the LIFO method?

8. Calculate and compare the following for 2008 under the LIFO method and the FIFO method: inventory turnover ratio, days of inventory on hand, gross profit margin, net profit margin, return on assets, current ratio, and total liabilities-to-equity ratio.

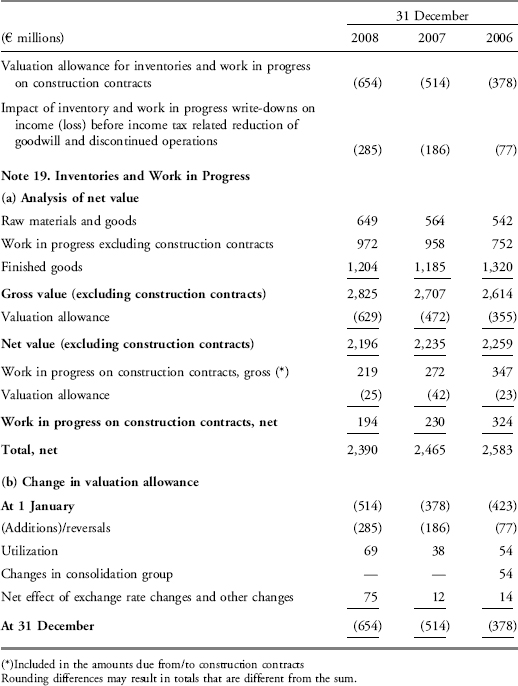

EXHIBIT 9-3 Caterpillar Inc. Selected Notes to Consolidated Financial Statements

Note 1. Operations and Summary of Significant Accounting Policies

D. Inventories

Inventories are stated at the lower of cost or market. Cost is principally determined using the last-in, first-out (LIFO) method. The value of inventories on the LIFO basis represented about 70% of total inventories at December 31, 2008 and about 75% of total inventories at December 31, 2007 and 2006.

If the FIFO (first-in, first-out) method had been in use, inventories would have been $3,183 million, $2,617 million and $2,403 million higher than reported at December 31, 2008, 2007, and 2006, respectively.

Note 9. Inventories

We had long-term material purchase obligations of approximately $363 million at December 31, 2008.

Solution to 1:

Solution to 2:

| 31 December (millions of dollars) | 2008 | 2007 |

| Cost of goods sold (LIFO method) | 38,415 | 32,626 |

| Less: Increase in LIFO reserve* | −566 | −214 |

| Cost of goods sold (FIFO method) | 37,849 | 32,412 |

*From Note 1.D, the increase in LIFO reserve for 2008 is 566 (3,183 − 2,617) and for 2007 is 214 (2,617 − 2,403).

Solution to 3:

| 31 December (millions of dollars) | 2008 | 2007 |

| Net income (LIFO method) | 3,557 | 3,541 |

| Reduction in cost of goods sold (increase in operating profit) | 566 | 214 |

| Taxes on increased operating profit* | *113 | *64 |

| Net income (FIFO method) | 4,010 | 3,691 |

*The taxes on the increased operating profit are assumed to be 113 (566 × 20%) for 2008 and 64 (214 × 30%) for 2007.

Solution to 4: The effect on a company’s net cash flow from operating activities is limited to the impact of the change on income taxes paid; changes in allocating inventory costs to ending inventory and cost of goods sold does not change any cash flows except income taxes. Consequently, the effect of using FIFO on CAT’s net operating cash flow from operating activities would be a decline of $113 million in 2008 and a decline of $64 million in 2007. These are the approximate incremental increases in income taxes that CAT would have incurred if the FIFO method were used instead of the LIFO method (see earlier solution to 3).

Solution to 5: Assuming tax rates of 20 percent for 2008 and 30 percent for earlier years, the cumulative amount of income tax savings that CAT has generated by using the LIFO method instead of FIFO is approximately $898 million (566 × 20%+2,617 × 30%). Note 1.D indicates a LIFO reserve of $2,617 million at the end of 2007 and an increase in the LIFO reserve of $566 million in 2008. Therefore, under the FIFO method, cumulative gross profits would have been $2,617 million higher as of the end of 2007 and an additional $566 million higher as of the end of 2008. The estimated tax savings would be higher (lower) if income tax rates were assumed to be higher (lower).

Solution to 6: The amount that would be added to CAT’s retained earnings is $2,285 million (3,183 − 898) or (566 × 80%+2,617 × 70%). This represents the cumulative increase in operating profit due to the decrease in cost of goods sold (LIFO reserve of $3,183 million) less the assumed taxes on that profit ($898 million, see solution to 5). Some analysts advocate ignoring the tax consequences and suggest simply adjusting inventory and equity by the same amount. They argue that the reported equity of the firm is understated by the difference between the current value of its inventory (approximated by the value under FIFO) and its carrying value (value under LIFO).

Solution to 7: Under the FIFO method, an additional $898 million is assumed to have been incurred for tax expenses. If CAT switched to FIFO, it would have an additional tax liability of $898 million as a consequence of the restatement of financial statements to the FIFO method. This illustrates the significant immediate income tax liabilities that may arise in the year of transition from the LIFO method to the FIFO method. If CAT switched to FIFO for tax purposes, there would be a cash outflow for the additional taxes. However, because the company is not actually converting at this point for either tax or reporting purposes, it is appropriate to reflect a deferred tax liability rather than a reduction in cash. In this case for analysis purposes, under FIFO, inventory would increase by $3,153 million, equity by $2,285 million, and noncurrent liabilities by $898 million.

