5.1 General Tax Rules for Property Sales

by J.K. Lasser Institute

J.K. Lasser's Your Income Tax 2013: For Preparing Your 2012 Tax Return

5.1 General Tax Rules for Property Sales

by J.K. Lasser Institute

J.K. Lasser's Your Income Tax 2013: For Preparing Your 2012 Tax Return

- Cover

- Contents: Chapter by Chapter

- Title

- Copyright

- What’s New for 2012

- Key Tax Numbers for 2012

- Looking Ahead to 2013

- Part 1: Filing Basics

- Do You Have to File a 2012 Tax Return?

- Filing Tests for Dependents: 2012 Returns

- Where to File

- Filing Deadlines (on or before)

- Choosing Which Tax Form to File

- Chapter 1: Filing Status

- 1.1 Which Filing Status Should You Use?

- 1.2 Tax Rates Based on Filing Status

- 1.3 Filing Separately Instead of Jointly

- 1.4 Filing a Joint Return

- 1.5 Nonresident Alien Spouse

- 1.6 Community Property Rules

- 1.7 Innocent Spouse Rules

- 1.8 Separate Liability Election for Former Spouses

- 1.9 Equitable Relief

- 1.10 Death of Your Spouse in 2012

- 1.11 Qualifying Widow(er) Status If Your Spouse Died in 2011 or 2010

- 1.12 Qualifying as Head of Household

- 1.13 Filing for Your Child

- 1.14 Return for Deceased

- 1.15 Return for an Incompetent Person

- 1.16 How a Nonresident Alien Is Taxed

- 1.17 How a Resident Alien Is Taxed

- 1.18 Who Is a Resident Alien?

- 1.19 When an Alien Leaves the United States

- 1.20 Expatriation Tax

- Part 2: Reporting Your Income

- Chapter 2: Wages, Salary, and Other Compensation

- 2.1 Salary and Wage Income

- 2.2 Constructive Receipt of Year-End Paychecks

- 2.3 Pay Received in Property Is Taxed

- 2.4 Commissions Taxable When Credited

- 2.5 Unemployment Benefits

- 2.6 Strike Pay Benefits and Penalties

- 2.7 Nonqualified Deferred Compensation

- 2.8 Did You Return Wages Received in a Prior Year?

- 2.9 Waiver of Executor’s and Trustee’s Commissions

- 2.10 Life Insurance Benefits

- 2.11 Educational Benefits for Employees’ Children

- 2.12 Sick Pay Is Taxable

- 2.13 Workers’ Compensation Is Tax Free

- 2.14 Disability Pensions

- 2.15 Stock Appreciation Rights (SARs)

- 2.16 Stock Options

- 2.17 Restricted Stock

- Chapter 3: Fringe Benefits

- 3.1 Tax-Free Health and Accident Coverage Under Employer Plans

- 3.2 Health Savings Accounts (HSAs) and Archer MSAs

- 3.3 Reimbursements and Other Tax-Free Payments From Employer Health and Accident Plans

