40.16 Home Office for Sideline Business

by J.K. Lasser Institute

J.K. Lasser's Your Income Tax 2013: For Preparing Your 2012 Tax Return

40.16 Home Office for Sideline Business

by J.K. Lasser Institute

J.K. Lasser's Your Income Tax 2013: For Preparing Your 2012 Tax Return

- Cover

- Contents: Chapter by Chapter

- Title

- Copyright

- What’s New for 2012

- Key Tax Numbers for 2012

- Looking Ahead to 2013

- Part 1: Filing Basics

- Do You Have to File a 2012 Tax Return?

- Filing Tests for Dependents: 2012 Returns

- Where to File

- Filing Deadlines (on or before)

- Choosing Which Tax Form to File

- Chapter 1: Filing Status

- 1.1 Which Filing Status Should You Use?

- 1.2 Tax Rates Based on Filing Status

- 1.3 Filing Separately Instead of Jointly

- 1.4 Filing a Joint Return

- 1.5 Nonresident Alien Spouse

- 1.6 Community Property Rules

- 1.7 Innocent Spouse Rules

- 1.8 Separate Liability Election for Former Spouses

- 1.9 Equitable Relief

- 1.10 Death of Your Spouse in 2012

- 1.11 Qualifying Widow(er) Status If Your Spouse Died in 2011 or 2010

- 1.12 Qualifying as Head of Household

- 1.13 Filing for Your Child

- 1.14 Return for Deceased

- 1.15 Return for an Incompetent Person

- 1.16 How a Nonresident Alien Is Taxed

- 1.17 How a Resident Alien Is Taxed

- 1.18 Who Is a Resident Alien?

- 1.19 When an Alien Leaves the United States

- 1.20 Expatriation Tax

- Part 2: Reporting Your Income

- Chapter 2: Wages, Salary, and Other Compensation

- 2.1 Salary and Wage Income

- 2.2 Constructive Receipt of Year-End Paychecks

- 2.3 Pay Received in Property Is Taxed

- 2.4 Commissions Taxable When Credited

- 2.5 Unemployment Benefits

- 2.6 Strike Pay Benefits and Penalties

- 2.7 Nonqualified Deferred Compensation

- 2.8 Did You Return Wages Received in a Prior Year?

- 2.9 Waiver of Executor’s and Trustee’s Commissions

- 2.10 Life Insurance Benefits

- 2.11 Educational Benefits for Employees’ Children

- 2.12 Sick Pay Is Taxable

- 2.13 Workers’ Compensation Is Tax Free

- 2.14 Disability Pensions

- 2.15 Stock Appreciation Rights (SARs)

- 2.16 Stock Options

- 2.17 Restricted Stock

- Chapter 3: Fringe Benefits

- 3.1 Tax-Free Health and Accident Coverage Under Employer Plans

- 3.2 Health Savings Accounts (HSAs) and Archer MSAs

- 3.3 Reimbursements and Other Tax-Free Payments From Employer Health and Accident Plans

