7.1 Retirement Distributions on Form 1099-R

On Form 1099-R, payments from pensions, annuities, IRAs, Roth IRAs, SIMPLE IRAs, insurance contracts, profit-sharing, and other qualified corporate and self-employed plans are reported to you and the IRS. Social Security benefits are reported on Form SSA-1099; see Chapter 34 for the special rules to apply in determining the taxable portion of Social Security benefits.

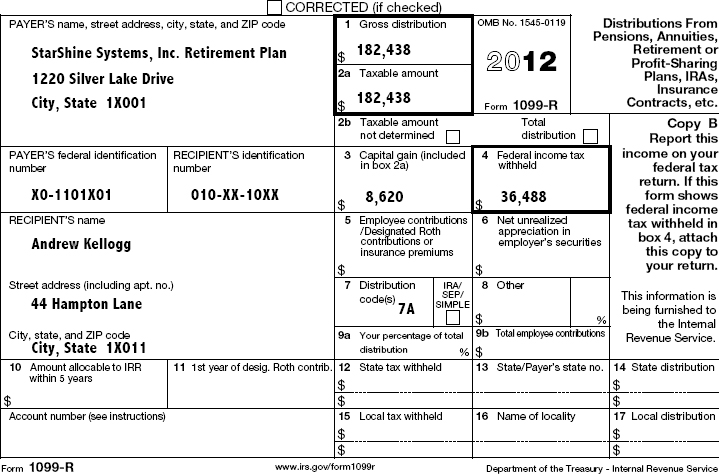

Here is a guide to the information reported on Form 1099-R. A sample form is on the next page.

Box 1.

The total amount received from the payer is shown here without taking any withholdings into account. If you file Form 1040, report the Box 1 total on Line 15a if the payment is from an IRA, or on Line 16a if from a pension or an annuity. However, if the amount is a qualifying lump-sum distribution for which you are claiming averaging, use Form 4972 (7.4).

If you file Form 1040A, report the Box 1 total on Line 11a if from an IRA or on Line 12a if from a pension or an annuity.

If an exchange of insurance contracts was made, the value of the contract will be shown in Box 1, but if the exchange qualified as tax free, a zero taxable amount will be shown in Box 2a and Code 6 will be entered in Box 7.

Boxes 2a and 2b.

The taxable portion of distributions from employer plans and insurance contracts may be shown in Box 2a. The taxable portion does not include your after-tax contributions to an employer plan or insurance premium payments.

If the payer cannot figure the taxable portion, the first box in 2b should be checked; Box 2a should be blank. You will then have to figure the taxable amount yourself. A 2012 payment from a pension or an annuity is only partially taxed if you contributed to the cost and you did not recover your entire cost investment before 2012. See the discussion of commercial annuities (7.23) or employee annuities (7.27) for details on computing the taxable portion if you have an unrecovered investment.

The payer of a traditional IRA distribution will probably not compute the taxable portion, and in this case, the total distribution from Box 1 will be entered as the taxable portion in Box 2a. This amount is fully taxable unless you have made nondeductible contributions, in which case Form 8606 is used to figure the taxable portion of the distribution (8.9). Form 8606 is also used to figure the taxable part, if any, of a Roth IRA distribution (8.23).

If the payment is from an employer plan and the “total distribution” box has been checked in 2b, see the discussion of possible rollover options (7.2, 7.7). If you were born on or before January 1, 1936,10-year averaging is available for a lump sum (7.2). The taxable amount in Box 2a should not include net unrealized appreciation (NUA (7.10)) in any employer securities included in the lump sum or the value of an annuity contract included in the distribution.

Box 3.

If the payment is a lump-sum distribution, you were born before January 2, 1936, and you participated in the plan before 1974, the amount shown here may be treated as capital gain (7.5).

Box 4.

Any federal income tax withheld is shown here. Do not forget to include it on Line 62 of Form 1040 or Line 36 of Form 1040A. If Box 4 shows any withholdings, attach Copy B of Form 1099-R to your return.

Box 5.

If you made after-tax contributions to your employer’s plan, or paid premiums for a commercial annuity or insurance contract, your contribution is shown here, less any such contributions previously distributed. IRA or SEP contributions (see Chapter 8) are not shown here.

Box 6.

If you received a qualifying lump-sum distribution that includes securities of your employer’s company, the total net unrealized appreciation (NUA) is shown here. Unless you elect to pay tax on it currently (7.10), this amount is not taxed until you sell the securities. If you did not receive a qualifying lump sum, the amount shown here is the net unrealized appreciation attributable to your after-tax employee contributions, which are also not taxed until you sell the securities (7.10).

Box 7.

In Box 7, the payer will indicate if the distribution is from a traditional IRA, SEP, or SIMPLE and enter codes that are used by the IRS to check whether you have reported the distribution correctly, including the penalty for distributions before age 59½.

Code 2 will be entered in Box 7 if you are under age 59½ and the payer knows that you qualify for an exception to the 10% early distribution penalty (7.15), such as the exception for separation of service after age 55 for an employer-plan distribution or for a distribution that is part of a series of substantially equal payments. Code 3 will be used if the disability exception applies. Code 4 is the exception for distributions paid to beneficiaries. If Code 1 is entered, this indicates that you were under age 59½ at the time of the distribution and, as far as the payer knows, no penalty exception applies. However, although Code 1 is entered, you may not be subject to a penalty. For example, you may qualify for the medical expense exception (7.15) or you may have made a tax-free rollover instead of having your employer make a direct rollover (7.7).

If the employer made a direct rollover, Code G will be entered, except Code H is used for a direct rollover from a designated Roth account to a Roth IRA.

If you are at least age 59½, Code 7 should be entered.

If you are the beneficiary of a deceased employee, Code 4 should be entered. The 10% early distribution penalty does not apply.

If you contribute to a 401(k) plan and are a highly compensated employee, your employer may have to make a corrective distribution to you of contributions (and allocable income) that exceed allowable nondiscrimination ceilings. In this case, the employer will enter Code 8 if the corrective distribution is taxable in 2012, Code P if taxable in 2011.

If you receive a lump-sum distribution that qualifies for special averaging, Code A will be entered. See the sample Form 1099-R below and the discussion of the special averaging rules (7.4).

Box 8.

If the value of an annuity contract was included as part of a lump sum you received, the value of the contract is shown here. It is not taxable when you receive it and should not be included in Boxes 1 and 2a. For purposes of computing averaging on Form 4972, this amount is added to the ordinary income portion of the distribution (7.4).

Box 9.

If several beneficiaries are receiving payment from an employer plan total distribution, the amount shown in Box 9a is your share of the distribution. Box 9b may show your after-tax contributions to your employer’s plan

Box 10.

A distribution from a designated Roth account allocable to an in-plan Roth rollover is reported here.

Boxes 12–15.

The payer may make entries in these boxes to show state or local income tax withholdings.

See the Andrew Kellogg Example (7.4)