- 3.4 Group-Term Life Insurance Premiums

- 3.5 Dependent Care Assistance

- 3.6 Adoption Benefits

- 3.7 Education Assistance Plans

- 3.8 Company Cars, Parking, and Transit Passes

- 3.9 Working Condition Fringe Benefits

- 3.10 De Minimis Fringe Benefits

- 3.11 Employer-Provided Retirement Advice

- 3.12 Employee Achievement Awards

- 3.13 Employer-Furnished Meals or Lodging

- 3.14 Minister’s Rental or Housing Allowance

- 3.15 Cafeteria Plans Provide Choice of Benefits

- 3.16 Flexible Spending Arrangements

- 3.17 Company Services Provided at No Additional Cost

- 3.18 Discounts on Company Products or Services

- Chapter 4: Dividend and Interest Income

- 4.1 Reporting Dividends and Mutual-Fund Distributions

- 4.2 Qualified Corporate Dividends Taxed at Favorable Capital Gain Rates

- 4.3 Dividends From a Partnership, S Corporation, Estate, or Trust

- 4.4 Real Estate Investment Trust (REIT) Dividends

- 4.5 Taxable Dividends of Earnings and Profits

- 4.6 Stock Dividends on Common Stock

- 4.7 Dividends Paid in Property

- 4.8 Taxable Stock Dividends

- 4.9 Who Reports the Dividends

- 4.10 Year Dividends Are Reported

- 4.11 Distribution Not Out of Earnings: Return of Capital

- 4.12 Reporting Interest on Your Tax Return

- 4.13 Interest on Frozen Accounts Not Taxed

- 4.14 Interest Income on Debts Owed to You

- 4.15 Reporting Interest on Bonds Bought or Sold

- 4.16 Forfeiture of Interest on Premature Withdrawals

- 4.17 Amortization of Bond Premium

- 4.18 Discount on Bonds

- 4.19 Reporting Original Issue Discount on Your Return

- 4.20 Reporting Income on Market Discount Bonds

- 4.21 Discount on Short-Term Obligations

- 4.22 Stripped Coupon Bonds and Stock

- 4.23 Sale or Retirement of Bonds and Notes

- 4.24 State and City Interest Generally Tax Exempt

- 4.25 Taxable State and City Interest

- 4.26 Tax-Exempt Bonds Bought at a Discount

- 4.27 Treasury Bills, Notes, and Bonds

- 4.28 Interest on United States Savings Bonds

- 4.29 Deferring United States Savings Bond Interest

- 4.30 Minimum Interest Rules

- 4.31 Interest-Free or Below-Market-Interest Loans

- 4.32 Minimum Interest on Seller-Financed Sales

- Chapter 5: Reporting Property Sales

- 5.1 General Tax Rules for Property Sales

- 5.2 How Property Sales Are Classified and Taxed

- 5.3 Capital Gains Rates and Holding Periods

- 5.4 Capital Losses and Carryovers

- 5.5 Capital Losses of Married Couples

- 5.6 Losses May Be Disallowed on Sales to Related Persons

- 5.7 Deferring or Excluding Gain on Small Business Stock Investment

- 5.8 Sample Entries of Capital Asset Sales on Form 8949 and on Schedule D

- 5.9 Counting the Months in Your Holding Period

- 5.10 Holding Period for Securities

- 5.11 Holding Period for Real Estate

- 5.12 Holding Period: Gifts, Inheritances, and Other Property

- 5.13 Calculating Gain or Loss

- 5.14 Amount Realized Is the Total Selling Price

- 5.15 Finding Your Cost

- 5.16 Unadjusted Basis of Your Property

- 5.17 Basis of Property You Inherited or Received as a Gift

- 5.18 Joint Tenancy Basis Rules for Surviving Tenants

- 5.19 Allocating Cost Among Several Assets

- 5.20 How To Find Adjusted Basis

- 5.21 Tax Advantage of Installment Sales

- 5.22 Figuring the Taxable Part of Installment Payments

- 5.23 Electing Not To Report on the Installment Method

- 5.24 Restriction on Installment Sales to Relatives

- 5.25 Contingent Payment Sales

- 5.26 Using Escrow and Other Security Arrangements

- 5.27 Minimum Interest on Deferred Payment Sales

- 5.28 Dispositions of Installment Notes

- 5.29 Repossession of Personal Property Sold on Installment

- 5.30 Boot in Like-Kind Exchange Payable in Installments

- 5.31 “Interest” Tax on Sales Over $150,000 Plus $5 Million Debt

- 5.32 Worthless Securities

- 5.33 Tax Consequences of Bad Debts

- 5.34 Four Rules To Prove a Bad Debt Deduction

- 5.35 Family Bad Debts

- Chapter 6: Tax-Free Exchanges of Property

- 6.1 Trades of Like-Kind Property

- 6.2 Personal Property Held for Business or Investment

- 6.3 Receipt of Cash and Other Property—“Boot”

- 6.4 Time Limits and Security Arrangements for Deferred Exchanges

- 6.5 Qualified Exchange Accommodation Arrangements (QEAAs) for Reverse Exchanges

- 6.6 Exchanges Between Related Parties

- 6.7 Property Transfers Between Spouses and Ex-Spouses

- 6.8 Tax-Free Exchanges of Stock in Same Corporation

- 6.9 Joint Ownership Interests

- 6.10 Setting up Closely Held Corporations

- 6.11 Exchanges of Coins and Bullion

- 6.12 Tax-Free Exchanges of Insurance Policies

- Chapter 7: Retirement and Annuity Income

- 7.1 Retirement Distributions on Form 1099-R

- 7.2 Lump-Sum Distributions

- 7.3 Lump-Sum Options If You Were Born Before January 2, 1936

- 7.4 Averaging on Form 4972

- 7.5 Capital Gain Treatment for Pre-1974 Participation

- 7.6 Lump-Sum Payments Received by Beneficiary

- 7.7 Tax-Free Rollovers From Qualified Plans

- 7.8 Direct Rollover or Personal Rollover

- 7.9 Rollover of Proceeds From Sale of Property

- 7.10 Distribution of Employer Stock or Other Securities

- 7.11 Survivor Annuity for Spouse

- 7.12 Court Distributions to Former Spouse Under a QDRO

- 7.13 When Retirement Benefits Must Begin

- 7.14 Payouts to Beneficiaries

- 7.15 Penalty for Distributions Before Age 59½

- 7.16 Restrictions on Loans From Company Plans

- 7.17 Tax Benefits of 401(k) Plans

- 7.18 Limit on Salary-Reduction Deferrals

- 7.19 Withdrawals From 401(k) Plans Restricted

- 7.20 Designated Roth Contributions to 401(k) Plans

- 7.21 Annuities for Employees of Tax-Exempts and Schools (403(b) Plans)

- 7.22 Government and Exempt Organization Deferred Pay Plans

- 7.23 Figuring the Taxable Part of Your Annuity

- 7.24 Life Expectancy Tables

- 7.25 When You Convert Your Endowment Policy

- 7.26 Reporting Employee Annuities

- 7.27 Simplified Method for Calculating Taxable Employee Annuity

- 7.28 Employee’s Cost in Annuity

- 7.29 Withdrawals From Employer’s Qualified Retirement Plan Before Annuity Starting Date

- Chapter 8: IRAs

- 8.1 Starting a Traditional IRA

- 8.2 Traditional IRA Contributions Must Be Based on Earnings

- 8.3 Contributions to a Traditional IRA If You Are Married

- 8.4 IRA Deduction Restrictions for Active Participants in Employer Plan

- 8.5 Active Participation in Employer Plan

- 8.6 Nondeductible Contributions to Traditional IRAs

- 8.7 Penalty for Excess Contributions to Traditional IRAs

- 8.8 Taxable Distributions From Traditional IRAs

- 8.9 Partially Tax-Free Traditional IRA Distributions Allocable to Nondeductible Contributions

- 8.10 Tax-Free Rollovers and Direct Transfers to Traditional IRAs

- 8.11 Transfer of Traditional IRA to Spouse at Divorce

- 8.12 Penalty for Traditional IRA Withdrawals Before Age 59½

- 8.13 Mandatory Distributions From a Traditional IRA After Age 70½

- 8.14 Inherited Traditional IRAs

- 8.15 SEP Basics

- 8.16 Salary-Reduction SEP Set Up Before 1997

- 8.17 Who Is Eligible for a SIMPLE IRA?