- 3.4 Group-Term Life Insurance Premiums

- 3.5 Dependent Care Assistance

- 3.6 Adoption Benefits

- 3.7 Education Assistance Plans

- 3.8 Company Cars, Parking, and Transit Passes

- 3.9 Working Condition Fringe Benefits

- 3.10 De Minimis Fringe Benefits

- 3.11 Employer-Provided Retirement Advice

- 3.12 Employee Achievement Awards

- 3.13 Employer-Furnished Meals or Lodging

- 3.14 Minister’s Rental or Housing Allowance

- 3.15 Cafeteria Plans Provide Choice of Benefits

- 3.16 Flexible Spending Arrangements

- 3.17 Company Services Provided at No Additional Cost

- 3.18 Discounts on Company Products or Services

- Chapter 4: Dividend and Interest Income

- 4.1 Reporting Dividends and Mutual-Fund Distributions

- 4.2 Qualified Corporate Dividends Taxed at Favorable Capital Gain Rates

- 4.3 Dividends From a Partnership, S Corporation, Estate, or Trust

- 4.4 Real Estate Investment Trust (REIT) Dividends

- 4.5 Taxable Dividends of Earnings and Profits

- 4.6 Stock Dividends on Common Stock

- 4.7 Dividends Paid in Property

- 4.8 Taxable Stock Dividends

- 4.9 Who Reports the Dividends

- 4.10 Year Dividends Are Reported

- 4.11 Distribution Not Out of Earnings: Return of Capital

- 4.12 Reporting Interest on Your Tax Return

- 4.13 Interest on Frozen Accounts Not Taxed

- 4.14 Interest Income on Debts Owed to You

- 4.15 Reporting Interest on Bonds Bought or Sold

- 4.16 Forfeiture of Interest on Premature Withdrawals

- 4.17 Amortization of Bond Premium

- 4.18 Discount on Bonds

- 4.19 Reporting Original Issue Discount on Your Return

- 4.20 Reporting Income on Market Discount Bonds

- 4.21 Discount on Short-Term Obligations

- 4.22 Stripped Coupon Bonds and Stock

- 4.23 Sale or Retirement of Bonds and Notes

- 4.24 State and City Interest Generally Tax Exempt

- 4.25 Taxable State and City Interest

- 4.26 Tax-Exempt Bonds Bought at a Discount

- 4.27 Treasury Bills, Notes, and Bonds

- 4.28 Interest on United States Savings Bonds

- 4.29 Deferring United States Savings Bond Interest

- 4.30 Minimum Interest Rules

- 4.31 Interest-Free or Below-Market-Interest Loans

- 4.32 Minimum Interest on Seller-Financed Sales

- Chapter 5: Reporting Property Sales

- 5.1 General Tax Rules for Property Sales

- 5.2 How Property Sales Are Classified and Taxed

- 5.3 Capital Gains Rates and Holding Periods

- 5.4 Capital Losses and Carryovers

- 5.5 Capital Losses of Married Couples

- 5.6 Losses May Be Disallowed on Sales to Related Persons

- 5.7 Deferring or Excluding Gain on Small Business Stock Investment

- 5.8 Sample Entries of Capital Asset Sales on Form 8949 and on Schedule D

- 5.9 Counting the Months in Your Holding Period

- 5.10 Holding Period for Securities

- 5.11 Holding Period for Real Estate

- 5.12 Holding Period: Gifts, Inheritances, and Other Property

- 5.13 Calculating Gain or Loss

- 5.14 Amount Realized Is the Total Selling Price

- 5.15 Finding Your Cost

- 5.16 Unadjusted Basis of Your Property

- 5.17 Basis of Property You Inherited or Received as a Gift

- 5.18 Joint Tenancy Basis Rules for Surviving Tenants

- 5.19 Allocating Cost Among Several Assets

- 5.20 How To Find Adjusted Basis

- 5.21 Tax Advantage of Installment Sales

- 5.22 Figuring the Taxable Part of Installment Payments

- 5.23 Electing Not To Report on the Installment Method

- 5.24 Restriction on Installment Sales to Relatives

- 5.25 Contingent Payment Sales

- 5.26 Using Escrow and Other Security Arrangements

- 5.27 Minimum Interest on Deferred Payment Sales

- 5.28 Dispositions of Installment Notes

- 5.29 Repossession of Personal Property Sold on Installment

- 5.30 Boot in Like-Kind Exchange Payable in Installments

- 5.31 “Interest” Tax on Sales Over $150,000 Plus $5 Million Debt

- 5.32 Worthless Securities

- 5.33 Tax Consequences of Bad Debts

- 5.34 Four Rules To Prove a Bad Debt Deduction

- 5.35 Family Bad Debts

- Chapter 6: Tax-Free Exchanges of Property

- 6.1 Trades of Like-Kind Property

- 6.2 Personal Property Held for Business or Investment

- 6.3 Receipt of Cash and Other Property—“Boot”

