CHAPTER 2

FINANCIAL REPORTING MECHANICS

After completing this chapter, you will be able to do the following:

- Explain the relationship of financial statement elements and accounts and classify accounts into the financial statement elements.

- Explain the accounting equation in its basic and expanded forms.

- Explain the process of recording business transactions using an accounting system based on the accounting equation.

- Explain the need for accruals and other adjustments in preparing financial statements.

- Explain the relationships among the income statement, balance sheet, statement of cash flows, and statement of owners’ equity.

- Describe the flow of information in an accounting system.

- Explain the use of the results of the accounting process in security analysis.

The financial statements of a company are end-products of a process for recording transactions of the company related to operations, financing, and investment. The structures of financial statements themselves reflect the system of recording and organizing transactions. To be an informed user of financial statements, the analyst must be knowledgeable about the principles of this system. This chapter will supply that essential knowledge, taking the perspective of the user rather than the preparer. Learning the process from this perspective will enable an analyst to grasp the critical concepts without being overwhelmed by the detailed technical skills required by the accountants who prepare financial statements that are a major component of financial reports.

This chapter is organized as follows: Section 2 describes the three groups into which business activities are classified for financial reporting purposes. Any transaction affects one or more of these groups. Section 3 describes how the elements of financial statements relate to accounts, the basic content unit of classifying transactions. The section is also an introduction to the linkages among the financial statements. Section 4 provides a step-by-step illustration of the accounting process. Section 5 explains the consequences of timing differences between the elements of a transaction. Section 6 provides an overview of how information flows through a business’s accounting system. Section 7 introduces the use of financial reporting in security analysis, and Section 8 presents a summary of key points. Practice problems in the CFA Institute multiple-choice format conclude the chapter.

2. THE CLASSIFICATION OF BUSINESS ACTIVITIES

Accountants give similar accounting treatment to similar types of business transactions. Therefore, a first step in understanding financial reporting mechanics is to understand how business activities are classified for financial reporting purposes.

Business activities may be classified into three groups for financial reporting purposes: operating, investing, and financing activities.

1. Operating activities are those activities that are part of the day-to-day business functioning of an entity. Examples include the sale of meals by a restaurant, the sale of services by a consulting firm, the manufacture and sale of ovens by an oven-manufacturing company, and taking deposits and making loans by a bank.

2. Investing activities are those activities associated with acquisition and disposal of long-term assets. Examples include the purchase of equipment or sale of surplus equipment (such as an oven) by a restaurant (contrast this to the sale of an oven by an oven manufacturer, which would be an operating activity), and the purchase or sale of an office building, a retail store, or a factory.

3. Financing activities are those activities related to obtaining or repaying capital. The two primary sources for such funds are owners (shareholders) or creditors. Examples include issuing common shares, taking out a bank loan, and issuing bonds.

Understanding the nature of activities helps the analyst understand where the company is doing well and where it is not doing so well. Ideally, an analyst would prefer that most of a company’s profits (and cash flow) come from its operating activities. Exhibit 2-1 provides examples of typical business activities and how these activities relate to the elements of financial statements described in the following section.

EXHIBIT 2-1 Typical Business Activities and Financial Statement Elements Affected

| Assets (A), Liabilities (L), Owners’ Equity (E), Revenue (R), and Expenses (X) | |

| Operating activities | Sales of goods and services to customers: (R) Costs of providing the goods and services: (X) Income tax expense: (X) Holding short-term assets or incurring short-term liabilities directly related to operating activities: (A), (L) |

| Investing activities | Purchase or sale of assets, such as property, plant, and equipment: (A) Purchase or sale of other entities’ equity and debt securities: (A) |

| Financing activities | Issuance or repurchase of the company’s own preferred or common stock: (E) Issuance or repayment of debt: (L) Payment of distributions (i.e., dividends to preferred or common stockholders): (E) |

Not all transactions fit neatly in this framework for purposes of financial statement presentation. For example, interest received by a bank on one of its loans would be considered part of operating activities because a bank is in the business of lending money. In contrast, interest received on a bond investment by a restaurant may be more appropriately classified as an investing activity because the restaurant is not in the business of lending money.

The next section discusses how transactions resulting from these business activities are reflected in a company’s financial records.

3. ACCOUNTS AND FINANCIAL STATEMENTS

Business activities resulting in transactions are reflected in the broad groupings of financial statement elements: Assets, Liabilities, Owners’ Equity, Revenue, and Expenses.1 In general terms, these elements can be defined as follows: assets are the economic resources of a company; liabilities are the creditors’ claims on the resources of a company; owners’ equity is the residual claim on those resources; revenues are inflows of economic resources to the company; and expenses are outflows of economic resources or increases in liabilities.2

Accounts provide individual records of increases and decreases in a specific asset, liability, component of owners’ equity, revenue, or expense. The financial statements are constructed using these elements.

3.1 Financial Statement Elements and Accounts

Within the financial statement elements, accounts are subclassifications. Accounts are individual records of increases and decreases in a specific asset, liability, component of owners’ equity, revenue, or expense. For financial statements, amounts recorded in every individual account are summarized and grouped appropriately within a financial statement element. Exhibit 2-2 provides a listing of common accounts. These accounts will be described throughout this chapter or in following chapters. Unlike the financial statement elements, there is no standard set of accounts applicable to all companies. Although almost every company has certain accounts, such as cash, each company specifies the accounts in its accounting system based on its particular needs and circumstances. For example, a company in the restaurant business may not be involved in trading securities and, therefore, may not need an account to record such an activity. Furthermore, each company names its accounts based on its business. A company in the restaurant business might have an asset account for each of its ovens, with the accounts named “Oven-1” and “Oven-2.” In its financial statements, these accounts would likely be grouped within long-term assets as a single line item called “Property, plant, and equipment.”

A company’s challenge is to establish accounts and account groupings that provide meaningful summarization of voluminous data but retain enough detail to facilitate decision making and preparation of the financial statements. The actual accounts used in a company’s accounting system will be set forth in a chart of accounts. Generally, the chart of accounts is far more detailed than the information presented in financial statements.

Certain accounts are used to offset other accounts. For example, a common asset account is accounts receivable, also known as “trade accounts receivable” or “trade receivables.” A company uses this account to record the amounts it is owed by its customers. In other words, sales made on credit are reflected in accounts receivable. In connection with its receivables, a company often expects some amount of uncollectible accounts and, therefore, records an estimate of the amount that may not be collected. The estimated uncollectible amount is recorded in an account called allowance for bad debts. Because the effect of the allowance for bad debts account is to reduce the balance of the company’s accounts receivable, it is known as a “contra asset account.” Any account that is offset or deducted from another account is called a “contra account.” Common contra asset accounts include allowance for bad debts (an offset to accounts receivable for the amount of accounts receivable that are estimated to be uncollectible), accumulated depreciation (an offset to property, plant, and equipment reflecting the amount of the cost of property, plant, and equipment that has been allocated to current and previous accounting periods), and sales returns and allowances (an offset to revenue reflecting any cash refunds, credits on account, and discounts from sales prices given to customers who purchased defective or unsatisfactory items).

EXHIBIT 2-2 Common Accounts

| Assets | Cash and cash equivalents Accounts receivable, trade receivables Prepaid expenses Inventory Property, plant, and equipment Investment property Intangible assets (patents, trademarks, licenses, copyright, goodwill) Financial assets, trading securities, investment securities Investments accounted for by the equity method Current and deferred tax assets [for banks, Loans (receivable)] |

| Liabilities | Accounts payable, trade payables Provisions or accrued liabilities Financial liabilities Current and deferred tax liabilities Reserves Minority interest Unearned revenue Debt payable Bonds (payable) [for banks, Deposits] |

| Owners’ Equity | Capital, such as common stock par value Additional paid-in capital Retained earnings Other comprehensive income |

| Revenue | Revenue, sales Gains Investment income (e.g., interest and dividends) |

| Expense | Cost of goods sold Selling, general, and administrative expenses “SG&A” (e.g., rent, utilities, salaries, advertising) Depreciation and amortization Interest expense Tax expense Losses |

For presentation purposes, assets are sometimes categorized as “current” or “noncurrent.” For example, Tesco (a large European retailer) presents the following major asset accounts in its 2006 financial reports:

Noncurrent assets

- Intangible assets including goodwill.

- Property, plant, and equipment.

- Investment property.

- Investments in joint ventures and associates.

Current assets

- Inventories.

- Trade and other receivables.

- Cash and cash equivalents.

Noncurrent assets are assets that are expected to benefit the company over an extended period of time (usually more than one year). For Tesco, these include the following: intangible assets, such as goodwill;3 property, plant, and equipment used in operations (e.g., land and buildings); other property held for investment, and investments in the securities of other companies.

Current assets are those that are expected to be consumed or converted into cash in the near future, typically one year or less. Inventories are the unsold units of product on hand (sometimes referred to as inventory stock). Trade receivables (also referred to as commercial receivables, or simply accounts receivable) are amounts customers owe the company for products that have been sold as well as amounts that may be due from suppliers (such as for returns of merchandise). Other receivables represent amounts owed to the company from parties other than customers. Cash refers to cash on hand (e.g., petty cash and cash not yet deposited to the bank) and in the bank. Cash equivalents are very liquid short-term investments, usually maturing in 90 days or less. The presentation of assets as current or noncurrent will vary from industry to industry and from country to country. Some industries present current assets first, whereas others list noncurrent assets first. This is discussed further in later chapters.

