CHAPTER 11

INCOME TAXES

After completing this chapter, you will be able to do the following:

- Describe the differences between accounting profit and taxable income, and define key terms, including deferred tax assets, deferred tax liabilities, valuation allowance, taxes payable, and income tax expense.

- Explain how deferred tax liabilities and assets are created and the factors that determine how a company’s deferred tax liabilities and assets should be treated for the purposes of financial analysis.

- Determine the tax base of a company’s assets and liabilities.

- Calculate income tax expense, income taxes payable, deferred tax assets, and deferred tax liabilities, and calculate and interpret the adjustment to the financial statements related to a change in the income tax rate.

- Evaluate the impact of tax rate changes on a company’s financial statements and ratios.

- Distinguish between temporary and permanent differences in pretax accounting income and taxable income.

- Describe the valuation allowance for deferred tax assets—when it is required and what impact it has on financial statements.

- Compare a company’s deferred tax items.

- Analyze disclosures relating to deferred tax items and the effective tax rate reconciliation, and explain how information included in these disclosures affects a company’s financial statements and financial ratios.

- Identify the key provisions of and differences between income tax accounting under IFRS and U.S. GAAP.

For those companies reporting under International Financial Reporting Standards (IFRS), IAS 12 covers accounting for a company’s income taxes and the reporting of deferred taxes. For those companies reporting under United States generally accepted accounting principles (U.S. GAAP), SFAS No. 1091 is the primary source for information on accounting for income taxes. Although IFRS and U.S. GAAP follow similar conventions on many income tax issues, there are some key differences that will be discussed in the reading.

Differences between how and when transactions are recognized for financial reporting purposes relative to tax reporting can give rise to differences in tax expense and related tax assets and liabilities. To reconcile these differences, companies that report under either IFRS or U.S. GAAP create a provision on the balance sheet called deferred tax assets or deferred tax liabilities, depending on the nature of the situation.

Deferred tax assets or liabilities usually arise when accounting standards and tax authorities recognize the timing of revenues and expenses at different times. Because timing differences such as these will eventually reverse over time, they are called “temporary differences.” Deferred tax assets represent taxes that have been recognized for tax reporting purposes (or often the carrying forward of losses from previous periods) but have not yet been recognized on the income statement prepared for financial reporting purposes. Deferred tax liabilities represent tax expense that has appeared on the income statement for financial reporting purposes, but has not yet become payable under tax regulations.

This reading provides a primer on the basics of income tax accounting and reporting. The reading is organized as follows. Section 2 describes the differences between taxable income and accounting profit. Section 3 explains the determination of tax base, which relates to the valuation of assets and liabilities for tax purposes. Section 4 discusses several types of timing differences between the recognition of taxable and accounting profit. Section 5 examines unused tax losses and tax credits. Section 6 describes the recognition and measurement of current and deferred tax. Section 7 discusses the disclosure and presentation of income tax information on companies’ financial statements and illustrates its practical implications for financial analysis. Section 8 provides an overview of the similarities and differences for income-tax reporting between IFRS and U.S. GAAP. A summary of the key points and practice problems in the CFA Institute multiple-choice format conclude the reading.

2. DIFFERENCES BETWEEN ACCOUNTING PROFIT AND TAXABLE INCOME

A company’s accounting profit is reported on its income statement in accordance with prevailing accounting standards. Accounting profit (also referred to as income before taxes or pretax income) does not include a provision for income tax expense.2 A company’s taxable income is the portion of its income that is subject to income taxes under the tax laws of its jurisdiction. Because of different guidelines for how income is reported on a company’s financial statements and how it is measured for income tax purposes, accounting profit and taxable income may differ.

A company’s taxable income is the basis for its income tax payable (a liability) or recoverable (an asset), which is calculated on the basis of the company’s tax rate and appears on its balance sheet. A company’s tax expense, or tax benefit in the case of a recovery, appears on its income statement and is an aggregate of its income tax payable (or recoverable in the case of a tax benefit) and any changes in deferred tax assets and liabilities.

When a company’s taxable income is greater than its accounting profit, then its income taxes payable will be higher than what would have otherwise been the case had the income taxes been determined based on accounting profit. Deferred tax assets, which appear on the balance sheet, arise when an excess amount is paid for income taxes (taxable income higher than accounting profit) and the company expects to recover the difference during the course of future operations. Actual income taxes payable will thus exceed the financial accounting income tax expense (which is reported on the income statement and is determined based on accounting profit). Related to deferred tax assets is a valuation allowance, which is a reserve created against deferred tax assets. The valuation allowance is based on the likelihood of realizing the deferred tax assets in future accounting periods. Deferred tax liabilities, which also appear on the balance sheet, arise when a deficit amount is paid for income taxes and the company expects to eliminate the deficit over the course of future operations. In this case, financial accounting income tax expense exceeds income taxes payable.

Income tax paid in a period is the actual amount paid for income taxes (not a provision, but the actual cash outflow). The income tax paid may be less than the income tax expense because of payments in prior periods or refunds received in the current period. Income tax paid reduces the income tax payable, which is carried on the balance sheet as a liability.

The tax base of an asset or liability is the amount at which the asset or liability is valued for tax purposes, whereas the carrying amount is the amount at which the asset or liability is valued according to accounting principles.3 Differences between the tax base and the carrying amount also result in differences between accounting profit and taxable income. These differences can carry through to future periods. For example, a tax loss carry forward occurs when a company experiences a loss in the current period that may be used to reduce future taxable income. The company’s tax expense on its income statement must not only reflect the taxes payable based on taxable income, but also the effect of these differences.

2.1. Current Tax Assets and Liabilities

A company’s current tax liability is the amount payable in taxes and is based on current taxable income. If the company expects to receive a refund for some portion previously paid in taxes, the amount recoverable is referred to as a current tax asset. The current tax liability or asset may, however, differ from what the liability would have been if it were based on accounting profit rather than taxable income for the period. Differences in accounting profit and taxable income are the result of the application of different rules. Such differences between accounting profit and taxable income can occur in several ways, including:

- Revenues and expenses may be recognized in one period for accounting purposes and a different period for tax purposes.

- Specific revenues and expenses may be either recognized for accounting purposes and not for tax purposes; or not recognized for accounting purposes but recognized for tax purposes.

- The carrying amount and tax base of assets and/or liabilities may differ.

- The deductibility of gains and losses of assets and liabilities may vary for accounting and income tax purposes.

- Subject to tax rules, tax losses of prior years might be used to reduce taxable income in later years, resulting in differences in accounting and taxable income (tax loss carry-forward).

- Adjustments of reported financial data from prior years might not be recognized equally for accounting and tax purposes or might be recognized in different periods.

2.2. Deferred Tax Assets and Liabilities

Deferred tax assets represent taxes that have been paid (or often the carrying forward of losses from previous periods) but have not yet been recognized on the income statement. Deferred tax liabilities occur when financial accounting income tax expense is greater than regulatory income tax expense. Deferred tax assets and liabilities usually arise when accounting standards and tax authorities recognize the timing of taxes due at different times; for example, when a company uses accelerated depreciation when reporting to the tax authority (to increase expense and lower tax payments in the early years) but uses the straight-line method on the financial statements. Although not similar in treatment on a year-to-year basis (e.g., depreciation of 5 percent on a straight-line basis may be permitted for accounting purposes whereas 10 percent is allowed for tax purposes) over the life of the asset, both approaches allow for the total cost of the asset to be depreciated (or amortized). Because these timing differences will eventually reverse or self-correct over the course of the asset’s depreciable life, they are called “temporary differences.”

Under IFRS, deferred tax assets and liabilities are always classified as noncurrent. Under U.S. GAAP, however, deferred tax assets and liabilities are classified on the balance sheet as current and noncurrent based on the classification of the underlying asset or liability.

Any deferred tax asset or liability is based on temporary differences that result in an excess or a deficit amount paid for taxes, which the company expects to recover from future operations. Because taxes will be recoverable or payable at a future date, it is only a temporary difference and a deferred tax asset or liability is created. Changes in the deferred tax asset or liability on the balance sheet reflect the difference between the amounts recognized in the previous period and the current period. The changes in deferred tax assets and liabilities are added to income tax payable to determine the company’s income tax expense (or credit) as it is reported on the income statement.

