7.23 Figuring the Taxable Part of Your Annuity

Tax treatment of a distribution depends on whether you receive it before or after the annuity starting date, and on the amount of your investment. A cash withdrawal before age 59½ from an annuity contract is generally subject to a 10% penalty, but there are exceptions; the penalty is discussed at the end of this section. If your annuity is from an employer plan, see 7.26.

The annuity starting date is either the first day of the first period for which you receive a payment or the date on which the obligation under the contract becomes fixed, whichever is later. If your right to an annuity is fixed on June 1, 2013, and your monthly payments start on December 1, 2013, for the period starting November 1, 2013, November 1, 2013 is your annuity starting date.

Payments before the annuity starting date.

If your commercial annuity contract was purchased after August 13, 1982, withdrawals before the annuity starting date are taxable to the extent that the cash value of the contract (ignoring any surrender charge), immediately before the distribution, exceeds your investment in the contract at that time. Loans under the contract or pledges are treated as cash withdrawals.

If the contract was purchased before August 14, 1982, withdrawals before the annuity starting date are taxable only to the extent they exceed your investment. Loans are tax free and are not treated as withdrawals subject to this rule. Where additional investments were made after August 13, 1982, cash withdrawals are first considered to be tax-free distributions of the investment before August 14, 1982. If the withdrawal exceeds this investment, the balance is fully taxable to the extent of earnings on the contract, with any excess withdrawals treated as a tax-free recovery of the investment made after August 13, 1982.

Payments on or after the annuity starting date.

If the withdrawal is a regular (not variable) annuity payment, the part of the annuity payment that is allocated to your cost investment is treated as a nontaxable return of the cost; the balance is taxable income earned on the investment. You may find the taxable part of your annuity payment by following the six steps listed below under “Taxable Portion of Commercial Annuity Payments.” If you have a variable annuity, the computation of the tax-free portion is discussed following Step 6.

Payments on or after the annuity starting date that are not part of the annuity, such as dividends, are generally taxable, but there are exceptions. If the contract is a life insurance or endowment contract, withdrawals of earnings are tax free to the extent of your investment, unless the contract is a modified endowment contract.

Taxable Portion of Commercial Annuity Payments

If the payer of the contract does not provide the taxable amount in Box 2a of Form 1099-R, you can compute the taxable amount of your commercial annuity using the following steps.

Step 1: Figure your investment in the annuity contract.

If you have no investment in the contract, annuity income is fully taxable; therefore, ignore Steps 2 through 6.

| If your annuity is— | Your cost is— |

| Single premium annuity contract | The single premium paid. |

| Deferred annuity contract | The total premiums paid. |

| A gift | Your donor’s cost. |

| An employee annuity | The total of your after-tax contributions to the plan plus your employer’s contributions that you were required to report as income (7.26). |

| With a refund feature | The value of the refund feature. |

From cost, you subtract the following items:

- Any premiums refunded, and rebates or dividends received on or before the annuity starting date.

- Additional premiums for double indemnity or disability benefits.

- Amounts received under the contract before the annuity starting date to the extent these amounts were not taxed; see above.

- Value of a refund feature; see below.

Value of refund feature.

Your investment in the contract is reduced by the value, if any, of the refund feature.

Your annuity has a refund feature when these three requirements are present: (1) the refund under the contract depends, even in part, on the life expectancy of at least one person; (2) the contract provides for payments to a beneficiary or the annuitant’s estate after the annuitant’s death; and (3) the payments to the estate or beneficiary are a refund of the amount paid for the annuity.