- 8.18 SIMPLE IRA Contributions and Distributions

- 8.19 Roth IRA Advantages

- 8.20 Annual Contributions to a Roth IRA

- 8.21 Converting a Traditional IRA to a Roth IRA

- 8.22 Recharacterizations and Reconversions

- 8.23 Distributions From a Roth IRA

- 8.24 Distributions to Roth IRA Beneficiaries

- Chapter 9: Income From Real Estate Rentals and Royalties

- 9.1 Reporting Rental Real Estate Income and Expenses

- 9.2 Checklist of Rental Deductions

- 9.3 Distinguishing Between a Repair and an Improvement

- 9.4 Reporting Rents From a Multi-Unit Residence

- 9.5 Depreciation on Converting a Home to Rental Property

- 9.6 Renting a Residence to a Relative

- 9.7 Personal Use and Rental of a Residence During the Year

- 9.8 Counting Personal-Use Days and Rental Days for a Residence

- 9.9 Allocating Expenses of a Residence to Rental Days

- 9.10 Rentals Lacking Profit Motive

- 9.11 Reporting Royalty Income

- 9.12 Production Costs of Books and Creative Properties

- 9.13 Deducting the Cost of Patents or Copyrights

- 9.14 Intangible Drilling Costs

- 9.15 Depletion Deduction

- 9.16 Oil and Gas Percentage Depletion

- Chapter 10: Loss Restrictions: Passive Activities and At-Risk Limits

- 10.1 Rental Activities

- 10.2 Rental Real Estate Loss Allowance of up to $25,000

- 10.3 Real Estate Professionals

- 10.4 Participation May Avoid Passive Loss Restrictions

- 10.5 Classifying Business Activities as One or Several

- 10.6 Material Participation Tests for Business

- 10.7 Tax Credits of Passive Activities Limited

- 10.8 Determining Passive or Nonpassive Income and Loss

- 10.9 Passive Income Recharacterized as Nonpassive Income

- 10.10 Working Interests in Oil and Gas Wells

- 10.11 Partners and Members of LLCs and LLPs

- 10.12 Form 8582

- 10.13 Suspended Losses Allowed on Disposition of Your Interest

- 10.14 Suspended Tax Credits

- 10.15 Personal Service and Closely Held Corporations

- 10.16 Sales of Property and of Passive Activity Interests

- 10.17 At-Risk Limits

- 10.18 What Is At Risk?

- 10.19 Amounts Not At Risk

- 10.20 At-Risk Investment in Several Activities

- 10.21 Carryover of Disallowed Losses

- 10.22 Recapture of Losses Where At Risk Is Less Than Zero

- Chapter 11: Other Income

- 11.1 Prizes and Awards

- 11.2 Lottery and Sweepstake Winnings

- 11.3 Gambling Winnings and Losses

- 11.4 Gifts and Inheritances

- 11.5 Refunds of State and Local Income Tax Deductions

- 11.6 Other Recovered Deductions

- 11.7 How Legal Damages Are Taxed

- 11.8 Cancellation of Debts You Owe

- 11.9 Schedule K-1

- 11.10 How Partners Report Partnership Profit and Loss

- 11.11 When a Partner Reports Income or Loss

- 11.12 Partnership Loss Limitations

- 11.13 Unified Tax Audits of Partnerships

- 11.14 Stockholder Reporting of S Corporation Income and Loss

- 11.15 How Beneficiaries Report Estate or Trust Income

- 11.16 Reporting Income in Respect of a Decedent (IRD)

- 11.17 Deduction for Estate Tax Attributable to IRD

- 11.18 How Life Insurance Proceeds Are Taxed to a Beneficiary

- 11.19 A Policy With a Family Income Rider

- 11.20 Selling or Surrendering Life Insurance Policy

- 11.21 Jury Duty Fees

- 11.22 Foster Care Payments

- Chapter 2: Wages, Salary, and Other Compensation

- Part 3: Claiming Deductions

- Chapter 12: Deductions Allowed in Figuring Adjusted Gross Income

- 12.1 Figuring Adjusted Gross Income (AGI)

- 12.2 Claiming Deductions From Gross Income

- 12.3 What Moving Costs Are Deductible?

- 12.4 The Distance Test

- 12.5 The 39-Week Test for Employees

- 12.6 The 78-Week Test for the Self-Employed and Partners

- 12.7 Claiming Deductible Moving Expenses

- 12.8 Reimbursements of Moving Expenses

- Chapter 13: Claiming the Standard Deduction or Itemized Deductions

- Chapter 14: Charitable Contribution Deductions

- 14.1 Deductible Contributions

- 14.2 Nondeductible Contributions

- 14.3 Contributions That Provide You With Benefits

- 14.4 Unreimbursed Expenses of Volunteer Workers

- 14.5 Support of a Student in Your Home

- 14.6 What Kind of Property Are You Donating?