At the end of each fiscal year, deferred tax assets and liabilities are recalculated by comparing the tax bases and carrying amounts of the balance sheet items. Identified temporary differences should be assessed on whether the difference will result in future economic benefits. For example, Pinto Construction (a hypothetical company) depreciates equipment on a straight-line basis of 10 percent per year. The tax authorities allow depreciation of 15 percent per year. At the end of the fiscal year, the carrying amount of the equipment for accounting purposes would be greater than the tax base of the equipment thus resulting in a temporary difference. A deferred tax item may only be created if it is not doubtful that the company will realize economic benefits in the future. In our example, the equipment is used in the core business of Pinto Construction. If the company is a going concern and stable, there should be no doubt that future economic benefits will result from the equipment and it would be appropriate to create the deferred tax item.

Should it be doubtful that future economic benefits will be realized from a temporary difference (such as Pinto Construction being under liquidation), the temporary difference will not lead to the creation of a deferred tax asset or liability. If a deferred tax asset or liability resulted in the past, but the criteria of economic benefits is not met on the current balance sheet date, then, under IFRS, an existing deferred tax asset or liability related to the item will be reversed. Under U.S. GAAP, a valuation allowance is established. In assessing future economic benefits, much is left to the discretion of the auditor in assessing the temporary differences and the issue of future economic benefits.

EXAMPLE 11-1

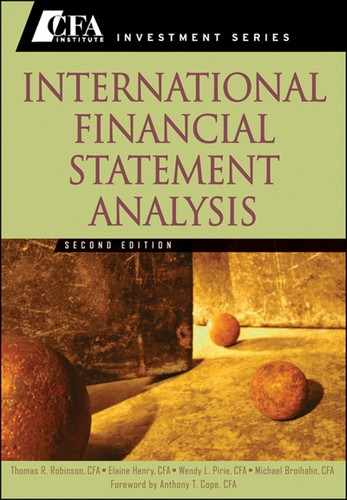

The following information pertains to a fictitious company, Reston Partners:

The financial performance and accounting profit of Reston Partners on this income statement is based on accounting principles appropriate for the jurisdiction in which Reston Partners operates. The principles used to calculate accounting profit (profit before tax in the previous example) may differ from the principles applied for tax purposes (the calculation of taxable income). For illustrative purposes, however, assume that all income and expenses on the income statement are treated identically for tax and accounting purposes except depreciation.

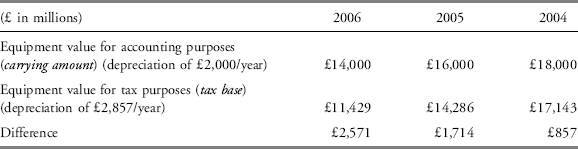

The depreciation is related to equipment owned by Reston Partners. For simplicity, assume that the equipment was purchased at the beginning of the 2004 fiscal year. Depreciation should thus be calculated and expensed for the full year. Assume that accounting standards permit equipment to be depreciated on a straight-line basis over a 10-year period, whereas the tax standards in the jurisdiction specify that equipment should be depreciated on a straight-line basis over a 7-year period. For simplicity, assume a salvage value of £0 at the end of the equipment’s useful life. Both methods will result in the full depreciation of the asset over the respective tax or accounting life.

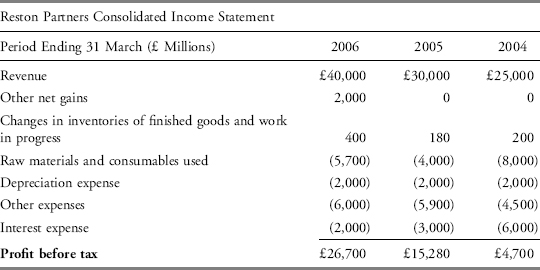

The equipment was originally purchased for £20,000. In accordance with accounting standards, over the next 10 years the company will recognize annual depreciation of £2,000 (£20,000 ÷ 10) as an expense on its income statement and for the determination of accounting profit. For tax purposes, however, the company will recognize £2,857 (£20,000 ÷ 7) in depreciation each year. Each fiscal year the depreciation expense related to the use of the equipment will, therefore, differ for tax and accounting purposes (tax base vs. carrying amount), resulting in a difference between accounting profit and taxable income.

The previous income statement reflects accounting profit (depreciation at £2,000 per year). The following table shows the taxable income for each fiscal year.

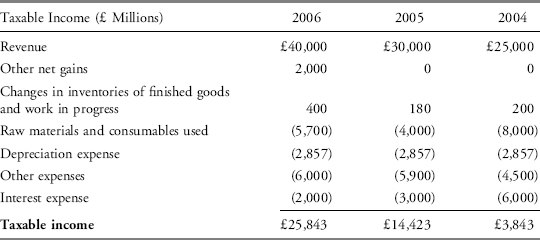

The carrying amount and tax base for the equipment is as follows:

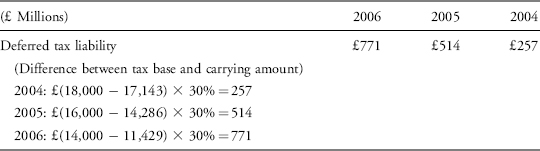

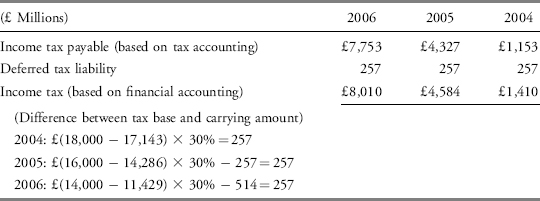

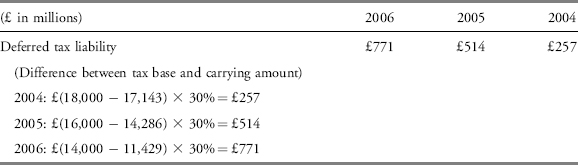

At each balance sheet date, the tax base and carrying amount of all assets and liabilities must be determined. The income tax payable by Reston Partners will be based on the taxable income of each fiscal year. If a tax rate of 30 percent is assumed, then the income taxes payable for 2004, 2005, and 2006 are £1,153 (30% × 3,843), £4,327 (30% × 14,423), and £7,753 (30% × 25,843).

Remember, though, that if the tax obligation is calculated based on accounting profits, it will differ because of the differences between the tax base and the carrying amount of equipment. The difference in each fiscal year is reflected in the earlier table. In each fiscal year the carrying amount of the equipment exceeds its tax base. For tax purposes, therefore, the asset tax base is less than its carrying value under financial accounting principles. The difference results in a deferred tax liability.

The comparison of the tax base and carrying amount of equipment shows what the deferred tax liability should be on a particular balance sheet date. In each fiscal year, only the change in the deferred tax liability should be included in the calculation of the income tax expense reported on the income statement prepared for accounting purposes.

On the income statement, the company’s income tax expense will be the sum of the deferred tax liability and income tax payable.

Note that because the different treatment of depreciation is a temporary difference, the income tax on the income statement is 30 percent of the accounting profit, although only a part is income tax payable and the rest is a deferred tax liability.

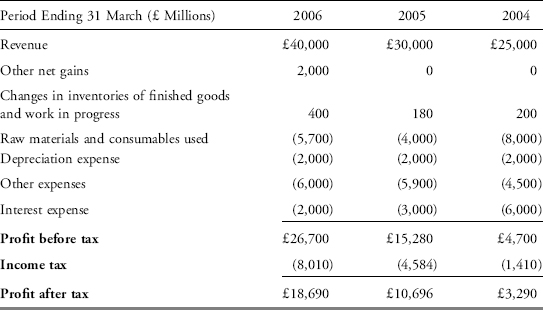

The consolidated income statement of Reston Partners including income tax is presented as follows:

Any amount paid to the tax authorities will reduce the liability for income tax payable and be reflected on the statement of cash flows of the company.

3. DETERMINING THE TAX BASE OF ASSETS AND LIABILITIES

As mentioned in Section 2, temporary differences arise from a difference in the tax base and carrying amount of assets and liabilities. The tax base of an asset or liability is the amount attributed to the asset or liability for tax purposes, whereas the carrying amount is based on accounting principles. Such a difference is considered temporary if it is expected that the taxes will be recovered or payable at a future date.

3.1. Determining the Tax Base of an Asset

The tax base of an asset is the amount that will be deductible for tax purposes in future periods as the economic benefits become realized and the company recovers the carrying amount of the asset.

For example, our previously mentioned Reston Partners (from Example 11-1) depreciates equipment on a straight-line basis at a rate of 10 percent per year. The tax authorities allow depreciation of approximately 15 percent per year. At the end of the fiscal year, the carrying amount of equipment for accounting purposes is greater than the asset tax base thus resulting in a temporary difference.

