CHAPTER 14

INTERCORPORATE INVESTMENTS

After completing this chapter, you will be able to do the following:

- Describe the classification, measurement, and disclosure under International Financial Reporting Standards (IFRS) for (1) investments in financial assets, (2) investments in associates, (3) joint ventures, (4) business combinations, and (5) special purpose and variable interest entities.

- Distinguish between IFRS and U.S. GAAP in the classification, measurement, and disclosure of investments in financial assets, investments in associates, joint ventures, business combinations, and special purpose and variable interest entities.

- Analyze effects on financial statements and ratios of different methods used to account for intercorporate investments.

Intercorporate investments can have a significant impact on the investing entity’s financial performance and position. Companies invest in the debt and equity securities of other companies to diversify their asset base, enter new markets, obtain competitive advantages, and achieve additional profitability. Debt securities include commercial paper, corporate and government bonds and notes, redeemable preferred stock, and asset-backed securities. Equity securities include common stock and nonredeemable preferred stock. The percentage of equity ownership a company acquires in an investee depends on the resources available, the ability to acquire the shares, and the desired level of influence or control.

The accounting standards that apply to the classification, measurement, and disclosure of intercorporate investments are increasingly reflective of a joint project undertaken by the International Accounting Standards Board (IASB) and the U.S. Financial Accounting Standards Board (FASB). The objective of this project is to remove differences between the sets of standards and to converge on a set of high-quality standards. The IASB and the FASB have issued a series of pronouncements that focus on the measurement, classification, and disclosure of intercorporate investments. These pronouncements have reduced differences between the two accounting standards and have improved the relevance, transparency, and comparability of information provided in financial statements.

As examples of the movement towards convergence, in December 2007 the FASB issued two new standards: SFAS 141(R), Business Combinations,1 and SFAS 160, Noncontrolling Interests in Consolidated Financial Statements.2 These statements introduced significant changes in the accounting for and reporting of business acquisitions and noncontrolling interests in a subsidiary. Both apply to business combinations occurring on or after 15 December 2008, with early adoption prohibited. In January 2008, the IASB revised IFRS 3, Business Combinations and amended IAS 27, Consolidated and Separate Financial Statements. These new requirements became effective on 1 July 2009, although entities were permitted to adopt them earlier. This reading includes accounting standards issued by IASB and FASB through 31 December 2009. Thus, the references for U.S. GAAP are typically those of the FASB Accounting Standards Codification™ (FASB ASC).

Although convergence between IFRS and U.S. GAAP is occurring and accounting is the same or similar for many transactions, differences still remain. In the case of differences, there is generally enough transparency in the disclosures to allow financial statement users to adjust for the differences. Understanding the appropriate accounting treatment for different intercorporate investments and the similarities and differences that exist between IFRS and U.S. GAAP will enable analysts to make better comparisons between companies and improve investment decision making. The terminology used in this reading is IFRS oriented. U.S. GAAP may not use identical terminology but in most cases, the terminology is similar.

This reading is organized as follows: Section 2 explains the basic categorization of corporate investments. Section 3 describes reporting for investments in financial assets; in this reading, financial assets are limited to debt and equity securities of other entities. Section 4 describes reporting for investments in associates where significant influence can exist, and Section 5 describes reporting for joint ventures, a common, important type of investment where control is shared. Section 6 describes reporting for business combinations, the parent/subsidiary relationship, and consolidated financial statements. Section 7 describes reporting for variable interest and special purpose entities. A summary and practice problems in the CFA Institute item set format complete the reading.

2. BASIC CORPORATE INVESTMENT CATEGORIES

In general, investments in marketable debt and equity securities can be categorized as (1) investments in financial assets in which the investor has no significant influence or control over the operations of the investee, (2) investments in associates in which the investor can exert significant influence (but not control) over the investee, and (3) business combinations, including investments in subsidiaries, in which the investor has control over the investee. The distinction between investments in financial assets, investments in associates, and business combinations is based on the degree of influence or control rather than purely on the percent holding. However, lack of influence is generally presumed when the investor holds less than a 20 percent equity interest, significant influence is generally presumed between 20 percent and 50 percent, and control is presumed when the percentage of ownership exceeds 50 percent. A fourth category, investments in joint ventures, indicates shared control by two or more entities.

The following excerpt is from the 2007 Annual Report of Volvo Group, a Swedish manufacturer of commercial vehicles, and illustrates the categorization in practice:

Consolidated financial statements comprise the Parent Company, subsidiaries, joint ventures, and associated companies. Subsidiaries are defined as companies in which Volvo holds more than 50% of the voting rights or in which Volvo otherwise has a controlling interest. Joint ventures are companies over which Volvo has joint control together with one or more external parties. Associated companies are companies in which Volvo has a significant influence, which is normally when Volvo’s holding equals at least 20% but less than 50% of the voting rights.

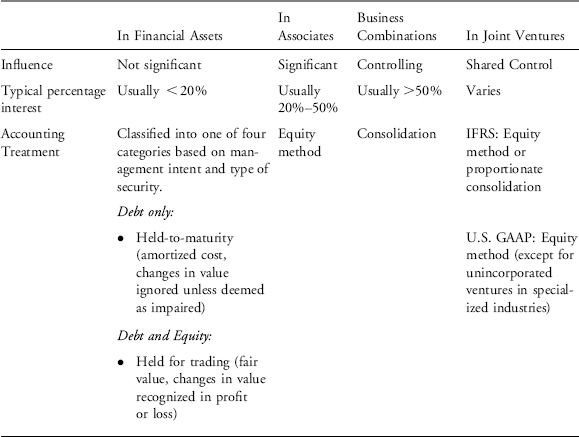

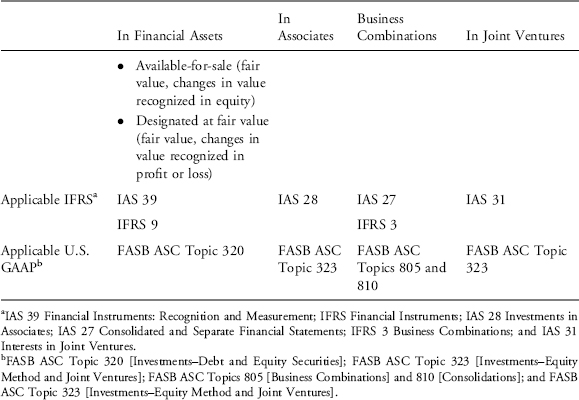

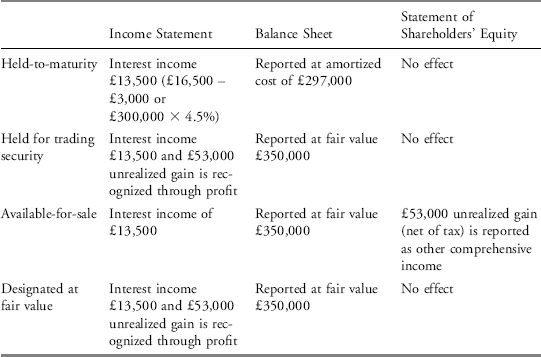

A summary of the accounting treatments and relevant standards for various types of corporate investment is presented in Exhibit 14-1 (the headings in Exhibit 14-1 use the terminology of IFRS; U.S. GAAP categorizes intercorporate investments similarly but not identically). The reader should be alert to the fact that value measurement and/or the treatment of changes in value can vary depending on the portfolio classification and whether IFRS or U.S. GAAP is used. The alternative treatments are discussed in greater depth later in this reading.

EXHIBIT 14-1 Summary of Accounting Treatments for Investments

3. INVESTMENTS IN FINANCIAL ASSETS

Investments in financial assets are considered passive; the investor cannot exert significant influence or control over the operations of the investee. IFRS and U.S. GAAP are similar regarding the accounting for investments in financial assets. IFRS has three basic categories of investments in financial assets: (1) held-to-maturity, (2) fair value through profit or loss, and (3) available-for-sale. Under IFRS, fair value through profit or loss includes held for trading financial assets and those designated as fair value through profit or loss, whereas U.S. GAAP has two separate categories: held for trading, and investments designated at fair value. These categories determine the reporting for the investments.

