43.4 Annual Ceilings on Depreciation

Annual ceilings limit the amount of depreciation you may deduct for passenger cars and certain light trucks and vans. The ceilings apply both to self-employed individuals and employees. As a result of the ceilings, the actual write-off period for your car may be several years longer than the minimum recovery period of six years (43.5).

Passenger cars.

The ceiling on depreciation for a car placed in service in 2012 is generally $3,160, reduced by personal use. However, bonus depreciation allows an $8,000 increase in the first-year ceiling for new vehicles used over 50% for business, to $11,160. For purposes of the annual depreciation ceilings, a car is any four-wheeled vehicle that is manufactured primarily for use on public thoroughfares and that is weight-rated by the manufacturer at 6,000 pounds or less when unloaded (without passengers or cargo). However, these vehicles are excluded from the car category and are thus exempt from the annual depreciation limits: (1) an ambulance, hearse, or combination ambulance-hearse used directly in a business, and (2) a vehicle such as a taxi cab used directly in the business of transporting persons or property for compensation or hire.

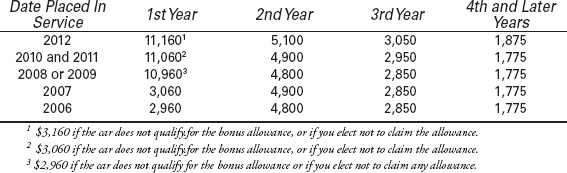

Year-by-year limits for cars placed in service in 2012 and prior years can be found in Table 43-2.

Table 43-2 Maximum Depreciation Deduction for Cars (Must Be Reduced for Personal Use)

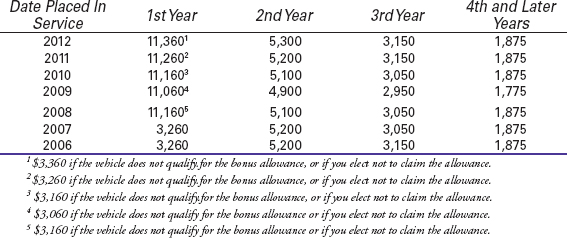

Table 43-3 Maximum Depreciation Deduction for Trucks and Vans (Must Be Reduced for Personal Use)

Light trucks, vans, and SUVs.

A light truck, van, minivan, or SUV (sport utility vehicle) built on a truck chassis that is weight-rated by the manufacturer at 6,000 pounds or less when fully loaded (gross vehicle weight rating) is generally subject to annual depreciation ceilings.

However, the depreciation limits do not apply to trucks and vans that are qualified non-personal-use vehicles. These include moving vans, flatbed trucks, and delivery trucks with seating only for the driver (or driver seat plus folding jump seat). Also included are specially modified trucks and vans that are unlikely to be used more than a minimal amount for personal purposes. An example would be a van that has been painted to display advertising or the company’s name and which has permanent shelving for carrying merchandise or equipment.

Where an exception does not apply, the deduction limits for light trucks, vans, and SUVs are slightly higher than those for cars. For trucks and vans placed in service in 2012, the 2012 limit is generally $3,360. However, bonus depreciation makes the 2012 limit for a new light truck or van used over 50% for business $11,360. The applicable limit must be reduced for personal use. Table 43-3 shows the year-by-year limits for trucks and vans.

Heavy trucks, vans, and SUVs.

Trucks, vans, and SUVs built on a truck chassis that are weight-rated by the manufacturer at more than 6,000 pounds gross vehicle weight are not subject to the annual depreciation ceilings. However, first-year expensing (42.3) for the vehicle may be limited to $25,000 rather than the general expensing limit, which for 2012 is $139,000 (42.3). The vehicle must be used more than 50% for business to qualify for first-year expensing. If first-year expensing is not or cannot be elected (42.3), a full depreciation deduction using the MACRS rate (43.5) is allowed with no dollar limit. Further, if bought new and placed in service in 2012 and used over 50% for business, 50% bonus depreciation can be used.

The $25,000 limit on first-year expensing applies to SUVs rated at more than 6,000 pounds but not more than 14,000 pounds gross vehicle weight. For purposes of the $25,000 expensing limit, an SUV means any four-wheeled vehicle primarily designed or which can be used to carry passengers over public thoroughfares. Trucks and vans as well as SUVs can be covered by this definition, but the law allows certain exceptions. Exceptions are allowed for vehicles with seating for more than nine passengers behind the driver, for pickup trucks with an interior cargo bed at least six feet long that is an open area or is enclosed by a cap and not readily accessible to passengers, and cargo vans without rear seating and with no body sections protruding more than 30 inches ahead of the windshield. For these excepted vehicles, the $25,000 limit on first-year expensing does not apply.