EXAMPLE 11-2 Determining the Tax Base of an Asset

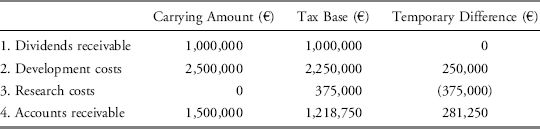

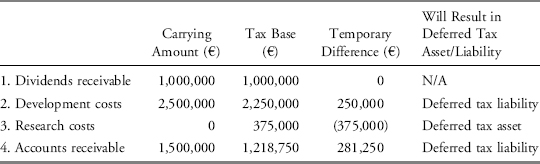

The following information pertains to Entiguan Sports, a hypothetical developer of products used to treat sports-related injuries. (The treatment of items for accounting and tax purposes is based on fictitious accounting and tax standards and is not specific to a particular jurisdiction.) Calculate the tax base and carrying amount for each item.

1. Dividends receivable: On its balance sheet, Entiguan Sports reports dividends of €1 million receivable from a subsidiary. Assume that dividends are not taxable.

2. Development costs: Entiguan Sports capitalized development costs of €3 million during the year. Entiguan amortized €500,000 of this amount during the year. For tax purposes amortization of 25 percent per year is allowed.

3. Research costs: Entiguan incurred €500,000 in research costs, which were all expensed in the current fiscal year for financial reporting purposes. Assume that applicable tax legislation requires research costs to be expensed over a four-year period rather than all in one year.

4. Accounts receivable: Included on the income statement of Entiguan Sports is a provision for doubtful debt of €125,000. The accounts receivable amount reflected on the balance sheet, after taking the provision into account, amounts to €1,500,000. The tax authorities allow a deduction of 25 percent of the gross amount for doubtful debt.

Solutions:

Comments:

1. Dividends receivable: Although the dividends received are economic benefits from the subsidiary, we are assuming that dividends are not taxable. Therefore, the carrying amount equals the tax base for dividends receivable.

2. Development costs: First, we assume that development costs will generate economic benefits for Entiguan Sports. Therefore, it may be included as an asset on the balance sheet for the purposes of this example. Second, the amortization allowed by the tax authorities exceeds the amortization accounted for based on accounting rules. Therefore, the carrying amount of the asset exceeds its tax base. The carrying amount is (€3,000,000 − €500,000) = €2,500,000 whereas the tax base is [€3,000,000 − (25% × €3,000,000)] = €2,250,000.

3. Research costs: We assume that research costs will result in future economic benefits for the company. If this were not the case, creation of a deferred tax asset or liability would not be allowed. The tax base of research costs exceeds their carrying amount. The carrying amount is €0 because the full amount has been expensed for financial reporting purposes in the year in which it was incurred. Therefore, there would not have been a balance sheet item “Research costs” for tax purposes, and only a proportion may be deducted in the current fiscal year. The tax base of the asset is (€500,000 − €500,000/4) = €375,000.

4. Accounts receivable: The economic benefits that should have been received from accounts receivable have already been included in revenues included in the calculation of the taxable income when the sales occurred. Because the receipt of a portion of the accounts receivable is doubtful, the provision is allowed. The provision, based on tax legislation, results in a greater amount allowed in the current fiscal year than would be the case under accounting principles. This results in the tax base of accounts receivable being lower than its carrying amount. Note that the example specifically states that the balance sheet amount for accounts receivable after the provision for accounting purposes amounts to €1,500,000. Therefore, accounts receivable before any provision was €1,500,000+€125,000 = €1,625,000. The tax base is calculated as (€1,500,000+€125,000) − [25% × (€1,500,000+€125,000)] = €1,218,750.

3.2. Determining the Tax Base of a Liability

The tax base of a liability is the carrying amount of the liability less any amounts that will be deductible for tax purposes in the future. With respect to payments from customers received in advance of providing the goods and services, the tax base of such a liability is the carrying amount less any amount of the revenue that will not be taxable in future. Keep in mind the following fundamental principle: In general, a company will recognize a deferred tax asset or liability when recovery/settlement of the carrying amount will affect future tax payments by either increasing or reducing the taxable profit. Remember, an analyst is not only evaluating the difference between the carrying amount and the tax base, but the relevance of that difference on future profits and losses and thus by implication future taxes.

IFRS offers specific guidelines with regard to revenue received in advance: IAS 12 states that the tax base is the carrying amount less any amount of the revenue that will not be taxed at a future date. Under U.S. GAAP, an analysis of the tax base would result in a similar outcome. The tax legislation within the jurisdiction will determine the amount recognized on the income statement and whether the liability (revenue received in advance) will have a tax base greater than zero. This will depend on how tax legislation recognizes revenue received in advance.

EXAMPLE 11-3 Determining the Tax Base of a Liability

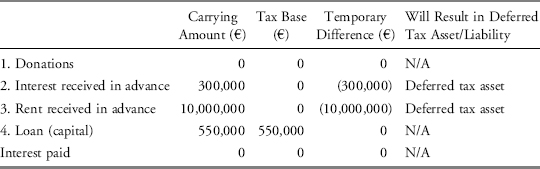

The following information pertains to Entiguan Sports for the 2006 year-end. The treatment of items for accounting and tax purposes is based on fictitious accounting and tax standards and is not specific to a particular jurisdiction. Calculate the tax base and carrying amount for each item.

1. Donations: Entiguan Sports made donations of €100,000 in the current fiscal year. The donations were expensed for financial reporting purposes, but are not tax deductible based on applicable tax legislation.

2. Interest received in advance: Entiguan Sports received in advance interest of €300,000. The interest is taxed because tax authorities recognize the interest to accrue to the company (part of taxable income) on the date of receipt.

3. Rent received in advance: Entiguan recognized €10 million for rent received in advance from a lessee for an unused warehouse building. Rent received in advance is deferred for accounting purposes but taxed on a cash basis.

4. Loan: Entiguan Sports secured a long-term loan for €550,000 in the current fiscal year. Interest is charged at 13.5 percent per annum and is payable at the end of each fiscal year.

Solutions:

Comments:

1. Donations: The amount of €100,000 was immediately expensed on Entiguan’s income statement; therefore, the carrying amount is €0. Tax legislation does not allow donations to be deducted for tax purposes, so the tax base of the donations equals the carrying amount. Note that while the carrying amount and tax base are the same, the difference in the treatment of donations for accounting and tax purposes (expensed for accounting purposes, but not deductible for tax purposes) represents a permanent difference (a difference that will not be reversed in future). Permanent and temporary differences are elaborated on in Section 4 and it will refer to this particular case with an expanded explanation.

2. Interest received in advance: Based on the information provided, for tax purposes, interest is deemed to accrue to the company on the date of receipt. For tax purposes, it is thus irrelevant whether it is for the current or a future accounting period; it must be included in taxable income in the financial year received. Interest received in advance is, for accounting purposes though, included in the financial period in which it is deemed to have been earned. For this reason, the interest income received in advance is a balance sheet liability. It was not included on the income statement because the income relates to a future financial year. Because the full €300,000 is included in taxable income in the current fiscal year, the tax base is €300,000 − 300,000 = €0. Note that although interest received in advance and rent received in advance are both taxed, the timing depends on how the particular item is treated in tax legislation.

3. Rent received in advance: The result is similar to interest received in advance. The carrying amount of rent received in advance would be €10,000,000 while the tax base is €0.

4. Loan: Repayment of the loan has no tax implications. The repayment of the capital amount does not constitute an income or expense. The interest paid is included as an expense in the calculation of taxable income as well as accounting income. Therefore, the tax base and carrying amount is €0. For clarity, the interest paid that would be included on the income statement for the year amounts to 13.5% × €550,000 = €74,250 if the loan was acquired at the beginning of the current fiscal year.

3.3. Changes in Income Tax Rates

The measurement of deferred tax assets and liabilities is based on current tax law. But if there are subsequent changes in tax laws or new income tax rates, existing deferred tax assets and liabilities must be adjusted for the effects of these changes. The resulting effects of the changes are also included in determining accounting profit in the period of change.

When income tax rates change, the deferred tax assets and liabilities are adjusted to the new tax rate. If income tax rates increase, deferred taxes (that is, the deferred tax assets and liabilities) will also increase. Likewise, if income tax rates decrease, deferred taxes will decrease. A decrease in tax rates decreases deferred tax liabilities, which reduces future tax payments to the taxing authorities. A decrease in tax rates will also decrease deferred tax assets, which reduces their value toward the offset of future tax payments to the taxing authorities.

To illustrate the effect of a change in tax rate, consider Example 11-1 again. In that illustration, the timing difference that led to the recognition of a deferred tax liability for Reston Partners was attributable to differences in the method of depreciation and the related effects on the accounting carrying value and the asset tax base. The relevant information is restated here.