Generally, investments in financial assets are initially recognized at fair value. Dividend and interest income from investments in financial assets, regardless of categorization, are reported in the income statement. The reporting of subsequent changes in fair value and the treatment of transaction costs, however, depends on the classification of the financial asset investment.

3.1. Held-to-Maturity

Held-to-maturity investments are investments in financial assets with fixed or determinable payments and fixed maturities (debt securities) that the investor has the positive intent and ability to hold to maturity. Held-to-maturity investments are exceptions from the general requirement (under both IFRS and U.S. GAAP) that investments in financial assets are subsequently recognized at fair value. Therefore, strict criteria apply before this designation can be used. Under both IFRS and U.S. GAAP, the investor must have a positive intent and ability to hold the security to maturity.

Reclassifications and sales prior to maturity may call into question the company’s intent and ability. Under IFRS, an entity is not permitted to classify any financial assets as held-to-maturity if it has, during the current or two preceding financial reporting years, sold or reclassified more than an insignificant amount of held-to-maturity investments before maturity unless the sale or reclassification meets certain criteria. Similarly, under U.S. GAAP, a sale (and by inference a reclassification) is taken as an indication that intent was not truly present and use of the held-to-maturity category will be precluded.

IFRS require that held-to-maturity securities be initially recognized at fair value plus transaction costs, whereas U.S. GAAP require held-to-maturity securities be initially recognized at cost including transaction costs. In most cases, however, initial fair value is equal to cost excluding transaction costs, so the treatment is identical. At each reporting date (subsequent to initial recognition), IFRS and U.S. GAAP require that held-to-maturity securities are reported at amortized cost using the effective interest rate method,3 unless objective evidence of impairment exists. Any difference—discount or premium—between maturity (par) value and fair value, typically including transaction costs, existing at the time of purchase is amortized over the life of the security. A discount (par value exceeds fair value) occurs when the stated interest rate is less than the effective rate, and a premium (fair value exceeds par value) occurs when the stated interest rate is greater than the effective rate. Amortization impacts the carrying value of the security. Any interest payments received are adjusted for amortization and are reported as interest income. If the security is sold before maturity (with the potential consequences described earlier), any realized gains or losses arising from the sale are recognized in profit or loss of the period.

3.2. Held for Trading4

Held for trading investments are debt or equity securities acquired with the intent to sell them in the near term. Held for trading securities are reported at fair value. Transaction costs are not included in fair value at initial or subsequent recognition points. At each reporting date, the held for trading investments are remeasured and recognized at fair value with any unrealized gains and losses arising from changes in fair value reported in profit or loss. Also included in profit or loss are interest received on debt securities and dividends received on equity securities.

3.3. Available-for-Sale5

Available-for-sale investments are debt and equity securities not classified as held-to-maturity or held for trading, and not designated at fair value through profit or loss. Under both IFRS and U.S. GAAP, investments classified as available-for-sale are initially measured at fair value, plus transaction costs. At each subsequent reporting date, the investments are remeasured and recognized at fair value, excluding transaction costs, with any unrealized gains or losses arising from changes in fair value reported in equity as other comprehensive income. The amount reported in other comprehensive income is net of taxes. When they are sold, the cumulative gain or loss previously recognized in other comprehensive income is reclassified (i.e., reversed out of comprehensive income) and reported as a reclassification adjustment on the income statement. Interest (calculated using the effective method) from debt securities and dividends from equity securities are included in profit or loss.

IFRS and U.S. GAAP differ on the treatment of foreign exchange gains and losses on available-for-sale debt securities.6 Under IFRS, for the purpose of recognizing foreign exchange gains and losses, a debt security is treated as if it were carried at amortized cost in the foreign currency. Exchange rate differences arising from changes in amortized cost are recognized in profit or loss, and other changes in the carrying amount are recognized in other comprehensive income. In other words, the total change in fair value of an available-for-sale debt security is divided into two components, with any portion attributable to foreign exchange gains and losses recognized on the income statement (in profit or loss) and the remaining portion recognized in other comprehensive income. Under U.S. GAAP, the total change in fair value of available-for-sale debt securities (including foreign exchange rate gains or losses) is included in other comprehensive income. For equity securities, under IFRS and U.S. GAAP, the gain or loss that is recognized in other comprehensive income arising from changes in fair value includes any related foreign exchange component. There is no separate recognition of foreign exchange gains or losses.

3.4. Designated at Fair Value7

Both IFRS and U.S. GAAP allow entities to initially designate investments at fair value that might otherwise be classified as available-for-sale or held-to-maturity. The accounting treatment for investments designated at fair value is similar to that of held for trading investments. At each subsequent reporting date, the investments are remeasured at fair value with any unrealized gains and losses arising from changes in fair value as well as any interest and dividends received included in profit or loss.

The accounting treatment for investments in financial assets under IFRS is illustrated in Exhibit 14-2. This excerpt from the 2007 Annual Report of Deutsche Bank, a global investment bank, describes how its investments are classified, measured, and reported on its financial statements.

Exhibit 14-2 Deutsche Bank 2007 Annual Report

Notes to the Consolidated Financial Statements Financial Assets and Liabilities at Fair Value through Profit or Loss

The Group classifies certain financial assets and financial liabilities as either held for trading or designated at fair value through profit or loss. They are carried at fair value and are presented as financial assets at fair value through profit or loss and financial liabilities at fair value through profit or loss, respectively. Related realized and unrealized gains and losses are included in net gains (losses) on financial assets/liabilities at fair value through profit or loss.

TRADING ASSETS AND LIABILITIES—financial instruments are classified as held for trading if they have been originated, acquired or incurred principally for the purpose of selling or repurchasing them in the near term, or they form part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent actual pattern of short-term profit-taking.

Financial Assets Classified as Available for Sale

Financial assets that are not classified at fair value through profit or loss or as loans are classified as AFS. A financial asset classified as AFS is initially recognized at its fair value plus transaction costs that are directly attributable to the acquisition of the financial asset. The amortization of premiums and accretion of discount are recorded in net interest income. Financial assets classified as AFS are carried at fair value with the changes in fair value reported in equity, in net gains (losses) not recognized in the income statement, unless the asset is subject to a fair value hedge, in which case changes in fair value resulting from the risk being hedged are recorded in other income. For monetary financial assets classified as AFS (for example, debt instruments), changes in carrying amounts relating to changes in foreign exchange rate are recognized in the income statement and other changes in carrying amount are recognized in equity as indicated previously. For financial assets classified as AFS that are not monetary items (for example, equity instruments), the gain or loss that is recognized in equity includes any related foreign exchange component.

Determination of Fair Value

Fair value is defined as the price at which an asset or liability could be exchanged in a current transaction between knowledgeable, willing parties, other than in a forced or liquidation sale. Where available, fair value is based on observable market prices or parameters or derived from such prices or parameters. Where observable prices or inputs are not available, valuation techniques appropriate for the particular instrument are applied. These valuation techniques involve some level of management estimation and judgment, the degree of which will depend on the price transparency for the instrument or market and the instrument’s complexity. The valuation process to determine fair value also includes making appropriate adjustments to the valuation model outputs to consider factors such as close out costs, liquidity and credit risk (both counterparty credit risk in relation to financial assets and the Bank’s own credit risk in relation to financial liabilities).

3.5. Reclassification of Investments

Both IFRS and U.S. GAAP permit entities to reclassify their intercorporate investments; however, there are certain restrictions and criteria that must be met. Reclassification may result in changes in how the asset value is measured and how unrealized gains or losses are recognized.

IFRS generally prohibits the reclassification of securities into or out of the designated-at-fair-value category,8 and reclassification out of the held for trading category is severely restricted. Held-to-maturity (debt) securities can be reclassified as available-for-sale if a change in intention or a change in ability to hold the security until maturity occurs. At the time of reclassification to available-for-sale, the security is remeasured at fair value with the difference between its carrying amount (amortized cost) and fair value recognized in other comprehensive income. Recall that the reclassification has implications for the use of the held-to-maturity category for existing debt securities and new purchases. A mandatory reclassification and a prohibition from future use may result from the reclassification.

