8.12 Penalty for Traditional IRA Withdrawals Before Age 59½

You have to pay a 10% penalty in addition to regular tax if you take a distribution from a traditional IRA before you are age 59½, unless you qualify for an exception specified in the tax law. There is no general exception for financial hardship. Although you may be forced in tough economic times to tap your IRA to cover living expenses, or you face a family emergency, you will be able to avoid the early distribution penalty only if you fit within one of the designated penalty exceptions, such as for disability, paying substantial medical expenses, or higher education expenses.

Here is the list of allowable penalty exceptions: (1) you take the distribution because you are totally disabled, (2) you pay medical expenses exceeding 7.5% of adjusted gross income, (3) you receive unemployment compensation for at least 12 consecutive weeks and pay medical insurance premiums, (4) you pay qualified higher education expenses, (5) the distribution is $10,000 or less and used for qualified first-time home-buyer expenses, (6) you receive a qualified reservist distribution, (7) the distribution is one of a series of payments being made under one of several annuity-type methods, (8) the distributions are made to you as a beneficiary of a deceased IRA owner, or (9) the distribution was due to an IRS levy on your IRA. These exceptions are further discussed below.

Also note that a qualifying rollover (8.10) of an IRA distribution is not subject to tax and therefore not subject to the 10% penalty even if you are under age 59½.

The penalty is 10% of the taxable IRA distribution. For example, if before age 59½ you withdraw $3,000 from your traditional IRA, you must include the $3,000 as part of your taxable income and, in addition, pay a $300 penalty tax. If part of a pre-59½ distribution is tax free because it is allocable to nondeductible contributions (8.9) or rolled over to another IRA (8.10), the 10% penalty applies only to the taxable portion of the distribution.

If you do not owe the penalty because you qualify for an exception, you may have to file Form 5329, depending on whether the payer of the distribution correctly marked the exception in Box 7 of Form 1099-R. If you qualify for the annuity-method exception and the payer correctly indicated that exception by marking Code 2 in Box 7, you do not have to file Form 5329. Similarly, if you are the beneficiary of a deceased IRA owner and the payer has correctly noted that with Code 4 in Box 7, you do not have to file Form 5329 to claim the exception.

If you qualify for the disability exception (see below), it is unlikely that the payer will know of that fact and thus Code 3 (for the disability exception) will probably not be marked in Box 7 of Form 1099-R. In that case, you must file Form 5329 to claim the exception. You also must file Form 5329 if the annuity method or beneficiary exception applies but it is not coded in Box 7 of Form 1099-R.

If part of your distribution is eligible for a penalty exception, you must enter the exception code on Form 5329 and figure the 10% penalty on the nonqualifying part. The penalty is entered on Form 1040 as an “Other Tax” on Line 58.

Beneficiaries.

Beneficiaries are exempt from the pre–age 59½ penalty. If the IRA owner was not your spouse and you liquidate the account and receive the proceeds, or if you receive annual payments as a beneficiary under the inherited IRA rules (8.14), any distributions you receive before age 59½ are not subject to the early distribution penalty.

If you inherit an IRA from your deceased spouse and elect to treat it as your own IRA as discussed in 8.14, you are not eligible for the beneficiary exception; distributions from the account before you reach age 59½ will be subject to the penalty unless another exception applies. The beneficiary exception applies if the account is maintained in the name of your deceased spouse and you are receiving the distribution according to the rules for a spousal beneficiary (8.14).

Disability exception.

To qualify for the disability exception, you must be able to show that you have a physical or mental condition that can be expected to last indefinitely or result in death and that prevents you from engaging in “substantial gainful activity” similar to the type of work you were doing before the condition arose.

In one case, a 53-year-old stockbroker claimed that his IRA withdrawal of over $200,000 should be exempt from the 10% penalty because he suffered from mental depression. However, the Tax Court upheld the IRS imposition of the penalty because he continued to work as a stockbroker.

Medical expense exception.

If you withdraw IRA funds in a year in which you pay substantial medical costs, part of the distribution may avoid the pre–age 59½ penalty. For example, if in 2012 you took a distribution and paid unreimbursed medical expenses that exceed 7.5% of your 2012 adjusted gross income (AGI), the penalty does not apply to the part of the distribution equal to the expenses over the 7.5% floor. The distribution must be received in the same year that the medical expenses are paid. The medical costs must be eligible for the itemized medical deduction (17.2), but the IRA penalty exception applies whether you itemize or claim the standard deduction.

Note: The 7.5% floor is scheduled to increase to 10% starting in 2013; see 17.1.

Unemployed person’s medical insurance exceptions.

There is no general penalty exception for being unemployed. However, if you are unemployed and received unemployment benefits under Federal or state law for at least 12 consecutive weeks, you may make penalty-free IRA withdrawals to the extent of medical insurance premiums paid during the year for you, your spouse, and your dependents. The withdrawals may be made in the year the 12-week unemployment test is met, or in the following year. However, the penalty exception does not apply to distributions made more than 60 days after you return to the work force.