The carrying amount and tax base for the equipment is:

At a 30 percent income tax rate, the deferred tax liability was then determined as follows:

For this illustration, assume that the taxing authority has changed the income tax rate to 25 percent for 2006. Although the difference between the carrying amount and the tax base of the depreciable asset are the same, the deferred tax liability for 2006 will be £643 (instead of £771 or a reduction of £128 in the liability). 2006: £(14,000 − 11,429) × 25% = £643.

Reston Partners’ provision for income tax expense is also affected by the change in tax rates. Taxable income for 2006 will now be taxed at a rate of 25 percent. The benefit of the 2006 accelerated depreciation tax shield is now only £214 (£857 × 25%) instead of the previous £257 (a reduction of £43). In addition, the reduction in the beginning carrying value of the deferred tax liability for 2006 (the year of change) further reduces the income tax expense for 2006. The reduction in income tax expense attributable to the change in tax rate is £85. 2006: (30% − 25%) × £1,714 = £85. Note that these two components together account for the reduction in the deferred tax liability (£43+£85 = £128).

As may be seen from this discussion, changes in the income tax rate have an effect on a company’s deferred tax asset and liability carrying values as well as an effect on the measurement of income tax expense in the year of change. The analyst must thus note that proposed changes in tax law can have a quantifiable effect on these accounts (and any related financial ratios that are derived from them) if the proposed changes are subsequently enacted into law.

4. TEMPORARY AND PERMANENT DIFFERENCES BETWEEN TAXABLE AND ACCOUNTING PROFIT

Temporary differences arise from a difference between the tax base and the carrying amount of assets and liabilities. The creation of a deferred tax asset or liability from a temporary difference is only possible if the difference reverses itself at some future date and to such an extent that the balance sheet item is expected to create future economic benefits for the company. IFRS and U.S. GAAP both prescribe the balance sheet liability method for recognition of deferred tax. This balance sheet method focuses on the recognition of a deferred tax asset or liability should there be a temporary difference between the carrying amount and tax base of balance sheet items.4

Permanent differences are differences between tax and financial reporting of revenue (expenses) that will not be reversed at some future date. Because they will not be reversed at a future date, these differences do not give rise to deferred tax. These items typically include

- Income or expense items not allowed by tax legislation.

- Tax credits for some expenditures that directly reduce taxes.

Because no deferred tax item is created for permanent differences, all permanent differences result in a difference between the company’s effective tax rate and statutory tax rate. The effective tax rate is also influenced by different statutory taxes should an entity conduct business in more than one tax jurisdiction. The formula for the reported effective tax rate is thus equal to:

![]()

The net change in deferred tax during a reporting period is the difference between the balance of the deferred tax asset or liability for the current period and the balance of the previous period.

4.1. Taxable Temporary Differences

Temporary differences are further divided into two categories, namely taxable temporary differences and deductible temporary differences. Taxable temporary differences are temporary differences that result in a taxable amount in a future period when determining the taxable profit as the balance sheet item is recovered or settled. Taxable temporary differences result in a deferred tax liability when the carrying amount of an asset exceeds its tax base and, in the case of a liability, when the tax base of the liability exceeds its carrying amount.

Under U.S. GAAP, a deferred tax asset or liability is not recognized for unamortizable goodwill. Under IFRS, a deferred tax account is not recognized for goodwill arising in a business combination. Since goodwill is a residual, the recognition of a deferred tax liability would increase the carrying amount of goodwill. Discounting deferred tax assets or liabilities is generally not allowed for temporary differences related to business combinations as it is for other temporary differences.

IFRS provides an exemption (that is, deferred tax is not provided on the temporary difference) for the initial recognition of an asset or liability in a transaction that: (a) is not a business combination (e.g., joint ventures, branches, and unconsolidated investments); and (b) affects neither accounting profit nor taxable profit at the time of the transaction. U.S. GAAP does not provide an exemption for these circumstances.

As a simple example of a temporary difference with no recognition of deferred tax liability, assume that a fictitious company, Corporate International, a holding company of various leisure related businesses and holiday resorts, buys an interest in a hotel in the current financial year. The goodwill related to the transaction will be recognized on the financial statements, but the related tax liability will not, as it relates to the initial recognition of goodwill.

4.2. Deductible Temporary Differences

Deductible temporary differences are temporary differences that result in a reduction or deduction of taxable income in a future period when the balance sheet item is recovered or settled. Deductible temporary differences result in a deferred tax asset when the tax base of an asset exceeds its carrying amount and, in the case of a liability, when the carrying amount of the liability exceeds its tax base. The recognition of a deferred tax asset is only allowed to the extent there is a reasonable expectation of future profits against which the asset or liability (that gave rise to the deferred tax asset) can be recovered or settled.

To determine the probability of sufficient future profits for utilization, one must consider the following: (1) Sufficient taxable temporary differences must exist that are related to the same tax authority and the same taxable entity; and (2) The taxable temporary differences that are expected to reverse in the same periods as expected for the reversal of the deductible temporary differences.

As with deferred tax liabilities, IFRS states that deferred tax assets should not be recognized in cases that would arise from the initial recognition of an asset or liability in transactions that are not a business combination and when, at the time of the transaction, there is no impact on either accounting or taxable profit. Subsequent to initial recognition under IFRS and U.S. GAAP, any deferred tax assets that arise from investments in subsidiaries, branches, associates, and interests in joint ventures are recognized as a deferred tax asset.

IFRS and U.S. GAAP allow the creation of a deferred tax asset in the case of tax losses and tax credits. These two unique situations will be further elaborated on in Section 6. IAS 12 does not allow the creation of a deferred tax asset arising from negative goodwill. Negative goodwill arises when the amount that an entity pays for an interest in a business is less than the net fair market value of the portion of assets and liabilities of the acquired company, based on the interest of the entity.

4.3. Examples of Taxable and Deductible Temporary Differences

Exhibit 11-1 summarizes how differences between the tax bases and carrying amounts of assets and liabilities give rise to deferred tax assets or deferred tax liabilities.

EXHIBIT 11-1 Treatment of Temporary Differences

| Balance Sheet Item | Carrying Amount vs. Tax Base | Results in Deferred Tax Asset/Liability |

| Asset | Carrying amount > tax base | Deferred tax liability |

| Asset | Carrying amount<tax base | Deferred tax asset |

| Liability | Carrying amount > tax base | Deferred tax asset |

| Liability | Carrying amount<tax base | Deferred tax liability |

EXAMPLE 11-4 Taxable and Deductible Temporary Differences

Examples 11-2 and 11-3 illustrated how to calculate the tax base of assets and liabilities, respectively. Based on the information provided in Examples 11-2 and 11-3, indicate whether the difference in the tax base and carrying amount of the assets and liabilities are temporary or permanent differences and whether a deferred tax asset or liability will be recognized based on the difference identified.

Solution to Example 11-2:

Example 11-2 included comments on the calculation of the carrying amount and tax base of the assets.

1. Dividends receivable: As a result of nontaxability, the carrying amount equals the tax base of dividends receivable. This constitutes a permanent difference and will not result in the recognition of any deferred tax asset or liability. A temporary difference constitutes a difference that will, at some future date, be reversed. Although the timing of recognition is different for tax and accounting purposes, in the end the full carrying amount will be expensed/recognized as income. A permanent difference will never be reversed. Based on tax legislation, dividends from a subsidiary are not recognized as income. Therefore, no amount will be reflected as dividend income when calculating the taxable income, and the tax base of dividends receivable must be the total amount received, namely €1,000,000. The taxable income and accounting profit will permanently differ with the amount of dividends receivable, even on future financial statements as an effect on the retained earnings reflected on the balance sheet.

2. Development costs: The difference between the carrying amount and tax base is a temporary difference that, in the future, will reverse. In this fiscal year, it will result in a deferred tax liability.

3. Research costs: The difference between the carrying amount and tax base is a temporary difference that results in a deferred tax asset. Remember the explanation in Section 2 for deferred tax assets—a deferred tax asset arises because of an excess amount paid for taxes (when taxable income is greater than accounting profit), which is expected to be recovered from future operations. Based on accounting principles, the full amount was deducted resulting in a lower accounting profit, while the taxable income by implication, should be greater because of the lower amount expensed.

4. Accounts receivable: The difference between the carrying amount and tax base of the asset is a temporary difference that will result in a deferred tax liability.

Solution to Example 11-3:

Example 11-3 included extensive comments on the calculation of the carrying amount and tax base of the liabilities.

1. Donations: It was assumed that tax legislation does not allow donations to be deducted for tax purposes. No temporary difference results from donations, and thus a deferred tax asset or liability will not be recognized. This constitutes a permanent difference.