- 6.4 Time Limits and Security Arrangements for Deferred Exchanges

- 6.5 Qualified Exchange Accommodation Arrangements (QEAAs) for Reverse Exchanges

- 6.6 Exchanges Between Related Parties

- 6.7 Property Transfers Between Spouses and Ex-Spouses

- 6.8 Tax-Free Exchanges of Stock in Same Corporation

- 6.9 Joint Ownership Interests

- 6.10 Setting up Closely Held Corporations

- 6.11 Exchanges of Coins and Bullion

- 6.12 Tax-Free Exchanges of Insurance Policies

- Chapter 7: Retirement and Annuity Income

- 7.1 Retirement Distributions on Form 1099-R

- 7.2 Lump-Sum Distributions

- 7.3 Lump-Sum Options If You Were Born Before January 2, 1936

- 7.4 Averaging on Form 4972

- 7.5 Capital Gain Treatment for Pre-1974 Participation

- 7.6 Lump-Sum Payments Received by Beneficiary

- 7.7 Tax-Free Rollovers From Qualified Plans

- 7.8 Direct Rollover or Personal Rollover

- 7.9 Rollover of Proceeds From Sale of Property

- 7.10 Distribution of Employer Stock or Other Securities

- 7.11 Survivor Annuity for Spouse

- 7.12 Court Distributions to Former Spouse Under a QDRO

- 7.13 When Retirement Benefits Must Begin

- 7.14 Payouts to Beneficiaries

- 7.15 Penalty for Distributions Before Age 59½

- 7.16 Restrictions on Loans From Company Plans

- 7.17 Tax Benefits of 401(k) Plans

- 7.18 Limit on Salary-Reduction Deferrals

- 7.19 Withdrawals From 401(k) Plans Restricted

- 7.20 Designated Roth Contributions to 401(k) Plans

- 7.21 Annuities for Employees of Tax-Exempts and Schools (403(b) Plans)

- 7.22 Government and Exempt Organization Deferred Pay Plans

- 7.23 Figuring the Taxable Part of Your Annuity

- 7.24 Life Expectancy Tables

- 7.25 When You Convert Your Endowment Policy

- 7.26 Reporting Employee Annuities

- 7.27 Simplified Method for Calculating Taxable Employee Annuity

- 7.28 Employee’s Cost in Annuity

- 7.29 Withdrawals From Employer’s Qualified Retirement Plan Before Annuity Starting Date

- Chapter 8: IRAs

- 8.1 Starting a Traditional IRA

- 8.2 Traditional IRA Contributions Must Be Based on Earnings

- 8.3 Contributions to a Traditional IRA If You Are Married

- 8.4 IRA Deduction Restrictions for Active Participants in Employer Plan

- 8.5 Active Participation in Employer Plan

- 8.6 Nondeductible Contributions to Traditional IRAs

- 8.7 Penalty for Excess Contributions to Traditional IRAs

- 8.8 Taxable Distributions From Traditional IRAs

- 8.9 Partially Tax-Free Traditional IRA Distributions Allocable to Nondeductible Contributions

- 8.10 Tax-Free Rollovers and Direct Transfers to Traditional IRAs

- 8.11 Transfer of Traditional IRA to Spouse at Divorce

- 8.12 Penalty for Traditional IRA Withdrawals Before Age 59½

- 8.13 Mandatory Distributions From a Traditional IRA After Age 70½

- 8.14 Inherited Traditional IRAs

- 8.15 SEP Basics

- 8.16 Salary-Reduction SEP Set Up Before 1997

- 8.17 Who Is Eligible for a SIMPLE IRA?