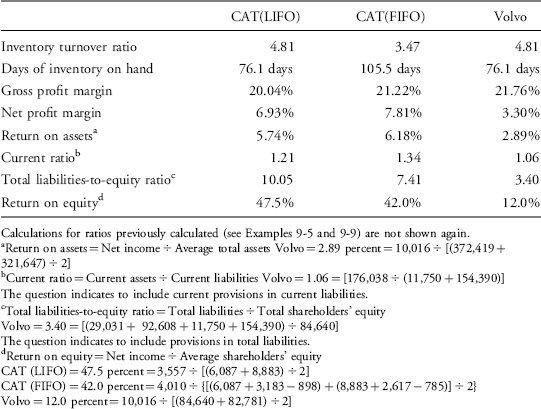

Solution to 8: CAT’s ratios for 2008 under the LIFO and FIFO methods are as follows:

| LIFO | FIFO | |

| Inventory turnover | 4.81 | 3.47 |

| Days of inventory on hand | 76.1 days | 105.5 days |

| Gross profit margin | 20.04% | 21.22% |

| Net profit margin | 6.93% | 7.81% |

| Return on assets | 5.74% | 6.18% |

| Current ratio | 1.21 | 1.34 |

| Total liabilities-to-equity ratio | 10.05 | 7.41 |

Inventory turnover ratio = Cost of goods sold ÷ Average inventory

LIFO = 4.81 = 38,415 ÷ [(8,781+7,204) ÷ 2]

FIFO = 3.47 = 37,849 ÷ [(11,964+9,821) ÷ 2]

The ratio is higher under LIFO because, given rising inventory costs, cost of goods sold will be higher and inventory carrying amounts will be lower under LIFO. If an analyst made no adjustment for the difference in inventory methods, it might appear that a company using the LIFO method manages its inventory more effectively.

Days of inventory on hand = Number of days in period÷Inventory turnover ratio

LIFO = 76.1 days = (366 days* ÷ 4.81)

FIFO = 105.5 days = (366 days ÷ 3.47)

*2008 was a leap year.

Without adjustment, a company using the LIFO method might appear to manage its inventory more effectively. This is primarily the result of the lower inventory carrying amounts under LIFO.

Gross profit margin = Gross profit ÷ Total revenue

LIFO = 20.04 percent = [(48,044 − 38,415) ÷ 48,044]

FIFO = 21.22 percent = [(48,044 − 37,849) ÷ 48,044]

Revenue of financial products is excluded from the calculation of gross profit. Gross profit is sales of machinery and engines less cost of goods sold. The gross profit margin is lower under LIFO because the cost of goods sold is higher given rising inventory costs.

Net profit margin = Net income ÷ Total revenue

LIFO = 6.93 percent = (3,557 ÷ 51,324)

FIFO = 7.81 percent = (4,010 ÷ 51,324)

The net profit margin is lower under LIFO because the cost of goods sold is higher. The absolute percentage difference is less than that of the gross profit margin because of income taxes on the increased income reported under FIFO and because net income is divided by total revenue including sales of machinery and engines and revenue of financial products. The company appears to be less profitable under LIFO.

Return on assets = Net income ÷ Average total assets

LIFO = 5.74 percent = 3,557 ÷ [(67,782+56,132) ÷ 2]

FIFO = 6.18 percent = 4,010 ÷ [(67,782+3,183)+(56,132+2,617) ÷ 2]

The total assets under FIFO are the LIFO total assets increased by the LIFO reserve. The return on assets is lower under LIFO because the lower net income due to the higher cost of goods sold has a greater impact on the ratio than the lower total assets, which are the result of lower inventory carrying amounts. The company appears to be less profitable under LIFO.

Current ratio = Current assets ÷ Current liabilities

LIFO = 1.21 = (31,633 ÷ 26,069)

FIFO = 1.34 = [(31,633+3,183) ÷ 26,069]

The current ratio is lower under LIFO primarily because of lower inventory carrying amount. The company appears to be less liquid under LIFO.

Total liabilities-to-equity ratio = Total liabilities ÷ Total shareholders’ equity

LIFO = 10.05 = (61,171 ÷ 6,087)

FIFO = 7.41 = [(61,171 +898) ÷ (6,087+2,285)]

The ratio is higher under LIFO because the addition to retained earnings under FIFO reduces the ratio. The company appears to be more highly leveraged under LIFO.

In summary, the company appears to be less profitable, less liquid, and more highly leveraged under LIFO. Yet, because a company’s value is based on the present value of future cash flows, LIFO will increase the company’s value because the cash flows are higher in earlier years due to lower taxes. LIFO is primarily used for the tax benefits it provides.

4.2. LIFO Liquidations

In periods of rising inventory unit costs, the carrying amount of inventory under FIFO will always exceed the carrying amount of inventory under LIFO. The LIFO reserve may increase over time as the result of the increasing difference between the older costs used to value inventory under LIFO and the more recent costs used to value inventory under FIFO. Also, when the number of inventory units manufactured or purchased exceeds the number of units sold, the LIFO reserve may increase as the result of the addition of new LIFO layers (the quantity of inventory units is increasing and each increase in quantity creates a new LIFO layer).