2. Interest received in advance: Interest received in advance results in a temporary difference that gives rise to a deferred tax asset. A deferred tax asset arises because of an excess amount paid for taxes (when taxable income is greater than accounting profit), which is expected to be recovered from future operations.

3. Rent received in advance: The difference between the carrying amount and tax base is a temporary difference that leads to the recognition of a deferred tax asset.

4. Loan: There are no temporary differences as a result of the loan or interest paid, and thus no deferred tax item is recognized.

4.4. Temporary Differences at Initial Recognition of Assets and Liabilities

In some situations the carrying amount and tax base of a balance sheet item may vary at initial recognition. For example, a company may deduct a government grant from the initial carrying amount of an asset or liability that appears on the balance sheet. For tax purposes, such grants may not be deducted when determining the tax base of the balance sheet item. In such circumstances, the carrying amount of the asset or liability will be lower than its tax base. Differences in the tax base of an asset or liability as a result of the circumstances described earliermay not be recognized as deferred tax assets or liabilities.

For example, a government may offer grants to small, medium, and micro enterprises (SMME) in an attempt to assist these entrepreneurs in their endeavors that contribute to the country’s GDP and job creation. Assume that a particular grant is offered for infrastructure needs (office furniture, property, plant, and equipment, etc.). In these circumstances, although the carrying amount will be lower than the tax base of the asset, the related deferred tax may not be recognized. As mentioned earlier, deferred tax assets and liabilities should not be recognized in cases that would arise from the initial recognition of an asset or liability in transactions that are not a business combination and when, at the time of the transaction, there is no impact on either accounting or taxable profit.

A deferred tax liability will also not be recognized at the initial recognition of goodwill. Although goodwill may be treated differently across tax jurisdictions, which may lead to differences in the carrying amount and tax base of goodwill, IAS 12 does not allow the recognition of such a deferred tax liability. Any impairment that an entity should, for accounting purposes, impose on goodwill will again result in a temporary difference between its carrying amount and tax base. Any impairment that an entity should, for accounting purposes, impose on goodwill and if part of the goodwill is related to the initial recognition, that part of the difference in tax base and carrying amount should not result in any deferred taxation because the initial deferred tax liability was not recognized. Any future differences between the carrying amount and tax base as a result of amortization and the deductibility of a portion of goodwill constitute a temporary difference for which provision should be made.

4.5. Business Combinations and Deferred Taxes

The fair value of assets and liabilities acquired in a business combination is determined on the acquisition date and may differ from the previous carrying amount. It is highly probable that the values of acquired intangible assets, including goodwill, would differ from their carrying amounts. This temporary difference will affect deferred taxes as well as the amount of goodwill recognized as a result of the acquisition.

4.6. Investments in Subsidiaries, Branches, Associates, and Interests in Joint Ventures

Investments in subsidiaries, branches, associates, and interests in joint ventures may lead to temporary differences on the consolidated versus the parent’s financial statements. The related deferred tax liabilities as a result of temporary differences will be recognized unless both of the following criteria are satisfied:

- The parent is in a position to control the timing of the future reversal of the temporary difference.

- It is probable that the temporary difference will not reverse in the future.

With respect to deferred tax assets related to subsidiaries, branches, and associates and interests, deferred tax assets will only be recognized if the following criteria are satisfied:

- The temporary difference will reverse in the future.

- Sufficient taxable profits exist against which the temporary difference can be used.

5. UNUSED TAX LOSSES AND TAX CREDITS

IAS 12 allows the recognition of unused tax losses and tax credits only to the extent that it is probable that in the future there will be taxable income against which the unused tax losses and credits can be applied. Under U.S. GAAP, a deferred tax asset is recognized in full but is then reduced by a valuation allowance if it is more likely than not that some or all of the deferred tax asset will not be realized. The same requirements for creation of a deferred tax asset as a result of deductible temporary differences also apply to unused tax losses and tax credits. The existence of tax losses may indicate that the entity cannot reasonably be expected to generate sufficient future taxable income. All other things held constant, the greater the history of tax losses, the greater the concern regarding the company’s ability to generate future taxable profits.

Should there be concerns about the company’s future profitability, then the deferred tax asset may not be recognized until it is realized. When assessing the probability that sufficient taxable profit will be generated in the future, the following criteria can serve as a guide:

- If there is uncertainty as to the probability of future taxable profits, a deferred tax asset as a result of unused tax losses or tax credits is only recognized to the extent of the available taxable temporary differences.

- Assess the probability that the entity will in fact generate future taxable profits before the unused tax losses and/or credits expire pursuant to tax rules regarding the carry forward of the unused tax losses.

- Verify that the above is with the same tax authority and based on the same taxable entity.

- Determine whether the past tax losses were a result of specific circumstances that are unlikely to be repeated.

- Discover if tax planning opportunities are available to the entity that will result in future profits. These may include changes in tax legislation that is phased in over more than one financial period to the benefit of the entity.

It is imperative that the timing of taxable and deductible temporary differences also be considered before creating a deferred tax asset based on unused tax credits.

6. RECOGNITION AND MEASUREMENT OF CURRENT AND DEFERRED TAX

Current taxes payable or recoverable from tax authorities are based on the applicable tax rates at the balance sheet date. Deferred taxes should be measured at the tax rate that is expected to apply when the asset is realized or the liability settled. With respect to the income tax for a current or prior period not yet paid, it is recognized as a tax liability until paid. Any amount paid in excess of any tax obligation is recognized as an asset. The income tax paid in excess or owed to tax authorities is separate from deferred taxes on the company’s balance sheet.

When measuring deferred taxes in a jurisdiction, there are different forms of taxation such as income tax, capital gains tax (any capital gains made), or secondary tax on companies (tax payable on the dividends that a company declares) and possibly different tax bases for a balance sheet item (as in the case of government grants influencing the tax base of an asset such as property). In assessing which tax laws should apply, it is dependent on how the related asset or liability will be settled. It would be prudent to use the tax rate and tax base that is consistent with how it is expected the tax base will be recovered or settled.

Although deferred tax assets and liabilities are related to temporary differences expected to be recovered or settled at some future date, neither are discounted to present value in determining the amounts to be booked. Both must be adjusted for changes in tax rates.

Deferred taxes as well as income taxes should always be recognized on the income statement of an entity unless it pertains to:

- Taxes or deferred taxes charged directly to equity.

- A possible provision for deferred taxes relates to a business combination.

The carrying amount of the deferred tax assets and liabilities should also be assessed. The carrying amounts may change even though there may have been no change in temporary differences during the period evaluated. This can result from:

- Changes in tax rates.

- Reassessments of the recoverability of deferred tax assets.

- Changes in the expectations for how an asset will be recovered and what influences the deferred tax asset or liability.

All unrecognized deferred tax assets and liabilities must be reassessed at the balance sheet date and measured against the criteria of probable future economic benefits. If such a deferred asset is likely to be recovered, it may be appropriate to recognize the related deferred tax asset.

Different jurisdictions have different requirements for determining tax obligations that can range from different forms of taxation to different tax rates based on taxable income. When comparing financial statements of entities that conduct business in different jurisdictions subject to different tax legislation, the analyst should be cautious in reaching conclusions because of the potentially complex tax rules that may apply.

6.1. Recognition of a Valuation Allowance

Deferred tax assets must be assessed at each balance sheet date. If there is any doubt whether the deferral will be recovered, then the carrying amount should be reduced to the expected recoverable amount. Should circumstances subsequently change and suggest the future will lead to recovery of the deferral, the reduction may be reversed.

Under U.S. GAAP, deferred tax assets are reduced by creating a valuation allowance. Establishing a valuation allowance reduces the deferred tax asset and income in the period in which the allowance is established. Should circumstances change to such an extent that a deferred tax asset valuation allowance may be reduced, the reversal will increase the deferred tax asset and operating income. Because of the subjective judgment involved, an analyst should carefully scrutinize any such changes.

6.2. Recognition of Current and Deferred Tax Charged Directly to Equity

In general, IFRS and U.S. GAAP require that the recognition of deferred tax liabilities and current income tax should be treated similarly to the asset or liability that gave rise to the deferred tax liability or income tax based on accounting treatment. Should an item that gives rise to a deferred tax liability be taken directly to equity, the same should hold true for the resulting deferred tax.

The following are examples of such items:

- Revaluation of property, plant, and equipment (revaluations are not permissible under U.S. GAAP).

- Long-term investments at fair value.

- Changes in accounting policies.

- Errors corrected against the opening balance of retained earnings.