3.2. Accounting Equations

The five financial statement elements noted previously serve as the inputs for equations that underlie the financial statements. This section describes the equations for three of the financial statements: balance sheet, income statement, and statement of retained earnings. A statement of retained earnings can be viewed as a component of the statement of stockholders’ equity, which shows all changes to owners’ equity, both changes resulting from retained earnings and changes resulting from share issuance or repurchase. The fourth basic financial statement, the statement of cash flows, will be discussed in a later section.

The balance sheet presents a company’s financial position at a particular point in time. It provides a listing of a company’s assets and the claims on those assets (liabilities and equity claims). The equation that underlies the balance sheet is also known as the “basic accounting equation.” A company’s financial position is reflected using the following equation:

Presented in this form, it is clear that claims on assets are from two sources: liabilities or owners’ equity. Owners’ equity is the residual claim of the owners (i.e., the owners’ remaining claim on the company’s assets after the liabilities are deducted). The concept of the owners’ residual claim is well illustrated by the slightly rearranged balance sheet equation, roughly equivalent to the structure commonly seen in the balance sheets of U.K. companies:

Other terms are used to denote owners’ equity, including shareholders’ equity, stockholders’ equity, net assets, equity, net worth, net book value, and partners’ capital. The exact titles depend upon the type of entity, but the equation remains the same. Owners’ equity at a given date can be further classified by its origin: capital contributed by owners, and earnings retained in the business up to that date:4

The income statement presents the performance of a business for a specific period of time. The equation reflected in the income statement is the following:

Note that net income (loss) is the difference between two of the elements: revenue and expenses. When a company’s revenue exceeds its expenses, it reports net income; when a company’s revenues are less than its expenses, it reports a net loss. Other terms are used synonymously with revenue, including sales and turnover (in the United Kingdom). Other terms used synonymously with net income include net profit and net earnings.

Also, as noted earlier, revenue and expenses generally relate to providing goods or services in a company’s primary business activities. In contrast, gains (losses) relate to increases (decreases) in resources that are not part of a company’s primary business activities. Distinguishing a company’s primary business activities from other business activities is important in financial analysis; however, for purposes of the accounting equation, gains are included in revenue and losses are included in expenses.

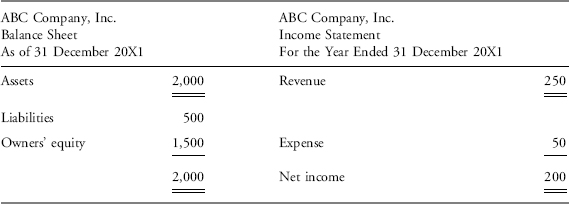

The balance sheet and income statement are two of the primary financial statements. Although these are the common terms for these statements, some variations in the names occur. A balance sheet can be referred to as a “statement of financial position” or some similar term that indicates it contains balances at a point in time. Income statements can be titled “statement of operations,” “statement of income,” “statement of profit and loss,” or some other similar term showing that it reflects the company’s operating activity for a period of time. A simplified balance sheet and income statement are shown in Exhibit 2-3.

EXHIBIT 2-3 Simplified Balance Sheet and Income Statement

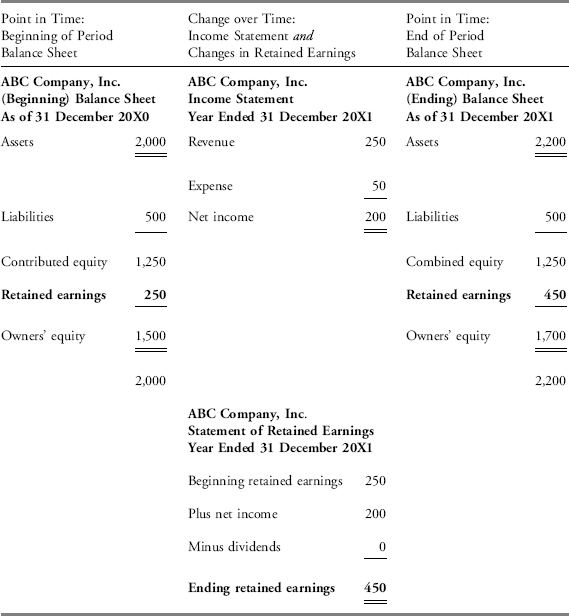

The balance sheet represents a company’s financial position at a point in time, and the income statement represents a company’s activity over a period of time. The two statements are linked together through the retained earnings component of owners’ equity. Beginning retained earnings is the balance in this account at the beginning of the accounting period, and ending retained earnings is the balance at the end of the period. A company’s ending retained earnings is composed of the beginning balance (if any), plus net income, less any distributions to owners (dividends). Accordingly, the equation underlying retained earnings is:

Or, substituting Equation 2.3 for Net income, equivalently:

As its name suggests, retained earnings represent the earnings (i.e., net income) that are retained by the company—in other words, the amount not distributed as dividends to owners. Retained earnings is a component of owners’ equity and links the “as of” balance sheet equation with the “activity” equation of the income statement. To provide a combined representation of the balance sheet and income statement, we can substitute Equation 2.2 into Equation 2.1a. This becomes the expanded accounting equation:

Or equivalently, substituting Equation 2.4b into Equation 2.5a, we can write:

The last five items, beginning with contributed capital, are components of owners’ equity.

The statement of retained earnings shows the linkage between the balance sheet and income statement. Exhibit 2-4 shows a simplified example of financial statements for a company that began the year with retained earnings of $250 and recognized $200 of net income during the period. The example assumes the company paid no dividends and, therefore, had ending retained earnings of $450.

EXHIBIT 2-4 Simplified Balance Sheet, Income Statement, and Statement of Retained Earnings

The basic accounting equation reflected in the balance sheet (Assets=Liabilities+Owners’ equity) implies that every recorded transaction affects at least two accounts in order to keep the equation in balance, hence the term double-entry accounting that is sometimes used to describe the accounting process. For example, the use of cash to purchase equipment affects two accounts (both asset accounts): cash decreases and equipment increases. As another example, the use of cash to pay off a liability also affects two accounts (one asset account and one liability account): cash decreases and the liability decreases. With each transaction, the accounting equation remains in balance, which is a fundamental accounting concept. Example 2-1 presents a partial balance sheet for an actual company and an application of the accounting equation. Examples 2-2 and 2-3 provide further practice for applying the accounting equations.

EXAMPLE 2-1 Using Accounting Equations (1)

Canon is a manufacturer of copy machines and other electronic equipment. Abbreviated balance sheets as of 31 December 2004 and 2005 are presented next.

Canon and Subsidiaries: Consolidated Balance Sheets (millions of yen)

| 31 Dec 2005 | 31 Dec 2004 | |

| Assets | ||

| Total assets | ¥4,043,553 | ¥3,587,021 |

| Liabilities and stockholders’ equity | ||

| Total liabilities | 1,238,535 | 1,190,331 |

| Total stockholders’ equity | ? | 2,396,690 |

| Total liabilities and stockholders’ equity | ¥4,043,553 | ¥3,587,021 |

Using Equation 2.1a, address the following:

1. Determine the amount of stockholders’ equity as of 31 December 2005.

2. A. Calculate and contrast the absolute change in total assets in 2005 with the absolute change in total stockholders’ equity in 2005.

B. Based on your answer to 2A, state and justify the relative importance of growth in stockholders’ equity and growth in liabilities in financing the growth of assets over the two years.

Solution to 1: Total stockholders’ equity is equal to assets minus liabilities; in other words, it is the residual claim to the company’s assets after deducting liabilities. For 2005, the amount of Canon’s total stockholders’ equity was thus ¥4,043,553 million − ¥1,238,535 million=¥2,805,018 million in 2005.

Solutions to 2:

A. Total assets increased by ¥4,043,553 million − ¥3,587,021 million=¥456,532 million. Total stockholders’ equity increased by ¥2,805,018 million − ¥2,396,690 million=¥408,328 million. Thus, in 2005, total assets grew by more than total stockholders’ equity (¥456,532 million is larger than ¥408,328 million).

B. Using the relationship Assets=Liabilities+Owners’ equity, the solution to 2A implies that total liabilities increased by the difference between the increase in total assets and the increase in total stockholders’ equity, that is, by ¥456,532 million − ¥408,328 million=¥48,204 million. (If liabilities had not increased by ¥48,204 million, the accounting equation would not be in balance.) Contrasting the growth in total stockholders’ equity (¥408,328 million) with the growth in total liabilities (¥48,204 million), we see that the growth in stockholders’ equity was relatively much more important than the growth in liabilities in financing total asset growth in 2005.

Having described the components and linkages of financial statements in abstract terms, we now examine more concretely how business activities are recorded. The next section illustrates the accounting process with a simple step-by-step example.

EXAMPLE 2-2 Using Accounting Equations (2)

An analyst has collected the following information regarding a company in advance of its year-end earnings announcement (amounts in millions):

| Estimated net income | $150 |

| Beginning retained earnings | $2,000 |

| Estimated distributions to owners | $50 |

The analyst’s estimate of ending retained earnings (in millions) should be closest to

A. $2,000.

B. $2,100.

C. $2,150.

D. $2,200.

Solution: B is correct. Beginning retained earnings is increased by net income and reduced by distributions to owners: $2,000+$150 − $50=$2,100.