- 14.7 Cars, Clothing, and Other Property Valued Below Cost

- 14.8 Bargain Sales of Appreciated Property

- 14.9 Art Objects

- 14.10 Interests in Real Estate

- 14.11 Life Insurance

- 14.12 Business Inventory

- 14.13 Donations Through Trusts

- 14.14 Records Needed To Substantiate Your Contributions

- 14.15 Form 8283 and Written Appraisal Requirements for Property Donations

- 14.16 Penalty for Substantial Overvaluation of Property

- 14.17 Ceiling on Charitable Contributions

- 14.18 Carryover for Excess Donations

- 14.19 Election To Reduce Fair Market Value by Appreciation

- Chapter 15: Itemized Deduction for Interest Expenses

- 15.1 Home Mortgage Interest

- 15.2 Home Acquisition Loans

- 15.3 Home Equity Loans

- 15.4 Home Construction Loans

- 15.5 Home Improvement Loans

- 15.6 Mortgage Insurance Premiums and Other Payment Rules

- 15.7 Interest on Refinanced Loans

- 15.8 “Points”

- 15.9 Cooperative and Condominium Apartments

- 15.10 Investment Interest Limitations

- 15.11 Debts To Carry Tax-Exempt Obligations

- 15.12 Earmarking Use of Loan Proceeds For Investment or Business

- 15.13 Year To Claim an Interest Deduction

- 15.14 Prepaid Interest

- Chapter 16: Deductions for Taxes

- 16.1 Deductible Taxes

- 16.2 Nondeductible Taxes

- 16.3 State and Local Income Taxes or General Sales Taxes

- 16.4 Deducting Real Estate Taxes

- 16.5 Assessments

- 16.6 Tenants’ Payment of Taxes

- 16.7 Allocating Taxes When You Sell or Buy Realty

- 16.8 Automobile License Fees

- 16.9 Taxes Deductible as Business Expenses

- 16.10 Foreign Taxes

- Chapter 17: Medical and Dental Expense Deductions

- 17.1 Medical Expenses Must Exceed AGI Threshold

- 17.2 Allowable Medical Care Costs

- 17.3 Nondeductible Medical Expenses

- 17.4 Reimbursements Reduce Deductible Expenses

- 17.5 Premiums of Medical Care Policies

- 17.6 Expenses of Your Spouse

- 17.7 Expenses of Your Dependents

- 17.8 Decedent’s Medical Expenses

- 17.9 Travel Costs May Be Medical Deductions

- 17.10 Schooling for the Mentally or Physically Disabled

- 17.11 Nursing Homes

- 17.12 Nurses’ Wages

- 17.13 Home Improvements as Medical Expenses

- 17.14 Costs Deductible as Business Expenses

- 17.15 Long-Term Care Premiums and Services

- 17.16 Life Insurance Used by Chronically ill or Terminally ill Persons

- Chapter 18: Casualty and Theft Losses and Involuntary Conversions

- 18.1 Sudden Event Test for Casualty Losses

- 18.2 When To Deduct a Casualty Loss

- 18.3 Disaster Losses

- 18.4 Who May Deduct a Casualty Loss

- 18.5 Bank Deposit Losses

- 18.6 Damage to Trees and Shrubs

- 18.7 Deducting Damage to Your Car

- 18.8 Proving a Casualty Loss

- 18.9 Theft Losses

- 18.10 Proving a Theft Loss

- 18.11 Nondeductible Casualty and Theft Losses

- 18.12 Floors for Personal-Use Property Losses

- 18.13 Figuring Your Loss on Form 4684

- 18.14 Personal and Business Use of Property

- 18.15 Repairs May Be a “Measure of Loss”

- 18.16 Insurance Reimbursements

- 18.17 Excess Living Costs Paid by Insurance Are Not Taxable

- 18.18 Do Your Casualty or Theft Losses Exceed Your Income?

- 18.19 Defer Gain by Replacing Property

- 18.20 Involuntary Conversions Qualifying for Tax Deferral

- 18.21 How To Elect To Defer Tax

- 18.22 Time Period for Buying Replacement Property

- 18.23 Types of Qualifying Replacement Property

- 18.24 Cost of Replacement Property Determines Postponed Gain

- 18.25 Special Assessments and Severance Damages

- 18.26 Reporting Gains From Casualties

- Chapter 19: Deducting Job Costs and Other Miscellaneous Expenses

- 19.1 2% AGI Floor Reduces Most Miscellaneous Expenses

- 19.2 Effect of 2% AGI Floor on Deductions

- 19.3 Checklist of Job Expenses Subject to the 2% AGI Floor

- 19.4 Job Expenses Not Subject to the 2% AGI Floor

- 19.5 Dues and Subscriptions

- 19.6 Uniforms and Work Clothes

- 19.7 Expenses of Looking for a New Job

- 19.8 Local Transportation Costs

- 19.9 Unusual Job Expenses

- 19.10 Computers Bought for Work

- 19.11 Cell Phones, Calculators, Copiers and Fax Machines

- 19.12 Small Tools

- 19.13 Employee Home Office Deductions

- 19.14 Telephone Costs

- 19.15 Checklist of Deductible Investment Expenses

- 19.16 Costs of Tax Return Preparation and Audits

- 19.17 Deducting Legal Costs

- 19.18 Contingent Fees Paid Out of Taxable Awards

- Chapter 20: Travel and Entertainment Expense Deductions

- 20.1 Deduction Guide for Travel and Transportation Expenses

- 20.2 Commuting Expenses

- 20.3 Overnight-Sleep Test Limits Deduction of Meal Costs

- 20.4 IRS Meal Allowance

- 20.5 Business Trip Deductions

- 20.6 Local Lodging Costs

- 20.7 When Are You Away From Home?