- Initial recognition of an equity component related to complex financial instruments.

- Exchange rate differences arising from the currency translation procedures for foreign operations.

Whenever it is determined that a deferred tax liability will not be reversed, an adjustment should be made to the liability. The deferred tax liability will be reduced and the amount by which it is reduced should be taken directly to equity. Any deferred taxes related to a business combination must also be recognized in equity.

Depending on the items that gave rise to the deferred tax liabilities, an analyst should exercise judgment regarding whether the taxes should be included with deferred tax liabilities or whether it should be taken directly to equity. It may be more appropriate simply to ignore deferred taxes.

EXAMPLE 11-5 Taxes Charged Directly to Equity

The following information pertains to Anderson Company (a hypothetical company). A building owned by Anderson Company was originally purchased for €1,000,000 on 1 January 2004. For accounting purposes, buildings are depreciated at 5 percent a year on a straight-line basis, and depreciation for tax purposes is 10 percent a year on a straight-line basis. On the first day of the 2006, the building is revalued at €1,200,000. It is estimated that the remaining useful life of the building from the date of revaluation is 20 years. Important: For tax purposes the revaluation of the building is not recognized.

Based on the information provided, the following illustrates the difference in treatment of the building for accounting and tax purposes.

| Carrying Amount of Building | Tax Baseof Building | |

| Balance on 1 January 2004 | €1,000,000 | €1,000,000 |

| Depreciation 2004 | 50,000 | 100,000 |

| Balance on 31 December 2004 | €950,000 | €900,000 |

| Depreciation 2005 | 50,000 | 100,000 |

| Balance on 31 December 2005 | €900,000 | €800,000 |

| Revaluation on 1 January 2006 | 300,000 | N/A |

| Balance on 1 January 2006 | €1,200,000 | €800,000 |

| Depreciation 2006 | 60,000 | 100,000 |

| Balance on 31 December 2006 | €1,140,000 | €700,000 |

| Accumulated depreciation | ||

| Balance on 1 January 2004 | €0 | €0 |

| Depreciation 2004 | 50,000 | 100,000 |

| Balance on 31 December 2004 | €50,000 | €100,000 |

| Depreciation 2005 | 50,000 | 100,000 |

| Balance on 31 December 2005 | €100,000 | €200,000 |

| Revaluation at 1 January 2006 | (100,000) | N/A |

| Balance on 1 January 2006 | €0 | €200,000 |

| Depreciation 2006 | 60,000 | 100,000 |

| Balance on 30 November 2006 | €60,000 | €300,000 |

| Carrying Amount | Tax Base | |

| On 31 December 2004 | €950,000 | €900,000 |

| On 31 December 2005 | €900,000 | €800,000 |

| On 31 December 2006 | €1,140,000 | €700,000 |

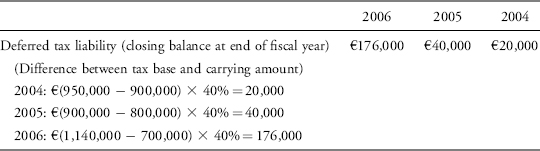

31 December 2004: On 31 December 2004, different treatments for depreciation expense result in a temporary difference that gives rise to a deferred tax liability. The difference in the tax base and carrying amount of the building was a result of different depreciation amounts for tax and accounting purposes. Depreciation appears on the income statement. For this reason the deferred tax liability will also be reflected on the income statement. If we assume that the applicable tax rate in 2004 was 40 percent, then the resulting deferred tax liability will be 40% × (€950,000 − €900,000) = €20,000.

31 December 2005: As of 31 December 2005, the carrying amount of the building remains greater than the tax base. The temporary difference again gives rise to a deferred tax liability. Again, assuming the applicable tax rate to be 40 percent, the deferred tax liability from the building is 40% × (€900,000 − €800,000) = €40,000.

31 December 2006: On 31 December 2006, the carrying amount of the building again exceeds the tax base. This is not the result of disposals or additions, but is a result of the revaluation at the beginning of the 2006 fiscal year and the different rates of depreciation. The deferred tax liability would seem to be 40% × (€1,140,000 − €700,000) = €176,000, but the treatment is different than it was for the 2004 and 2005. In 2006, revaluation of the building gave rise to a balance sheet equity account, namely “Revaluation Surplus” in the amount of €300,000, which is not recognized for tax purposes.

The deferred tax liability would usually have been calculated as follows:

The change in the deferred tax liability in 2004 is €20,000, in 2005: €20,000 (€40,000 − €20,000) and, it would seem, in 2006: €136,000 (€176,000 − €40,000). In 2006, although it would seem that the balance for deferred tax liability should be €176,000, the revaluation is not recognized for tax purposes. Only the portion of the difference between the tax base and carrying amount that is not a result of the revaluation is recognized as giving rise to a deferred tax liability.

The effect of the revaluation surplus and the associated tax effects are accounted for in a direct adjustment to equity. The revaluation surplus is reduced by the tax provision associated with the excess of the fair value over the carry value and it affects retained earnings (€300,000 × 40% = €120,000).

The deferred tax liability that should be reflected on the balance sheet is thus not €176,000 but only €56,000 (€176,000 − €120,000). Given the balance of deferred tax liability at the beginning of the 2006 fiscal year in the amount of €40,000, the change in the deferred tax liability is only €56,000 − €40,000 = €16,000.

In the future, at the end of each year, an amount equal to the depreciation as a result of the revaluation minus the deferred tax effect will be transferred from the revaluation reserve to retained earnings. In 2006 this will amount to a portion of depreciation resulting from the revaluation, €15,000 (€300,000 ÷ 20), minus the deferred tax effect of €6,000 (€15,000 × 40%), thus €9,000.

7. PRESENTATION AND DISCLOSURE

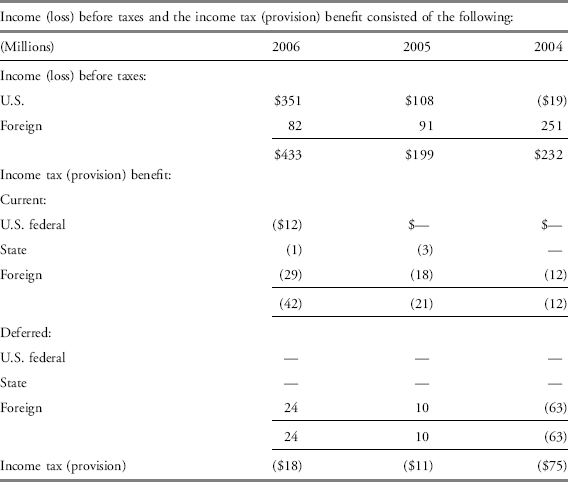

We will discuss the presentation and disclosure of income tax related information by way of example. The Consolidated Statements of Operations (Income Statements) and Consolidated Balance Sheets for Micron Technology (MU) are provided in Exhibits 11-2 and 11-3, respectively. Exhibit 11-4 provides the income tax note disclosures for MU for the 2004, 2005, and 2006 fiscal years.

EXHIBIT 11-2 Micron Technology, Inc. Consolidated Statements of Operations (Amounts in Millions except Per Share)

EXHIBIT 11-3 Micron Technology, Inc. Consolidated Balance Sheets (Dollars in Millions)

| As of | 31 Aug. 2006 | 1 Sept. 2005 |

| Assets | ||

| Cash and equivalents | $1,431 | $524 |

| Short-term investments | 1,648 | 766 |

| Receivables | 956 | 794 |

| Inventories | 963 | 771 |

| Prepaid expenses | 77 | 39 |

| Deferred income taxes | 26 | 32 |

| Total current assets | 5,101 | 2,926 |

| Intangible assets, net | 388 | 260 |

| Property, plant, and equipment, net | 5,888 | 4,684 |

| Deferred income taxes | 49 | 30 |

| Goodwill | 502 | 16 |

| Other assets | 293 | 90 |

| Total assets | $12,221 | $8,006 |

| Liabilities and shareholders’ equity | ||

| Accounts payable and accrued expenses | $1,319 | $753 |

| Deferred income | 53 | 30 |

| Equipment purchase contracts | 123 | 49 |

| Current portion of long-term debt | 166 | 147 |

| Total current liabilities | 1,661 | 979 |

| Long-term debt | 405 | 1,020 |

| Deferred income taxes | 28 | 35 |

| Other liabilities | 445 | 125 |

| Total liabilities | 2,539 | 2,159 |

| Commitments and contingencies | — | — |

| Noncontrolling interests in subsidiaries | 1,568 | — |

| Common stock of $0.10 par value, authorized 3 billion shares, issued and outstanding 749.4 million and 616.2 million shares | 75 | 62 |

| Additional capital | 6,555 | 4,707 |

| Retained earnings | 1,486 | 1,078 |

| Accumulated other comprehensive loss | (2) | — |

| Total shareholders’ equity | 8,114 | 5,847 |

| Total liabilities and shareholders’ equity | $12,221 | $8,006 |

EXHIBIT 11-4 Micron Technology, Inc. Income Taxes Note to the Consolidated Financial Statements