EXAMPLE 2-3 Using Accounting Equations (3)

An analyst has compiled the following information regarding RDZ, Inc.

| Liabilities at year-end | €1,000 |

| Contributed capital at year-end | €1,000 |

| Beginning retained earnings | €500 |

| Revenue during the year | €4,000 |

| Expenses during the year | €3,800 |

There have been no distributions to owners. The analyst’s estimate of total assets at year-end should be closest to

A. €2,000.

B. €2,300.

C. €2,500.

D. €2,700.

Solution: D is correct. Ending retained earnings is first determined by adding revenue minus expenses to beginning retained earnings to obtain €700. Total assets would be equal to the sum of liabilities, contributed capital, and ending retained earnings: €1,000+€1,000+€700=€2,700.

The accounting process involves recording business transactions such that periodic financial statements can be prepared. This section illustrates how business transactions are recorded in a simplified accounting system.

4.1. An Illustration

Key concepts of the accounting process can be more easily explained using a simple illustration. We look at an illustration in which three friends decide to start a business, Investment Advisers, Ltd. (IAL). They plan to issue a monthly newsletter of securities trading advice and to sell investment books. Although they do not plan to manage any clients’ funds, they will manage a trading portfolio of the owners’ funds to demonstrate the success of the recommended strategies from the newsletter. Because this illustration is meant to present accounting concepts, any regulatory implications will not be addressed. Additionally, for this illustration, we will assume that the entity will not be subject to income taxes; any income or loss will be passed through to the owners and be subject to tax on their personal income tax returns.

As the business commences, various business activities occur. Exhibit 2-5 provides a listing of the business activities that have taken place in the early stages of operations. Note that these activities encompass the types of operating, investing, and financing business activities discussed previously.

4.2. The Accounting Records

If the owners want to evaluate the business at the end of January 2006, Exhibit 2-5 does not provide a sufficiently meaningful report of what transpired or where the company currently stands. It is clear that a system is needed to track this information and to address three objectives:

1. Identify those activities requiring further action (e.g., collection of outstanding receivable balances).

2. Assess the profitability of the operations over the month.

3. Evaluate the current financial position of the company (such as cash on hand).

An accounting system will translate the company’s business activities into usable financial records. The basic system for recording transactions in this illustration is a spreadsheet with each of the different types of accounts represented by a column. The accounting equation provides a basis for setting up this system. Recall the accounting Equation 2.5b:

![]()

EXHIBIT 2-5 Business Activities for Investment Advisers, Ltd.

| Date | Business Activity | |

| 1 | 31 December 2005 | File documents with regulatory authorities to establish a separate legal entity. Initially capitalize the company through deposit of $150,000 from the three owners. |

| 2 | 2 January 2006 | Set up a $100,000 investment account and purchase a portfolio of equities and fixed-income securities. |

| 3 | 2 January 2006 | Pay $3,000 to landlord for office/warehouse. $2,000 represents a refundable deposit, and $1,000 represents the first month’s rent. |

| 4 | 3 January 2006 | Purchase office equipment for $6,000. The equipment has an estimated life of two years with no salvage value.5 |

| 5 | 3 January 2006 | Receive $1,200 cash for a one-year subscription to the monthly newsletter. |

| 6 | 10 January 2006 | Purchase and receive 500 books at a cost of $20 per book for a total of $10,000. Invoice terms are that payment from IAL is due in 30 days. No cash changes hands. These books are intended for resale. |

| 7 | 10 January 2006 | Spend $600 on newspaper and trade magazine advertising for the month. |

| 8 | 15 January 2006 | Borrow $12,000 from a bank for working capital. Interest is payable annually at 10 percent. The principal is due in two years. |

| 9 | 15 January 2006 | Ship first order to a customer consisting of five books at $25 per book. Invoice terms are that payment is due in 30 days. No cash changes hands. |

| 10 | 15 January 2006 | Sell for cash 10 books at $25 per book at an investment conference. |

| 11 | 30 January 2006 | Hire a part-time clerk. The clerk is hired through an agency that also handles all payroll taxes. The company is to pay $15 per hour to the agency. The clerk works six hours prior to 31 January, but no cash will be paid until February. |

| 12 | 31 January 2006 | Mail out the first month’s newsletter to customer. This subscription had been sold on 3 January. See item 5. |

| 13 | 31 January 2006 | Review of the investment portfolio shows that $100 of interest income was earned and the market value of the portfolio has increased by $2,000. The balance in the investment account is now $102,100. The securities are classified as “trading” securities. |

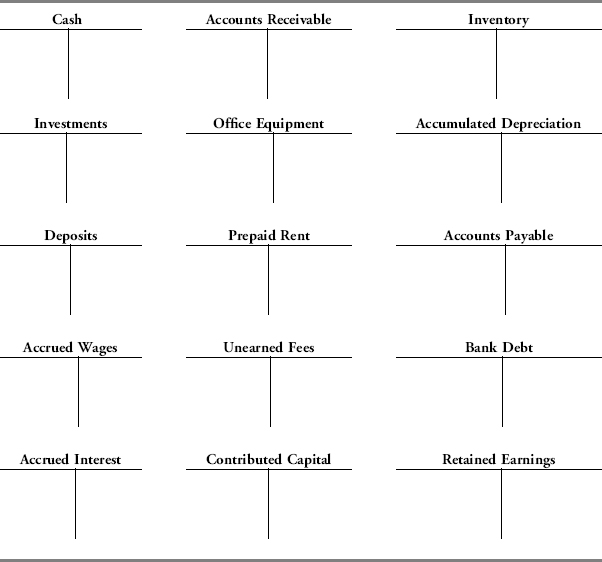

The specific accounts to be used for IAL’s system include the following:

Asset Accounts:

Cash

Investments

Prepaid rent (cash paid for rent in advance of recognizing the expense)

Rent deposit (cash deposited with the landlord, but returnable to the company)

Office equipment

Inventory

Accounts receivable

Liability Accounts:

Unearned fees (fees that have not been earned yet, even though cash has been received)

Accounts payable (amounts owed to suppliers)

Bank debt

Equity Accounts:

Contributed capital

Retained earnings

Income

Revenue

Expenses

Dividends

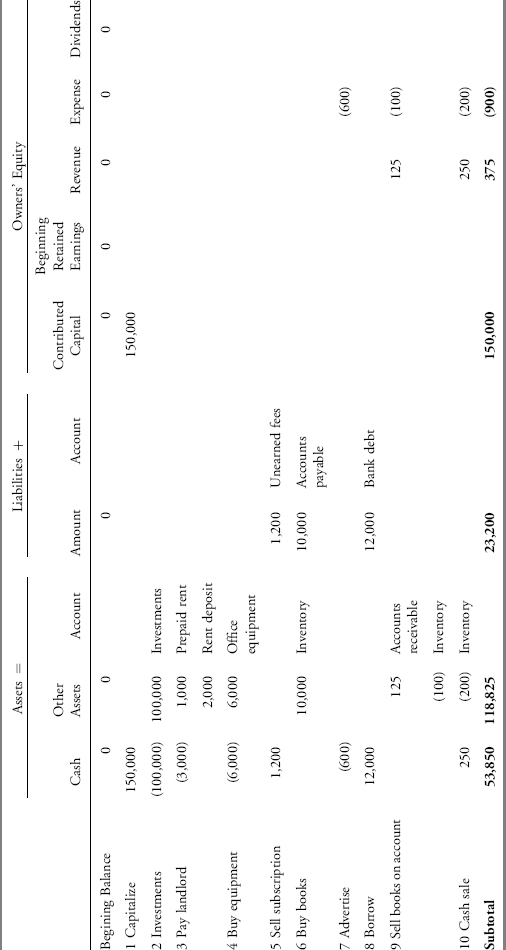

Exhibit 2-6 presents the spreadsheet representing IAL’s accounting system for the first 10 transactions. Each event is entered on a new row of the spreadsheet as it occurs. To record events in the spreadsheet, the financial impact of each needs to be assessed and the activity expressed as an accounting transaction. In assessing the financial impact of each event and converting these events into accounting transactions, the following steps are taken:

1. Identify which accounts are affected, by what amount, and whether the accounts are increased or decreased.

2. Determine the element type for each account identified in Step 1 (e.g., cash is an asset) and where it fits in the basic accounting equation. Rely on the economic characteristics of the account and the basic definitions of the elements to make this determination.

3. Using the information from Steps 1 and 2, enter the amounts in the appropriate column of the spreadsheet.

4. Verify that the accounting equation is still in balance.

At any point in time, basic financial statements can be prepared based on the subtotals in each column.

The following discussion identifies the accounts affected and the related element (Steps 1 and 2) for the first 10 events listed in Exhibit 2-5. The accounting treatment shows the account affected in bold and the related element in brackets. The recording of these entries into a basic accounting system (Steps 3 and 4) is depicted on the spreadsheet in Exhibit 2-6.