- 20.8 Fixing a Tax Home If You Work in Different Locations

- 20.9 Tax Home of Married Couple Working in Different Cities

- 20.10 Deducting Living Costs on Temporary Assignment

- 20.11 Business-Vacation Trips Within the United States

- 20.12 Business-Vacation Trips Outside the United States

- 20.13 Deducting Expenses of Business Conventions

- 20.14 Travel Expenses of a Spouse or Dependents

- 20.15 Restrictions on Foreign Conventions and Cruises

- 20.16 50% Deduction Limit

- 20.17 The Restrictive Tests for Meals and Entertainment

- 20.18 Directly Related Dining and Entertainment

- 20.19 Goodwill Entertainment

- 20.20 Home Entertaining

- 20.21 Your Personal Share of Entertainment Costs

- 20.22 Entertainment Costs of Spouses

- 20.23 Entertainment Facilities and Club Dues

- 20.24 Restrictive Test Exception for Reimbursements

- 20.25 50% Cost Limitation on Meals and Entertainment

- 20.26 Business Gift Deductions Are Limited

- 20.27 Record-Keeping Requirements

- 20.28 Proving Travel and Entertainment Expenses

- 20.29 Reporting T&E Expenses If You Are Self-Employed

- 20.30 Employee Reporting of Unreimbursed T&E Expenses

- 20.31 Tax Treatment of Reimbursements

- 20.32 What Is an Accountable Plan?

- 20.33 Per Diem Travel Allowance Under Accountable Plans

- 20.34 Automobile Mileage Allowance

- 20.35 Reimbursements Under Non-Accountable Plans

- Chapter 21: Personal Exemptions

- 21.1 How Many Exemptions May You Claim?

- 21.2 Your Spouse as an Exemption

- 21.3 Qualifying Children

- 21.4 Qualifying Relatives

- 21.5 Meeting the Support Test for a Qualifying Relative

- 21.6 Multiple Support Agreements

- 21.7 Special Rule for Divorced or Separated Parents

- 21.8 The Dependent Must Meet a Citizen or Resident Test

- 21.9 The Dependent Does Not File a Joint Return

- 21.10 Spouses’ Names and Social Security Numbers on Joint Return

- 21.11 Reporting Social Security Numbers of Dependents

- 21.12 Personal Exemptions Not Subject to Phaseout for 2012

- Chapter 12: Deductions Allowed in Figuring Adjusted Gross Income

- Part 4: Personal Tax Computations

- Chapter 22: Figuring Your Regular Income Tax Liability

- Chapter 23: Alternative Minimum Tax (AMT)

- Chapter 24: Computing the “Kiddie Tax” on Your Child’s Investment Income

- Chapter 25: Personal Tax Credits Reduce Your Tax Liability

- 25.1 Overview of Personal Tax Credits

- 25.2 Child Tax Credit for Children Under Age 17

- 25.3 Figuring the Child Tax Credit

- 25.4 Qualifying for Child and Dependent Care Credit

- 25.5 Limits on the Dependent Care Credit

- 25.6 Earned Income Test for Dependent Care Credit

- 25.7 Credit Allowed for Care of Qualifying Persons

- 25.8 Expenses Qualifying for the Dependent Care Credit

- 25.9 Dependent Care Credit Rules for Separated Couples

- 25.10 Qualifying Tests for EIC

- 25.11 Income Tests for Earned Income Credit (EIC)

- 25.12 Look up EIC in Government Tables

- 25.13 Qualifying for the Adoption Credit

- 25.14 Claiming the Adoption Credit on Form 8839

- 25.15 Eligibility for the Saver’s Credit

- 25.16 Figuring the Saver’s Credit

- 25.17 Health Coverage Credit

- 25.18 Mortgage Interest Credit

- 25.19 Residential Energy Credits

- 25.20 Credits for Fuel Cell Vehicles and Plug-in Electric Vehicles

- 25.21 Repayment of the First-Time Homebuyer Credit

- Chapter 26: Tax Withholdings

- 26.1 Withholdings Should Cover Estimated Tax

- 26.2 Income Taxes Withheld on Wages

- 26.3 Low Earners May Be Exempt From Withholding

- 26.4 Are You Withholding the Right Amount?

- 26.5 Voluntary Withholding on Government Payments

- 26.6 When Tips Are Subject to Withholding

- 26.7 Withholding on Gambling Winnings

- 26.8 FICA Withholdings

- 26.9 Withholding on Retirement Distributions

- 26.10 Backup Withholding

- Chapter 27: Estimated Tax Payments

- Part 5: Tax Planning

- Chapter 28: Tax Planning Overview

- Chapter 29: Tax Savings for Residence Sales

- 29.1 Avoiding Tax on Sale of Principal Residence

- 29.2 Meeting the Ownership and Use Tests

- 29.3 Home Sales by Married Persons

- 29.4 Reduced Maximum Exclusion

- 29.5 Figuring Gain or Loss

- 29.6 Figuring Adjusted Basis

- 29.7 Personal and Business Use of a Home

- 29.8 No Loss Allowed on Personal Residence

- 29.9 Loss on Residence Converted to Rental Property

- 29.10 Loss on Residence Acquired by Gift or Inheritance

- Chapter 30: Tax Rules for Investors in Securities

- 30.1 Planning Year-End Securities Transactions

- 30.2 Earmarking Stock Lots

- 30.3 Sale of Stock Dividends

- 30.4 Stock Rights

- 30.5 Short Sales of Stock

- 30.6 Wash Sales

- 30.7 Convertible Stocks and Bonds

- 30.8 Constructive Sales of Appreciated Financial Positions

- 30.9 Straddle Losses

- 30.10 Capital Gain Restricted on Conversion Transactions

- 30.11 Puts and Calls and Index Options

- 30.12 Investing in Tax-Exempts

- 30.13 Ordinary Loss for Small Business Stock (Section 1244)

- 30.14 Series EE Bonds

- 30.15 I Bonds

- 30.16 Trader, Dealer, or Investor?