- 8.18 SIMPLE IRA Contributions and Distributions

- 8.19 Roth IRA Advantages

- 8.20 Annual Contributions to a Roth IRA

- 8.21 Converting a Traditional IRA to a Roth IRA

- 8.22 Recharacterizations and Reconversions

- 8.23 Distributions From a Roth IRA

- 8.24 Distributions to Roth IRA Beneficiaries

- Chapter 9: Income From Real Estate Rentals and Royalties

- 9.1 Reporting Rental Real Estate Income and Expenses

- 9.2 Checklist of Rental Deductions

- 9.3 Distinguishing Between a Repair and an Improvement

- 9.4 Reporting Rents From a Multi-Unit Residence

- 9.5 Depreciation on Converting a Home to Rental Property

- 9.6 Renting a Residence to a Relative

- 9.7 Personal Use and Rental of a Residence During the Year

- 9.8 Counting Personal-Use Days and Rental Days for a Residence

- 9.9 Allocating Expenses of a Residence to Rental Days

- 9.10 Rentals Lacking Profit Motive

- 9.11 Reporting Royalty Income

- 9.12 Production Costs of Books and Creative Properties

- 9.13 Deducting the Cost of Patents or Copyrights

- 9.14 Intangible Drilling Costs

- 9.15 Depletion Deduction

- 9.16 Oil and Gas Percentage Depletion

- Chapter 10: Loss Restrictions: Passive Activities and At-Risk Limits

- 10.1 Rental Activities

- 10.2 Rental Real Estate Loss Allowance of up to $25,000

- 10.3 Real Estate Professionals

- 10.4 Participation May Avoid Passive Loss Restrictions

- 10.5 Classifying Business Activities as One or Several

- 10.6 Material Participation Tests for Business

- 10.7 Tax Credits of Passive Activities Limited

- 10.8 Determining Passive or Nonpassive Income and Loss

- 10.9 Passive Income Recharacterized as Nonpassive Income

- 10.10 Working Interests in Oil and Gas Wells

- 10.11 Partners and Members of LLCs and LLPs

- 10.12 Form 8582

- 10.13 Suspended Losses Allowed on Disposition of Your Interest

- 10.14 Suspended Tax Credits

- 10.15 Personal Service and Closely Held Corporations

- 10.16 Sales of Property and of Passive Activity Interests

- 10.17 At-Risk Limits

- 10.18 What Is At Risk?

- 10.19 Amounts Not At Risk

- 10.20 At-Risk Investment in Several Activities

- 10.21 Carryover of Disallowed Losses

- 10.22 Recapture of Losses Where At Risk Is Less Than Zero

- Chapter 11: Other Income

- 11.1 Prizes and Awards

- 11.2 Lottery and Sweepstake Winnings

- 11.3 Gambling Winnings and Losses

- 11.4 Gifts and Inheritances

- 11.5 Refunds of State and Local Income Tax Deductions

- 11.6 Other Recovered Deductions

- 11.7 How Legal Damages Are Taxed

- 11.8 Cancellation of Debts You Owe

- 11.9 Schedule K-1

- 11.10 How Partners Report Partnership Profit and Loss

- 11.11 When a Partner Reports Income or Loss

- 11.12 Partnership Loss Limitations

- 11.13 Unified Tax Audits of Partnerships

- 11.14 Stockholder Reporting of S Corporation Income and Loss

- 11.15 How Beneficiaries Report Estate or Trust Income

- 11.16 Reporting Income in Respect of a Decedent (IRD)

- 11.17 Deduction for Estate Tax Attributable to IRD

- 11.18 How Life Insurance Proceeds Are Taxed to a Beneficiary

- 11.19 A Policy With a Family Income Rider

- 11.20 Selling or Surrendering Life Insurance Policy

- 11.21 Jury Duty Fees

- 11.22 Foster Care Payments

- Chapter 2: Wages, Salary, and Other Compensation

- Part 3: Claiming Deductions

- Chapter 12: Deductions Allowed in Figuring Adjusted Gross Income

- 12.1 Figuring Adjusted Gross Income (AGI)

- 12.2 Claiming Deductions From Gross Income

- 12.3 What Moving Costs Are Deductible?

