43.5 MACRS Rates for Cars, Trucks, and Vans

Business autos, trucks, and vans are technically in a five-year MACRS class (42.4), but because of the half-year or mid-quarter convention and the annual deduction ceilings (43.3), the minimum depreciation period is six years.

Accelerated MACRS rate allowed only if business use in the first year exceeds 50%.

To use accelerated MACRS rates, you must meet the more-than-50%-business-use test (43.3) in the year the vehicle is placed in business service. Generally, the accelerated MACRS rate is based on the 200% declining balance method, but as shown on Table 43-4 (half-year convention) or Table 43-5 (mid-quarter convention), a 150% declining balance rate may be elected, which may be advantageous when you are subject to the alternative minimum tax (23.2).

Table 43-4 MACRS Deduction: Half-Year Convention

| Year— | 200% Rate | 150% Rate |

| 1 | 20.00% | 15.00% |

| 2 | 32.00 | 25.50 |

| 3 | 19.20 | 17.85 |

| 4 | 11.52 | 16.66 |

| 5 | 11.52 | 16.66 |

| 6 | 5.76 | 8.33 |

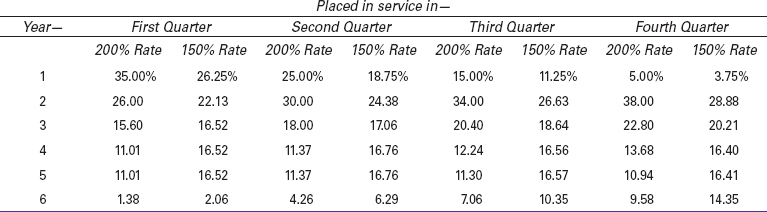

Table 43-5 MACRS Deduction: Mid-Quarter Convention

For a vehicle purchased new in 2012 and used over 50% for business, the first-year deduction ceiling is increased by a bonus of $8,000 (reduced for personal use); see 43.4, Tables 43-2 and 43-3.

If you do not meet the more-than-50%-business-use test in the year the vehicle is placed in service, you must compute your depreciation deductions using the straight-line rates shown in 43.6, subject to the annual limit; see 43.4 and Table 43-2 or Table 43-3.

Deductions for later years in the recovery period.

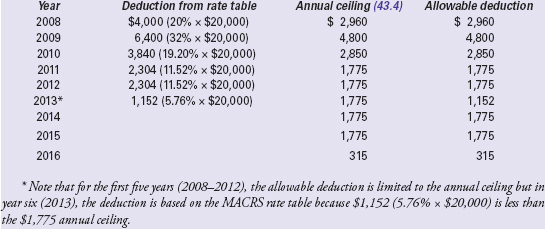

For years two through six of the recovery period, the MACRS rate from Table 43-4 or Table 43-5 is used unless business use for a year falls to 50% or less (43.10). However, the deduction figured under the MACRS table is allowed only if it does not exceed the annual depreciation ceiling (43.4) shown in Table 43-2 or Table 43-3; see the Bill Johnston Example on page 696. See below for details on using the MACRS tables.

Caution If you used the 100% bonus depreciation rule for vehicles placed in service after September 8, 2010 and before 2012 to increase your first-year depreciation deduction, you must use an IRS safe harbor to figure your deductions starting in the second recovery year, as explained in IRS Publication 463 and Revenue Procedure 2011-26. Without the safe harbor, no depreciation deductions at all would be allowed for years two through six of the recovery period, as the remaining basis in excess of the first-year limit ($11,060 for a 2011 car or $11,260 for a truck/van) would be treated as unrecovered basis that could only be deducted starting in year seven.

Deduction for year of disposition.

If you dispose of your vehicle before the end of the six-year MACRS recovery period, a partial-year deduction is allowed for the year of disposition under the half-year or mid-quarter convention (43.7).

Use of vehicle after end of recovery period.

If you continue to use the vehicle for business after the end of the recovery period, and the annual deduction ceilings prevented you from deducting your full unadjusted basis during the recovery period, you generally may deduct depreciation in the succeeding years up to the annual ceiling (43.8).

Business use falls to 50% or less after the first year.

What if business use exceeds 50% in the year the vehicle is placed in service but in a later year within the recovery period business use drops to 50% or lower? In that case, the right to use accelerated MACRS (200% or 150% declining balance method) terminates. You must use the straight-line method and recapture the benefit of the accelerated deductions claimed for the prior years (43.10).

Straight-line election for vehicle if business use exceeds 50%.

If business use of your vehicle exceeds 50%, you may elect to write off your cost under the straight-line method (43.6) instead of using the regular MACRS 200% declining balance method. The straight-line deduction is limited by the annual ceilings shownin Tables 43-2 and 43-3. By electing straight-line depreciation, you avoid the recapture of excess MACRS deductions if business use drops to 50% or less in a later year (43.10). If the election is made, you must also use the straight-line method for all other five-year property placed in service during the same year as the vehicle.

Electing 150% declining balance method.