When the number of units sold exceeds the number of units purchased or manufactured, the number of units in ending inventory is lower than the number of units in beginning inventory and a company using LIFO will experience a LIFO liquidation (some of the older units held in inventory are assumed to have been sold). If inventory unit costs have been rising from period to period and LIFO liquidation occurs, this will produce an inventory-related increase in gross profits. The increase in gross profits occurs because of the lower inventory carrying amounts of the liquidated units. The lower inventory carrying amounts are used for cost of sales and the sales are at the current prices. The gross profit on these units is higher than the gross profit that would be recognized using more current costs. These inventory profits caused by a LIFO liquidation, however, are one-time events and are not sustainable.

LIFO liquidations can occur for a variety of reasons. The reduction in inventory levels may be outside of management’s control; for example, labor strikes at a supplier may force a company to reduce inventory levels to meet customer demands. In periods of economic recession or when customer demand is declining, a company may choose to reduce existing inventory levels rather than invest in new inventory. Analysts should be aware that management can potentially manipulate and inflate their company’s reported gross profits and net income at critical times by intentionally reducing inventory quantities and liquidating older layers of LIFO inventory (selling some units of beginning inventory). During economic downturns, LIFO liquidation may result in higher gross profit than would otherwise be realized. If LIFO layers of inventory are temporarily depleted and not replaced by fiscal year-end, LIFO liquidation will occur resulting in unsustainable higher gross profits. Therefore, it is imperative to review the LIFO reserve footnote disclosures to determine if LIFO liquidation has occurred. A decline in the LIFO reserve from the prior period may be indicative of LIFO liquidation.

EXAMPLE 9-6 LIFO Liquidation: Financial Statement Impact and Disclosure

The following excerpts are from the 2007 10-K of Sturm Ruger & Co., Inc. (NYSE:RGR):

Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations

“Reduction in inventory generated positive cash flow for the Company, partially offset by the tax impact of the consequent LIFO liquidation, which generated negative cash flow as it created taxable income, resulting in higher tax payments.”

Balance Sheets

| Year Ended December 31 (In thousands, except per share data) | 2007 | 2006 |

| Assets | ||

| Current Assets | ||

| ⋮ | ⋮ | ⋮ |

| Gross inventories: Less LIFO reserve Less excess and obsolescence reserve |

64,330 (46,890) (4,143) |

87,477 (57,555) (5,516) |

| Net inventories | 13,297 | 24,406 |

| ⋮ | ⋮ | ⋮ |

| Total Current Assets | 73,512 | 81,785 |

| ⋮ | ⋮ | ⋮ |

| Total Assets | $101,882 | $117,066 |

Statements of Income

| Year Ended December 31(In thousands, except per share data) | 2007 | 2006 |

| ⋮ | ⋮ | ⋮ |

| Total net sales | 156,485 | 167,620 |

| Cost of products sold | 117,186 | 139,610 |

| Gross profit | 39,299 | 28,010 |

| Expenses: | ||

| ⋮ | ⋮ | ⋮ |

| Total expenses | 30,184 | 27,088 |

| Operating income | 9,115 | 922 |

| ⋮ | ⋮ | ⋮ |

| Total other income, net | 7,544 | 921 |

| Income before income taxes | 16,659 | 1,843 |

| Income taxes | 6,330 | 739 |

| Net income | $10,329 | $1,104 |

| Basic and Diluted Earnings Per Share | $0.46 | $0.04 |

| Cash Dividends Per Share | $0.00 | $0.00 |

Notes to Financial Statements

1. Significant Accounting Policies

⋮

Inventories

Inventories are stated at the lower of cost, principally determined by the last-in, first-out (LIFO) method, or market. If inventories had been valued using the first-in, first-out method, inventory values would have been higher by approximately $46.9 million and $57.6 million at December 31, 2007 and 2006, respectively. During 2007 and 2006, inventory quantities were reduced. This reduction resulted in a liquidation of LIFO inventory quantities carried at lower costs prevailing in prior years as compared with the current cost of purchases, the effect of which decreased costs of products sold by approximately $12.1 million and $7.1 million in 2007 and 2006, respectively. There was no LIFO liquidation in 2005.

1. What is the decrease in the LIFO reserve on the balance sheet? How much less was the cost of products sold in 2007, because of LIFO liquidation, according to the note disclosure?

2. How did the decreased cost of products sold compare to operating income in 2007?

3. How did the LIFO liquidation affect cash flows?

Solution to 1: The LIFO reserve decreased by $10,665 thousands (57,555 − 46,890) in 2007. The LIFO liquidation decreased costs of products sold by approximately $12.1 million in 2007. The decrease in the LIFO reserve is indicative of a LIFO liquidation but is not sufficient to determine the exact amount of the LIFO liquidation.

Solution to 2: The decreased cost of products sold of approximately $12.1 million exceeds the operating income of approximately $9 million.

Solution to 3: The LIFO liquidation (reduction in inventory) generated positive cash flow. The positive cash flow effect of the LIFO liquidation was reduced by its tax impact. The LIFO liquidation resulted in higher taxable income and higher tax payments.