- 30.17 Mark-to-Market Election for Traders

- Chapter 31: Tax Savings for Investors in Real Estate

- 31.1 Real Estate Ventures

- 31.2 Sales of Subdivided Land—Dealer or Investor?

- 31.3 Exchanging Real Estate Without Tax

- 31.4 Timing Your Real Property Sales

- 31.5 Cancellation of a Lease

- 31.6 Sale of an Option

- 31.7 Granting of an Easement

- 31.8 Special Tax Credits for Real Estate Investments

- 31.9 Foreclosures, Repossessions, Short Sales, and Voluntary Conveyances to Creditors

- 31.10 Restructuring Mortgage Debt

- 31.11 Abandonments

- 31.12 Seller’s Repossession After Buyer’s Default on Mortgage

- 31.13 Foreclosure on Mortgages Other Than Purchase Money

- 31.14 Foreclosure Sale to Third Party

- 31.15 Transferring Mortgaged Realty

- Chapter 32: Tax Rules for Investors in Mutual Funds

- 32.1 Timing of Your Investment Can Affect Your Taxes

- 32.2 Reinvestment Plans

- 32.3 Mutual-Fund Distributions Reported on Form 1099-DIV

- 32.4 Tax-Exempt Bond Funds

- 32.5 Fund Expenses

- 32.6 Tax Credits From Mutual Funds

- 32.7 How To Report Mutual Fund Distributions

- 32.8 Redemptions and Exchanges of Fund Shares

- 32.9 Basis of Redeemed Shares

- 32.10 Comparison of Basis Methods

- Chapter 33: Educational Tax Benefits

- 33.1 Scholarships and Grants

- 33.2 Tuition Reductions for College Employees

- 33.3 How Fulbright Awards Are Taxed

- 33.4 United States Savings Bond Tuition Plans

- 33.5 Contributing to a Qualified Tuition Program (Section 529 Plan)

- 33.6 Distributions From Qualified Tuition Programs (Section 529 Plans)

- 33.7 Education Tax Credits

- 33.8 American Opportunity Credit

- 33.9 Lifetime Learning Credit

- 33.10 Contributing to a Coverdell Education Savings Account (ESA)

- 33.11 Distributions From Coverdell ESAs

- 33.12 Tuition and Fees Deduction

- 33.13 Student Loan Interest Deduction

- 33.14 Types of Deductible Work-Related Costs

- 33.15 Work-Related Tests for Education Costs

- 33.16 Local Transportation and Travel Away From Home To Take Courses

- Chapter 34: Special Tax Rules for Senior Citizens

- 34.1 Senior Citizens Get Certain Filing Breaks

- 34.2 Social Security Benefits Subject to Tax

- 34.3 Computing Taxable Social Security Benefits

- 34.4 Election for Lump-Sum Social Security Benefit Payment

- 34.5 Retiring on Social Security Benefits

- 34.6 How Tax on Social Security Reduces Your Earnings

- 34.7 Claiming the Credit for the Elderly and Disabled

- 34.8 Base Amount for the Elderly or Disabled Credit

- 34.9 Reduction of the Base Amount and Liability Limitation for the Credit

- 34.10 Tax Effects of Moving to a Continuing Care Facility

- 34.11 Medicare Part B and Part D Premiums for 2013

- Chapter 35: Members of the Armed Forces

- 35.1 Taxable Armed Forces Pay and Benefits

- 35.2 Tax-Free Armed Forces Benefits

- 35.3 Deductions for Armed Forces Personnel

- 35.4 Tax-Free Pay for Service in Combat Zone

- 35.5 Tax Deadlines Extended for Combat Zone or Contingency Operation Service

- 35.6 Tax Forgiveness for Combat Zone or Terrorist or Military Action Deaths

- 35.7 Extension To Pay Your Tax When Entering the Service

- 35.8 Tax Information for Reservists

- Chapter 36: How To Treat Foreign Earned Income

- 36.1 Claiming the Foreign Earned Income Exclusion

- 36.2 What Is Foreign Earned Income?

- 36.3 Qualifying for the Foreign Earned Income Exclusion

- 36.4 How To Treat Housing Costs

- 36.5 Meeting the Foreign Residence or Physical Presence Test

- 36.6 Claiming Deductions

- 36.7 Exclusion Not Established When Your Return Is Due

- 36.8 Tax-Free Meals and Lodging for Workers in Camps

- 36.9 Virgin Islands, Samoa, Guam, and Northern Marianas

- 36.10 Earnings in Puerto Rico

- 36.11 Tax Treaties With Foreign Countries

- 36.12 Exchange Rates and Blocked Currency

- 36.13 Foreign Tax Credit

- Chapter 37: Planning Alimony and Marital Settlements

- 37.1 Planning Alimony Agreements

- 37.2 Decree or Agreement Required

- 37.3 Cash Payments Required

- 37.4 Payments Must Stop at Death

- 37.5 Child Support Payments Are Not Alimony

- 37.6 No Minimum Payment Period for Alimony

- 37.7 3rd Year Recapture If Alimony Drops by More Than $15,000

- 37.8 Legal Fees of Marital Settlements

- Chapter 38: Household Employment Taxes (“Nanny Tax”)

- Chapter 39: Gift and Estate Tax Planning Basics

- 39.1 Gifts of Appreciated Property

- 39.2 Gift Tax Basics

- 39.3 Filing a Gift Tax Return

- 39.4 Gift Tax Credit

- 39.5 Custodial Accounts for Minors

- 39.6 Trusts in Family Planning

- 39.7 What is the Estate Tax?