Self-employed persons who are ineligible by law for unemployment benefits may be treated as meeting the 12-week test, and thus eligible for the exception, under regulations to be issued by the IRS.

Higher education expenses exception.

A penalty exception is allowed for IRA distributions that do not exceed higher education expenses, including graduate school costs, for you, your spouse, your or your spouse’s children, or your or your spouse’s grandchildren that you paid during the year of the IRA distribution. Eligible expenses include tuition, fees, books, supplies, and equipment that are required for enrollment or attendance, plus room and board for a person who is at least a half-time student.

The penalty exception applies only if the withdrawal from the IRA and the payment of the qualified higher education expenses occur within the same year. For example, in one case, a taxpayer under age 59½ took IRA distributions in 2001 to pay credit card debt incurred in 1999 and 2000 to pay qualified higher education expenses for those years. Another taxpayer under age 59½ took IRA distributions in 2002 and used them to pay qualified expenses incurred in 2003 and 2004. In both cases, the Tax Court agreed with the IRS that the penalty exception was not available because the IRA withdrawals were not made in the same year that the qualified higher education expenses were incurred.

First-time home-buyer expense exception.

A penalty exception is allowed for up to $10,000 of qualifying “first-time” home-buyer expenses. You are a qualifying first-time home-buyer if you did not have a present ownership interest in a principal residence in the two-year period ending on the acquisition date of the new home. If you are married, your spouse also must have had no such ownership interest within the two-year period. The penalty does not apply to IRA distributions that are used within 120 days to buy, construct, or reconstruct a principal residence for you, your spouse, child, grandchild, or ancestor of you or your spouse. Qualifying home acquisition costs include reasonable settlement, financing, or other closing costs. If you qualify, the exception applies only for $10,000 of home-buyer expenses. This is a lifetime cap per IRA owner and not an annual limit.

If you take a distribution, intending to use it for home acquisition costs that would qualify for the first-time buyer exception, but the transaction falls through, you have 120 days from the date you receive the distribution to roll it back to an IRA (8.10).

IRS levy.

The 10% penalty does not apply to an “involuntary” distribution due to an IRS levy on your IRA.

Qualified reservist distribution.

If you are a member of the reserves called to active military duty for over 179 days, or indefinitely, distributions received during the active duty period are not subject to the early distribution penalty. Furthermore, a qualified reservist distribution may be recontributed to the plan within two years after the end of your active duty period without regard to the regular limits on IRA contributions (8.2). A recontribution is not deductible.

Annuity Schedule Payments Avoid 10% Penalty

You may avoid the penalty if you are willing to receive annual distributions under one of the three IRS-approved annuity-type methods discussed in this section. Before arranging an annuity-type schedule, consider these points: all of the payments will be taxable (unless allocable to nondeductible contributions (8.9)), and if you do not continue the payments for a minimum number of years, the IRS will impose the 10% penalty for all taxable payments received before age 59½, plus interest charges. The minimum payout period rules do not apply to totally disabled individuals or to beneficiaries of deceased IRA owners.

The payments must continue for at least five years, or until you reach age 59½, whichever period is longer. Thus, if you are in your 40s, you would have to continue the scheduled payments until you are age 59½. If you are in your mid-50s, the minimum payout period is not as serious a burden, as you only need to continue the scheduled payments for at least five years, starting with the date of the first distribution, provided that the period ends after you reach age 59½.

During this minimum period, the arranged annuity-type schedule generally may not be changed unless you become disabled. For example, taking a lump-sum distribution of your account balance before the end of the minimum payout period would trigger the retroactive penalty, plus interest charges. The penalty is triggered even if the change in distribution methods is made after you reach age 59½. However, the IRS may allow a reduction in payments during the minimum period, such as where part of an IRA has been transferred to an ex-spouse following a divorce. Also, as discussed below, the IRS allows a one-time irrevocable switch from the fixed amortization method or fixed annuitization method to the required minimum distribution method. After the minimum payout period, you can discontinue the payments or change the method without penalty.

Three approved payment methods.

If you would like to take advantage of this penalty exception, you may apply one of the following three payout methods that have been approved by the IRS. With each method, you must receive at least one distribution annually. Under Method 1, the payment changes annually based on the value of the account. Under Methods 2 and 3 the annual payment is generally fixed when the payments begin, but in private rulings the IRS has approved payment schedules that from inception recalculate the amount to be withdrawn each year. Methods 2 and 3 require the assistance of a tax professional and financial advisor to plan the series of payments. The IRS allows taxpayers receiving payments under Method 2 or 3 to reduce the required annual amount without penalty by switching to Method 1.