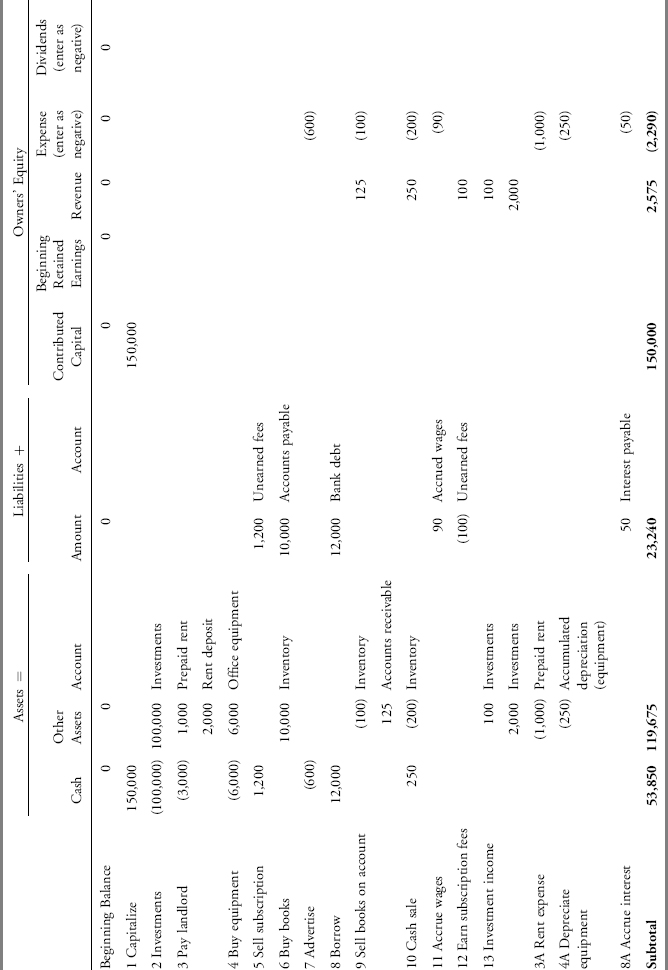

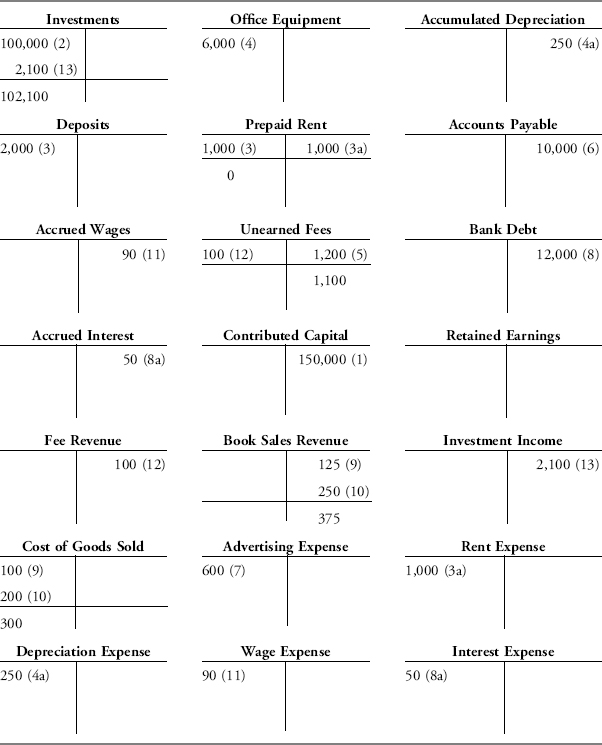

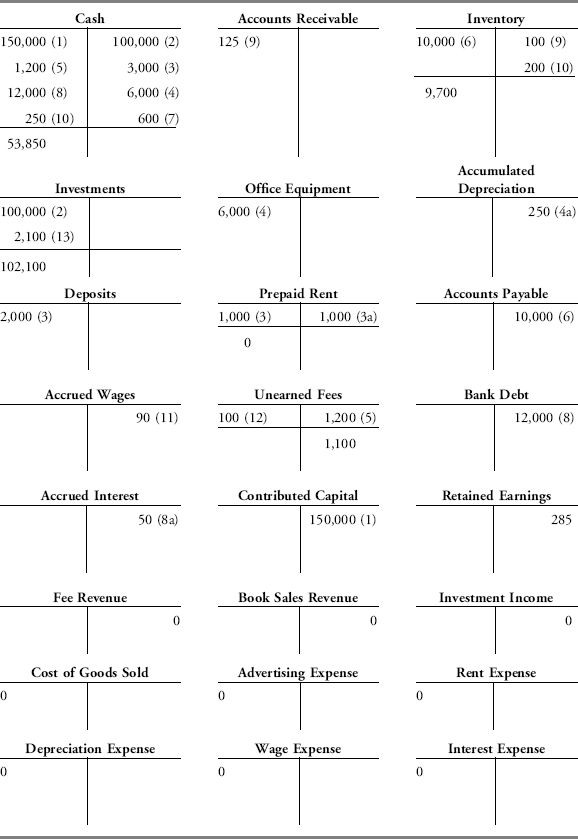

EXHIBIT 2-6 Accounting System for Investment Advisers, Ltd.

Because this is a new business, the accounting equation begins at zero on both sides. There is a zero beginning balance in all accounts.

31 December 2005

| Business Activity | Accounting Treatment | |

| 1 | File documents with regulatory authorities to establish a separate legal entity. Initially capitalize the company through deposit of $150,000 from the three owners. | Cash [A] is increased by $150,000, and contributed capital [E]6 is increased by $150,000. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

This transaction affects two elements: assets and equity. Exhibit 2-6 demonstrates this effect on the accounting equation. The company’s balance sheet at this point in time would be presented by subtotaling the columns in Exhibit 2-6:

Investment Advisers, Ltd. Balance Sheet As of 31 December 2005

| Assets | |

| Cash | $150,000 |

| Total assets | $150,000 |

| Liabilities and owners’ equity | |

| Contributed capital | $150,000 |

| Total liabilities and owners’ equity | $150,000 |

The company has assets (resources) of $150,000, and the owners’ claim on the resources equals $150,000 (their contributed capital) as there are no liabilities at this point.

For this illustration, we present an unclassified balance sheet. An unclassified balance sheet is one that does not show subtotals for current assets and current liabilities. Assets are simply listed in order of liquidity (how quickly they are expected to be converted into cash). Similarly, liabilities are listed in the order in which they are expected to be satisfied (or paid off).

2 January 2006

| Business Activity | Accounting Treatment | |

| 2 | Set up a $100,000 investment account and purchase a portfolio of equities and fixed-income securities. | Investments[A] were increased by $100,000, and cash [A] was decreased by $100,000. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

This transaction affects two accounts, but only one element (assets) and one side of the accounting equation, as depicted in Exhibit 2-6. Cash is reduced when the securities are purchased. Another type of asset, investments, increases. We examine the other transaction from 2 January before taking another look at the company’s balance sheet.

2 January 2006

| Business Activity | Accounting Treatment | |

| 3 | Pay $3,000 to landlord for office/warehouse. $2,000 represents a refundable deposit, and $1,000 represents the first month’s rent. | Cash [A] was decreased by $3,000, deposits [A] were increased by $2,000, and prepaid rent [A] was increased by $1,000. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

Once again, this transaction affects only asset accounts. Note that the first month’s rent is initially recorded as an asset, prepaid rent. As time passes, the company will incur rent expense, so a portion of this prepaid asset will be transferred to expenses and thus will appear on the income statement as an expense.7 This will require a later adjustment in our accounting system. Note that the transactions so far have had no impact on the income statement. At this point in time, the company’s balance sheet would be:

Investment Advisers, Ltd. Balance Sheet As of 2 January 2006

| Assets | |

| Cash | $47,000 |

| Investments | 100,000 |

| Prepaid rent | 1,000 |

| Deposits | 2,000 |

| Total assets | $150,000 |

| Liabilities and owners’ equity | |

| Contributed capital | $150,000 |

| Total liabilities and owners’ equity | $150,000 |

Note that the items in the balance sheet have changed, but it remains in balance; the amount of total assets equals total liabilities plus owners’ equity. The company still has $150,000 in resources, but the assets now comprise cash, investments, prepaid rent, and deposits. Each asset is listed separately because they are different in terms of their ability to be used by the company. Note also that the owners’ equity claim on these assets remains $150,000 because the company still has no liabilities.

3 January 2006

| Business Activity | Accounting Treatment | |

| 4 | Purchase office equipment for $6,000 in cash. The equipment has an estimated life of two years with no salvage value. | Cash [A] was decreased by $6,000, and office equipment [A] was increased by $6,000. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

The company has once again exchanged one asset for another. Cash has decreased while office equipment has increased. Office equipment is a resource that will provide benefits over multiple future periods and, therefore, its cost must also be spread over multiple future periods. This will require adjustments to our accounting records as time passes. Depreciation is the term for the process of spreading this cost over multiple periods.