- 39.8 Take Inventory and Estimate the Value of Your Potential Estate

- 39.9 Estate Tax for 2012

- 39.10 Planning for a Potential Estate Tax

- Part 6: Business Tax Planning

- Chapter 40: Income or Loss From Your Business or Profession

- 40.1 Forms of Doing Business

- 40.2 Reporting Self-Employed Income

- 40.3 Accounting Methods for Reporting Business Income

- 40.4 Tax Reporting Year for Self-Employed

- 40.5 Reporting Certain Payments and Receipts to the IRS

- 40.6 Filing Schedule C

- 40.7 Deductions for Professionals

- 40.8 Nondeductible Expense Items

- 40.9 How Authors and Artists May Write Off Expenses

- 40.10 Deducting Expenses of a Sideline Business or Hobby

- 40.11 Deducting Expenses of Looking for a New Business

- 40.12 Home Office Deduction

- 40.13 What Home Office Expenses Are Deductible?

- 40.14 Allocating Expenses to Business Use

- 40.15 Business Income May Limit Home Office Deductions

- 40.16 Home Office for Sideline Business

- 40.17 Depreciation of Office in Cooperative Apartment

- 40.18 Net Operating Losses (NOLs)

- 40.19 Your Net Operating Loss

- 40.20 How To Report a Net Operating Loss

- 40.21 How To Carry Back Your Net Operating Loss

- 40.22 Election To Carry Forward Losses

- 40.23 Overview of the Domestic Production Activities Deduction

- 40.24 Qualified Production Activities

- 40.25 Figuring the Deduction

- 40.26 Business Credits

- 40.27 Filing Schedule F

- 40.28 Farming Expenses

- Chapter 41: Retirement and Medical Plans for Self-Employed

- 41.1 Overview of Retirement and Medical Plans

- 41.2 Choosing a Keogh Plan

- 41.3 Choosing a SEP

- 41.4 Deductible Keogh or SEP Contributions

- 41.5 How To Claim the Keogh or SEP Deduction

- 41.6 How To Qualify a Keogh Plan or SEP Plan

- 41.7 Annual Keogh Plan Return

- 41.8 How Keogh Plan Distributions Are Taxed

- 41.9 SIMPLE IRA Plans

- 41.10 Health Savings Account (HSA) Basics

- 41.11 Limits on Deductible HSA Contributions

- 41.12 Distributions From HSAs

- 41.13 Archer MSAs

- 41.14 Small Business Health Tax Credit

- Chapter 42: Claiming Depreciation Deductions

- 42.1 What Property May Be Depreciated?

- 42.2 Claiming Depreciation on Your Tax Return

- 42.3 First-Year Expensing Deduction

- 42.4 MACRS Recovery Periods

- 42.5 MACRS Rates

- 42.6 Half-Year Convention for MACRS

- 42.7 Last Quarter Placements—Mid-Quarter Convention

- 42.8 150% Rate Election

- 42.9 Straight-Line Depreciation

- 42.10 Computers and Other Listed Property

- 42.11 Assets in Service Before 1987

- 42.12 MACRS for Real Estate Placed in Service After 1986

- 42.13 Demolishing a Building

- 42.14 Leasehold Improvements

- 42.15 Depreciating Real Estate Placed in Service After 1980 and Before 1987

- 42.16 When MACRS Is Not Allowed

- 42.17 Amortizing Goodwill and Other Intangibles (Section 197)

- 42.18 Deducting the Cost of Computer Software

- 42.19 Amortizing Song Rights

- 42.20 Bonus Depreciation

- Chapter 43: Deducting Car and Truck Expenses

- 43.1 Standard Mileage Rate

- 43.2 Expense Allocations

- 43.3 Depreciation Restrictions on Cars, Trucks, and Vans

- 43.4 Annual Ceilings on Depreciation

- 43.5 MACRS Rates for Cars, Trucks, and Vans

- 43.6 Straight-Line Method

- 43.7 Depreciation for Year Vehicle Is Disposed Of

- 43.8 Depreciation After Recovery Period Ends

- 43.9 Trade-in of Business Vehicle

- 43.10 Recapture of Deductions on Business Car, Truck, or Van

- 43.11 Keeping Records of Business Use

- 43.12 Leased Business Vehicles: Deductions and Income

- Chapter 44: Sales of Business Property

- 44.1 Depreciation Recaptured as Ordinary Income on Sale of Personal Property

- 44.2 Depreciation Recaptured as Ordinary Income on Sale of Real Estate

- 44.3 Recapture of First-Year Expensing

- 44.4 Gifts and Inheritances of Depreciable Property

- 44.5 Involuntary Conversions and Tax-Free Exchanges

- 44.6 Installment Sale of Depreciable Property

- 44.7 Sale of a Proprietorship

- 44.8 Property Used in a Business (Section 1231 Assets)

- 44.9 Sale of Property Used for Business and Personal Purposes

- 44.10 Should You Trade in Business Equipment?