Debt securities initially designated as available-for-sale may be reclassified to held-to-maturity if a change in intention or ability has occurred. The fair-value carrying amount of the security at the time of reclassification becomes its new (amortized) cost. Any previous gain or loss that had been recognized in other comprehensive income is amortized to profit or loss over the remaining life of the security using the effective interest method. Any difference between the new amortized cost of the security and its maturity value is amortized over the remaining life of the security using the effective method.

Any financial asset classified as available-for-sale may be reclassified at cost, in the rare instances where there is no reliable measure of fair value and no evidence of impairment. However, if a reliable fair value measure becomes available, the financial asset must be reclassified to the available-for-sale category with changes in value recognized in other comprehensive income.

U.S. GAAP allows reclassifications (transfers) of securities between all categories using the fair value of the security at the date of transfer. However, recall that the reclassification of securities from the held-to-maturity category has implications for the use of this category for other securities. The treatment of unrealized holding gains and losses on the transfer date, however, depends on the initial classification of the security. For a security initially classified as held for trading that is being reclassified as available-for-sale, any unrealized gains and losses (arising from the difference between its carrying value and current fair value) are recognized in income. For a security transferred into the held-for-trading category, the unrealized gains or losses are recognized immediately. In the case of transfer from available-for-sale, the cumulative amount of gains and losses previously recognized in other comprehensive income is recognized in income on the date of transfer. For a debt security transferred into the available-for-sale category from held-to-maturity, the unrealized holding gain or loss at the date of the transfer (i.e., the difference between the fair value and amortized cost) is reported in other comprehensive income. For a debt security transferred into the held-to-maturity category from available-for-sale, the cumulative amount of gains or losses previously reported in other comprehensive income will be amortized over the remaining life of the security as an adjustment of yield (interest income) in the same manner as a premium or discount.

3.6. Impairments

A financial asset (in this case debt or equity securities) becomes impaired whenever its carrying amount is expected to permanently exceed its recoverable amount. There are key differences in the approaches that IFRS and U.S. GAAP take to determine if a financial asset is impaired and how the impairment loss is measured and reported.

Under IFRS, at the end of each reporting period, financial assets not carried at fair value through profit or loss (individually or as a group) need to be assessed, whether there is any objective evidence that the assets are impaired. Since investments classified as fair value through profit or loss and held for trading are reported at fair value, any impairment loss will have already been recognized in profit or loss as the events were occurring or will be recognized in profit or loss immediately.

A debt security is impaired if one or more events (loss events) occur after initial recognition that has impact on its estimated future cash flows that can be reliably estimated. Although it may not be possible to identify a single specific event that caused the impairment, the combined effect of several events may cause the impairment. Losses expected as a result of future events no matter how likely are not recognized. Examples of loss events causing impairment are:

- Significant financial difficulty of the issuer.

- Default or delinquency in interest or principal payments.

- The borrower experiences financial difficulty and receives a concession from the lender as a result.

- It becomes probable that the borrower will enter bankruptcy or other financial reorganization.

The disappearance of an active market because an entity’s financial instruments are no longer publicly traded is not evidence of impairment. A downgrade of an entity’s credit rating or a decline in fair value of a security below its cost or amortized cost is also not by itself evidence of impairment. However, it may be evidence of impairment when considered with other available information.

For equity securities, objective evidence of a loss event includes:

- Significant changes in the technological, market, economic, and/or legal environments that have an adverse affect on the investee and indicate that the initial cost of the equity investment may not be recovered.

- A significant or prolonged decline in the fair value of an equity investment below its cost.

For held-to-maturity (debt) investments that have become impaired, the amount of the loss is measured as the difference between the security’s carrying value and the present value of its estimated future cash flows discounted at the security’s original effective interest rate (the effective interest rate computed at initial recognition). The carrying amount of the security is then reduced either directly or through the use of an allowance account, and the amount of the loss is recognized in profit or loss. If in a subsequent period the amount of the impairment loss decreases and the decrease can be objectively related to an event occurring after the impairment was recognized (for example, an improvement in the debtor’s credit rating), the previously recognized impairment loss can be reversed either directly (by increasing the carrying value of the security) or by adjusting the allowance account. The amount of this reversal is then recognized in profit or loss.

For available-for-sale securities that have become impaired, the cumulative loss that had been recognized in other comprehensive income is reclassified from equity to profit or loss as a reclassification adjustment. The amount of the cumulative loss to be reclassified is the difference between acquisition cost (net of any principal repayment and amortization) and current fair value, less any impairment loss that has previously been recognized in profit or loss. Impairment losses on available-for-sale equity securities cannot be reversed. However, impairment losses on available-for-sale debt securities can be reversed if a subsequent increase in fair value can be objectively related to an event occurring after the impairment loss was recognized in profit and loss. In this case, the impairment loss is reversed with the amount of the reversal recognized in profit or loss.

Exhibit 14-3 contains an excerpt from Deutsche Bank’s 2007 annual report that describes how impairment losses for its financial assets are determined, measured, and recognized on its financial statements.

Exhibit 14-3 Excerpt from Deutsche Bank 2007 Annual Report

Impairment of Financial Assets

At each balance sheet date, the Group assesses whether there is objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or group of financial assets is impaired and impairment losses are incurred if there is:

- objective evidence of impairment as a result of a loss event that occurred after the initial recognition of the asset and up to the balance sheet date (“a loss event”);

- the loss event had an impact on the estimated future cash flows of the financial asset or the group of financial assets; and

- a reliable estimate of the amount can be made.

Impairment of Financial Assets Classified as Available for Sale

For financial assets classified as AFS, management assesses at each balance sheet date whether there is objective evidence that an asset or group of assets is impaired. In the case of equity investments classified as AFS, objective evidence would include a significant or prolonged decline in the fair value of the investment below cost. In the case of debt securities classified as AFS, impairment is assessed based on the same criteria as for loans.

Where there is evidence of impairment, the cumulative unrealized loss previously recognized in equity, in net gains (losses) not recognized in the income statement, is removed from equity and recognized in the income statement for the period, reported in net gains (losses) on financial assets available for sale. This amount is determined as the difference between the acquisition cost (net of any principal repayments and amortization) and current fair value of the asset less any impairment loss on that investment previously recognized in the income statement. Reversals of impairment losses on equity investments classified as AFS are not reversed through the income statement; increases in their fair value after impairment are recognized in equity.

Reversals of impairment of debt securities are recognized in the income statement if the recovery is objectively related to a specific event occurring after the impairment loss was recognized in the income statement.

Under U.S. GAAP, the determination of impairment and the calculation of the impairment loss are different than under IFRS. For securities classified as available-for-sale or held-to-maturity, the investor is required to determine at each balance sheet date, whether the decline in value is other than temporary. For debt securities classified as held-to-maturity, this means that the investor will be unable to collect all amounts due according to the contractual terms existing at acquisition. If the decline in fair value is deemed to be other than temporary, the cost basis of the security is written down to its fair value, which then becomes the new cost basis of the security. The amount of the write-down is treated as a realized loss and reported on the income statement.

For available-for-sale securities (both debt and equity) if the decline in fair value is other than temporary, the cost basis of the security is written down to its fair value, which becomes the new cost basis, and the amount of the write-down is treated as a realized loss. However, the new cost basis cannot be increased for subsequent increases in fair value. Instead, subsequent increases in fair value (and decreases if other than temporary) are treated as unrealized gains or losses and included in other comprehensive income.

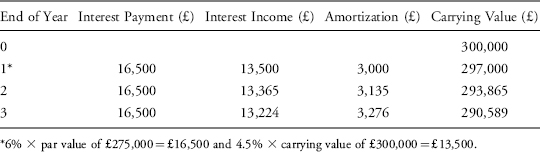

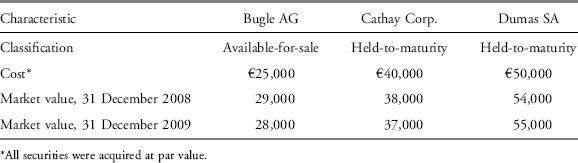

EXAMPLE 14-1 Accounting for Investments in Debt Securities

In this example, two fictitious companies are used. On 1 January 2008, Baxter Inc. invested £300,000 in Cartel Co. debt securities (with a 6 percent stated rate on par value, payable each 31 December). The par value of the securities was £275,000. On 31 December 2008, the fair value of Baxter’s investment in Cartel is £350,000.