Depreciation rates under the half-year and mid-quarter conventions are generally based on the 200% declining balance method. You may instead make an irrevocable election to apply the 150% declining balance method. The 150% method may be advantageous when you are subject to the alternative minimum tax. For alternative minimum tax (AMT) purposes (23.2), vehicle depreciation is based on the 150% declining balance method unless you use the straight-line method for regular tax purposes. If you are subject to AMT and use the 150% declining balance method instead of the 200% declining balance method for regular tax purposes, you do not have to report an AMT adjustment on Form 6251.

An election to use the 150% declining balance method is irrevocable and must be applied to all depreciable assets placed in service in the same year, except for nonresidential real and residential rental property.

MACRS Tables Applying the Half-Year Convention or Mid-Quarter Convention if Business Use Exceeds 50%

For the year you place the vehicle in service and the year (within the recovery period) you dispose of the property, you may not claim a full year’s worth of depreciation. The deduction is limited by either the half-year convention or the mid-quarter convention, depending on the month in which the vehicle was placed in service and the other business assets, if any, placed in service during that year.

The applicable convention determines the rate table you will use to figure your depreciation deduction for the entire six-year recovery period, assuming that your business use each year exceeds 50%. The half-year and mid-quarter convention rates shown in Table 43-4 or Table 43-5 reflect the 200% or 150% declining balance method, with a switch to the straight-line method when that method provides a larger deduction; the switch to straight line is built into the tables.

Rate applied to unadjusted basis.

For each year in the recovery period, the rate from MACRS Table 43-4 or Table 43-5 is applied against the business use percentage of your unadjusted basis for the vehicle. The deduction figured using the table rate may be claimed to the extent that it does not exceed the annual depreciation ceiling (43.4); see the Bill Johnston Example on the next page. Investment use may be added to the business use percentage, but keep in mind that the MACRS table may be used only if business use by itself exceeds 50% (43.3).

Unadjusted basis is your cost minus any first-year expensing deduction as well as any special first-year bonus depreciation (for a vehicle placed into service after September 10, 2001, and before January 1, 2005, and during 2008 through 2011). The basis reduction for bonus depreciation applies if you were eligible for the special allowance (vehicle purchased new and used over 50% for business) even if you did not claim it, unless on your return you “elected out” of the special allowance for the vehicle and all other five-year property placed in service during the same year.

Note: If you used 100% bonus depreciation for a vehicle placed in service after September 8, 2010 and before 2012, you must use an IRS safe harbor to claim any deduction for years two through six; see the Caution on page 694.

Basis for vehicle converted from personal to business use.

The basis for depreciation is the lower of the market value of the vehicle at the time of conversion or its adjusted basis, which is your original cost plus any substantial improvements and minus any deductible casualty losses or diesel fuel tax credit claimed for the vehicle. In most cases, the value of the vehicle will be lower than adjusted basis, and thus the value will be your depreciable basis. For a vehicle converted to business use in 2012, the MACRS rate is applied to basis allocated to business travel. Unless you have mileage records for the entire year, you should base your business-use percentage on driving after the conversion. For example, in April 2012, you started to use your car for business and in the last nine months of the year you drove 10,000 miles, 8,000 of which were for business. This business percentage of 80% is multiplied by the fraction 9/12 (months used for business divided by 12) to give you a business-use percentage for the year of 60% (9/12 of 80%).

Deter mining whether the half-year convention or mid-quarter convention applies.

If you bought a vehicle for use in your business in 2012, and it was the only business equipment placed in service during the year, then the half-year convention applies, unless you bought the vehicle in the last quarter of 2012 (October, November, or December). Under the half-year convention, the vehicle is treated as if it were placed in service in the middle of the year. Use the table below to determine your deduction under the half-year convention.

If the only business equipment bought in 2012 was a vehicle bought in the last quarter (October, November, or December), the mid-quarter convention applies. Under the table for mid-quarter convention rates on page 697, a 5% rate applies for fourth-quarter property under the 200% declining balance method, subject to the deduction ceiling in 2012 (43.4).

If you bought other business equipment in addition to the vehicle, you must consider the total cost basis of property placed in service during the last quarter of 2012. If the total bases of such acquisitions (other than realty) exceed 40% of the total bases of all property placed in service during the year, then a mid-quarter rate applies to all of the property (other than realty). The mid-quarter rate for each asset then depends on the quarter the asset was placed in service. If the 40% test is not met, then the half-year convention applies to all the property acquisitions. As shown in the mid-quarter convention table (Table 43-5), mid-quarter rates for each year of the recovery period depend on the quarter the property is placed in service.

Deduction from table cannot exceed annual ceiling.

If the deduction figured under the half-year or mid-quarter convention MACRS table (Table 43-4 or 43-5) exceeds the annual deduction ceiling (Table 43-2 or 43-3), your deduction is limited to the annual ceiling, reduced by the percentage of your personal use. Keep in mind that if you were eligible for the special first-year depreciation allowance (bonus depreciation) for a vehicle placed in service after September 10, 2001, and before January 1, 2005 and during 2008 through 2012, basis for MACRS purposes is reduced by the special allowance unless you elected on your return not to claim it. Also, if you used bonus depreciation for a vehicle placed in service after September 8, 2010 and before 2012, you cannot claim any deduction in years two through six unless you use an IRS safe harbor; see the Caution on page 694.