- 44.11 Corporate Liquidation

- Chapter 45: Figuring Self-Employment Tax

- Chapter 40: Income or Loss From Your Business or Profession

- Part 7: Filing Your Return and What Happens After You File

- Chapter 46: Filing Your Return

- Chapter 47: Filing Refund Claims, and Amended Returns

- Chapter 48: If the IRS Examines Your Return

- 48.1 Odds of Being Audited

- 48.2 When the IRS Can Assess Additional Taxes

- 48.3 Audit Overview

- 48.4 Preparing for the Audit

- 48.5 Handling the Audit

- 48.6 Tax Penalties for Inaccurate Returns

- 48.7 Penalties for Not Reporting Foreign Financial Accounts

- 48.8 Agreeing to the Audit Changes

- 48.9 Disputing the Audit Changes

- 48.10 Offer in Compromise

- 48.11 Recovering Costs of a Tax Dispute

- 48.12 Suing the IRS for Unauthorized Collection

- Glossary

- Index

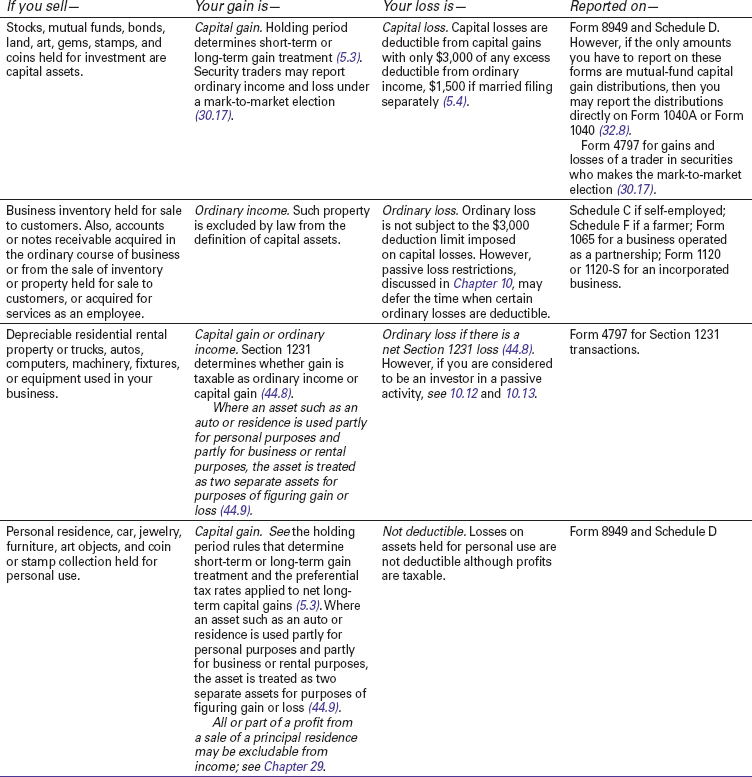

5.1 General Tax Rules for Property Sales

1. Property is classified according to its nature and your purpose for holding it; see 5.2, Table 5-1, and holding period rules at 5.3 and 5.9–5.12.

Table 5-1 Capital or Ordinary Gains and Losses From Sales and Exchanges of Property

2. Sales of capital assets must generally be reported on Form 8949, with Part I used for short-term gains and losses and Part II for long-term gains and losses (5.3). You must indicate on Form 8949 if you received a Form 1099-B from a broker showing your basis in securities sold. You may need to file multiple Forms 8949 depending on how basis was reported on Form 1099-B. Total amounts for sales price and basis are transferred from Form 8949 to Schedule D of Form 1040. On Schedule D you net short-term and long-term transactions to figure your net gain or loss for the year and, if you have net long-term gain, you are directed to the appropriate IRS worksheet for computing your tax liability taking into account the favorable capital gain rates, as discussed in the next paragraph. Filing Form 8949 or Schedule D may not be necessary if your only capital gains are from a mutual fund or REIT (32.8).

3. If you sell property at a gain, the applicable tax rate depends on the classification of the property (see Table 5-1) and, in the case of capital assets, the period you held the property before sale. A capital gain is long term if you held the asset for more than one year, short-term if you held it for one year or less. Short-term capital gains that are not offset by short- or long-term losses are subject to regular income tax rates.

If you have net capital gain for the year (net long-term gain over net short-term loss if any), your gains are subject to favorable capital gain rates. Depending on your taxable income and the amount and source of your long-term gains, gains for 2012 may be completely tax free under the 0% rate or subject to a maximum rate of 15%, 25%, or 28% where that maximum rate is less than the otherwise applicable regular tax rate (5.3).

If you do not have 28% rate gains or unrecaptured Section 1250 gains subject to a maximum 25% rate, you compute your 2012 tax liability taking into account the 0% and 15% capital gain rates on the Qualified Dividends and Capital Gain Tax Worksheet in the Form 1040 instructions. If you have either 28% gain or unrecaptured Section 1250 gain, use the Schedule D Tax Worksheet in the Schedule D instructions to compute your tax liability.

4. Loss deductions are allowed on the sale of investment and business property but not personal assets; see Table 5-1. Capital loss deductions in excess of capital gains are limited to $3,000 annually, $1,500 if married filing separately; see the details on the capital loss limitations later in this Chapter (5.4 − 5.5).

- - - - - - - - - -

Loss on Personal-Use Assets

You may not deduct a capital loss on the sale of property held for personal use, such as a car or vacation home. The loss is not deductible.

Losses on the sale of property held for investment, such as stock or mutual-fund shares, are fully deductible against capital gains but any excess loss is subject to the $3,000 limit (5.4).

- - - - - - - - - -

-

No Comment

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.