Assume that the market interest rate in effect when the bonds were purchased was 4.5 percent.9 If the investment is designated as held-to-maturity, the investment is reported at amortized cost using the effective interest method. A portion of the amortization table is as follows:

1. How would this investment be reported on the balance sheet, income statement, and statement of shareholders’ equity at 31 December 2008, under either IFRS or U.S. GAAP (accounting is essentially the same in this case), if Baxter designated the investment as (1) held-to-maturity, (2) held for trading, (3) available-for-sale, or (4) designated at fair value?

2. How would the gain be recognized if the debt securities were sold on 1 January 2009 for £352,000?

3. How would this investment appear on the balance sheet at 31 December 2009?

4. How would the classification and reporting differ if Baxter had invested in Cartel’s equity securities instead of its debt securities?

Solution to 1:

Solution to 2: If the debt securities were sold on 1 January 2009 for £352,000, the amount of the realized gain would be as follows:

Held-to-maturity: gain on income statement of £55,000 (£352,000 − £297,000)

Fair value through profit or loss (held for trading): gain on income statement of £2,000 (£352,000 − £350,000)

Available-for-sale: gain on income statement of £55,000 = (£352,000 − £350,000)+ £53,000 (removed from other comprehensive income)

Solution to 3: If the investment was classified as held-to-maturity, the reported amount at amortized cost at the end of Year 2 on the balance sheet would be £293,865. If the investment was classified as either held for trading securities, available-for-sale, or designated at fair value, it would be measured at its fair value at the end of Year 2.

Solution to 4: If the investment had been in Cartel Co. equity securities rather than debt securities, the analysis would change in the following ways:

- There would not be a held-to-maturity option.

- Dividend income (if any) would replace interest income.

The convergence between IFRS and U.S. GAAP in the classification and reporting standards for investments in financial assets has made it easier for analysts to evaluate investment returns. Analysts typically evaluate performance separately for operating and investing activities. Analysis of operating performance should exclude items related to investing activities such as interest income, dividends, and realized and unrealized gains and losses. For comparative purposes, analysts should exclude nonoperating assets in the determination of return on net operating assets. IFRS and U.S. GAAP10 require disclosure of fair value of each class of investment in financial assets. Using market values and adjusting pro forma financial statements for consistency improves assessments of performance ratios across companies.

Under both IFRS and U.S. GAAP, when an entity (investor) holds 20 to 50 percent of the voting rights of an associate (investee), either directly or indirectly (i.e., through subsidiaries), it is presumed (unless circumstances demonstrate otherwise) that the entity has (or can exercise) significant influence, but not control, over the investee’s business activities.11 Conversely, if the investor holds, directly or indirectly, less than 20 percent of the voting power of the associate (investee), it is presumed that the investor does not have (or cannot exercise) significant influence, unless such influence can be demonstrated. IAS 28 (IFRS) and FASB ASC Topic 323 (U.S. GAAP) apply to most investments in which an investor has significant influence; they also provide guidance on accounting for investments in associates using the equity method.12 These standards note that significant influence may be evidenced by

- Representation on the board of directors.

- Participation in the policy-making process.

- Material transactions between the investor and the investee.

- Interchange of managerial personnel.

- Technological dependency.

Being able to exert significant influence means that the financial and operating performance of the investee is partly attributable to the management decisions and operational skills of the investor. The equity method of accounting for the investment reflects the economic reality of this relationship and provides a more objective basis for reporting investment income.

Under the equity method of accounting, the investment is initially recognized at cost and is increased (decreased) to recognize the investor’s share of the investee’s profit (loss) and decreased by any distributions (dividends) received from the investee after the acquisition date. As a result the change in the investment account reflects the investor’s proportionate share of the change in the investee’s net assets. The investor also reports its share of the investee’s profit or loss on its income statement.

4.1. Equity Method of Accounting: Basic Principles

Under the equity method of accounting, the equity investment is initially recorded on the investor’s balance sheet at cost. In subsequent periods, the carrying amount of the investment is adjusted to recognize the investor’s proportionate share of the investee’s earnings or losses, and these earnings or losses are reported in income. Dividends or other distributions received from the investee are treated as a return of capital and reduce the carrying amount of the investment and are not reported in the investor’s profit or loss. The equity method is often referred to as “one-line consolidation” since the investor’s proportionate ownership interest in the assets and liabilities of the investee is disclosed as a single line item (net assets) on its balance sheet, and the investor’s share of the revenues and expenses of the investee is disclosed as a single line item on its income statement (contrast these disclosures with the disclosures on consolidated statements in Section 6). Equity method investments are classified as noncurrent assets on the balance sheet. The investor’s share of the profit or loss of equity method investments, and the carrying amount of those investments, must be separately disclosed on the income statement and balance sheet.

EXAMPLE 14-2 Equity Method: Balance in Investment Account

Branch (a fictitious company) purchases a 20 percent interest in Williams (a fictitious company) for €200,000 on 1 January 2008. Williams reports income and dividends as follows:

| Income | Dividends | |

| 2008 | €200,000 | €50,000 |

| 2009 | 300,000 | 100,000 |

| 2010 | 400,000 | 200,000 |

| €900,000 | €350,000 |

Calculate the investment in Williams that appears on Branch’s balance sheet as of the end of 2010.

Solution: Investment in Williams at 31 December 2010:

| Initial cost | €200,000 | |

| Equity income 2008 | €40,000 | = (20% of €200,000 Income) |

| Dividends received 2008 | (€10,000) | = (20% of €50,000 Dividends) |

| Equity income 2009 | €60,000 | = (20% of €300,000 Income) |

| Dividends received 2009 | (€20,000) | = (20% of €100,000 Dividends) |

| Equity income 2010 | €80,000 | = (20% of €400,000 Income) |

| Dividends received 2010 | (€40,000) | = (20% of €200,000 Dividends) |

| Balance | €310,000 | = [€200,000+20% × (€900,000 − €350,000)] |

This simple example implicitly assumes that the purchase price equals the purchased equity in the book value of Williams’ net assets. Sections 4.2 and 4.3 will cover the more common case in which the purchase price does not equal the proportional share of the book value of the investee’s net assets.

Using the equity method, the investor includes its share of the investee’s profit and losses on the income statement. The equity investment is carried at cost, plus its share of postacquisition income less dividends received. The recorded investment value can decline as a result of investee losses or a permanent decline in the investee’s market value (see Section 4.5 for treatment of impairments). If the investment value is reduced to zero, the investor usually discontinues the equity method and does not record further losses. If the investee subsequently reports profits, the equity method is resumed after the investor’s share of the profits equals the share of losses not recognized during the suspension of the equity method. Exhibit 14-4 contains an excerpt from Deutsche Bank’s 2007 annual report in which it describes the treatment for its investments in associates.

Exhibit 14-4 Excerpt from Deutsche Bank 2007 Annual Report

Associates and Jointly Controlled Entities

An associate is an entity in which the Group has significant influence, but not a controlling interest, over the operating and financial management policy decisions of the entity. Significant influence is generally presumed when the Group holds between 20% and 50% of the voting rights. The existence and effect of potential voting rights that are currently exercisable or convertible are considered in assessing whether the Group has significant influence. Among the other factors that are considered in determining whether the Group has significant influence are representation on the board of directors (supervisory board in the case of German stock corporations) and material intercompany transactions. The existence of these factors could require the application of the equity method of accounting for a particular investment even though the Group’s investment is for less than 20% of the voting stock.

A jointly controlled entity exists when the Group has a contractual arrangement with one or more parties to undertake activities through entities which are subject to joint control.

Equity Method Investments

Investments in associates and jointly controlled entities are accounted for using the equity method of accounting unless they are held for sale. As of December 31, 2007, there were two significant associates which were accounted for as held for sale. For information on assets held for sale please refer to Note [22].