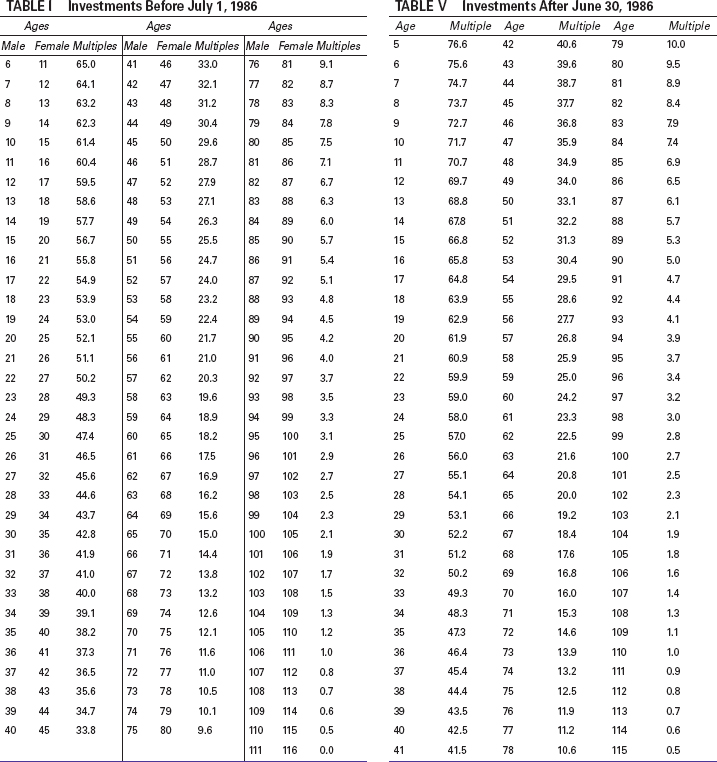

The value of the refund feature is figured by using a life expectancy multiple that may be found in Treasury Table III or Table VII, depending on the date of your investment; the tables are in IRS Publication 939.

Where an employer paid part of the cost, the refund is figured on only the part paid by the employee.

The refund feature is considered to be zero if (1) for a joint and survivor annuity, both annuitants are age 74 or younger, the payments are guaranteed for less than 2½ years, and the survivor’s annuity is at least 50% of the first annuitant’s (retiree’s) annuity or (2) for a single-life annuity without survivor benefits, the payments are guaranteed for less than 2½ years and you are age 57 or younger if using the new (unisex) annuity tables, age 42 or younger if male and using the old annuity tables, or age 47 or younger if female and using the old annuity tables.

Also subtract from cost any tax-free recovery of your investment received before the annuity starting date, as previously discussed.

Step 2: Find your expected return.

This is the total of all the payments you are to receive. If the payments are to be made to you for life, your expected return is figured by multiplying the amount of the annual payment by your life expectancy as of the nearest birthday to the annuity starting date. The annuity starting date is the first day of the first period for which an annuity payment is received. For example, on January 1 you complete payment under an annuity contract providing for monthly payments starting on July 1 for the period beginning June 1. The annuity starting date is June 1. Use that date in computing your investment in the contract under Step 1 and your expected return.

If payments are for life, you find your life expectancy in IRS tables included in IRS Publication 939. If you have a single life annuity for which you made any investment after June 30, 1986, use IRS Table V from Publication 939, shown in Table 7-2 below. Table 7-2 also shows IRS Table I, which generally is used if the entire investment was before July 1, 1986, but you may elect to use Table V (7.24). When using the single life table, your age is the age at the birthday nearest the annuity starting date. If you have a joint and survivor annuity and after your death the same payments are to be made to a second annuitant, the expected return is based on your joint life expectancy. Use Table II in IRS Publication 939 to get joint life expectancy if the entire investment was before July 1, 1986. Use Table VI if any investment was made after June 30, 1986. If your joint and survivor annuity provides for a different payment amount to the survivor, you must separately compute the expected return for each annuitant; this method is explained in Publication 939. Adjustments to the life expectancy multiple are required when your annuity is payable quarterly, semiannually, or annually (7.24).

Table 7-2 Life Expectancy Tables from IRS Publication 939

| Age of primary annuitant at annuity starting date | Number of expected monthly payments | |

| Annuity starting date before November 19, 1996 | Annuity starting date after November 18, 1996 | |

| 55 and under | 300 | 360 |

| 56–60 | 260 | 310 |

| 61–65 | 240 | 260 |

| 66–70 | 170 | 210 |

| 71 and over | 120 | 160 |

| Combined ages of annuitants at annuity starting date | Number of expected monthly payments |

| 110 and under | 410 |

| 111–120 | 360 |

| 121–130 | 310 |

| 131–140 | 260 |

| 141 and over | 210 |

If the payments are for a fixed number of years or for life, whichever is shorter, find your expected return by multiplying your annual payments by a life expectancy multiple found in Table IV if your entire investment was before July 1, 1986, or Table VIII if any investment was made after June 30, 1986.