3 January 2006

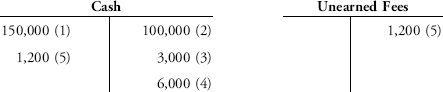

| Business Activity | Accounting Treatment | |

| 5 | Receive $1,200 cash for a one-year subscription to the monthly newsletter. | Cash [A] was increased by $1,200, and unearned fees [L] was increased by $1,200. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

In this transaction, the company has received cash related to the sale of subscriptions. However, the company has not yet actually earned the subscription fees because it has an obligation to deliver newsletters in the future. So, this amount is recorded as a liability called unearned fees (or unearned revenue). In the future, as the company delivers the newsletters and thus fulfills its obligation, this amount will be transferred to revenue. If the company fails to deliver the newsletters, the fees will need to be returned to the customer. As of 3 January 2006, the company’s balance sheet would appear as

Investment Advisers, Ltd. Balance Sheet As of 3 January 2006

| Assets | |

| Cash | $42,200 |

| Investments | 100,000 |

| Prepaid rent | 1,000 |

| Deposits | 2,000 |

| Office equipment | 6,000 |

| Total assets | $151,200 |

| Liabilities and owners’ equity | |

| Liabilities | |

| Unearned fees | $1,200 |

| Equity | |

| Contributed capital | 150,000 |

| Total liabilities and owners’ equity | $151,200 |

The company now has $151,200 of resources, against which there is a claim by the subscription customer of $1,200 and a residual claim by the owners of $150,000. Again, the balance sheet remains in balance, with total assets equal to total liabilities plus equity.

10 January 2006

| Business Activity | Accounting Treatment | |

| 6 | Purchase and receive 500 books at a cost of $20 per book for a total of $10,000. Invoice terms are that payment from IAL is due in 30 days. No cash changes hands. These books are intended for resale. | Inventory [A] is increased by $10,000, and accounts payable [L] is increased by $10,000. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

The company has obtained an asset, inventory, which can be sold to customers at a later date. Rather than paying cash to the supplier currently, the company has incurred an obligation to do so in 30 days. This represents a liability to the supplier that is termed accounts payable.

10 January 2006

| Business Activity | Accounting Treatment | |

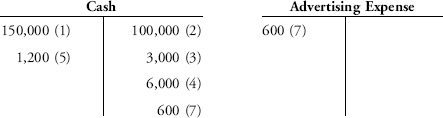

| 7 | Spend $600 on newspaper and trade magazine advertising for the month. | Cash [A] was decreased by $600, and advertising expense [X] was increased by $600. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

Unlike the previous expenditures, advertising is an expense, not an asset. Its benefits relate to the current period. Expenditures such as advertising are recorded as an expense when they are incurred. Contrast this expenditure with that for equipment, which is expected to be useful over multiple periods and thus is initially recorded as an asset, and then reflected as an expense over time. Also, contrast this treatment with that for rent expense, which was paid in advance and can be clearly allocated over time, and thus is initially recorded as a prepaid asset and then reflected as an expense over time. The advertising expenditure in this example relates to the current period. If the company had paid in advance for several years’ worth of advertising, then a portion would be capitalized (i.e., recorded as an asset), similar to the treatment of equipment or prepaid rent and expensed in future periods. We can now prepare a partial income statement for the company reflecting this expense:

Investment Advisers, Ltd. Income Statement For the Period 1 January through 10 January 2006

| Total revenue | $0 |

| Expenses Advertising | 600 |

| Total expense | 600 |

| Net income (loss) | $(600) |

Because the company has incurred a $600 expense but has not recorded any revenue (the subscription revenue has not been earned yet), an income statement for Transactions 1 through 7 would show net income of minus $600 (i.e., a net loss). To prepare a balance sheet for the company, we need to update the retained earnings account. Beginning retained earnings was $0 (zero). Adding the net loss of $600 (made up of $0 revenue minus $600 expense) and deducting any dividend ($0 in this illustration) gives ending retained earnings of minus $600. The ending retained earnings covering Transactions 1–7 is included in the interim balance sheet:

Investment Advisers, Ltd. Balance Sheet As of 10 January 2006

| Assets | |

| Cash | $41,600 |

| Investments | 100,000 |

| Inventory | 10,000 |

| Prepaid rent | 1,000 |

| Deposits | 2,000 |

| Office equipment | 6,000 |

| Total assets | $160,600 |

| Liabilities and owners’ equity | |

| Liabilities | |

| Accounts payable | $10,000 |

| Unearned fees | 1,200 |

| Total liabilities | 11,200 |

| Equity | |

| Contributed capital | 150,000 |

| Retained earnings | (600) |

| Total equity | 149,400 |

| Total liabilities and owners’ equity | $160,600 |

As with all balance sheets, the amount of total assets equals total liabilities plus owners’ equity—both are $160,600. The owners’ claim on the business has been reduced to $149,400. This is due to the negative retained earnings (sometimes referred to as a retained “deficit”). As noted, the company has a net loss after the first seven transactions, a result of incurring $600 of advertising expenses but not yet producing any revenue.

15 January 2006

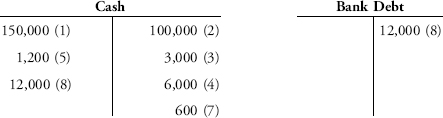

| Business Activity | Accounting Treatment | |

| 8 | Borrow $12,000 from a bank for working capital. Interest is payable annually at 10 percent. The principal is due in two years. | Cash [A] is increased by $12,000, and bank debt [L] is increased by $12,000. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

Cash is increased, and a corresponding liability is recorded to reflect the amount owed to the bank. Initially, no entry is made for interest that is expected to be paid on the loan. In the future, interest will be recorded as time passes and interest accrues (accumulates) on the loan.

15 January 2006

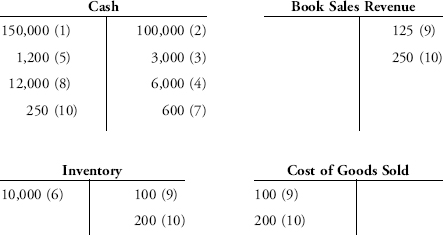

| Business Activity | Accounting Treatment | |

| 9 | Ship first order to a customer consisting of five books at $25 per book. Invoice terms are that payment is due in 30 days. No cash changes hands. | Accounts receivable [A] increased by $125, and revenue [R] increased by $125. Additionally, inventory [A] decreased by $100, and cost of goods sold [X] increased by $100. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

The company has now made a sale. Sale transaction records have two parts. One part represents the $125 revenue to be received from the customer, and the other part represents the $100 cost of the goods that have been sold. Although payment has not yet been received from the customer in payment for the goods, the company has delivered the goods (five books) and so revenue is recorded. A corresponding asset, accounts receivable, is recorded to reflect amounts due from the customer. Simultaneously, the company reduces its inventory balance by the cost of the five books sold and also records this amount as an expense termed cost of goods sold.

15 January 2006

| Business Activity | Accounting Treatment | |

| 10 | Sell for cash 10 books at $25 per book at an investment conference. | Cash[A] is increased by $250, and revenue[R] is increased by $250. Additionally, inventory[A] is decreased by $200, and cost of goods sold [X] is increased by $200. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

Similar to the previous sale transaction, both the $250 sales proceeds and the $200 cost of the goods sold must be recorded. In contrast with the previous sale, however, the sales proceeds are received in cash. Subtotals from Exhibit 2-6 can once again be used to prepare a preliminary income statement and balance sheet to evaluate the business to date:

Investment Advisers, Ltd. Income Statement For the Period 1 January through 15 January 2006

| Total revenue | $375 |

| Expenses | |

| Cost of goods sold | 300 |

| Advertising | 600 |

| Total expenses | 900 |

| Net income (loss) | $(525) |

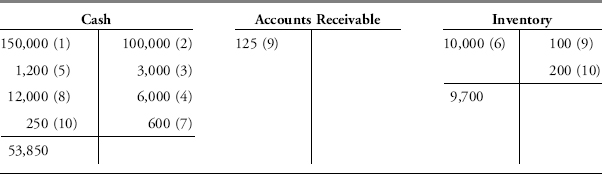

Investment Advisers, Ltd. Balance Sheet As of 15 January 2006

| Assets | |

| Cash | $53,850 |

| Accounts receivable | 125 |

| Investments | 100,000 |

| Inventory | 9,700 |

| Prepaid rent | 1,000 |

| Deposits | 2,000 |

| Office equipment | 6,000 |

| Total assets | $172,675 |

| Liabilities and owners’ equity | |

| Liabilities | |

| Accounts payable | $10,000 |

| Unearned fees | 1,200 |

| Bank debt | 12,000 |

| Total liabilities | 23,200 |

| Equity | |

| Contributed capital | 150,000 |

| Retained earnings | (525) |

| Total equity | 149,475 |

| Total liabilities and owners’ equity | $172,675 |

An income statement covering Transactions 1–10 would reflect revenue to date of $375 for the sale of books minus the $300 cost of those books and minus the $600 advertising expense. The net loss is $525, which is shown in the income statement as $(525) using the accounting convention that indicates a negative number using parentheses. This net loss is also reflected on the balance sheet in retained earnings. The amount in retained earnings at this point equals the net loss of $525 because retained earnings had $0 beginning balance and no dividends have been distributed. The balance sheet reflects total assets of $172,675 and claims on the assets of $23,200 in liabilities and $149,475 owners’ equity. Within assets, the inventory balance represents the cost of the 485 remaining books (a total of 15 have been sold) at $20 each.

Transactions 1–10 occurred throughout the month and involved cash, accounts receivable, or accounts payable; accordingly, these transactions clearly required an entry into the accounting system. The other transactions, items 11–13, have also occurred and need to be reflected in the financial statements, but these transactions may not be so obvious. In order to prepare complete financial statements at the end of a reporting period, an entity needs to review its operations to determine whether any accruals or other adjustments are required. A more complete discussion of accruals and adjustments is set forth in the next section, but generally speaking, such entries serve to allocate revenue and expense items into the correct accounting period. In practice, companies may also make adjustments to correct erroneous entries or to update inventory balances to reflect a physical count.