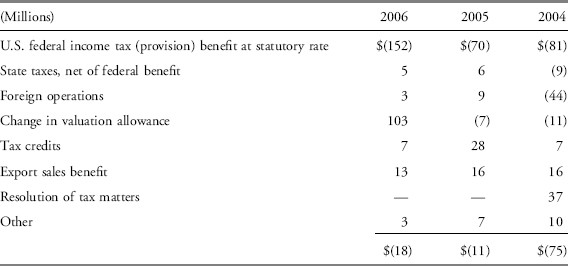

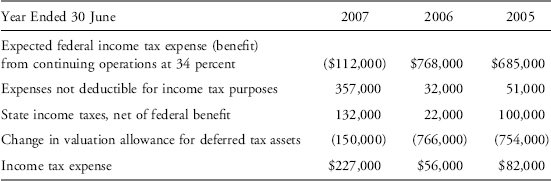

MU’s income tax provision (i.e., income tax expense) for fiscal year 2006 is $18 million (see Exhibit 11-2). The income tax note disclosure in Exhibit 11-4 reconciles how the income tax provision was determined beginning with MU’s reported income before taxes (shown in Exhibit 11-2 as $433 million for fiscal year 2006). The note disclosure then denotes the income tax provision for 2006 that is current ($42 million), which is then offset by the deferred tax benefit for foreign taxes ($24 million), for a net income tax provision of $18 million. Exhibit 11-4 further shows a reconciliation of how the income tax provision was derived from the U.S. federal statutory rate. Many public companies comply with this required disclosure by displaying the information in percentage terms, but MU has elected to provide the disclosure in absolute dollar amounts. From this knowledge, we can see that the dollar amount shown for U.S. federal income tax provision at the statutory rate ($152 million) was determined by multiplying MU’s income before taxes by the 35 percent U.S. federal statutory rate ($433 × 0.35 = $152). Furthermore, after considering tax credits and changes in the valuation allowance for deferred tax assets, MU’s $18 million tax provision for 2006 is only 4.16 percent of its income before taxes ($18 ÷ $433 = 4.16%).

In addition, the note disclosure in Exhibit 11-4 provides detailed information about the derivation of the deferred tax assets ($26 million current and $49 million noncurrent) and deferred tax liabilities ($28 million noncurrent) that are shown on MU’s consolidated balance sheet for fiscal year 2006 in Exhibit 11-3.

The company’s income tax (provision) computed using the U.S. federal statutory rate and the company’s income tax (provision) benefit is reconciled as follows:

State taxes reflect investment tax credits of $23 million, $14 million, and $9 million for 2006, 2005, and 2004, respectively. Deferred income taxes reflect the net tax effects of temporary differences between the bases of assets and liabilities for financial reporting and income tax purposes. The company’s deferred tax assets and liabilities consist of the following as of the end of the periods shown here:

| ($ Millions) | 2006 | 2005 |

| Deferred tax assets: | ||

| Net operating loss and credit carry-forwards | $929 | $1,202 |

| Basis differences in investments in joint ventures | 301 | — |

| Deferred revenue | 160 | 76 |

| Accrued compensation | 51 | 40 |

| Accounts payable | 43 | 25 |

| Inventories | 16 | 33 |

| Accrued product and process technology | 11 | 12 |

| Other | 36 | 87 |

| Gross deferred assets | 1,547 | 1,475 |

| Less valuation allowance | (915) | (1,029) |

| Deferred tax assets, net of valuation allowance | 632 | 446 |

| Deferred tax liabilities: | ||

| Excess tax over book depreciation | (308) | (315) |

| Receivables | (91) | — |

| Intangibles | (68) | — |

| Unremitted earnings on certain subsidiaries | (58) | (49) |

| Product and process technology | (45) | (39) |

| Other | (15) | (16) |

| Deferred tax liabilities | (585) | (419) |

| Net deferred tax assets | $47 | $27 |

| Reported as: | ||

| Current deferred tax assets | $26 | $32 |

| Noncurrent deferred tax assets | 49 | 30 |

| Noncurrent deferred tax liabilities | (28) | (35) |

| Net deferred tax assets | $47 | $27 |

The company has a valuation allowance against substantially all of its U.S. net deferred tax assets. As of 31 August 2006, the company had aggregate U.S. tax net operating loss carry-forwards of $1.7 billion and unused U.S. tax credit carry-forwards of $164 million. The company also has unused state tax net operating loss carry-forwards of $1.4 billion and unused state tax credits of $163 million. During 2006, the company utilized approximately $1.1 billion of its U.S. tax net operating loss carry-forwards as a result of IMFT, MP Mask, and related transactions.5 Substantially all of the net operating loss carry-forwards expire in 2022 to 2025 and substantially all of the tax credit carry-forwards expire in 2013 to 2026.

The changes in valuation allowance of ($114) million and $25 million in 2006 and 2005, respectively, are primarily a result of uncertainties of realizing certain U.S. net operating losses and certain tax credit carry-forwards. The change in the valuation allowance in 2006 and 2005 includes $12 million and $2 million, respectively, for stock plan deductions, which will be credited to additional capital if realized.

Provision has been made for deferred taxes on undistributed earnings of non-U.S. subsidiaries to the extent that dividend payments from such companies are expected to result in additional tax liability. Remaining undistributed earnings of $686 million as of 31 August 2006 have been indefinitely reinvested; therefore, no provision has been made for taxes due upon remittance of these earnings. Determination of the amount of unrecognized deferred tax liability on these unremitted earnings is not practicable.

EXAMPLE 11-6 Financial Analysis Example

Use the financial statement information and disclosures provided by MU in Exhibits 11-2, 11-3, and 11-4 to answer the following questions:

1. MU discloses a valuation allowance of $915 million (see Exhibit 11-4) against total deferred assets of $1,547 million in 2006. Does the existence of this valuation allowance have any implications concerning MU’s future earning prospects?

2. How would MU’s deferred tax assets and deferred tax liabilities be affected if the federal statutory tax rate was changed to 32 percent? Would a change in the rate to 32 percent be beneficial to MU?

3. How would reported earnings have been affected if MU were not using a valuation allowance?

4. How would MU’s $929 million in net operating loss carry-forwards in 2006 (see Exhibit 11-4) affect the valuation that an acquiring company would be willing to offer?

5. Under what circumstances should the analyst consider MU’s deferred tax liability as debt or as equity? Under what circumstances should the analyst exclude MU’s deferred tax liability from both debt and equity when calculating the debt-to-equity ratio?

Solution to 1:

According to Exhibit 11-4, MU’s deferred tax assets expire gradually until 2026 (2022 to 2025 for the net operating loss carry-forwards and 2013 to 2026 for the tax credit carry-forwards).

Because the company is relatively young, it is likely that most of these expirations occur toward the end of that period. Because cumulative federal net operating loss carry-forwards total $1.7 billion, the valuation allowance could imply that MU is not reasonably expected to earn $1.7 billion over the next 20 years. However, as we can see in Exhibit 11-2, MU has earned profits for 2006, 2005, and 2004, thereby showing that the allowance could be adjusted downward if the company continues to generate profits in the future, making it more likely than not that the deferred tax asset would be recognized.

Solution to 2:

MU’s total deferred tax assets exceed total deferred tax liabilities by $47 million. A change in the federal statutory tax rate to 32 percent from the current rate of 35 percent would make these net deferred assets less valuable. Also, because it is possible that the deferred tax asset valuation allowance could be adjusted downward in the future (see discussion to solution 1), the impact could be far greater in magnitude.

Solution to 3:

The disclosure in Exhibit 11-4 shows that the reduction in the valuation allowance reduced the income tax provision as reported on the income statement by $103 million in 2006. Additional potential reductions in the valuation allowance could similarly reduce reported income taxes (actual tax income taxes would not be affected by a valuation allowance established for financial reporting) in future years (see discussion to solution 1).

Solution to 4:

If an acquiring company is profitable, it may be able to use MU’s tax loss carry-forwards to offset its own tax liabilities. The value to an acquirer would be the present value of the carry-forwards, based on the acquirer’s tax rate and expected timing of realization. The higher the acquiring company’s tax rate, and the more profitable the acquirer, the sooner it would be able to benefit. Therefore, an acquirer with a high current tax rate would theoretically be willing to pay more than an acquirer with a lower tax rate.