- 12.4 The Distance Test

- 12.5 The 39-Week Test for Employees

- 12.6 The 78-Week Test for the Self-Employed and Partners

- 12.7 Claiming Deductible Moving Expenses

- 12.8 Reimbursements of Moving Expenses

- Chapter 13: Claiming the Standard Deduction or Itemized Deductions

- Chapter 14: Charitable Contribution Deductions

- 14.1 Deductible Contributions

- 14.2 Nondeductible Contributions

- 14.3 Contributions That Provide You With Benefits

- 14.4 Unreimbursed Expenses of Volunteer Workers

- 14.5 Support of a Student in Your Home

- 14.6 What Kind of Property Are You Donating?

- 14.7 Cars, Clothing, and Other Property Valued Below Cost

- 14.8 Bargain Sales of Appreciated Property

- 14.9 Art Objects

- 14.10 Interests in Real Estate

- 14.11 Life Insurance

- 14.12 Business Inventory

- 14.13 Donations Through Trusts

- 14.14 Records Needed To Substantiate Your Contributions

- 14.15 Form 8283 and Written Appraisal Requirements for Property Donations

- 14.16 Penalty for Substantial Overvaluation of Property

- 14.17 Ceiling on Charitable Contributions

- 14.18 Carryover for Excess Donations

- 14.19 Election To Reduce Fair Market Value by Appreciation

- Chapter 15: Itemized Deduction for Interest Expenses

- 15.1 Home Mortgage Interest

- 15.2 Home Acquisition Loans

- 15.3 Home Equity Loans

- 15.4 Home Construction Loans

- 15.5 Home Improvement Loans

- 15.6 Mortgage Insurance Premiums and Other Payment Rules

- 15.7 Interest on Refinanced Loans

- 15.8 “Points”

- 15.9 Cooperative and Condominium Apartments

- 15.10 Investment Interest Limitations

- 15.11 Debts To Carry Tax-Exempt Obligations

- 15.12 Earmarking Use of Loan Proceeds For Investment or Business

- 15.13 Year To Claim an Interest Deduction

- 15.14 Prepaid Interest

- Chapter 16: Deductions for Taxes

- 16.1 Deductible Taxes

- 16.2 Nondeductible Taxes

- 16.3 State and Local Income Taxes or General Sales Taxes

- 16.4 Deducting Real Estate Taxes

- 16.5 Assessments

- 16.6 Tenants’ Payment of Taxes

- 16.7 Allocating Taxes When You Sell or Buy Realty

- 16.8 Automobile License Fees

- 16.9 Taxes Deductible as Business Expenses

- 16.10 Foreign Taxes

- Chapter 17: Medical and Dental Expense Deductions

- 17.1 Medical Expenses Must Exceed AGI Threshold

- 17.2 Allowable Medical Care Costs

- 17.3 Nondeductible Medical Expenses

- 17.4 Reimbursements Reduce Deductible Expenses

- 17.5 Premiums of Medical Care Policies

- 17.6 Expenses of Your Spouse

- 17.7 Expenses of Your Dependents

- 17.8 Decedent’s Medical Expenses

- 17.9 Travel Costs May Be Medical Deductions

- 17.10 Schooling for the Mentally or Physically Disabled

- 17.11 Nursing Homes

- 17.12 Nurses’ Wages

- 17.13 Home Improvements as Medical Expenses

- 17.14 Costs Deductible as Business Expenses

- 17.15 Long-Term Care Premiums and Services

- 17.16 Life Insurance Used by Chronically ill or Terminally ill Persons

- Chapter 18: Casualty and Theft Losses and Involuntary Conversions

- 18.1 Sudden Event Test for Casualty Losses

- 18.2 When To Deduct a Casualty Loss

- 18.3 Disaster Losses

- 18.4 Who May Deduct a Casualty Loss

- 18.5 Bank Deposit Losses

- 18.6 Damage to Trees and Shrubs

- 18.7 Deducting Damage to Your Car

- 18.8 Proving a Casualty Loss

- 18.9 Theft Losses

- 18.10 Proving a Theft Loss

- 18.11 Nondeductible Casualty and Theft Losses

- 18.12 Floors for Personal-Use Property Losses

- 18.13 Figuring Your Loss on Form 4684

- 18.14 Personal and Business Use of Property

- 18.15 Repairs May Be a “Measure of Loss”

- 18.16 Insurance Reimbursements

- 18.17 Excess Living Costs Paid by Insurance Are Not Taxable

- 18.18 Do Your Casualty or Theft Losses Exceed Your Income?