If payments are for a fixed number of years (as in an endowment contract) without regard to your life expectancy, find your expected return by multiplying your annual payment by the number of years.

Note: There is more information on the life expectancy tables in the following section (7.24).

Step 3: Divide the investment in the contract (Step 1) by the expected return (Step 2).

This will give you the tax-free percentage of your yearly annuity payments. The tax-free percentage remains the same for the remaining years of the annuity, even if payments increase due to a cost-of-living adjustment. A different computation of the tax-free percentage applies to variable annuities; see below.

If your annuity started before 1987, and you live longer than your projected life expectancy (shown in the IRS table), you may continue to apply the same tax-free percentage to each payment you receive. Thus, you may exclude from income more than you paid. However, if your annuity starting date is after 1986, your lifetime exclusion may not exceed your net cost, generally your unrecovered investment as of the annuity starting date, without reduction for any refund feature. Once you have recovered your net cost, further payments are fully taxable.

If your annuity starting date is after July 1, 1986, and you die before recovering your net cost, a deduction is allowed on your final tax return for the unrecovered cost. If a refund of the investment is made under the contract to a beneficiary, the beneficiary is allowed the deduction. The deduction is claimed as a miscellaneous itemized deduction that is not subject to the 2% adjusted gross income floor; see Chapter 19.

Step 4: Find your total annuity payments for the year.

For example, you received 10 monthly payments of $1,000 as your annuity began in March. Your total payments are $10,000, the monthly payment multiplied by 10.

Step 5: Nontaxable portion—multiply the percentage in Step 3 by the total in Step 4.

The result is the nontaxable portion (or excludable amount) of your annuity payments.

Step 6: Taxable portion—subtract the amount in Step 5 from the amount in Step 4.

This is the part of your annuity for the year that is subject to tax.

Note: There is an example of figuring the taxable and nontaxable portions for a single life annuity in the following section (7.24).

Variable annuities.

If you have a variable annuity that pays different benefits depending on cost-of-living indexes, profits earned by the annuity fund, or similar fluctuating standards, the tax-free portion of each payment is computed by dividing your investment in the contract (Step 1 above) by the total number of payments you expect to receive. If the annuity is for a definite period, the total number of payments equals the number of payments to be made each year multiplied by the number of years you will receive payments. If the annuity is for life, you divide the amount you invested in the contract by a multiple obtained from the appropriate life expectancy table; see Step 2. The result is the tax-free amount of annual annuity income.

If you receive a payment that is less than the nontaxable amount, you may elect when you receive the next payment to recalculate the nontaxable portion. The amount by which the prior nontaxable portion exceeded the payment you received is divided by the number of payments you expect as of the time of the next payment. The result is added to the previously calculated nontaxable portion, and the sum is the amount of each future payment to be excluded from tax. A statement must be attached to your return explaining the recomputation.

| Investment in the contract | $12,000 |

| Multiple (from Table V) | 20.0 |

| Amount of each payment excluded from tax ($12,000 ÷ 20) | $600 |

| Amount excludable in 2013 | $600 |

| Amount received in 2013 | 500 |

| Difference | $100 |

| Multiple as of 1/1/2014 (see Table V in Table 7-2 for age 67) | 18.4 |

| Amount added to previously determined annual exclusion ($100 ÷ 18.4) | $5.43 |

| Revised annual exclusion for 2014 and later years ($600 + $5.43) | $605.43 |

| Amount taxable in 2014 ($1,200 − $605.43) | $594.57 |

Penalty on Premature Withdrawals From Deferred Annuities

Withdrawals before the annuity starting date may be taxable or tax free, depending on whether investments were made before or after August 13, 1982 (7.23).

Withdrawals before age 59½ are also generally subject to a penalty of 10% of the amount includable in income. A withdrawal from an annuity contract is penalized unless: