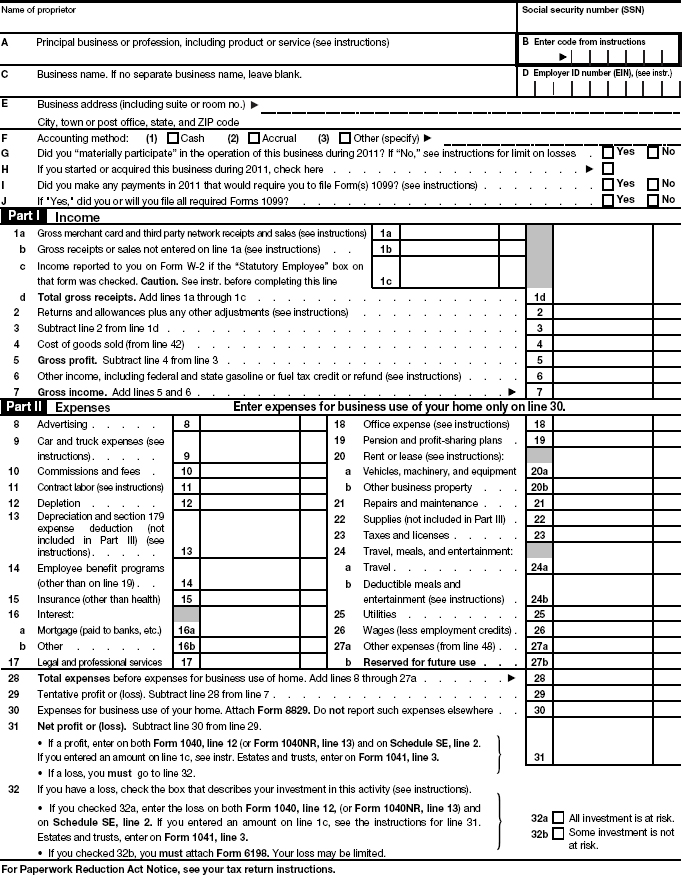

40.6 Filing Schedule C

In this section are explanations of how a sole proprietor reports income and expenses on Schedule C, a sample of which is on page 641. If you have more than one sole proprietorship, use a separate Schedule C for each business.

Schedule C-EZ.

This simple form is designed for persons on the cash basis who do not have a net business loss and have:

- Business expenses of $5,000 or less;

- No inventory at any time during the year;

- Only one sole proprietorship;

- No employees;

- No home office expense deduction;

- No prior year suspended passive activity losses from this business; and

- No depreciation to be reported on Form 4562.

Statutory employees.

Statutory employees report income and expenses on Schedule C. Thus, expenses may be deducted in full on Schedule C rather than as a miscellaneous itemized deduction (19.1), subject to the 2% adjusted gross income (AGI) floor on Schedule A. Statutory employees are full-time life insurance salespersons, agent or commission drivers distributing certain foods and beverages, pieceworkers, and full-time traveling or city salespersons who solicit on behalf of and transmit to their principals orders from wholesalers and retailers for merchandise for resale or for supplies.

The term full time refers to an exclusive or principal business activity for a single company or person and not to the time spent on the job. If your principal activity is soliciting orders for one company, but you also solicit incidental orders for another company, you are a full-time salesperson for the primary company. Solicitations of orders are considered incidental to a principal business activity if you devote 20% or less of your time to the solicitation activity. A city or traveling salesperson is presumed to meet the principal business activity test in a calendar year in which he or she devotes 80% or more of working time to soliciting orders for one principal.

IRS regulations give this example: A salesperson’s principal activity is getting orders from retail pharmacies for a wholesale drug company called Que Company. He occasionally takes orders for two other companies. He is a statutory employee only for Que Company.

If you are a statutory employee, your company checks Box 13 on Form W-2, identifying you as a statutory employee. Although a statutory employee may treat job expenses as business expenses, the employer withholds FICA (Social Security and Medicare) taxes on wages and commissions.