- 18.19 Defer Gain by Replacing Property

- 18.20 Involuntary Conversions Qualifying for Tax Deferral

- 18.21 How To Elect To Defer Tax

- 18.22 Time Period for Buying Replacement Property

- 18.23 Types of Qualifying Replacement Property

- 18.24 Cost of Replacement Property Determines Postponed Gain

- 18.25 Special Assessments and Severance Damages

- 18.26 Reporting Gains From Casualties

- Chapter 19: Deducting Job Costs and Other Miscellaneous Expenses

- 19.1 2% AGI Floor Reduces Most Miscellaneous Expenses

- 19.2 Effect of 2% AGI Floor on Deductions

- 19.3 Checklist of Job Expenses Subject to the 2% AGI Floor

- 19.4 Job Expenses Not Subject to the 2% AGI Floor

- 19.5 Dues and Subscriptions

- 19.6 Uniforms and Work Clothes

- 19.7 Expenses of Looking for a New Job

- 19.8 Local Transportation Costs

- 19.9 Unusual Job Expenses

- 19.10 Computers Bought for Work

- 19.11 Cell Phones, Calculators, Copiers and Fax Machines

- 19.12 Small Tools

- 19.13 Employee Home Office Deductions

- 19.14 Telephone Costs

- 19.15 Checklist of Deductible Investment Expenses

- 19.16 Costs of Tax Return Preparation and Audits

- 19.17 Deducting Legal Costs

- 19.18 Contingent Fees Paid Out of Taxable Awards

- Chapter 20: Travel and Entertainment Expense Deductions

- 20.1 Deduction Guide for Travel and Transportation Expenses

- 20.2 Commuting Expenses

- 20.3 Overnight-Sleep Test Limits Deduction of Meal Costs

- 20.4 IRS Meal Allowance

- 20.5 Business Trip Deductions

- 20.6 Local Lodging Costs

- 20.7 When Are You Away From Home?

- 20.8 Fixing a Tax Home If You Work in Different Locations

- 20.9 Tax Home of Married Couple Working in Different Cities

- 20.10 Deducting Living Costs on Temporary Assignment

- 20.11 Business-Vacation Trips Within the United States

- 20.12 Business-Vacation Trips Outside the United States

- 20.13 Deducting Expenses of Business Conventions

- 20.14 Travel Expenses of a Spouse or Dependents

- 20.15 Restrictions on Foreign Conventions and Cruises

- 20.16 50% Deduction Limit

- 20.17 The Restrictive Tests for Meals and Entertainment

- 20.18 Directly Related Dining and Entertainment

- 20.19 Goodwill Entertainment

- 20.20 Home Entertaining

- 20.21 Your Personal Share of Entertainment Costs

- 20.22 Entertainment Costs of Spouses

- 20.23 Entertainment Facilities and Club Dues

- 20.24 Restrictive Test Exception for Reimbursements

- 20.25 50% Cost Limitation on Meals and Entertainment

- 20.26 Business Gift Deductions Are Limited

- 20.27 Record-Keeping Requirements

- 20.28 Proving Travel and Entertainment Expenses

- 20.29 Reporting T&E Expenses If You Are Self-Employed

- 20.30 Employee Reporting of Unreimbursed T&E Expenses

- 20.31 Tax Treatment of Reimbursements

- 20.32 What Is an Accountable Plan?

- 20.33 Per Diem Travel Allowance Under Accountable Plans

- 20.34 Automobile Mileage Allowance

- 20.35 Reimbursements Under Non-Accountable Plans

- Chapter 21: Personal Exemptions

- 21.1 How Many Exemptions May You Claim?

