41.4 Deductible Keogh or SEP Contributions

The deductible limit for a Keogh plan depends on whether you have a defined-contribution plan (profit-sharing or money-purchase pension plan) or a defined-benefit plan. A SEP is treated as a profit-sharing plan subject to the defined-contribution plan deduction limits explained below.

If you have a defined-benefit plan, you generally may deduct contributions needed to produce the accrued benefits provided for by the plan, including any unfunded current liability. This is a complicated calculation requiring actuarial computations that call for the services of a pension expert.

Deductible contribution to a defined-contribution Keogh Plan or a SEP.

Before figuring the deductible contribution you can make for 2012 to a profit-sharing Keogh or SEP account, or to a money-purchase pension plan, you must first figure your self-employment tax liability on Schedule SE and the employer equivalent portion of self-employment tax to be claimed on Line 27 of Form 1040. In computing your deductible plan contribution, your net profit from Line 31 of Schedule C, Line 3 of Schedule C-EZ, or Line 36 of Schedule F is reduced by the deduction for the employer equivalent portion of self-employment tax; see the Example below.

As a self-employed person, you are not allowed to figure the deductible contribution for yourself by applying the contribution rate stated in your plan. The rate must be reduced, as required by law, to reflect the reduction of net earnings by the deductible contribution itself. If your plan rate is a whole number, the reduced percentage is shown in the Rate Table for Self-Employed on page 664. If the plan rate is fractional, the reduced percentage is figured using the Fractional Rate Worksheet for Self-Employed on page 664.

Figuring your maximum deductible contribution.

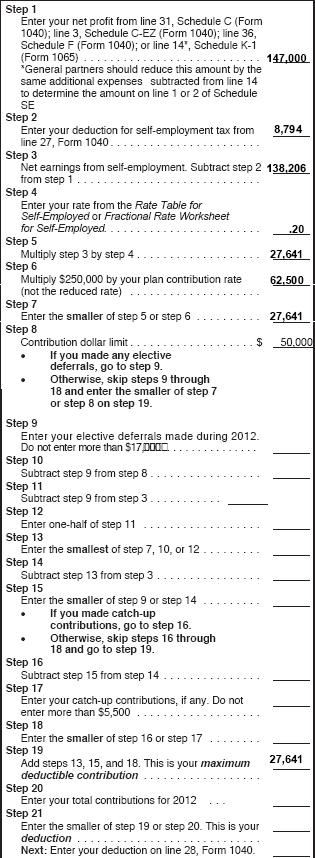

After figuring your net earnings and reducing that amount by the employer equivalent portion of your self-employment tax liability, you multiply the balance by the reduced rate from the Rate Table or Fractional Rate Worksheet for Self-Employed on page 664. This is generally your maximum deductible contribution to a profit-sharing Keogh plan or SEP. However, the maximum deductible contribution cannot exceed the annual limit on additions to a defined contribution plan. The annual limit for 2012 is the lesser of (1) $50,000, or (2) $250,000 (maximum compensation that can be taken into account) multiplied by the stated plan contribution rate, not the reduced rate. See the Deduction Worksheet for Self-Employed on the next page, which takes you through the steps of figuring your deductible contribution.

If elective deferrals were made during the year, extra steps are required to compute the maximum deductible contribution; see Step 9 of the the Deduction Worksheet for Self-Employed shown below.

Deduction Worksheet for Self-Employed

Table 41-1 Rate Table for Self-Employed

| If plan rate is— | Self-employed person’s reduced rate is— |

| 1 % | .009901 |

| 2 | .019608 |

| 3 | .029126 |

| 4 | .038462 |

| 5 | .047619 |

| 6 | .056604 |

| 7 | .065421 |

| 8 | .074074 |

| 9 | .082569 |

| 10 | .090909 |

| 11 | .099099 |

| 12 | .107143 |

| 13 | .115044 |

| 14 | .122807 |

| 15 | .130435 |

| 16 | .137931 |

| 17 | .145299 |

| 18 | .152542 |

| 19 | .159664 |

| 20 | .166667 |

| 21 | .173554 |

| 22 | .180328 |

| 23 | .186992 |

| 24 | .193548 |

| 25* | .200000* |

* The maximum deductible percentage for contributions (other than elective deferrals) to your own profit-sharing Keogh, money-purchase Keogh, or SEP is 20% and for your employees, 25%.

Fractional Rate Worksheet for Self-Employed

| If the plan rate is fractional and thus not listed in the table above, figure your deductible percentage this way: | ||

| 1. | Write the plan rate as a decimal. For example, if the plan rate is 10.5%, write .105 as the decimal amount. | _____________ |

| 2. | Add 1 to the decimal rate. For example, if the rate is .105, the result is 1.105. | _____________ |

| 3. | Divide Step 1 by Step 2. This gives you the deductible percentage. If the plan rate is .105, the deductible percentage is .0950 (.105 ÷ 1.105). | _____________ |

Contributions for your employees.

The deduction complications that apply to your own contributions do not apply to contributions for employees. You make contributions for your employees at the rate specified in your plan, based upon their compensation, subject to the annual limit discussed above. Thus, if your plan contribution rate is 25%, you would contribute 25% of your employees’ pay to the plan, even though your own contribution rate is reduced to 20% under the Rate Table for Self Employed shown above. You deduct contributions for employees when figuring your net earnings from self-employment on Schedule C or Schedule F before figuring your own deductible contribution using the steps shown in the Example above.

Contributions allowed after age 70½.

You may continue to make contributions for yourself to a Keogh plan or SEP as long as you have self-employment income. However, you must begin to receive required minimum distributions from a SEP by April 1 of the year following the year in which you reach age 70½ (8.15). This age 70½ required distribution beginning date also applies to a Keogh plan if you are a more-than-5% owner of the business (7.13).

Excess contributions.

Contributions to a plan exceeding the deduction ceiling may be carried over and deducted in later years subject to the ceiling for those years. However, if contributions exceed the deductible amount, you are generally subject to a 10% penalty on nondeductible contributions that are not returned by the end of your tax year. The penalty is computed on Form 5330, which must be filed with the IRS by the end of the seventh month following the end of the tax year.