39.9 Estate Tax for 2012

The estate tax is figured by the executor on Form 706 (United States Estate (and Generation-Skipping Transfer) Tax Return). An executor must file Form 706 for the estate of an individual dying in 2012 if the gross estate, plus adjusted taxable gifts made after 1976, is more than $5,120,000, the basic estate tax exemption for 2012. A timely Form 706 also must be filed, regardless of the size of the decedent’s gross estate, if the executor wants to make the portability election (see below) to permit the decedent’s surviving spouse to use the decedent’s unused exclusion amount. Form 706 must be filed within nine months after the date of death; an automatic six-month filing extension can be obtained by filing Form 4768.

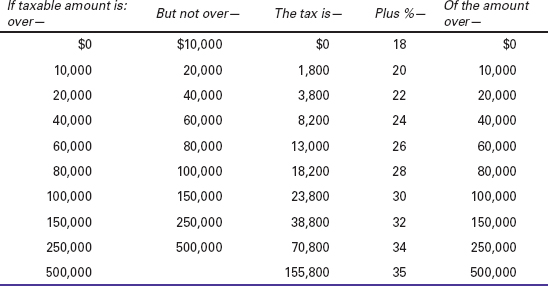

The estate tax rates from Table 39-1 are applied to the taxable estate (gross estate minus allowable deductions as figured on the schedules of Form 706). If taxable gifts (over the annual gift tax exclusion) were made after 1976, the gifts are added to the taxable estate and the tax is figured on the total. The tentative tax from the rate table is reduced by the gift taxes paid or payable on the post-1976 gifts (refigured as required by the Form 706 instructions).

The resulting gross estate tax is then reduced by the applicable credit. The credit equals the tax on the exemption amount. The basic exemption for 2012 is $5,120,000, so the 2012 applicable credit is $1,772,800, the tax on a taxable estate of $5,120,000. The exemption is increased above $5,120,000 if the decedent is the surviving spouse of a predeceased spouse who died after 2010 and the executor of the earlier estate made the portability election on Form 706. If the 2012 exemption is increased by the portability election, the applicable credit is also increased, so that it equals the tax on the increased exemption amount.

If there is any estate tax due on Form 706 after subtracting the applicable credit (and any other available credits), the balance must be paid within nine months after the date of death, but if it is impossible or impractical to meet the deadline, a request for a payment extension may be made on Form 4768; a detailed explanation must be attached to justify the request.

Uncertainty for years after 2012. When this book went to press, it was unclear what the exemption and credit for gift and estate taxes would be in 2013. As noted in the Law Alert in this section, legislation is needed to prevent a substantial drop in the exemption and the equivalent credit.

Portability election.

The estate of a married individual dying in 2012 can make a special exemption portability election to benefit a surviving spouse. The election allows any estate tax/gift tax exemption that was unused by the deceased spouse to be left to the surviving spouse. The estate of a married person who died in 2011 could also make the election by timely filing Form 706.

The estate of a 2012 decedent makes the portability election on Part 6 of Form 706. Actually, an affirmative election is not required. The election is made by completing and timely filing the Form 706, including Sections B and C of Part 6. In Section C of Part 6, the estate computes the unused exemption that is being transferred to the surviving spouse. The Form 706 must be timely filed to make the election, even if the assets of the estate are below the filing threshold of $5.12 million for 2012. If the estate is below the filing threshold, the executor may estimate the value of the gross estate on Form 706 based on a good faith determination; see the Form 706 instructions. If an estate below the filing threshold does not file Form 706, this is treated as opting out of the election.

If the estate of a decedent with a surviving spouse is required to file Form 706 and does not want to elect portability, a box may be checked in Section A of Part 6 to opt out.

Caution: The 2010 law authorizing portability allowed the election to be made only by estates of individuals dying in 2011 or 2012, and the unused exemption could be used by the surviving spouse only for 2012 gifts or by the estate of the surviving spouse only if he or she also died before 2013. However, Congress is expected to extend the portability rules beyond 2012, along with the other estate tax rules that otherwise would expire at the end of 2012 (the $5.12 million exemption, and maximum tax rate of 35%). See the e-Supplement at jklasser.com for legislation developments.

Table 39-1 Unified Estate and Gift Tax Schedule for 2012