- 21.2 Your Spouse as an Exemption

- 21.3 Qualifying Children

- 21.4 Qualifying Relatives

- 21.5 Meeting the Support Test for a Qualifying Relative

- 21.6 Multiple Support Agreements

- 21.7 Special Rule for Divorced or Separated Parents

- 21.8 The Dependent Must Meet a Citizen or Resident Test

- 21.9 The Dependent Does Not File a Joint Return

- 21.10 Spouses’ Names and Social Security Numbers on Joint Return

- 21.11 Reporting Social Security Numbers of Dependents

- 21.12 Personal Exemptions Not Subject to Phaseout for 2012

- Chapter 12: Deductions Allowed in Figuring Adjusted Gross Income

- Part 4: Personal Tax Computations

- Chapter 22: Figuring Your Regular Income Tax Liability

- Chapter 23: Alternative Minimum Tax (AMT)

- Chapter 24: Computing the “Kiddie Tax” on Your Child’s Investment Income

- Chapter 25: Personal Tax Credits Reduce Your Tax Liability

- 25.1 Overview of Personal Tax Credits

- 25.2 Child Tax Credit for Children Under Age 17

- 25.3 Figuring the Child Tax Credit

- 25.4 Qualifying for Child and Dependent Care Credit

- 25.5 Limits on the Dependent Care Credit

- 25.6 Earned Income Test for Dependent Care Credit

- 25.7 Credit Allowed for Care of Qualifying Persons

- 25.8 Expenses Qualifying for the Dependent Care Credit

- 25.9 Dependent Care Credit Rules for Separated Couples

- 25.10 Qualifying Tests for EIC

- 25.11 Income Tests for Earned Income Credit (EIC)

- 25.12 Look up EIC in Government Tables

- 25.13 Qualifying for the Adoption Credit

- 25.14 Claiming the Adoption Credit on Form 8839

- 25.15 Eligibility for the Saver’s Credit

- 25.16 Figuring the Saver’s Credit

- 25.17 Health Coverage Credit

- 25.18 Mortgage Interest Credit

- 25.19 Residential Energy Credits

- 25.20 Credits for Fuel Cell Vehicles and Plug-in Electric Vehicles

- 25.21 Repayment of the First-Time Homebuyer Credit

- Chapter 26: Tax Withholdings

- 26.1 Withholdings Should Cover Estimated Tax

- 26.2 Income Taxes Withheld on Wages

- 26.3 Low Earners May Be Exempt From Withholding

- 26.4 Are You Withholding the Right Amount?

- 26.5 Voluntary Withholding on Government Payments

- 26.6 When Tips Are Subject to Withholding

- 26.7 Withholding on Gambling Winnings

- 26.8 FICA Withholdings

- 26.9 Withholding on Retirement Distributions

- 26.10 Backup Withholding

- Chapter 27: Estimated Tax Payments

- Part 5: Tax Planning

- Chapter 28: Tax Planning Overview

- Chapter 29: Tax Savings for Residence Sales

- 29.1 Avoiding Tax on Sale of Principal Residence

- 29.2 Meeting the Ownership and Use Tests

- 29.3 Home Sales by Married Persons

- 29.4 Reduced Maximum Exclusion

- 29.5 Figuring Gain or Loss

- 29.6 Figuring Adjusted Basis

- 29.7 Personal and Business Use of a Home

- 29.8 No Loss Allowed on Personal Residence

- 29.9 Loss on Residence Converted to Rental Property

- 29.10 Loss on Residence Acquired by Gift or Inheritance

- Chapter 30: Tax Rules for Investors in Securities

- 30.1 Planning Year-End Securities Transactions

- 30.2 Earmarking Stock Lots

- 30.3 Sale of Stock Dividends

- 30.4 Stock Rights

- 30.5 Short Sales of Stock

- 30.6 Wash Sales

- 30.7 Convertible Stocks and Bonds

- 30.8 Constructive Sales of Appreciated Financial Positions

- 30.9 Straddle Losses

- 30.10 Capital Gain Restricted on Conversion Transactions

- 30.11 Puts and Calls and Index Options

- 30.12 Investing in Tax-Exempts

- 30.13 Ordinary Loss for Small Business Stock (Section 1244)

- 30.14 Series EE Bonds

- 30.15 I Bonds

- 30.16 Trader, Dealer, or Investor?