Solution to 5:

The analyst should classify the deferred tax liability as debt if the liability is expected to reverse with subsequent tax payment. If the liability is not expected to reverse, there is no expectation of a cash outflow and the liability should be treated as equity. By way of example, future company losses may preclude the payment of any income taxes, or changes in tax laws could result in taxes that are never paid. The deferred tax liability should be excluded from both debt and equity when both the amounts and timing of tax payments resulting from the reversals of temporary differences are uncertain.

8. COMPARISON OF IFRS AND U.S. GAAP

As mentioned earlier, though IFRS and U.S. GAAP follow similar conventions on many tax issues, there are some notable differences (such as revaluation). Exhibit 11-5 summarizes many of the key similarities and differences between IFRS and U.S. GAAP. Though both frameworks require a provision for deferred taxes, there are differences in the methodologies.

EXHIBIT 11-5 Deferred Income Tax Issues IFRS and U.S. GAAP Methodology Similarities and Differences

Sources: IFRS: IAS 1, IAS 12, and IFRS 3.

| Issue | IFRS | U.S. GAAP |

| General considerations: | ||

| General approach | Full provision. | Similar to IFRS. |

| Basis for deferred tax assets and liabilities | Temporary differences—i.e., the difference between carrying amount and tax base of assets and liabilities (see exceptions following). | Similar to IFRS. |

| Exceptions (i.e., deferred tax is not provided on the temporary difference) | Nondeductible goodwill (that which is not deductible for tax purposes) does not give rise to taxable temporary differences. | Similar to IFRS, except no initial recognition exemption and special requirements apply in computing deferred tax on leveraged leases. |

| General considerations: | ||

| Initial recognition of an asset or liability in a transaction that: (a) is not a business combination; and (b) affects neither accounting profit nor taxable profit at the time of the transaction. Other amounts that do not have a tax consequence (commonly referred to as permanent differences) exist and depend on the tax rules and jurisdiction of the entity. | ||

| Specific applications: | ||

| Revaluation of plant, property, and equipment and intangible assets | Deferred tax recognized in equity. | Not applicable, as revaluation is prohibited. |

| Foreign nonmonetary assets/liabilities when the tax reporting currency is not the functional currency | Deferred tax is recognized on the difference between the carrying amount, determined using the historical rate of exchange, and the tax base, determined using the balance sheet date exchange rate. | No deferred tax is recognized for differences related to assets and liabilities that are remeasured from local currency into the functional currency resulting from changes in exchange rates or indexing for tax purposes. |

| Investments in subsidiaries—treatment of undistributed profit | Deferred tax is recognized except when the parent is able to control the distribution of profit and it is probable that the temporary difference will not reverse in the foreseeable future. | Deferred tax is required on temporary differences arising after 1992 that relate to investments in domestic subsidiaries, unless such amounts can be recovered tax-free and the entity expects to use that method. No deferred taxes are recognized on undistributed profits of foreign subsidiaries that meet the indefinite reversal criterion. Deferred tax assets may be recorded only to the extent they will reverse in the foreseeable future. |

| Investments in joint ventures—treatment of undistributed profit | Deferred tax is recognized except when the venturer can control the sharing of profits and if it is probable that the temporary difference will not reverse in the foreseeable future. | Deferred tax is required on temporary differences arising after 1992 that relate to investment in domestic corporate joint ventures. No deferred taxes are recognized on undistributed profits of foreign corporate joint ventures that meet the indefinite reversal criterion. Deferred tax assets may be recorded only to the extent they will reverse in the foreseeable future. |

| Investment in associates—treatment of undistributed profit | Deferred tax is recognized except when the investor can control the sharing of profits and it is probable that the temporary difference will not reverse in the foreseeable future. | Deferred tax is recognized on temporary differences relating to investments in investees. |

| Uncertain tax positions | Reflects the tax consequences that follow from the manner in which the entity expects, at the balance sheet date, to be paid to (recovered from) the taxation authorities. | A tax benefit from an uncertain tax position may be recognized only if it is “more likely than not” that the tax position is sustainable based on its technical merits. The tax position is measured as the largest amount of tax benefit that is greater than 50 percent likely of being realized upon ultimate settlement. |

| Measurement of deferred tax: | ||

| Tax rates | Tax rates and tax laws that have been enacted or substantively enacted. | Use of substantively enacted rates is not permitted. Tax rate and tax laws used must have been enacted. |

| Recognition of deferred tax assets | A deferred tax asset is recognized if it is probable (more likely than not) that sufficient taxable profit will be available against which the temporary difference can be utilized. | A deferred tax asset is recognized in full but is then reduced by a valuation allowance if it is more likely than not that some or all of the deferred tax asset will not be realized. |

| Business combinations—Acquisitions: | ||

| Step-up of acquired assets/liabilities to fair value | Deferred tax is recorded unless the tax base of the asset is also stepped up. | Similar to IFRS. |

| Previously unrecognized tax losses of the acquirer | A deferred tax asset is recognized if the recognition criteria for the deferred tax asset are met as a result of the acquisition. Offsetting credit is recorded in income. | Similar to IFRS, except the offsetting credit is recorded against goodwill. |

| Tax losses of the acquiree (initial recognition) | Similar requirements as for the acquirer except the offsetting credit is recorded against goodwill. | Similar to IFRS. |

| Subsequent resolution of income tax uncertainties in a business combination | If the resolution is more than one year after the year in which the business combination occurred, the result is recognized on the income statement. | The subsequent resolution of any tax uncertainty relating to a business combination is recorded against goodwill. |

| Subsequent recognition of deferred tax assets that were not “probable” at the time of the business combination | A deferred tax asset that was not considered probable at the time of the business combination but later becomes probable is recognized. The adjustment is to income tax expense with a corresponding adjustment to goodwill. The income statement shows a debit to goodwill expense and a credit to income tax expense. There is no time limit for recognition of this deferred tax asset. | The subsequent resolution of any tax uncertainty relating to a business combination is recorded first against goodwill, then noncurrent intangibles, and then income tax expense. There is no time limit for recognition of this deferred tax asset. |

| Presentation of deferred tax: | ||

| Offset of deferred tax assets and liabilities | Permitted only when the entity has a legally enforceable right to offset and the balance relates to tax levied by the same authority. | Similar to IFRS. |

| Current/noncurrent | Deferred tax assets and liabilities are classified net as noncurrent on the balance sheet, with supplemental note disclosure for (1) the components of the temporary differences, and (2) amounts expected to be recovered within 12 months and more than 12 months from the balance sheet date. | Deferred tax assets and liabilities are either classified as current or noncurrent, based on the classification of the related nontax asset or liability for financial reporting. Tax assets or liabilities not associated with an underlying asset or liability are classified based on the expected reversal period. |

| Reconciliation of actual and expected tax expense | Required. Computed by applying the applicable tax rates to accounting profit, disclosing also the basis on which the applicable tax rates are calculated. | Required for public companies only. Calculated by applying the domestic federal statutory tax rates to pretax income from continuing operations. |

U.S. GAAP: FAS 109 and FIN 48.

“Similarities and Differences—A Comparison of IFRS and U.S. GAAP,” PricewaterhouseCoopers, October 2006.

Income taxes are a significant category of expense for profitable companies. Analyzing income tax expenses is often difficult for the analyst because there are many permanent and temporary timing differences between the accounting that is used for income tax reporting and the accounting that is used for financial reporting on company financial statements. The financial statements and notes to the financial statements of a company provide important information that the analyst needs to assess financial performance and to compare a company’s financial performance with other companies. Key concepts in this reading are as follows:

- Differences between the recognition of revenue and expenses for tax and accounting purposes may result in taxable income differing from accounting profit. The discrepancy is a result of different treatments of certain income and expenditure items.

- The tax base of an asset is the amount that will be deductible for tax purposes as an expense in the calculation of taxable income as the company expenses the tax basis of the asset. If the economic benefit will not be taxable, the tax base of the asset will be equal to the carrying amount of the asset.

- The tax base of a liability is the carrying amount of the liability less any amounts that will be deductible for tax purposes in the future. With respect to revenue received in advance, the tax base of such a liability is the carrying amount less any amount of the revenue that will not be taxable in the future.

- Temporary differences arise from recognition of differences in the tax base and carrying amount of assets and liabilities. The creation of a deferred tax asset or liability as a result of a temporary difference will only be allowed if the difference reverses itself at some future date and to the extent that it is expected that the balance sheet item will create future economic benefits for the company.