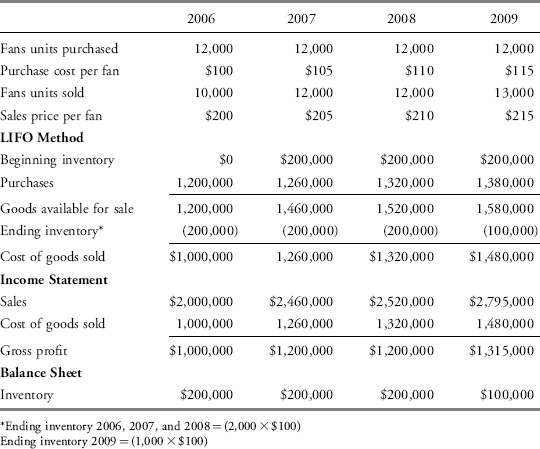

EXAMPLE 9-7 LIFO Liquidation Illustration

Reliable Fans, Inc. (RF), a hypothetical company, sells high quality fans and has been in business since 2006. Exhibit 9-4 provides relevant data and financial statement information about RF’s inventory purchases and sales of fan inventory for the years 2006 through 2009. RF uses the LIFO method and a periodic inventory system. What amount of RF’s 2009 gross profit is due to LIFO liquidation?

EXHIBIT 9-4 RF Financial Statement Information under LIFO

Solution: RF’s reported gross profit for 2009 is $1,315,000. RF’s 2009 gross profit due to LIFO liquidation is $15,000. If RF had purchased 13,000 fans in 2009 rather than 12,000 fans, the cost of goods sold under the LIFO method would have been $1,495,000 (13,000 fans sold at $115.00 purchase cost per fan), and the reported gross profit would have been $1,300,000 ($2,795,000 less $1,495,000). The gross profit due to LIFO liquidation is $15,000 ($1,315,000 reported gross profit less the $1,300,000 gross profit that would have been reported without the LIFO liquidation). The gross profit due to LIFO liquidation may also be determined by multiplying the number of units liquidated times the difference between the replacement cost of the units liquidated and their historical purchase cost. For RF, 1,000 units times $15 ($115 replacement cost per fan less the $100 historical cost per fan) equals the $15,000 gross profit due to LIFO liquidation.

Companies on rare occasion change inventory valuation methods. Under IFRS, a change in method is acceptable only if the change “results in the financial statements providing reliable and more relevant information about the effects of transactions, other events, or conditions on the business entity’s financial position, financial performance, or cash flows.”11 If the change is justifiable, then it is applied retrospectively.

This means that the change is applied to comparative information for prior periods as far back as is practicable. The cumulative amount of the adjustments relating to periods prior to those presented in the current financial statements is made to the opening balance of each affected component of equity (i.e., retained earnings or comprehensive income) of the earliest period presented. For example, if a company changes its inventory method in 2009 and it presents three years of comparative financial statements (2007, 2008, and 2009) in its annual report, it would retrospectively reflect this change as far back as possible. The change would be reflected in the three years of financial statements presented; the financial statements for 2007 and 2008 would be restated as if the new method had been used in these periods, and the cumulative effect of the change on periods prior to 2007 would be reflected in the 2007 opening balance of each affected component of equity. An exemption to the restatement applies when it is impracticable to determine either the period-specific effects or the cumulative effect of the change.

Under U.S. GAAP, the conditions to make a change in accounting policy and the accounting for a change in inventory policy are similar to IFRS.12 U.S. GAAP, however, requires companies to thoroughly explain why the newly adopted inventory accounting method is superior and preferable to the old method. If a company decides to change from LIFO to another inventory method, U.S. GAAP requires a retrospective restatement as described earlier. However, if a company decides to change to the LIFO method, it must do so on a prospective basis and retrospective adjustments are not made to the financial statements. The carrying amount of inventory under the old method becomes the initial LIFO layer in the year of LIFO adoption.

Analysts should carefully evaluate changes in inventory valuation methods. Although the stated reason for the inventory change may be to better match inventory costs with sales revenue (or some other plausible business explanation), the real underlying (and unstated) purpose may be to reduce income tax expense (if changing to LIFO from FIFO or average cost), or to increase reported profits (if changing from LIFO to FIFO or average cost). As always, the choice of inventory valuation method can have a significant impact on financial statements and the financial ratios that are derived from them. As a consequence, analysts must carefully consider the impact of the change in inventory valuation methods and the differences in inventory valuation methods when comparing a company’s performance with that of its industry or its competitors.

Significant financial risk can result from the holding of inventory. The cost of inventory may not be recoverable due to spoilage, obsolescence, or declines in selling prices. IFRS state that inventories shall be measured (and carried on the balance sheet) at the lower of cost and net realizable value.13 Net realizable value is the estimated selling price in the ordinary course of business less the estimated costs necessary to make the sale and estimated costs to get the inventory in condition for sale. The assessment of net realizable value is typically done item by item or by groups of similar or related items. In the event that the value of inventory declines below the carrying amount on the balance sheet, the inventory carrying amount must be written down to its net realizable value14 and the loss (reduction in value) recognized as an expense on the income statement. This expense may be included as part of cost of sales or reported separately.

In each subsequent period, a new assessment of net realizable value is made. Reversal (limited to the amount of the original write-down) is required for a subsequent increase in value of inventory previously written down. The reversal of any write-down of inventories is recognized as a reduction in cost of sales (reduction in the amount of inventories recognized as an expense).

U.S. GAAP specify the lower of cost or market to value inventories.15 This is broadly consistent with IFRS with one major difference: U.S. GAAP prohibit the reversal of write-downs. Market value is defined as current replacement cost subject to upper and lower limits. Market value cannot exceed net realizable value (selling price less reasonably estimated costs of completion and disposal). The lower limit of market value is net realizable value less a normal profit margin. Any write-down reduces the value of the inventory, and the loss in value (expense) is generally reflected in the income statement in cost of goods sold.

