29.4 Reduced Maximum Exclusion

Generally, no exclusion is allowed on a sale of a principal residence if you owned or used the home for less than two of the five years preceding the sale (29.2). Similarly, an exclusion is generally disallowed if within the two-year period ending on the date of sale, you sold another home at a gain that was wholly or partially excluded from your income.

However, even if a sale of a principal residence is made before meeting the ownership and use tests or it is within two years of a prior sale for which an exclusion was claimed, an exclusion is available if the primary reason for the sale is: (1) a change in the place of employment, (2) health, or (3) unforeseen circumstances. If the sale is for one of these qualifying reasons, you are entitled to a prorated portion of the regular $250,000 or $500,000 exclusion limit. The employment change, health problem, or unforeseen circumstance can be attributable to you or another “qualified individual,” as defined below.

You automatically qualify for the reduced exclusion if your sale is within a safe harbor established by the IRS. If a safe harbor is not available, you may qualify by showing that the “facts and circumstances” of your situation establish that the primary reason for the sale was a change in the place of employment, health problem or unforeseen circumstances.

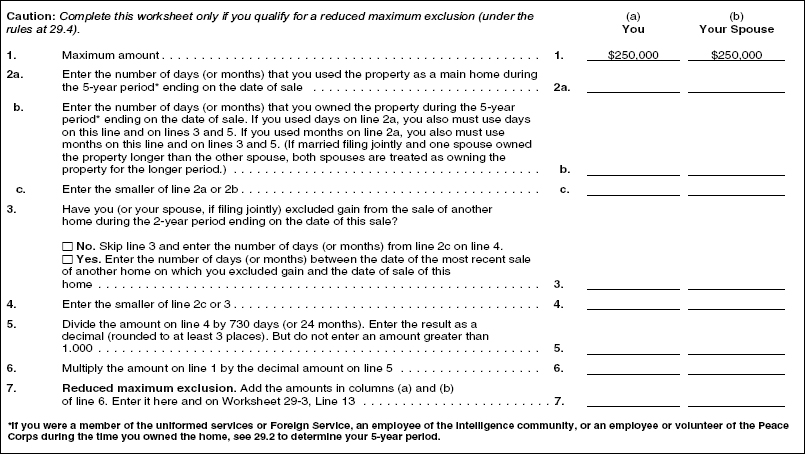

When you fall within a safe harbor or meet the primary reason test, you are allowed an allocable percentage of the regular $250,000 or $500,000 exclusion limit, depending on how much of the regular two-year ownership and use test was satisfied, or the time between this sale and a sale within the prior two years. For example, if you owned and lived in your home for 438 days before selling it to take a new job, you are entitled to 60% of the regular exclusion limit, which is based on 730 qualifying days (438/730 = 60%). Use Worksheet 29-1 to figure your reduced exclusion limit. Although the maximum exclusion is reduced, this may not disadvantage you. If the reduced exclusion limit equals or exceeds your gain, none of your gain is subject to tax.

Qualified individual.

In addition to yourself, the following persons are considered qualified individuals for purposes of qualifying for the reduced maximum exclusion: your spouse, a co-owner of the residence, or any person whose main home was your principal residence.

For purposes of the “health reasons” category, qualified individuals include not only the above individuals but also their family members: parents or step-parents, grandparents, children, stepchildren, adopted children, grandchildren, siblings (including step- or half-siblings), in-laws (mother/father, brother/sister, son/daughter), uncles, aunts, nephews, or nieces.

Sale due to change in place of employment.

The reduced exclusion limit applies if the primary reason for your sale is a change in the location of a qualified individual’s employment; see the above definition of qualified individual. “Employment” includes working for the same employer at a different location or starting with a new employer. It also includes the commencement of self-employment or the continuation of self-employment at a new location.

The IRS provides a safe harbor based on distance. If a qualified individual’s new place of employment is at least 50 miles farther from the sold home than the old place of employment was, the reduced exclusion limit is allowed so long as the change in employment occurred while you owned and used the home as your principal residence. If an unemployed qualified person obtains employment, the safe harbor applies if the sold home is at least 50 miles from the place of employment.

If the 50-mile safe harbor cannot be met, the facts and circumstances may indicate that a change in the place of employment was the primary reason for the sale, thereby allowing the reduced exclusion limit.

Sale due to health problems.

The reduced exclusion limit applies if a principal residence is sold primarily to obtain or facilitate the diagnosis, treatment, or mitigation of a qualified person’s disease, illness or injury, or to obtain or provide medical or personal care for a qualified individual suffering from a disease, illness, or injury. A sale does not qualify if it is merely to improve general health. Note that for “health sales,” the definition of qualified individual is broadened to include family members; see above.

A physician’s recommendation of a change in residence for health reasons automatically qualifies under an IRS safe harbor.

Sale due to unforeseen circumstances.

A sale of a principal residence due to any of the following events fits within an IRS safe harbor for unforeseen circumstances and automatically qualifies for a reduced maximum exclusion:

The IRS may expand the list of safe harbors in generally applicable revenue rulings or in private rulings requested by individual taxpayers.

Sales not covered by a safe harbor can qualify if the facts and circumstances indicate that the home was sold primarily because of an event that could not have been reasonably anticipated before the residence was purchased and occupied. The IRS in private letter rulings has been quite liberal in allowing the reduced maximum exclusion for unforeseen sales. However, an improvement in financial circumstances does not qualify under IRS regulations, even if the improvement is the result of unforeseen events, such as receiving a promotion and a large salary increase that would allow the purchase of a bigger home.

Worksheet 29-1 Reduced Maximum Exclusion