As of December 31, 2007, the following investees were significant, representing 75% of the carrying value of equity method investments.

| Investment1 | Ownership Percentage |

| AKA Ausfuhrkredit-Gesellschaft mit beschränkter Haftung, Frankfurt | 26.89 |

| Beijing Gouhua Real Estate Co., Ltd., Beijing | 30.00 |

| Compañia Logistica de Hidrocarburos CLH, S.A., Madrid2 | 5.00 |

| DB Global Masters (Fundamental Value Trading II) Fund Ltd, George Town | 27.88 |

| DB Phoebus Lux S.à.r.l., Luxembourg3 | 74.90 |

| Deutsche Interhotel Holding GmbH & Co. KG, Berlin | 45.51 |

| Discovery Russian Realty Paveletskaya Project Ltd., George Town | 33.33 |

| DMG & Partners Securities Pte. Ltd., Singapore | 49.00 |

| Fincasa Hipotecaria, S.A. de C.V. Sociedad Financiera de Objeto Limitado, Mexico City | 49.00 |

| Fondo Immobiliare Chiuso Piramide Globale, Milan | 42.45 |

| Force 2005-1 Limited Partnership, St. Helier | 40.00 |

| Gemeng International Energy Group Company Limited, Taiyuan2 | 19.00 |

| Hanoi Building Commercial Joint Stock Bank, Hanoi2 | 10.00 |

| K&N Kenanga Holdings Bhd, Kuala Lumpur2 | 16.55 |

| Ligusterfonds, Amsterdam | 25.85 |

| Makkolli Trading Ltd, Hamilton | 45.00 |

| MFG Flughafen-Grundstücksverwaltungsgesellschaft mbH & Co. BETA KG, Gruenwald | 25.03 |

| Mountaineer Natural Gas Trust, Wilmington | 50.00 |

| Paternoster Limited, Douglas | 30.99 |

| PX Holdings Limited, Stockton on Tees | 43.00 |

| Redwood Russia PLP1 Limited, St. Helier | 40.10 |

| Rongde Asset Management Company Limited, Beijing | 40.70 |

| RREEF America REIT III, Inc., Chicago2 | 9.67 |

| RREEF Global Opportunities Fund II LLC, Wilmington2 | 9.90 |

| STC Capital YK, Tokyo | 50.00 |

| SWIP Multi Manager Global Real Estate Fund, London | 24.70 |

| SWIP Property Trust, London | 37.38 |

| SWIP UK Income Fund, London | 35.99 |

| SWIP UK Smaller Cos, London | 34.24 |

| VCG Venture Capital Gesellschaft mbH & Co. Fonds III KG, Munich | 36.98 |

1All significant equity method investments are investments in associates.

2The Group has significant influence over the investee through board seats or other measures.

3The Group does not have a controlling financial interest in the investee.

Summarized aggregated financial information of these significant equity method investees were as follows:

| (€ in millions) | Dec. 31, 2007 | Dec. 31, 2006 |

| Total assets | 22,107 | 20,062 |

| Total liabilities | 13,272 | 12,113 |

| Revenues | 2,368 | 2,344 |

| Net income/loss | 528 | 1,195 |

The following are the components of the net income (loss) from all equity method investments:

| (€ in millions) | 2007 | 2006 |

| Net income (loss) from equity method investments: | ||

| Pro rata share of investees’ net income (loss) | 358 | 207 |

| Net gains (losses) on disposal of equity method investments1 | 9 | 217 |

| Impairments | (14) | (5) |

| Total net income (loss) from equity method investments | 353 | 419 |

1Net gains (losses) on disposal of equity method investments in 2006 included a gain of €131 million from the sale of the Group’s remaining holding in EUROHYPO AG.

There was no unrecognized share of losses of an investee, neither for the period, or cumulatively.

Equity method investments for which there are published price quotations had a carrying value of €160 million and a fair value of €168 million as of December 31, 2007 and a carrying value of €219 million and a fair value of €228 million as of December 31, 2006.

It is interesting to note the explanations for the treatment as associates when the ownership percentage is less than 20 percent or is greater than 50 percent. The equity method reflects the strength of the relationship between the investor and its associates. In the instances where the percentage ownership is less than 20 percent, Deutsche Bank uses the equity method because it has significant influence over these associates’ operating and financial policies either through its representation on their boards of directors and/or material intercompany transactions. The equity method provides a more objective basis for reporting investment income than the accounting treatment for investments in financial assets, since the investor can potentially influence the timing of dividend distributions.

4.2. Investment Costs That Exceed the Book Value of the Investee

The cost (purchase price) to acquire shares of an investee is often greater than the book value of those shares. This is because many of the investee’s assets and liabilities reflect historical cost rather than fair values. IFRS allow an entity to measure its property, plant, and equipment using either historical cost or fair value (less accumulated depreciation).13 U.S. GAAP, however, require the use of historical cost (less accumulated depreciation) to measure property, plant, and equipment.14

When the cost of the investment exceeds the investor’s proportionate share of the investee’s (associate’s) net identifiable assets (e.g., inventory, property, plant, and equipment), the difference is first allocated to specific assets (or categories of assets). These differences are then amortized to the investor’s proportionate share of the investee’s profit or loss over the economic lives of the assets whose fair values exceeded book values. It should be noted that the allocation is not recorded formally; what appears initially in the investment account on the balance sheet of the investor is the cost. Over time, as the differences are amortized, the balance in the investment account will come closer to representing the ownership percentage of the book value of the net assets of the associate.

IFRS and U.S. GAAP both treat the difference between the cost of the acquisition and investor’s share of the fair value of the net identifiable assets as goodwill. Therefore, any remaining difference between the acquisition cost and the fair value of net identifiable assets that cannot be allocated to specific assets is treated as goodwill and is not amortized. Instead it is reviewed for impairment on a regular basis, and written down for any identified impairment. Goodwill, however, is included in the carrying amount of the investment, since investment is reported as a single line item on the investor’s balance sheet.15

EXAMPLE 14-3 Equity Method Investment in Excess of Book Value

Assume that the hypothetical Blake Co. acquires 30 percent of the outstanding shares of the hypothetical Brown Co. At the acquisition date, book values and fair values of Brown’s recorded assets and liabilities are as follows:

| Book Value | Fair Value | |

| Current assets | €10,000 | €10,000 |

| Plant and equipment | 190,000 | 220,000 |

| Land | 120,000 | 140,000 |

| €320,000 | €370,000 | |

| Liabilities | 100,000 | 100,000 |

| Net assets | €220,000 | €270,000 |

Blake Co. believes the value of Brown Co. is higher than the fair value of its identifiable net assets. They offer €100,000 for a 30 percent interest in Brown Co. Part of the excess purchase price is attributable to the €50,000 difference between book value and fair value of the identifiable assets and so the remaining amount is attributable to goodwill. Calculate goodwill.

Solution:

| Purchase price | €100,000 |

| 30 percent of book value of Brown (30% × €220,000) | 66,000 |

| Excess purchase price | €34,000 |

| Attributable to net assets | |

| Plant and equipment (30% × €30,000) | €9,000 |

| Land (30% × €20,000) | 6,000 |

| Goodwill (residual) | 19,000 |

| €34,000 |

As illustrated earlier, goodwill is the residual excess not allocated to identifiable assets or liabilities.

4.3. Amortization of Excess Purchase Price

The excess purchase price allocated to the assets and liabilities is accounted for in a manner that is consistent with the accounting treatment for the specific asset or liability to which it is assigned. Amounts allocated to assets and liabilities that are expensed (such as inventory) or periodically depreciated or amortized (plant, property, and intangible assets) must be treated in a similar manner. These allocated amounts are not reflected on the financial statements of the investee (associate), and the investee’s income statement will not reflect the necessary periodic adjustments. Therefore, the investor must directly record these adjustment effects by reducing the carrying amount of the investment on its balance sheet and by reducing its share of the investee’s profit recognized on its income statement. Amounts allocated to assets or liabilities that are not systematically amortized (e.g., land) will continue to be reported at their fair value as of the date the investment was acquired. As stated earlier, goodwill is included in the carrying amount of the investment instead of being separately recognized. It is not amortized since it is considered to have an indefinite life.

Using the previous example and assuming a 10-year useful life for plant, property, and equipment and using straight-line depreciation, the annual amortization is as follows:

Annual amortization would reduce the investor’s share of the investee’s reported income (equity income) and the balance in the investment account by €900 for each year over the 10-year period.