An inventory write-down reduces both profit and the carrying amount of inventory on the balance sheet and thus has a negative effect on profitability, liquidity, and solvency ratios. However, activity ratios (for example, inventory turnover and total asset turnover) will be positively affected by a write-down because the asset base (denominator) is reduced. The negative impact on some key ratios, due to the decrease in profit, may result in the reluctance by some companies to record inventory write-downs unless there is strong evidence that the decline in the value of inventory is permanent. This is especially true under U.S. GAAP where reversal of a write-down is prohibited.

IAS 2 [Inventories] does not apply to the inventories of producers of agricultural and forest products and minerals and mineral products, nor to commodity broker–traders. These inventories may be measured at net realizable value (fair value less costs to sell and complete) according to well-established industry practices. If an active market exists for these products, the quoted market price in that market is the appropriate basis for determining the fair value of that asset. If an active market does not exist, a company may use market determined prices or values (such as the most recent market transaction price) when available for determining fair value. Changes in the value of inventory (increase or decrease) are recognized in profit or loss in the period of the change. U.S. GAAP is similar to IFRS in its treatment of inventories of agricultural and forest products and mineral ores. Mark-to-market inventory accounting is allowed for bullion.

EXAMPLE 9-8 Accounting for Declines and Recoveries of Inventory Value

Acme Enterprises, a hypothetical company, manufactures computers and prepares its financial statements in accordance with IFRS. In 2008, the cost of ending inventory was €5.2 million but its net realizable value was €4.9 million. The current replacement cost of the inventory is €4.7 million. This figure exceeds the net realizable value less a normal profit margin. In 2009, the net realizable value of Acme’s inventory was €0.5 million greater than the carrying amount.

1. What was the effect of the write-down on Acme’s 2008 financial statements? What was the effect of the recovery on Acme’s 2009 financial statements?

2. Under U.S. GAAP, what would be the effects of the write-down on Acme’s 2008 financial statements and of the recovery on Acme’s 2009 financial statements?

3. What would be the effect of the recovery on Acme’s 2009 financial statements if Acme’s inventory were agricultural products instead of computers?

Solution to 1: For 2008, Acme would write its inventory down to €4.9 million and record the change in value of €0.3 million as an expense on the income statement. For 2009, Acme would increase the carrying amount of its inventory and reduce the cost of sales by €0.3 million (the recovery is limited to the amount of the original write-down).

Solution to 2: Under U.S. GAAP, for 2008, Acme would write its inventory down to €4.7 million and typically include the change in value of €0.5 million in cost of goods sold on the income statement. For 2009, Acme would not reverse the write-down.

Solution to 3: If Acme’s inventory were agricultural products instead of computers, inventory would be measured at net realizable value and Acme would, therefore, increase inventory by and record a gain of €0.5 million for 2009.

Analysts should consider the possibility of an inventory write-down because the impact on a company’s financial ratios may be substantial. The potential for inventory write-downs can be high for companies in industries where technological obsolescence of inventories is a significant risk. Analysts should carefully evaluate prospective inventory impairments (as well as other potential asset impairments) and their potential effects on the financial ratios when debt covenants include financial ratio requirements. The breaching of debt covenants can have a significant impact on a company.

Companies that use specific identification, weighted average cost, or FIFO methods are more likely to incur inventory write-downs than companies that use the LIFO method. Under the LIFO method, the oldest costs are reflected in the inventory carrying amount on the balance sheet. Given increasing inventory costs, the inventory carrying amounts under the LIFO method are already conservatively presented at the oldest and lowest costs. Thus, it is far less likely that inventory write-downs will occur under LIFO—and if a write-down does occur, it is likely to be of a lesser magnitude.

EXAMPLE 9-9 Effect of Inventory Write-Downs on Financial Ratios

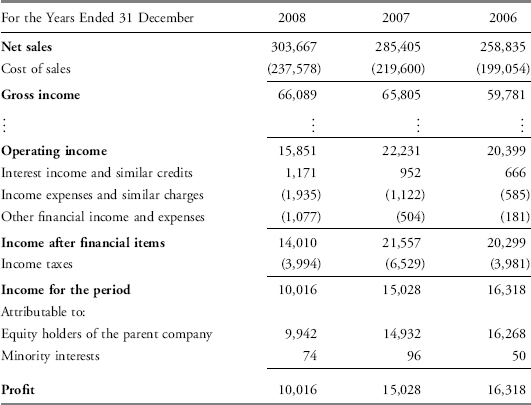

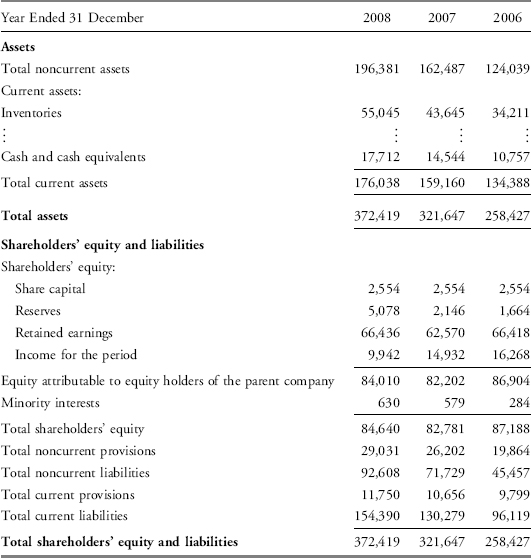

The Volvo Group (OMX Nordic Exchange: VOLV B), based in Göteborg, Sweden, is a leading supplier of commercial transport products such as construction equipment, trucks, buses, and drive systems for marine and industrial applications as well as aircraft engine components.16 Excerpts from Volvo’s consolidated financial statements are shown in Exhibits 9-5 and 9-6. Notes pertaining to Volvo’s inventories are presented in Exhibit 9-7.

