5.17 Basis of Property You Inherited or Received as a Gift

Special basis rules apply to property you received as a gift or that you inherited. Gifts from a spouse are subject to the rules discussed in 6.7. If you are a surviving joint tenant who received full title to property upon the death of the other joint tenant, see 5.18.

Basis of Property Received as Gift

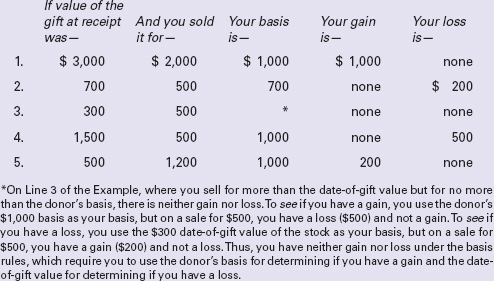

If the fair market value of the property equalled or exceeded the donor’s adjusted basis (5.20) at the time you received the gift, your basis for figuring gain or loss when you sell it is the donor’s adjusted basis plus all or part of any gift tax paid; see the gift tax rule below. Additional basis adjustments may be required for the period you held the property (5.20).

If on the date of the gift the fair market value was less than the donor’s adjusted basis, your basis for purposes of figuring gain is the donor’s adjusted basis, and your basis for figuring loss is the fair market value on the date of the gift. Additional basis adjustments may be required for the period you held the property (5.20).

Did the donor pay gift tax?

If the donor paid a gift tax (39.2) on the gift to you, your basis for the property is increased under these rules:

Depreciation on property received as a gift.

If the property is depreciable (Chapter 42), your basis for computing depreciation deductions is the donor’s adjusted basis (5.20), plus all or part of the gift tax paid by the donors as previously discussed.

To figure gain or loss when you sell the property, you must adjust basis for depreciation you claimed and make other adjustments required for the period you hold the property (5.20). If accelerated depreciation is claimed and you sell at a gain, you are subject to the ordinary income recapture rules (44.1).

Basis of Inherited Property

Your basis for property inherited from someone who died before or after 2010 is generally “stepped up” to the fair market value of the property on the date of the decedent’s death. This is also generally the rule if the decedent died in 2010, but see below for the exception where the executor filed Form 8939. If the executor of the decedent’s estate elected to use an alternate valuation date (within six months after the date of death), your basis is the fair market value on the alternate valuation date. Where basis for inherited property is the value at the decedent’s death or alternate valuation date, income tax is completely avoided on the appreciation in value that occurred while the decedent owned the property.

If you owned the property jointly with the deceased, see 5.18.

If you inherit appreciated property that you (or your spouse) gave to the deceased person within one year of his or her death, your basis is the decedent’s basis immediately before death, not its fair market value.

If the inherited property is subject to a mortgage, your basis is the value of the property, and not its equity at the date of death. If the property is subject to a lease under which no income is to be received for years, the basis is the value of the property—not the equity.

You might be given the right to buy the deceased person’s property under his or her will. This is not the same as inheriting that property. Your basis is what you pay—not what the property is worth on the date of the deceased’s death.

If property was inherited from an individual who died after 1976 and before November 7, 1978, and the executor elected to apply a carryover basis to all estate property, your basis is figured with reference to the decedent’s basis. The executor must inform you of the basis of such property.

Community property.

Upon the death of a spouse in a community property state, one-half of the fair market value of the community property is generally included in the deceased spouse’s estate for estate tax purposes. The surviving spouse’s basis for his or her half of the property is 50% of the total fair market value. For the other half, the surviving spouse, if he/she receives the asset, or the other heirs of the deceased spouse have a basis equal to 50% of the fair market value.

Did executor of decedent who died in 2010 elect modified carryover basis rules on Form 8939?

If you inherited property from a person who died in 2010, you get a full stepped-up basis (to fair market value on date of death or alternate valuation date), provided the executor did not elect to file Form 8939. Under the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010, the executors of estates of individuals dying in 2010 were allowed to opt out of estate tax entirely (no estate tax at all applied even if the gross estate exceeded the $5 million exemption) provided an election was made on Form 8939 to apply modified carryover basis rules under which the heirs generally received a stepped-up basis only for the first $1.3 million in assets, plus an additional $3 million for property passing to a surviving spouse. Executors had to make the modified carryover basis election on Form 8939 by January 17, 2012.

If the executor of a 2010 estate did not elect on Form 8939 to apply the modified carryover basis rules, the regular stepped-up basis rules apply.