If you received a Form W-2 with “Statutory employee” checked in Box 13, include the income from Box 1 of the W-2 on Line 1c of Schedule C (or C-EZ). If you also have self-employment earnings from another business, you must report the self-employment earnings and statutory employee income on separate Schedules C. If both types of income are earned in the same business, allocate the expenses between the two activities on the separate schedules.

Gross receipts or sales on Schedule C.

Your gross receipts are reported on Line 1 of Schedule C, split between Lines 1a through 1c, depending on how you were paid.

Payments from merchant cards and third party networks (Line 1a): This line is for for reporting business payments you received through merchant credit cards and third party networks such as PayPal and Google Checkout. Such payments should have been reported to you by banks and third party network payers in Box 1 of Form 1099-K if your total transactions exceeded $20,000 and the number of transactions exceeded 200 for the year. In 2011, the IRS instructed you to not enter amounts from Form 1099-K on line 1a but instead enter them as part of gross receipts on line 1b. See the e-Supplement at jklasser.com for instructions on 2012 entries.

Other gross receipts (Line 1b): Business payments you received that are not reportable on Line 1a are entered on Line 1b. Do not report as receipts on Schedule C the following items:

- Gains or losses on the sale of property used in your business or profession. These transactions are reported on Schedule D and Form 4797.

- Dividends from stock held in the ordinary course of your business. These are reported as dividends from stocks that are held for investment.

Statutory employee income from Form W-2 (Line 1c): As discussed above, “statutory employee” income from Form W-2 is entered on Line 1c.

Deductions on Schedule C.

You can usually deduct most expenses incurred in your business, although there may be limits on the amount or timing of deductions. The basic requirement for deductibility is that expenses must be ordinary and necessary to your business. An ordinary expense is one that is common and accepted in your business; a necessary expense is one that is helpful and appropriate to your business.

Deductible business expenses are claimed in Part II; the descriptive breakdown of items is generally self-explanatory. However, note these points:

Car and truck expenses (Line 9): In the year you place a car in service, you may choose between the IRS mileage allowance and deducting actual expenses, plus depreciation. You must also attach Form 4562 to support a depreciation deduction; see Chapter 43.

Depreciation (Line 13): Enter here the amount of your annual depreciation deduction or Section 179 expensing. A complete discussion of depreciation may be found in Chapter 42. You must figure your deduction on Form 4562 for assets placed in service in 2012, or for cars, computers, or other “listed property,” regardless of when the assets were placed in service.

Sample Schedule C—Profit or Loss From Business

(This sample is subject to change; see the e-Supplement at jklasser.com )

Employee benefit programs including health insurance (Line 14): Enter your cost for the following programs you provide for your employees: accident or health plans; long-term care insurance coverage; wage continuation; self-insured medical reimbursement plans; educational assistance programs; supplemental unemployment benefits; and prepaid legal expenses. Retirement plan contributions, such as to pension and profit-sharing plans, are reported separately on Line 19.

Insurance other than health insurance (Line 15): Insurance policy premiums for the protection of your business, such as accident, burglary, embezzlement, marine risks, plate glass, public liability, workers’ compensation, fire, storm, or theft, and indemnity bonds upon employees, are deductible. State unemployment insurance payments are deducted here or as taxes if they are considered taxes under state law.

Premiums paid on an insurance policy on the life of an employee or one financially interested in a business, for the purpose of protecting you from loss in the event of the death of the insured, are not deductible.

Under a “12-month” rule, prepaid premiums can be deducted in the year paid if the coverage term does not extend more than 12 months beyond the first date coverage is received, and also does not extend beyond the taxable year following the year in which the premium is paid.

Premiums for disability insurance to cover loss of earnings when out ill or injured are nondeductible personal expenses. But you may deduct premiums covering business overhead expenses.

Interest (Line 16): Include interest on business debts, but prepaid interest that applies to future years is not deductible.