EXHIBIT 9-5 Volvo Group Consolidated Income Statements (Swedish Krona in millions, except per share data)

EXHIBIT 9-6 Volvo Group Consolidated Balance Sheets (Swedish Krona in millions)

1. What inventory values would Volvo have reported for 2008, 2007, and 2006 if it had no allowance for inventory obsolescence?

2. Assuming that any changes to the allowance for inventory obsolescence are reflected in the cost of sales, what amount would Volvo’s cost of sales be for 2008 and 2007 if it had not recorded inventory write-downs in 2008 and 2007?

3. What amount would Volvo’s profit (net income) be for 2008 and 2007 if it had not recorded inventory write-downs in 2008 and 2007? Assume tax rates of 28.5 percent for 2008 and 30 percent for 2007.

4. What would Volvo’s 2008 profit (net income) have been if it had reversed all past inventory write-downs in 2008? This question is independent of 1, 2, and 3. Assume a tax rate of 28.5 percent for 2008.

5. Compare the following for 2008 based on the numbers as reported and those assuming no allowance for inventory obsolescence as in questions 1, 2, and 3: inventory turnover ratio, days of inventory on hand, gross profit margin, and net profit margin.

6. CAT (Example 9-5) has no disclosures indicative of either inventory write-downs or a cumulative allowance for inventory obsolescence in its 2008 financial statements. Provide a conceptual explanation as to why Volvo incurred inventory write-downs for 2008 but CAT did not.

EXHIBIT 9-7 Volvo Group Selected Notes to Consolidated Financial Statements

NOTE 1. ACCOUNTING PRINCIPLES

Inventories

Inventories are reported at the lower of cost, in accordance with the first-in, first-out method (FIFO), or net realizable value. The acquisition value is based on the standard cost method, including costs for all direct manufacturing expenses and the apportionable share of the capacity and other related manufacturing costs. The standard costs are tested regularly and adjustments are made based on current conditions. Costs for research and development, selling, administration and financial expenses are not included. Net realizable value is calculated as the selling price less costs attributable to the sale.

NOTE 2. KEY SOURCES OF ESTIMATION UNCERTAINTY

Inventory obsolescence

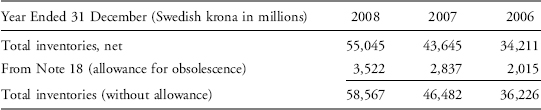

Inventories are reported at the lower of cost, in accordance with the first-in, first-out method (FIFO), or net realizable value. The estimated net realizable value includes management consideration of outdated articles, overstocking, physical damages, inventory-lead-time, handling and other selling costs. If the estimated net realizable value is lower than cost, a valuation allowance is established for inventory obsolescence. The total inventory value, net of inventory obsolescence allowance, is per 31 December 2008, SEK (in millions) 55,045.

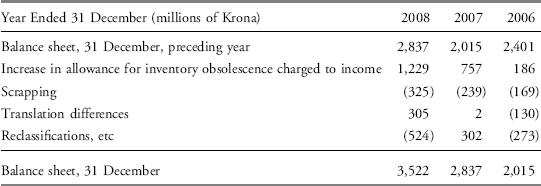

NOTE 18. INVENTORIES

Increase (decrease) in allowance for inventory obsolescence

Solution to 1:

Solution to 2:

| Year Ended 31 December (Swedish krona in millions) | 2008 | 2007 |

| Cost of sales | 237,578 | 219,600 |

| Less: Increase in allowance for obsolescence* | −685 | −822 |

| Cost of sales (without allowance) | 236,893 | 218,778 |

*From Note 18, the increase in allowance for obsolescence for 2008 is 685 (3,522 − 2,837) and for 2007 is 822 (2,837 − 2,015).

Solution to 3:

| Year Ended 31 December (Swedish krona in millions) | 2008 | 2007 |

| Profit (net income) | 10,016 | 15,028 |

| Reduction in cost of sales (increase in operating profit) | 685 | 822 |

| Taxes on increased operating profit* | −195 | −247 |

| Profit (without allowance) | 10,506 | 15,603 |

*Taxes on the increased operating profit are assumed to be 195 (685 × 28.5%) for 2008 and 247 (822 × 30%) for 2007.

Solution to 4:

| Year Ended 31 December (Swedish krona in millions) | 2008 |

| Profit (net income) | 10,016 |

| Reduction in cost of sales (increase in operating profit) | 3,522 |

| Taxes on increased operating profit* | −1,004 |

| Profit (after recovery of previous write-downs) | 12,534 |

*Taxes on the increased operating profit are assumed to be 1,004 (3,522 × 28.5%) for 2008.