In this illustration, adjustments are needed for a number of transactions in order to allocate amounts across accounting periods. The accounting treatment for these transactions is shown in Exhibit 2-7. Transactions are numbered sequentially, and an “a” is added to a transaction number to denote an adjustment relating to a previous transaction. Exhibit 2-8 presents the completed spreadsheet reflecting these additional entries in the accounting system.

EXHIBIT 2-7 Investment Advisers Ltd. Accruals and Other Adjusting Entries on 31 January 2006

| Items 11–13 are repeated from Exhibit 2-5. | ||

| Items 3a, 4a, and 8a reflect adjustments relating to items 3, 4, and 8 from Exhibit 2-5. | ||

| Business Activity | Accounting Treatment | |

| 11 | Hire a part-time clerk. The clerk is hired through an agency that also handles all payroll taxes. The company is to pay $15 per hour to the agency. The clerk works six hours prior to 31 January, but no cash will be paid until February. | The company owes $90 for wages at month end. Under accrual accounting, expenses are recorded when incurred, not when paid. Accrued wages [L] is increased by $90, and payroll expense [X] is increased by $90. The accrued wage liability will be eliminated when the wages are paid. |

| 12 | Mail out the first month’s newsletter to customer. This subscription had been sold on 3 January. | One month (or 1/12) of the $1,200 subscription has been satisfied, so $100 can be recognized as revenue. Unearned fees [L] is decreased by $100, and fee revenue [R] is increased by $100. |

| 13 | Review of the investment portfolio shows that $100 of interest income was earned and the market value of the portfolio has increased by $2,000. The balance in the investment account is now $102,100. The securities are classified as “trading” securities. | Interest income [R] is increased by $100, and the investments account [A] is increased by $100. The $2,000 increase in the value of the portfolio represents unrealized gains that are part of income for traded securities. The investments account [A] is increased by $2,000, and unrealized gains [R] is increased by $2,000. |

| 3a | In item 3, $3,000 was paid to the landlord for office/warehouse, including a $2,000 refundable deposit and $1,000 for the first month’s rent. Now, the first month has ended, so this rent has become a cost of doing business. |

To reflect the full amount of the first month’s rent as a cost of doing business, prepaid rent [A] is decreased by $1,000, and rent expense [X] is increased by $1,000. |

| 4a | In item 4, office equipment was purchased for $6,000 in cash. The equipment has an estimated life of two years with no salvage value. Now, one month (or 1/24) of the useful life of the equipment has ended, so a portion of the equipment cost has become a cost of doing business. |

A portion (1/24) of the total $6,000 cost of the office equipment is allocated to the current period’s cost of doing business. Depreciation expense [X] is increased by $250, and accumulated depreciation [A] (a contra asset account) is increased by $250. Accumulated depreciation is a contra asset account to office equipment. |

| 8a | The company borrowed $12,000 from a bank on 15 January, with interest payable annually at 10 percent and the principal due in two years. Now, one-half of one month has passed since the borrowing. |

One-half of one month of interest expense has become a cost of doing business. $12,000 × 10%=$1,200 of annual interest, equivalent to $100 per month or $50 for one-half month. Interest expense [X] is increased by $50, and interest payable [L] is increased by $50. |

Accounting Elements: Assets (A), Liabilities (L), Equity (E), Revenue (R), and Expenses (X)

EXHIBIT 2-8 Accounting System for Investment Advisers, Ltd.

A final income statement and balance sheet can now be prepared reflecting all transactions and adjustments.

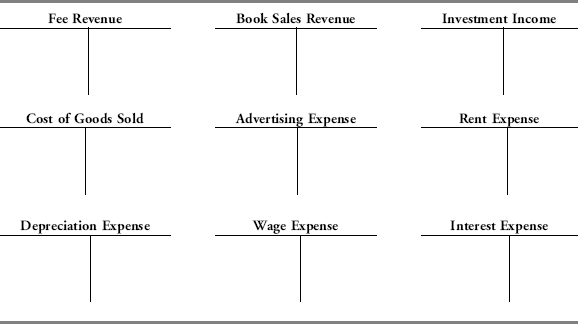

Investment Advisers, Ltd. Income Statement For the Period 1 January through 31 January 2006

| Revenues | |

| Fee revenue | $100 |

| Book sales | 375 |

| Investment income | 2,100 |

| Total revenues | $2,575 |

| Expenses | |

| Cost of goods sold | $300 |

| Advertising | 600 |

| Wage | 90 |

| Rent | 1,000 |

| Depreciation | 250 |

| Interest | 50 |

| Total expenses | 2,290 |

| Net income (loss) | $285 |

Investment Advisers, Ltd. Balance Sheet As of 31 January 2006

| Assets | |

| Cash | $53,850 |

| Accounts receivable | 125 |

| Investments | 102,100 |

| Inventory | 9,700 |

| Prepaid rent | 0 |

| Office equipment, net | 5,750 |

| Deposits | 2,000 |

| Total assets | $173,525 |

| Liabilities and owners’ equity | |

| Liabilities | |

| Accounts payable | $10,000 |

| Accrued wages | 90 |

| Interest payable | 50 |

| Unearned fees | 1,100 |

| Bank debt | 12,000 |

| Total liabilities | 23,240 |

| Equity | |

| Contributed capital | 150,000 |

| Retained earnings | 285 |

| Total equity | 150,285 |

| Total liabilities and owners’ equity | $173,525 |

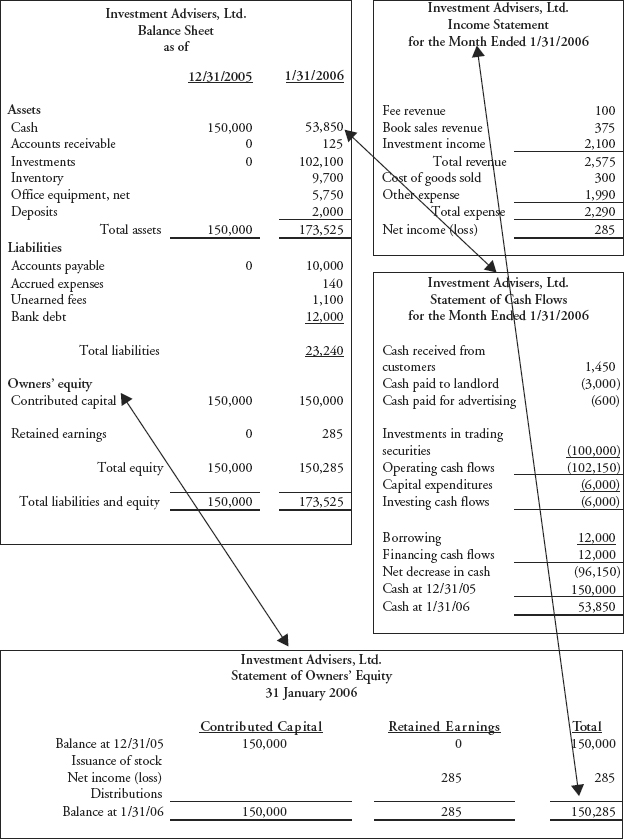

From the income statement, we can determine that the business was profitable for the month. The business earned $285 after expenses. The balance sheet presents the financial position. The company has assets of $173,525, and claims against those assets included liabilities of $23,240 and an owners’ claim of $150,285. The owners’ claim reflects their initial investment plus reinvested earnings. These statements are explored further in the next section.

4.3. Financial Statements

The spreadsheet in Exhibit 2-8 is an organized presentation of the company’s transactions and can help in preparing the income statement and balance sheet presented above. Exhibit 2-9 presents all financial statements and demonstrates their relationships. Note that the data for the income statement come from the revenue and expense columns of the spreadsheet (which include gains and losses). The net income of $285 (revenue of $2,575 minus expenses of $2,290) was retained in the business rather than distributed to the owners as dividends. The net income, therefore, becomes part of ending retained earnings on the balance sheet. The detail of retained earnings is shown in the statement of owners’ equity.

The balance sheet presents the financial position of the company using the assets, liabilities, and equity accounts from the accounting system spreadsheet. The statement of cash flows summarizes the data from the cash column of the accounting system spreadsheet to enable the owners and others to assess the sources and uses of cash. These sources and uses of cash are categorized according to group of business activity: operating, investing, or financing. The format of the statement of cash flows presented here is known as the direct format, which refers to the operating cash section appearing simply as operating cash receipts less operating cash disbursements. An alternative format for the operating cash section, which begins with net income and shows adjustments to derive operating cash flow, is known as the indirect format. The alternative formats and detailed rules are discussed in the chapter on cash flow statements.

Financial statements use the financial data reported in the accounting system and present this data in a more meaningful manner. Each statement reports on critical areas. Specifically, a review of the financial statements for the IAL illustration provides the following information:

- Balance Sheet. This statement provides information about a company’s financial position at a point in time. It shows an entity’s assets, liabilities, and owners’ equity at a particular date. Two years are usually presented so that comparisons can be made. Less significant accounts can be grouped into a single line item. One observation from the IAL illustration is that although total assets have increased significantly (about 16 percent), equity has increased less than 0.2 percent—most of the increase in total assets is due to the increase in liabilities.

- Income Statement. This statement provides information about a company’s profitability over a period of time. It shows the amount of revenue, expense, and resulting net income or loss for a company during a period of time. Again, less significant accounts can be grouped into a single line item—in this illustration, expenses other than cost of goods sold are grouped into a single line item. The statement shows that IAL has three sources of revenue and made a small profit in its first month of operations. Significantly, most of the revenue came from investments rather than subscriptions or book sales.

- Statement of Cash Flows. This statement provides information about a company’s cash flows over a period of time. It shows a company’s cash inflows (receipts) and outflows (payments) during the period. These flows are categorized according to the three groups of business activities: operating, financing, and investing. In the illustration, IAL reported a large negative cash flow from operations ($102,150), primarily because its trading activities involved the purchase of a portfolio of securities but no sales were made from the portfolio. (Note that the purchase of investments for IAL appears in its operating section because the company is in the business of trading securities. In contrast, for a nontrading company, investment activity would be shown as investing cash flows rather than operating cash flows.) IAL’s negative operating and investing cash flows were funded by $12,000 bank borrowing and a $96,150 reduction in the cash balance.

EXHIBIT 2-9 Investment Advisers, Ltd. Financial Statements

- Statement of Owners’ Equity. This statement provides information about the composition and changes in owners’ equity during a period of time. In this illustration, the only change in equity resulted from the net income of $285. A Statement of Retained Earnings (not shown) would report the changes in a company’s retained earnings during a period of time.

These statements again illustrate the interrelationships among financial statements. On the Balance Sheet, we see beginning and ending amounts for assets, liabilities, and owners’ equity. Owners’ equity increased from $150,000 to $150,285. The Statement of Owners’ Equity presents a breakdown of this $285 change. The arrow from the statement of owners’ equity to the owners’ equity section of the balance sheet explains that section of the balance sheet. In the IAL illustration, the entire $285 change resulted from an increase in retained earnings. In turn, the increase in retained earnings resulted from $285 net income. The Income Statement presents a breakdown of the revenues and expenses resulting in this $285. The arrow from the income statement to the net income figure in the owners’ equity section explains how reported net income came about.

Also on the Balance Sheet, we see that cash decreased from $150,000 at the beginning of the month to $53,850 at the end of the month. The Statement of Cash Flows provides information on the increases and decreases in cash by group of business activity. The arrow from the cash flow statement to the ending cash figure shows that the cash flow statement explains in detail the ending cash amount.

In summary, the balance sheet provides information at a point in time (financial position), whereas the other statements provide useful information regarding the activity during a period of time (profitability, cash flow, and changes in owners’ equity).

5. ACCRUALS AND VALUATION ADJUSTMENTS

In a simple business model such as the investment company discussed in the illustration above, many transactions are handled in cash and settled in a relatively short time frame. Furthermore, assets and liabilities have a fixed and determinable value. Translating business transactions into the accounting system is fairly easy. Difficulty usually arises when a cash receipt or disbursement occurs in a different period than the related revenue or expense, or when the reportable values of assets vary. This section will address the accounting treatment for these situations—namely, accruals and valuation adjustments.

5.1. Accruals

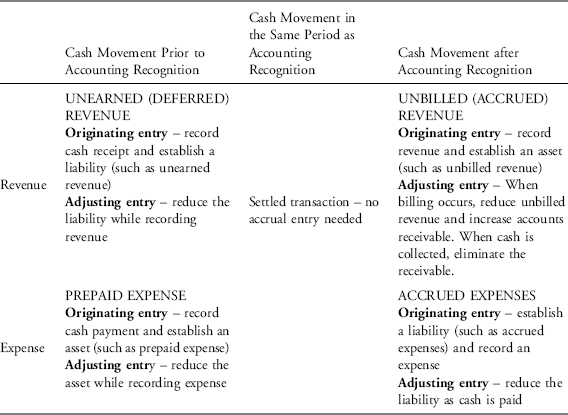

Accrual accounting requires that revenue be recorded when earned and that expenses be recorded when incurred, irrespective of when the related cash movements occur. The purpose of accrual entries is to report revenue and expense in the proper accounting period. Because accrual entries occur due to timing differences between cash movements and accounting recognition of revenue or expense, it follows that there are only a few possibilities. First, cash movement and accounting recognition can occur at the same time, in which case there is no need for accruals. Second, cash movement may occur before or after accounting recognition, in which case accruals are required. The possible situations requiring accrual entries are summarized into four types of accrual entries shown in Exhibit 2-10 and discussed below. Each type of accrual involves an originating entry and at least one adjusting entry at a later date or dates.

EXHIBIT 2-10 Accruals

Unearned (or deferred) revenue arises when a company receives cash prior to earning the revenue. In the IAL illustration, in Transaction 5, the company received $1,200 for a 12-month subscription to a monthly newsletter. At the time the cash was received, the company had an obligation to deliver 12 newsletters and thus had not yet earned the revenue. Each month, as a newsletter is delivered, this obligation will decrease by 1/12th (i.e., $100). And at the same time, $100 of revenue will be earned. The accounting treatment involves an originating entry (the initial recording of the cash received and the corresponding liability to deliver newsletters) and, subsequently, 12 future adjusting entries, the first one of which was illustrated as Transaction 12. Each adjusting entry reduces the liability and records revenue.

In practice, a large amount of unearned revenue may cause some concern about a company’s ability to deliver on this future commitment. Conversely, a positive aspect is that increases in unearned revenue are an indicator of future revenues. For example, a large liability on the balance sheet of an airline relates to cash received for future airline travel. Revenue will be recognized as the travel occurs, so an increase in this liability is an indicator of future increases in revenue.

Unbilled (or accrued) revenue arises when a company earns revenue prior to receiving cash but has not yet recognized the revenue at the end of an accounting period. In such cases, the accounting treatment involves an originating entry to record the revenue earned through the end of the accounting period and a related receivable reflecting amounts due from customers. When the company receives payment (or if goods are returned), an adjusting entry eliminates the receivable.

Accrued revenue specifically relates to end-of-period accruals; however, the concept is similar to any sale involving deferred receipt of cash. In the IAL illustration, in Transaction 9, the company sold books on account, so the revenue was recognized prior to cash receipt. The accounting treatment involved an entry to record the revenue and the associated receivable. In the future, when the company receives payment, an adjusting entry (not shown) would eliminate the receivable. In practice, it is important to understand the quality of a company’s receivables (i.e., the likelihood of collection).

Prepaid expense arises when a company makes a cash payment prior to recognizing an expense. In the illustration, in Transaction 3, the company prepaid one month’s rent. The accounting treatment involves an originating entry to record the payment of cash and the prepaid asset reflecting future benefits, and a subsequent adjusting entry to record the expense and eliminate the prepaid asset. (See the boxes showing the accounting treatment of Transaction 3, which refers to the originating entry, and Transaction 3a, which refers to the adjusting entry.) In other words, prepaid expenses are assets that will be subsequently expensed. In practice, particularly in a valuation, one consideration is that prepaid assets typically have future value only as future operations transpire, unless they are refundable.

Accrued expenses arise when a company incurs expenses that have not yet been paid as of the end of an accounting period. Accrued expenses result in liabilities that usually require future cash payments. In the IAL illustration, the company had incurred wage expenses at month end, but the payment would not be made until after the end of the month (Transaction 11). To reflect the company’s position at the end of the month, the accounting treatment involved an originating entry to record wage expense and the corresponding liability for wages payable, and a future adjusting entry to eliminate the liability when cash is paid (not shown because wages will be paid only in February). Similarly, the IAL illustration included interest accrual on the company’s bank borrowing. (See the boxes showing the accounting treatment of Transaction 8, where Transaction 8 refers to the originating entry, and Transaction 8a, which refers to the adjusting entry.)

As with accrued revenues, accrued expenses specifically relate to end-of-period accruals. Accounts payable are similar to accrued expenses in that they involve a transaction that occurs now but the cash payment is made later. Accounts payable is also a liability but often relates to the receipt of inventory (or perhaps services) as opposed to recording an immediate expense. Accounts payable should be listed separately from other accrued expenses on the balance sheet because of their different nature.

Overall, in practice, complex businesses require additional accruals that are theoretically similar to the four categories of accruals discussed above but which require considerably more judgment. For example, there may be significant lags between a transaction and cash settlement. In such cases, accruals can span many accounting periods (even 10–20 years!), and it is not always clear when revenue has been earned or an expense has been incurred. Considerable judgment is required to determine how to allocate/distribute amounts across periods. An example of such a complex accrual would be the estimated annual revenue for a contractor on a long-term construction project, such as building a nuclear power plant. In general, however, accruals fall under the four general types and follow essentially the same pattern of originating and adjusting entries as the basic accruals described.

5.2. Valuation Adjustments

In contrast to accrual entries that allocate revenue and expenses into the appropriate accounting periods, valuation adjustments are made to a company’s assets or liabilities—only where required by accounting standards—so that the accounting records reflect the current market value rather than the historical cost. In this discussion, we focus on valuation adjustments to assets. For example, in the IAL illustration, Transaction 13 adjusted the value of the company’s investment portfolio to its current market value. The income statement reflects the $2,100 increase (including interest), and the ending balance sheets report the investment portfolio at its current market value of $102,100. In contrast, the equipment in the IAL illustration was not reported at its current market value and no valuation adjustment was required.

As this illustration demonstrates, accounting regulations do not require all types of assets to be reported at their current market value. Some assets (e.g., trading securities) are shown on the balance sheet at their current market value, and changes in that market value are reported in the income statement. Some assets are shown at their historical cost (e.g., specific classes of investment securities being held to maturity). Other assets (e.g., a particular class of investment securities) are shown on the balance sheet at their current market value, but changes in market value bypass the income statement and are recorded directly into shareholders’ equity under a component referred to as “other comprehensive income.” This topic will be discussed in more detail in later chapters.

In summary, where valuation adjustment entries are required for assets, the basic pattern is the following for increases in assets: An asset is increased with the other side of the equation being a gain on the income statement or an increase to other comprehensive income. Conversely for decreases: An asset is decreased with the other side of the equation being a loss on the income statement or a decrease to other comprehensive income.

The accounting system set forth for the IAL illustration involved a very simple business, a single month of activity, and a small number of transactions. In practice, most businesses are more complicated and have many more transactions. Accordingly, actual accounting systems, although using essentially the same logic as discussed in the illustration, are both more efficient than a spreadsheet and more complex.

6.1. Flow of Information in an Accounting System

Accounting texts typically discuss accounting systems in detail because accountants need to understand each step in the process. While analysts do not need to know the same details, they should be familiar with the flow of information through a financial reporting system. This flow and the key related documents are described in Exhibit 2-11.

6.2. Debits and Credits

Reviewing the example of IAL, it is clear that the accounting treatment of every transaction involved at least two accounts and the transaction either increased or decreased the value of any affected account. Traditionally, accounting systems have used the terms debit and credit to describe changes in an account resulting from the accounting processing of a transaction. The correct usage of “debit” and “credit” in an accounting context differs from how these terms are used in everyday language.8 The accounting definitions of debit and credit ensure that, in processing a transaction, the sum of the debits equals the sum of the credits, which is consistent with the accounting equation (i.e., Equation 2.7) always remaining in balance.

EXHIBIT 2-11 Accounting System Flow and Related Documents

| Journal entries and adjusting entries | A journal is a document or computer file in which business transactions are recorded in the order in which they occur (chronological order). The general journal is the collection of all business transactions in an accounting system sorted by date. All accounting systems have a general journal to record all transactions. Some accounting systems also include special journals. For example, there may be one journal for recording sales transactions and another for recording inventory purchases. |

| Journal entries—recorded in journals—are dated, and show the accounts affected and the amounts. If necessary, the entry will include an explanation of the transaction and documented authorization to record the entry. As the initial step in converting business transactions into financial information, the journal entry is useful for obtaining detailed information regarding a particular transaction. | |

| Adjusting journal entries, a subset of journal entries, are typically made at the end of an accounting period to record items such as accruals that are not yet reflected in the accounting system. | |

| ↓ | |

| General ledger and T-accounts | A ledger is a document or computer file that shows all business transactions by account. Note that the general ledger, the core of every accounting system, contains all of the same entries as that posted to the general journal—the only difference is that the data are sorted by date in a journal and by account in the ledger. The general ledger is useful for reviewing all of the activity related to a single account. T-accounts, explained in Appendix 2A, are representations of ledger accounts and are frequently used to describe or analyze accounting transactions. |

| ↓ | |

| Trial balance and adjusted trial balance | A trial balance is a document that lists account balances at a particular point in time. Trial balances are typically prepared at the end of an accounting period as a first step in producing financial statements. A key difference between a trial balance and a ledger is that the trial balance shows only total ending balances. An initial trial balance assists in the identification of any adjusting entries that may be required. Once these adjusting entries are made, an adjusted trial balance can be prepared. |

| ↓ | |

| Financial statements | The financial statements, a final product of the accounting system, are prepared based on the account totals from an adjusted trial balance. |

Although mastering the usage of the terms “debit” and “credit” is essential for an accountant, an analyst can still understand financial reporting mechanics without speaking in terms of debits and credits. In general, this text avoids the use of debit/credit presentation; however, for reference, Appendix 2A presents the IAL illustration in a debit and credit system.

The following section broadly describes some considerations for using financial statements in security analysis.

7. USING FINANCIAL STATEMENTS IN SECURITY ANALYSIS

Financial statements serve as a foundation for credit and equity analysis, including security valuation. Analysts may need to make adjustments to reflect items not reported in the statements (certain assets/liabilities and future earnings). Analysts may also need to assess the reasonableness of management judgment (e.g., in accruals and valuations). Because analysts typically will not have access to the accounting system or individual entries, they will need to infer what transactions were recorded by examining the financial statements.

7.1. The Use of Judgment in Accounts and Entries

Quite apart from deliberate misrepresentations, even efforts to faithfully represent the economic performance and position of a company require judgments and estimates. Financial reporting systems need to accommodate complex business models by recording accruals and changes in valuations of balance sheet accounts. Accruals and valuation entries require considerable judgment and thus create many of the limitations of the accounting model. Judgments could prove wrong or, worse, be used for deliberate earnings manipulation. An important first step in analyzing financial statements is identifying the types of accruals and valuation entries in an entity’s financial statements. Most of these items will be noted in the critical accounting policies/estimates section of management’s discussion and analysis (MD&A) and in the significant accounting policies footnote, both found in the annual report. Analysts should use this disclosure to identify the key accruals and valuations for a company. The analyst needs to be aware, as Example 2-4 shows, that the manipulation of earnings and assets can take place within the context of satisfying the mechanical rules governing the recording of transactions.

EXAMPLE 2-4 The Manipulation of Accounting Earnings

As discussed in this chapter, the accounting equation can be expressed as Assets=Liabilities+Contributed capital+Ending retained earnings (Equation 2.5a). Although the equation must remain in balance with each transaction, management can improperly record a transaction to achieve a desired result. For example, when a company spends cash and records an expense, assets are reduced on the left side of the equation and expenses are recorded, which lowers retained earnings on the right side. The balance is maintained. If, however, a company spent cash but did not want to record an expense in order to achieve higher net income, the company could manipulate the system by reducing cash and increasing another asset. The equation would remain in balance and the right-hand side of the equation would not be affected at all. This was one of the techniques used by managers at WorldCom to manipulate financial reports, as summarized in a U.S. Securities and Exchange Commission complaint against the company (emphasis added):

In general, WorldCom manipulated its financial results in two ways. First, WorldCom reduced its operating expenses by improperly releasing certain reserves held against operating expenses. Second, WorldCom improperly reduced its operating expenses by recharacterizing certain expenses as capital assets. Neither practice was in conformity with generally accepted accounting principles (“GAAP”). Neither practice was disclosed to WorldCom’s investors, despite the fact that both practices constituted changes from WorldCom’s previous accounting practices. Both practices falsely reduced WorldCom’s expenses and, accordingly, had the effect of artificially inflating the income WorldCom reported to the public in its financial statements from 1999 through the first quarter of 2002.9

In 2005, the former CEO of WorldCom was sentenced to 25 years in prison for his role in the fraud.10 The analyst should be aware of the possibility of manipulation of earnings and be on the lookout for large increases in existing assets, new unusual assets, and unexplained changes in financial ratios.

7.2. Misrepresentations

It is rare in this age of computers that the mechanics of an accounting system do not work. Most computer accounting systems will not allow a company to make one-sided entries. It is important to note, however, that just because the mechanics work does not necessarily mean that the judgments underlying the financial statements are correct. An unscrupulous accountant could structure entries to achieve a desired result. For example, if a manager wanted to record fictitious revenue, a fictitious asset (a receivable) could be created to keep the accounting equation in balance. If the manager paid for something but did not want to record an expense, the transaction could be recorded in a prepaid asset account. If cash is received but the manager does not want to record revenue, a liability could be created. Understanding that there has to be another side to every entry is key in detecting inappropriate accounting because—usually in the course of “fixing” one account—there will be another account with a balance that does not make sense. In the case of recording fictitious revenue, there is likely to be a growing receivable whose collectability is in doubt. Ratio analysis, which is discussed further in later chapters, can assist in detecting suspect amounts in these accounts. Furthermore, the accounting equation can be used to detect likely accounts where aggressive or even fraudulent accounting may have occurred.

The accounting process is a key component of financial reporting. The mechanics of this process convert business transactions into records necessary to create periodic reports on a company. An understanding of these mechanics is useful in evaluating financial statements for credit and equity analysis purposes and in forecasting future financial statements. Key concepts are as follows:

- Business activities can be classified into three groups: operating activities, investing activities, and financing activities.

- Companies classify transactions into common accounts that are components of the five financial statement elements: assets, liabilities, equity, revenue, and expense.

- The core of the accounting process is the basic accounting equation: Assets=Liabilities+Owners’ equity.

- The expanded accounting equation is Assets=Liabilities+Contributed capital+Beginning retained earnings+Revenue − Expenses − Dividends.

- Business transactions are recorded in an accounting system that is based on the basic and expanded accounting equations.

- The accounting system tracks and summarizes data used to create financial statements: the balance sheet, income statement, statement of cash flows, and statement of owners’ equity. The statement of retained earnings is a component of the statement of owners’ equity.

- Accruals are a necessary part of the accounting process and are designed to allocate activity to the proper period for financial reporting purposes.

- The results of the accounting process are financial reports that are used by managers, investors, creditors, analysts, and others in making business decisions.

- An analyst uses the financial statements to make judgments on the financial health of a company.