Deductible interest on an insurance loan is limited if you borrow against a life insurance policy covering yourself as an employee or the life of any other employee, officer, or other person financially interested in your business. Interest on such a loan is deductible only if the policy covers an officer or 20% owner (no more than five such “key persons” can be counted) and the loan is no more than $50,000 per person. If you own policies covering the same employees (or other persons) in more than one business, the $50,000 limit applies on an aggregate basis to all the policies. The interest deduction limit applies even if a sole proprietor borrows against a policy on his or her own life and uses the proceeds in a business; interest is not deductible to the extent the loan exceeds $50,000.

Pension and profit-sharing plans (Line 19): Keogh plan or SEP contributions made for your employees are entered here; contributions made for your account are entered directly on Form 1040 as an adjustment to income. In addition, you may have to file an information return by the last day of the seventh month following the end of the plan year (41.8).

Rent on business property (Line 20): Rent paid for the use of lofts, buildings, trucks, and other equipment is deductible. Prepaid rents can be deducted by cash-method taxpayers in the year of payment if the rent term does not extend more than 12 months beyond the first day of the lease and also not beyond the end of the taxable year following the taxable year in which the prepayment is made. However, the economic performance rules prevent accrual-method taxpayers from deducting prepaid rent; economic performance occurs only ratably over the lease term.

Taxes on leased property that you pay to the lessor are deductible as additional rent.

Repairs (Line 21): The cost of repairs and maintenance is deductible provided they do not materially add to the value of the property or appreciably prolong its life. Expenses of replacements that arrest deterioration and appreciably increase the value of the property are capitalized and their cost recovered through depreciation.

Taxes (Line 23): Deduct real estate and personal property taxes on business assets here. Also deduct your share of Social Security and Medicare taxes paid on behalf of employees and payments of federal unemployment tax. Federal highway use tax is deductible. Federal import duties and excise and stamp taxes normally not deductible as itemized deductions are deductible as business taxes if incurred by the business. Taxes on business property, such as an ad valorem tax, must be deducted here; they are not to be treated as itemized deductions. However, the IRS holds that you may not deduct state income taxes on business income as a business expense. Its reasoning: Income taxes are personal taxes even when paid on business income. As such, you may deduct state income tax only as an itemized deduction on Schedule A. The Tax Court supports the IRS rule on the grounds that it reflects Congressional intent toward the treatment of state income taxes in figuring taxable income.

For purposes of computing a net operating loss, state income tax on business income is treated as a business deduction.

If you pay or accrue sales tax on the purchase of nondepreciable business property, the sales tax is a deductible business expense. If the property is depreciable, add the sales tax to the cost basis for purposes of computing depreciation deductions.

Travel, meals, and entertainment (Line 24): Travel expenses on overnight business trips while “away from home” (20.5) are claimed on Line 24a. Total meals and entertainment expenses, reduced by 50%, are claimed on Line 24b. The 50% limit for meals and entertainment is increased to 75% for transportation industry workers subject to the Department of Transportation hours of service limits.

Self-employed persons may use the IRS meal allowance rates (20.4), instead of claiming actual expenses. Record-keeping requirements for travel and entertainment expenses are discussed in Chapter 20 (20.26–20.28).

Utilities (Line 25): Deduct utilities such as gas, electric, and telephone expenses incurred in your business. However, if you have a home office (40.12), you may not deduct the base rate (including taxes) of the first phone line into your home (19.14).

Wages (Line 26): You do not deduct wages paid to yourself. You may deduct reasonable wages paid to family members who work for you. If you have an employee who works in your office and also in your home, such as a domestic worker, you deduct that part of the salary allocated to the work in your office. If you claim any employment-related tax credit, the wage deduction is reduced by the credit. Check the e-Supplement at jklasser.com to see which employment-related credits apply for 2012.

Other expenses (Line 27): In Part V of Schedule C, you list deductible expenses not reported in Part II, such as amortizable business start-up costs (40.11), business-related education (33.15), subscriptions, and postage, and enter the total on Line 27.