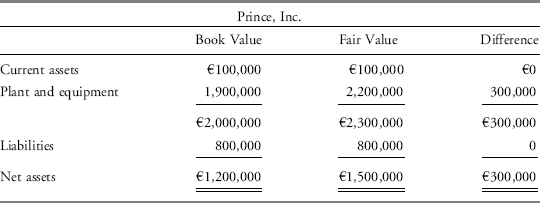

EXAMPLE 14-4 Equity Method Investments with Goodwill

On 1 January 2009 Parker Company acquired 30 percent of Prince Inc. common shares for the cash price of €500,000 (both companies are fictitious). It is determined that Parker has the ability to exert significant influence on Prince’s financial and operating decisions. The following information concerning Prince’s assets and liabilities on 1 January 2009 is provided:

The plant and equipment are depreciated on a straight-line basis and have 10 years of remaining life. Prince reports net income for 2009 of €100,000 and pays dividends of €50,000. Calculate the following:

1. Goodwill included in the purchase price.

2. Investment in associate (Prince) at the end of 2009.

Solution to 1:

| Purchase price | €500,000 |

| Acquired equity in book value of Prince’s net assets (30% × €1,200,000) | 360,000 |

| Excess purchase price | €140,000 |

| Attributable to plant and equipment (30% × €300,000) | 90,000 |

| Goodwill (residual) | 50,000 |

| €140,000 |

Solution to 2: Investment in associate

| Purchase price | €500,000 |

| Parker’s share of Prince’s net income (30% × €100,000) | 30,000 |

| Dividends received (30% of €50,000) | (15,000) |

| Amortization of excess purchase price attributable to plant and equipment (€90,000 ÷ 10 years) | (9,000) |

| 31 December 09 balance in investment in Prince | €506,000 |

An alternate way to look at the balance in the investment account is that it reflects the basic valuation principle of the equity method. At any point in time, the investment account balance equals the investor’s (Parker) proportionate share of the net equity (net assets at book value) of the investee (Prince) plus the unamortized balance of the original excess purchase price. Applying this principle to this example:

| 2009 Beginning net assets = | €1,200,000 |

| Plus: Net income | 100,000 |

| Less: Dividends | (50,000) |

| 2009 Ending net assets | €1,250,000 |

| Parker’s proportionate share of Prince’s recorded net assets (30% × €1,250,000) | €375,000 |

| Unamortized excess purchase price (€140,000 − 9,000) | 131,000 |

| Investment in Prince | €506,000 |

Note that the unamortized excess purchase price is a cost incurred by Parker, not Prince. Therefore, the total amount is included in the investment account balance.

4.4. Fair Value Option

Both IFRS and U.S. GAAP give the investor the option to account for their equity method investment at fair value.16 Under U.S. GAAP this option is available to all entities; however, under IFRS, its use is restricted to venture capital organizations, mutual funds, unit trusts, and similar entities, including investment-linked insurance funds.

Both standards require that the election to use the fair value option occur at the time of initial recognition and is irrevocable. Subsequent to initial recognition, the investment is reported at fair value with unrealized gains and losses arising from changes in fair value as well as any interest and dividends received included in the investor’s profit or loss (income). Under the fair value method, the investment account on the investor’s balance sheet does not reflect the investor’s proportionate share of the investee’s profit or loss, dividends, or other distributions. In addition, the excess of cost over the fair value of the investee’s identifiable net assets is not amortized, nor is goodwill created.

4.5. Impairment

Both IFRS and U.S. GAAP require periodic reviews of equity method investments for impairment. If the fair value of the investment is below its carrying value and this decline is deemed to be other than temporary, an impairment loss must be recognized.

Under IFRS, there must be objective evidence of impairment as a result of one or more (loss) events that occurred after the initial recognition of the investment, and that loss event has an impact on the investment’s future cash flows, which can be reliably estimated. Because goodwill is included in the carrying amount of the investment and is not separately recognized, it is not separately tested for impairment. Instead, the entire carrying amount of the investment is tested for impairment by comparing its recoverable amount with its carrying amount.17 The impairment loss is recognized on the income statement, and the carrying amount of the investment on the balance sheet is either reduced directly or through the use of an allowance account.

U.S. GAAP takes a different approach. If the fair value of the investment declines below its carrying value and the decline is determined to be permanent, U.S. GAAP18 requires an impairment loss to be recognized on the income statement and the carrying value of the investment on the balance sheet is reduced to its fair value.

Both IFRS and U.S. GAAP prohibit the reversal of impairment losses even if the fair value later increases.

Section 6.4.5 of this reading discusses impairment tests for the goodwill attributed to a controlling investment (consolidated subsidiary). Note the distinction between the disaggregated goodwill impairment test for consolidated statements and the total fair value of impairment test for equity method investments.

4.6. Transactions with Associates

An investor company can influence the terms and timing of transactions with its associates so profits from such transactions cannot be realized until confirmed through use or sale to third parties. Accordingly, the investor company’s share of any unrealized profit must be deferred by reducing the amount recorded under the equity method. In the subsequent period(s) when this deferred profit is considered confirmed, it is added back to the equity income. At that time, the equity income is again based on the recorded values in the associate’s accounts.

Transactions between the two affiliates may be upstream (associate to investor) or downstream (investor to associate). In an upstream sale, the profit on the intercompany transaction is recorded on the associate’s income (profit or loss) statement. The investor’s share of the unrealized profit is thus included in equity income on the investor’s income statement. In a downstream sale, the profit is recorded on the investor’s income statement. Both IFRS and U.S. GAAP require that the unearned profits be eliminated to the extent of the investor’s interest in the associate.19 The result is an adjustment to equity income on the investor’s income statement.

EXAMPLE 14-5 Equity Method with Sale of Inventory: Upstream Sale

On 1 January 2009, Wicker Company acquired a 25 percent interest in Foxworth Company (both companies are fictitious) for €1,000,000 and used the equity method to account for its investment. The book value of Foxworth’s net assets on that date was €3,800,000. An analysis of fair values revealed that all assets and liabilities were equal to book values except for a building. The building was undervalued by €40,000 and has a 20-year remaining life. The company used straight-line depreciation for the building. Foxworth paid €3,200 in dividends in 2009. During 2009, Foxworth reported net income of €20,000. During the year, Foxworth sold inventory to Wicker. At the end of the year, there was €8,000 profit from the upstream sale in Wicker’s inventory because the goods had not been sold to an outside party.

1. Calculate the equity income to be reported as a line item on Wicker’s 2009 income statement.

2. Calculate the balance in the investment in Foxworth to be reported on the 31 December 2009 balance sheet.

| Purchase price | €1,000,000 |

| Acquired equity in book value of Foxworth’;s net assets (25% × €3,800,000) | 950,000 |

| Excess purchase price | €50,000 |

| Attributable to: | |

| Building (25% × €40,000) | €10,000 |

| Goodwill (residual) | 40,000 |

| €50,000 |

Solution to 1: Equity Income

| Wicker’s share of Foxworth’s reported income (25% × €20,000) | €5,000 |

| Amortization of excess purchase price attributable to building (€10,000 ÷ 20) | (500) |

| Unrealized profit (25% × €8,000) | (2,000) |

| Equity income 2009 | €2,500 |

Solution to 2: Investment in Foxworth:

| Purchase price | €1,000,000 |

| Equity income 2009 | 2,500 |

| Dividends received (25% × €3,200) | (800) |

| Investment in Foxworth, 31 Dec 2009 | €1,001,700 |

| Composition of investment account: | |

| Wicker’s proportionate share of Foxworth’s net equity (net assets at book value) [25% × (€3,800,000+(20,000 − 8,000) − 3,200)] | €952,200 |

| Unamortized excess purchase price (€50,000 − 500) | 49,500 |

| €1,001,700 |

EXAMPLE 14-6 Equity Method with Sale of Inventory: Downstream Sale

Jones Company owns 25 percent of Jason Company (both fictitious companies) and appropriately applies the equity method of accounting. Amortization of excess purchase price, related to undervalued assets at the time of the investment, is €8,000 per year. During 2009 Jones sold €96,000 of inventory to Jason for €160,000. Jason resold €120,000 of this inventory during 2009. The remainder was sold in 2010. Jason reports income from its operations of €800,000 in 2009 and €820,000 in 2010.