Solution to 5: The Volvo Group’s financial ratios for 2008 with the allowance for inventory obsolescence and without the allowance for inventory obsolescence are as follows:

| With Allowance (as Reported) | Without Allowance (Adjusted) | |

| Inventory turnover ratio | 4.81 | 4.51 |

| Days of inventory on hand | 76.1 | 81.2 |

| Gross profit margin | 21.76% | 21.99% |

| Net profit margin | 3.30% | 3.46% |

Inventory turnover ratio = Cost of sales÷Average inventory

With allowance (as reported) = 4.81 = 237,578÷[(55,045+43,645)÷2]

Without allowance (adjusted) = 4.51 = 236,893÷[(58,567+46,482)÷2]

Inventory turnover is higher based on the numbers as reported because cost of sales will be higher (assuming inventory write-downs are reported as part of cost of sales) and inventory carrying amounts will be lower with an allowance for inventory obsolescence. The company appears to manage its inventory more efficiently when it has inventory write-downs.

Days of inventory on hand = Number of days in period÷Inventory turnover ratio

With allowance (as reported) = 76.1 days = (366 days* ÷4.81)

Without allowance (adjusted) = 81.2 days = (366 days÷4.51)

*2008 was a leap year.

Days of inventory on hand are lower based on the numbers as reported because the inventory turnover is higher. A company with inventory write-downs might appear to manage its inventory more effectively. This is primarily the result of the lower inventory carrying amounts.

Gross profit margin = Gross income÷Net sales

With allowance (as reported) = 21.76 percent = (66,089÷303,667)

Without allowance (adjusted) = 21.99 percent = [(66,089+685)÷303,667]

The gross profit margin is lower with inventory write-downs because the cost of sales is higher. This assumes that inventory write-downs are reported as part of cost of sales.

Net profit margin = Profit÷Net sales

With allowance (as reported) = 3.30 percent = (10,016÷303,667)

Without allowance (adjusted) = 3.46 percent = (10,506÷303,667)

The net profit margin is lower with inventory write-downs because the cost of sales is higher (assuming the inventory write-downs are reported as part of cost of sales). The absolute percentage difference is less than that of the gross profit margin because of income taxes on the increased income without write-downs.

The profitability ratios (gross profit margin and net profit margin) for Volvo Group would have been slightly better (higher) for 2008 if the company had not recorded inventory write-downs. The activity ratio (inventory turnover ratio) would appear less attractive without the write-downs. The inventory turnover ratio is slightly better (higher) with inventory write-downs because inventory write-downs increase cost of sales (numerator) and decrease the average inventory (denominator), making inventory management appear more efficient with write-downs.

Solution to 6: CAT uses the LIFO method whereas Volvo uses the FIFO method. Given increasing inventory costs, companies that use the FIFO inventory method are far more likely to incur inventory write-downs than those companies that use the LIFO method. This is because under the LIFO method, the inventory carrying amounts reflect the oldest costs and therefore the lowest costs given increasing inventory costs. Because inventory carrying amounts under the LIFO method are already conservatively presented, it is less likely that inventory write-downs will occur.

7. EVALUATION OF INVENTORY MANAGEMENT

The choice of inventory valuation method impacts the financial statements. The financial statement items impacted include cost of sales, gross profit, net income, inventories, current assets, and total assets. Therefore, the choice of inventory valuation method also affects financial ratios that contain these items. Ratios such as current ratio, return on assets, gross profit margin, and inventory turnover are impacted. As a consequence, analysts must carefully consider inventory valuation method differences when evaluating a company’s performance over time or when comparing its performance with the performance of the industry or industry competitors. Additionally, the financial statement items and ratios may be impacted by adjustments of inventory carrying amounts to net realizable value or current replacement cost.

7.1. Presentation and Disclosure

Disclosures are useful when analyzing a company. IFRS require the following financial statement disclosures concerning inventory:

a. The accounting policies adopted in measuring inventories, including the cost formula (inventory valuation method) used.

b. The total carrying amount of inventories and the carrying amount in classifications (for example, merchandise, raw materials, production supplies, work in progress, and finished goods) appropriate to the entity.

c. The carrying amount of inventories carried at fair value less costs to sell.

d. The amount of inventories recognized as an expense during the period (cost of sales).

e. The amount of any write-down of inventories recognized as an expense in the period.

f. The amount of any reversal of any write-down that is recognized as a reduction in cost of sales in the period.

g. The circumstances or events that led to the reversal of a write-down of inventories.

h. The carrying amount of inventories pledged as security for liabilities.

Inventory-related disclosures under U.S. GAAP are very similar to the disclosures cited earlier, except that requirements (f) and (g) are not relevant because U.S. GAAP do not permit the reversal of prior-year inventory write-downs. U.S. GAAP also require disclosure of significant estimates applicable to inventories and of any material amount of income resulting from the liquidation of LIFO inventory.

7.2. Inventory Ratios

Three ratios often used to evaluate the efficiency and effectiveness of inventory management are inventory turnover, days of inventory on hand, and gross profit margin.17 These ratios are directly impacted by a company’s choice of inventory valuation method. Analysts should be aware, however, that many other ratios are also affected by the choice of inventory valuation method, although less directly. These include the current ratio, because inventory is a component of current assets; the return-on-assets ratio, because cost of sales is a key component in deriving net income and inventory is a component of total assets; and even the debt-to-equity ratio, because the cumulative measured net income from the inception of a business is an aggregate component of retained earnings.

The inventory turnover ratio measures the number of times during the year a company sells (i.e., turns over) its inventory. The higher the turnover ratio, the more times that inventory is sold during the year and the lower the relative investment of resources in inventory. Days of inventory on hand can be calculated as days in the period divided by inventory turnover. Thus, inventory turnover and days of inventory on hand are inversely related. It may be that inventory turnover, however, is calculated using average inventory in the year whereas days of inventory on hand is based on the ending inventory amount. In general, inventory turnover and the number of days of inventory on hand should be benchmarked against industry norms and compared across years.

A high inventory turnover ratio and a low number of days of inventory on hand might indicate highly effective inventory management. Alternatively, a high inventory ratio and a low number of days of inventory on hand could indicate that the company does not carry an adequate amount of inventory or that the company has written down inventory values. Inventory shortages could potentially result in lost sales or production problems in the case of the raw materials inventory of a manufacturer. To assess which explanation is more likely, analysts can compare the company’s inventory turnover and sales growth rate with those of the industry and review financial statement disclosures. Slower growth combined with higher inventory turnover could indicate inadequate inventory levels. Write-downs of inventory could reflect poor inventory management. Minimal write-downs and sales growth rates at or above the industry’s growth rates would support the interpretation that the higher turnover reflects greater efficiency in managing inventory.

A low inventory turnover ratio and a high number of days of inventory on hand relative to industry norms could be an indicator of slow-moving or obsolete inventory. Again, comparing the company’s sales growth across years and with the industry and reviewing financial statement disclosures can provide additional insight.

The gross profit margin, the ratio of gross profit to sales, indicates the percentage of sales being contributed to net income as opposed to covering the cost of sales. Firms in highly competitive industries generally have lower gross profit margins than firms in industries with fewer competitors. A company’s gross profit margin may be a function of its type of product. A company selling luxury products will generally have higher gross profit margins than a company selling staple products. The inventory turnover of the company selling luxury products, however, is likely to be much lower than the inventory turnover of the company selling staple products.

7.3. Financial Analysis Illustrations

IFRS and U.S. GAAP require companies to disclose, either on the balance sheet or in the notes to the financial statements, the carrying amounts of inventories in classifications suitable to the company. For manufacturing companies, these classifications might include production supplies, raw materials, work in progress, and finished goods. For a retailer, these classifications might include significant categories of merchandise or the grouping of inventories with similar attributes. These disclosures may provide signals about a company’s future sales and profits.

For example, a significant increase (attributable to increases in unit volume rather than increases in unit cost) in raw materials and/or work-in-progress inventories may signal that the company expects an increase in demand for its products. This suggests an anticipated increase in sales and profit. However, a substantial increase in finished goods inventories while raw materials and work-in-progress inventories are declining may signal a decrease in demand for the company’s products and hence lower future sales and profit. This may also signal a potential future write-down of finished goods inventory. Irrespective of the signal, an analyst should thoroughly investigate the underlying reasons for any significant changes in a company’s raw materials, work-in-progress, and finished goods inventories.

Analysts also should compare the growth rate of a company’s sales to the growth rate of its finished goods inventories, because this could also provide a signal about future sales and profits. For example, if the growth of inventories is greater than the growth of sales, this could indicate a decline in demand and a decrease in future earnings. The company may have to lower (mark down) the selling price of its products to reduce its inventory balances, or it may have to write down the value of its inventory because of obsolescence, both of which would negatively affect profits. Besides the potential for mark-downs or write-downs, having too much inventory on hand or the wrong type of inventory can have a negative financial effect on a company because it increases inventory-related expenses such as insurance, storage costs, and taxes. In addition, it means that the company has less cash and working capital available to use for other purposes.

Inventory write-downs may have a substantial impact on a company’s activity, profitability, liquidity, and solvency ratios. It is critical for the analyst to be aware of industry trends toward product obsolescence and to analyze the financial ratios for their sensitivity to potential inventory impairment. Companies can minimize the impact of inventory write-downs by better matching their inventory composition and growth with prospective customer demand. To obtain additional information about a company’s inventory and its future sales, a variety of sources of information are available. Analysts should consider the management’s discussion and analysis (MD&A) or similar sections of the company’s financial reports, industry-related news and publications, and industry economic data.

When conducting comparisons, differences in the choice of inventory valuation method can significantly affect the comparability of financial ratios between companies. A restatement from the LIFO method to the FIFO method is critical to make a valid comparison with companies using a method other than the LIFO method such as those companies reporting under IFRS. Analysts should seek out as much information as feasible when analyzing the performance of companies.

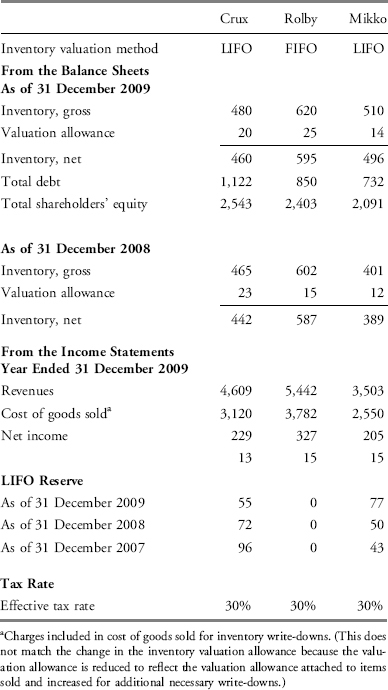

EXAMPLE 9-10 Comparative Illustration