1. Required minimum distribution method. This is the easiest method to figure but provides smaller annual payments than the other methods. Figure the annual withdrawal by dividing your account balance by your life expectancy or by the joint life and last survivor expectancy of you and your beneficiary.

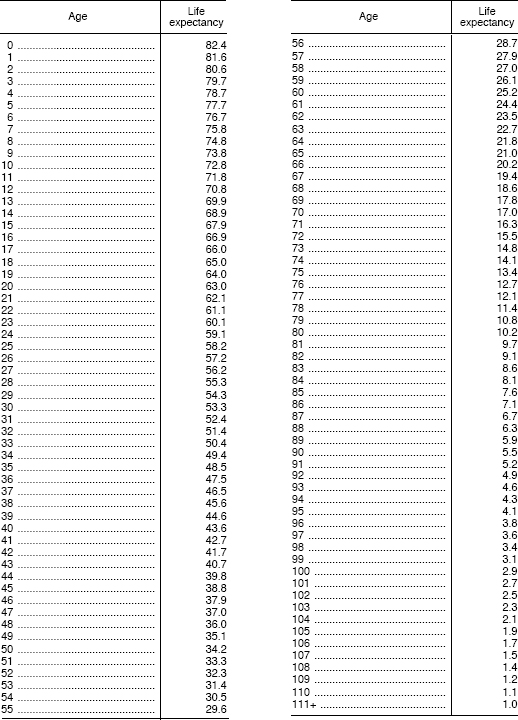

For example, assume that you are age 50 in 2013 and have an IRA of $100,000 at the beginning of the year. If you use your single life expectancy, you may take a penalty-free payment of $2,924 in 2013 ($100,000 account balance ÷ 34.2 life expectancy). Single life expectancy is shown in Table 8-5, Beneficiary’s Single-Life Expectancy Table (8.14).

Table 8-5 Beneficiary’s Single Life Expectancy Table

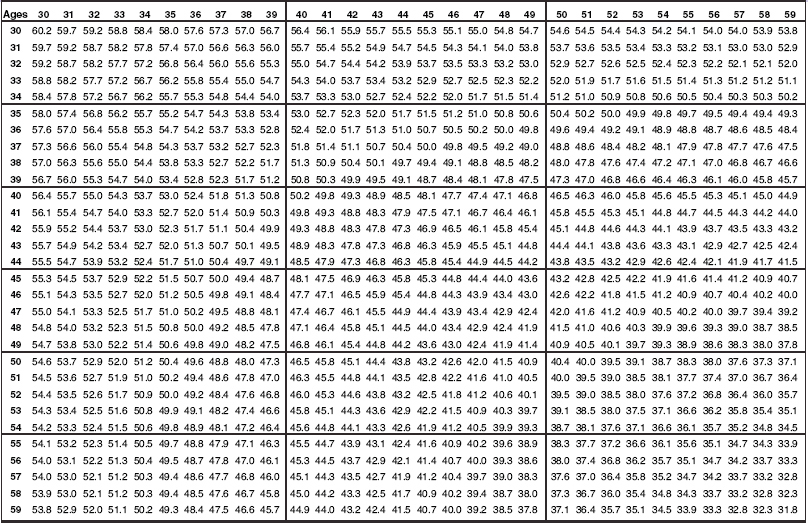

If instead of using your single life expectancy you used the joint life and last survivor expectancy of you and your beneficiary, the annual penalty-free amount would be smaller given the longer joint life expectancy. For example, if your beneficiary was age 45, your joint life and last survivor life expectancy would be 43.2 years (using ages 50 and 45), and the penalty-free withdrawal $2,315 ($100,000 account balance ÷ 43.2). See Table 8-2 for a sample section of the IRS joint life and last survivor life expectancy table. The full IRS table showing joint life and last survivor life expectancy is in IRS Publication 590 and can also be obtained from your IRA trustee.

Table 8-2 Joint Life and Last Survivor Life Expectancy (see “Required minimum distribution method” above)

2. Fixed amortization method. Under this method, you amortize your IRA account balance like a mortgage, using the same life expectancy as under Method 1 (your single life expectancy or the joint life and last survivor expectancy of you and your beneficiary). The interest rate used must be no more than 120% of the federal mid-term rate for either of the two months immediately preceding the month in which distributions begin. In private rulings, the IRS has approved proposed payment schedules that annually recalculate the payments to be received under the fixed amortization method. See Revenue Ruling 2002-62 for further details on this method.

3. Fixed annuitization method. This method is similar to the fixed amortization method, but an annuity factor from a mortality table is used. Revenue Ruling 2002-62 provides the mortality table to be used. The maximum interest rate used cannot exceed 120% of the federal mid-term rate for either of the two months immediately preceding the month in which distributions begin. In private rulings, the IRS has approved proposed payment schedules that annually recalculate the payments to be received under the fixed annuitization method.