1. Calculate the equity income to be reported as a line item on Jones’s 2009 income statement.

2. Calculate the equity income to be reported as a line item on Jones’s 2010 income statement.

Solution to 1: Equity Income 2009

| Jones’s share of Jason’s reported income (25% × €800,000) | €200,000 |

| Amortization of excess purchase price | (8,000) |

| Unrealized profit (25% × €16,000) | (4,000) |

| Equity income 2009 | €188,000 |

Jones’s profit on the sale to Jason = €160,000 − 96,000 = €64,000

Jason sells 75% (€120,000/160,000) of the goods purchased from Jones; 25% is unsold.

Total unrealized profit = €64,000 × 25% = €16,000

Jones’s share of the unrealized profit = €16,000 × 25% = €4,000

Alternative approach:

Jones’s profit margin on sale to Jason: 40 percent (€64,000/€160,000)

Jason’s inventory of Jones’s goods at 31 Dec. 2009: €40,000

Jones’s profit margin on this was 40% × 40,000 = €16,000

Jones’s share of profit on unsold goods = €16,000 × 25% = €4,000

Solution to 2: Equity Income 2010

| Jones’s share of Jason’s reported income (25% × €820,000) | €205,000 |

| Amortization of excess purchase price | (8,000) |

| Realized profit (25% × €16,000) | 4,000 |

| Equity income 2010 | €201,000 |

Jason sells the remaining 25 percent of the goods purchased from Jones.

4.7. Disclosure

The notes to the financial statements are an integral part of the information necessary for investors. Both IFRS and U.S. GAAP require disclosure about the assets, liabilities, and results of equity method investments. For example, in their 2007 annual report, Deutsche Bank reports that:

Investments in associates and jointly controlled entities are accounted for under the equity method of accounting. The Group’s share of the results of associates and jointly controlled entities is adjusted to conform with the accounting policies of the Group. Unrealized gains on transactions are eliminated to the extent of the Group’s interest in the investee.

Under the equity method of accounting, the Group’s investments in associates and jointly controlled entities are initially recorded at cost, and subsequently increased (or decreased) to reflect both the Group’s pro-rata share of the post acquisition net income (or loss) of the associate or jointly controlled entity and other movements included directly in the equity of the associate or jointly controlled entity. Goodwill arising on the acquisition of an associate or a jointly controlled entity is included in the carrying value of the investment (net of any accumulated impairment loss). Equity method losses in excess of the Group’s carrying value of the investment in the entity are charged against other assets held by the Group related to the investee. If those assets are written down to zero, a determination is made whether to report additional losses based on the Group’s obligation to fund such losses.

For practical reasons, associated companies’ results are sometimes included in the investor’s accounts with a certain time lag, normally not more than one quarter. Dividends from associated companies are not included in investor income because it would be a double counting. Applying the equity method recognizes the investor’s full share of the associate’s income. Dividends received involve exchanging a portion of equity interest for cash. In the consolidated balance sheet, the book value of shareholdings in associated companies is increased by the investor’s share of the company’s net income and reduced by amortization of surplus values and the amount of dividends received.

4.8. Issues for Analysts

Equity method accounting presents several challenges for analysis. First, analysts should question whether the equity method is appropriate. For example, an investor holding 19 percent of an associate may in fact exert significant influence but may attempt to avoid using the equity method to avoid reporting associate losses. On the other hand, an investor holding 25 percent of an associate may be unable to exert significant influence and may be unable to access cash flows, and yet prefers the equity method to capture associate income.

Second, the investment account represents the investor’s percentage ownership in the net assets of the investee company through “one-line consolidation.” There can be significant assets and liabilities of the investee that are not reflected on the investor’s balance sheet, which will significantly affect debt ratios. Net margin ratios could be overstated because income for the associate is included in investor net income but is not specifically included in sales. An investor may actually control the investee with less than 50 percent ownership but prefer the financial results using the equity method. Careful analysis can reveal financial performance driven by accounting structure.

Finally, the analyst must consider the quality of the equity method earnings. The equity method assumes that a percentage of each dollar earned by the investee company is earned by the investor (i.e., a fraction of the dollar equal to the fraction of the company owned), even if cash is not received. Analysts should, therefore, consider potential restrictions on dividend cash flows (the statement of cash flows).

Joint ventures—ventures undertaken and controlled by two or more parties—can be a convenient way to enter foreign markets, conduct specialized activities, and engage in risky projects. They can be organized in a variety of different forms and structures. Some joint ventures are primarily contractual relationships, whereas others have common ownership of assets. They can be partnerships, corporations, or other legal forms (unincorporated associations, for example).

Joint ventures are defined differently under IFRS and U.S. GAAP. This can result in the same arrangement being classified differently under the two standards. In turn, this can affect reported financial results, ratios, and covenants.

IFRS identify the following common characteristics of joint ventures: (1) contractual arrangement exists between two or more venturers and (2) the contractual arrangement establishes joint control. IFRS distinguish between three types of joint ventures with each type having specific accounting requirements, although proportionate consolidation is the generally preferred accounting treatment. Proportionate consolidation requires the venturer’s share of the assets, liabilities, income, and expenses of the joint venture to be combined on a line-by-line basis with similar items on the venturer’s financial statements. The three types of joint venture identified under IFRS are:

1. Jointly controlled operations: Each venturer uses its own assets and other resources for a specific project, rather than establishing a separate entity from the venturers. For example, two or more venturers combine their operations, resources, and expertise to manufacture, market, and distribute jointly a particular product. Each venturer recognizes in its financial statements the assets that it controls, the liabilities and expenses that it incurs, and its share of the revenue generated by the joint venture.

2. Jointly controlled assets: The venturers jointly control and/or jointly own assets. These assets are used to obtain benefits for the venturers. For example, oil production companies may jointly control and operate an oil pipeline. Each venturer recognizes in its own accounting records and financial statements its share of the jointly controlled assets (classified by the nature of the assets), any liabilities it has incurred on behalf of those assets as well as its share of jointly incurred liabilities, any profit earned from the use of its share of the jointly controlled assets, together with its share of any expense incurred by the joint venture. In addition, it would recognize any expense (for example, interest expense related to financing the venturer’s interest in the assets) it has incurred directly in respect of its interest in the joint venture.

3. Jointly controlled entities: The predominant arrangement involves the establishment of a separate entity (corporation, partnership) in which each venturer has an interest. The project or venture is then conducted through this incorporated or unincorporated separate entity. The entity operates in the same way as other entities, except that a contractual arrangement between the venturers establishes joint control over the economic activity of the entity. To account for this arrangement, IFRS recommends using proportionate consolidation but permits the equity method.20

Proportionate consolidation requires the venturer’s share of the assets, liabilities, income, and expenses of the joint venture to be combined on a line-by-line basis with similar items on the venturer’s financial statements.21 In contrast, as explained in Section 4, the equity method results in a single line item (equity in income of the joint venture) on the income statement and a single line item (investment in joint venture) on the balance sheet.

Because the single line item on the income statement under the equity method reflects the net effect of the sales and expenses of the joint venture, the total income recognized is identical under the two methods. In addition, because the single line item on the balance sheet item (investment in joint venture) under the equity method reflects the investors’ share of the net assets of the joint venture, the total net assets of the investor is identical under both methods. There can be significant differences, however, in ratio analysis between the two methods because of the differential effects on values for total assets, liabilities, sales, expenses, and so forth.

Under U.S. GAAP the term joint venture refers only to a jointly controlled separate entity in which business activities are conducted. A corporate joint venture is a corporation that is owned and operated by two or more venturers as a separate and specific business for the mutual benefit of the venturers.22 U.S. GAAP requires the use of the equity method to account for joint ventures. Proportionate consolidation is generally not permitted except for unincorporated entities operating in certain industries.

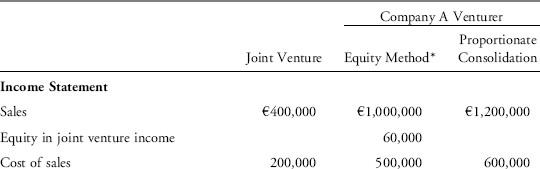

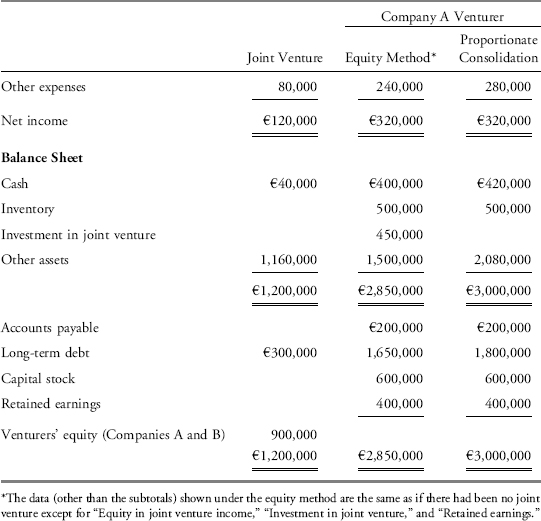

EXAMPLE 14-7 Joint Venture (Jointly Controlled Entity)

Assume that hypothetical Companies A and B enter into a joint venture, each with a 50 percent interest. The second column presents the financial statement for the joint venture in its first year. Columns 3 and 4 reflect the financial results for Company A under the two methods of accounting for its interest in the joint venture.

First, examine the income statement. Notice that net income is €320,000 using either the equity method or proportionate consolidation. But sales, cost of sales, and expenses are different because under the equity method the net effect of sales, cost of sales, and expenses is reflected in the €60,000 equity in joint venture income.

On the balance sheet, the line item “investment in joint venture” observed under the equity method is replaced by the proportionate share of each balance sheet account in the proportionate consolidation method. The single line item is replaced with a line-by-line consolidation. In other words, because the venturer has a 50 percent interest in the joint venture, 50 percent of joint venture assets and liabilities are included in the proportionate balance sheet.

The analyst will observe differences in performance ratios based on the accounting method used for joint ventures.

| Equity Method | Proportionate Consolidation | |

| Net profit margin | 32.0% | 26.7% |

| Return on assets | 11.2% | 10.7% |

| Debt/Equity | 1.65 | 1.80 |

The proportional consolidation method is the preferred method for joint ventures under IFRS because it more effectively conveys the economic scope of an entity’s operations when those operations include interests in one or more jointly controlled entities.

Business combinations (controlling interest investments) involve the combination of two or more entities into a larger economic entity. Business combinations are typically motivated by expectations of added value through synergies, including elimination of duplicate costs, tax advantages, coordination of the production process, and efficiency gains in the management of assets.

Under IFRS, there is no distinction among business combinations based on the resulting structure of the larger economic entity. For all business combinations, one of the parties to the business combination is identified as the acquirer. Under U.S. GAAP, an acquirer is identified, but business combinations are categorized as merger, acquisition, or consolidation based on the structure after the combination. Each of these types of business combinations has distinctive characteristics that are described in Exhibit 14-5. Exhibit 14-5 also describes the features of variable interest and special purpose entities. Variable interest and special purpose entities are additional instances where control is exerted by another entity.

Exhibit 14-5 Types of Business Combinations

Merger

The distinctive feature of a merger is that only one of the entities remains in existence. One hundred percent of the target is absorbed into the acquiring company. Company A may issue common stock, preferred stock, bonds, or pay cash to acquire the net assets. The net assets of Company B are transferred to Company A. Company B ceases to exist and Company A is the only entity that remains.

![]()

Acquisition

The distinctive feature of an acquisition is the legal continuity of the entities. Each entity continues operations but is connected through a parent–subsidiary relationship. Each entity is an individual that maintains separate financial records, but the parent (the acquirer) provides consolidated financial statements in each reporting period. Unlike a merger or consolidation, the acquiring company does not need to acquire 100 percent of the target. In fact, in some cases, it may acquire less than 50 percent and still exert control (see Section 6.4.2). If the acquiring company acquires less than 100 percent, noncontrolling (minority) shareholders’ interests are reported on the consolidated financial statements.

![]()

Consolidation

The distinctive feature of a consolidation is that a new legal entity is formed and none of the predecessor entities remain in existence. A new entity is created to take over the net assets of Company A and Company B. Company A and Company B cease to exist and Company C is the only entity that remains.

![]()

Special Purpose Entities

The distinctive feature of a special purpose (variable interest) entity is that control is not usually based on voting control, because equity investors do not have a sufficient amount at risk for the entity to finance its activities without additional subordinated financial support. Furthermore, the equity investors may lack a controlling financial interest. The sponsoring company usually creates a special purpose entity (SPE) for a narrowly defined purpose. IFRS require consolidation if the substance of the relationship indicates control by the sponsor. Variable interests will be discussed more thoroughly in Section 7.

In the past, business combinations could be accounted for either as a purchase transaction or as a uniting (or pooling) of interests. The accounting standards that currently govern business combinations are reflective of the joint project between IASB and FASB to converge on a single set of high-quality accounting standards. As part of the first phase of the project, in 2001 the FASB issued SFAS 141, Business Combinations and SFAS 142, Goodwill and other Intangible Assets.23 In 2004, the IASB issued IFRS 3, Business Combinations. These standards prohibited the use of the pooling of interests (uniting of interest) method, required the use of the acquisition (purchase) method, and prohibited the amortization of goodwill.

In the second phase of the joint project, the FASB and IASB further reduced differences between IFRS and U.S. GAAP and ensured that the standards would be applied consistently. In December 2007, the FASB issued two new standards, SFAS 141(R), Business Combinations, and SFAS 160, Noncontrolling Interests in Consolidated Financial Statements.24 Both statements applied prospectively to business combinations occurring on or after 15 December 2008, with early adoption prohibited. In January 2008, the IASB issued a revised IFRS 3, Business Combinations and an amended IAS 27, Consolidated and Separate Financial Statements. These “new” standards became effective on 1 July 2009, although entities were permitted to adopt them earlier. These standards are expected to improve the relevance, representational faithfulness, transparency, and comparability of information provided in financial statements about business combinations and their effects on the reporting entity.

IFRS and U.S. GAAP now require that all business combinations be accounted for as acquisitions, whereby one entity (the parent) takes management control of another entity (subsidiary), or the parent takes control of the subsidiary’s assets and liabilities.25 The acquisition method developed by the IASB and the FASB replaces the purchase method, and substantially reduces any differences between IFRS and U.S. GAAP for business combinations. By requiring acquirers to account for business combinations in a similar manner, it should make it easier for analysts to evaluate how the operations of acquirer and the target business will combine and the effect of this combination on the combined entity’s subsequent financial performance and position.

6.1. Pooling of Interests

Prior to June 2001, under U.S. GAAP, combining companies that met twelve strict criteria could use the pooling of interests accounting method for the business combination. Companies not meeting these criteria used the purchase method. In a pooling of interests, the combined companies were portrayed as if they had always operated as a single economic entity. Consequently, assets and liabilities were recorded at book values, and the precombination retained earnings were included in the balance sheet of the combined companies. This treatment was consistent with the view that there was a continuity of ownership and no new basis of accounting existed. Similar rules applied under IFRS, which used the term uniting of interests in reference to the same concept. IFRS permitted use of the uniting of interests method until March 2004. Currently, neither IFRS nor U.S. GAAP allows use of the pooling/uniting of interests method.

In contrast, a combination accounted for as a purchase is viewed as a purchase of net assets, and those net assets are recorded at fair values. An increase in the value of depreciable assets resulted in additional depreciation expense. As a result, for the same level of revenue, the purchase method resulted in lower reported income than the pooling of interests method. For this reason, managers had a tendency to favor the pooling of interests method.

Although the pooling of interests method is no longer allowed, companies may continue to use pooling of interests accounting for business combinations that occurred prior to its disallowance as a method. We discuss the method here because pooling of interests accounting was commonly used and will have an impact on financial statements for the foreseeable future. Because of the ongoing effect, an understanding of pooling of interests will facilitate the analyst’s assessment of the performance and financial position of the company.

6.2. Acquisition Method

IFRS and U.S. GAAP currently require the acquisition method of accounting for business combinations, although both have a few specific exemptions.