- 30.17 Mark-to-Market Election for Traders

- Chapter 31: Tax Savings for Investors in Real Estate

- 31.1 Real Estate Ventures

- 31.2 Sales of Subdivided Land—Dealer or Investor?

- 31.3 Exchanging Real Estate Without Tax

- 31.4 Timing Your Real Property Sales

- 31.5 Cancellation of a Lease

- 31.6 Sale of an Option

- 31.7 Granting of an Easement

- 31.8 Special Tax Credits for Real Estate Investments

- 31.9 Foreclosures, Repossessions, Short Sales, and Voluntary Conveyances to Creditors

- 31.10 Restructuring Mortgage Debt

- 31.11 Abandonments

- 31.12 Seller’s Repossession After Buyer’s Default on Mortgage

- 31.13 Foreclosure on Mortgages Other Than Purchase Money

- 31.14 Foreclosure Sale to Third Party

- 31.15 Transferring Mortgaged Realty

- Chapter 32: Tax Rules for Investors in Mutual Funds

- 32.1 Timing of Your Investment Can Affect Your Taxes

- 32.2 Reinvestment Plans

- 32.3 Mutual-Fund Distributions Reported on Form 1099-DIV

- 32.4 Tax-Exempt Bond Funds

- 32.5 Fund Expenses

- 32.6 Tax Credits From Mutual Funds

- 32.7 How To Report Mutual Fund Distributions

- 32.8 Redemptions and Exchanges of Fund Shares

- 32.9 Basis of Redeemed Shares

- 32.10 Comparison of Basis Methods

- Chapter 33: Educational Tax Benefits

- 33.1 Scholarships and Grants

- 33.2 Tuition Reductions for College Employees

- 33.3 How Fulbright Awards Are Taxed

- 33.4 United States Savings Bond Tuition Plans

- 33.5 Contributing to a Qualified Tuition Program (Section 529 Plan)

- 33.6 Distributions From Qualified Tuition Programs (Section 529 Plans)

- 33.7 Education Tax Credits

- 33.8 American Opportunity Credit

- 33.9 Lifetime Learning Credit

- 33.10 Contributing to a Coverdell Education Savings Account (ESA)

- 33.11 Distributions From Coverdell ESAs

- 33.12 Tuition and Fees Deduction

- 33.13 Student Loan Interest Deduction

- 33.14 Types of Deductible Work-Related Costs

- 33.15 Work-Related Tests for Education Costs

- 33.16 Local Transportation and Travel Away From Home To Take Courses

- Chapter 34: Special Tax Rules for Senior Citizens

- 34.1 Senior Citizens Get Certain Filing Breaks

- 34.2 Social Security Benefits Subject to Tax

- 34.3 Computing Taxable Social Security Benefits

- 34.4 Election for Lump-Sum Social Security Benefit Payment

- 34.5 Retiring on Social Security Benefits

- 34.6 How Tax on Social Security Reduces Your Earnings

- 34.7 Claiming the Credit for the Elderly and Disabled

- 34.8 Base Amount for the Elderly or Disabled Credit

- 34.9 Reduction of the Base Amount and Liability Limitation for the Credit

- 34.10 Tax Effects of Moving to a Continuing Care Facility

- 34.11 Medicare Part B and Part D Premiums for 2013

- Chapter 35: Members of the Armed Forces

- 35.1 Taxable Armed Forces Pay and Benefits

- 35.2 Tax-Free Armed Forces Benefits

- 35.3 Deductions for Armed Forces Personnel

- 35.4 Tax-Free Pay for Service in Combat Zone

- 35.5 Tax Deadlines Extended for Combat Zone or Contingency Operation Service

- 35.6 Tax Forgiveness for Combat Zone or Terrorist or Military Action Deaths

- 35.7 Extension To Pay Your Tax When Entering the Service

- 35.8 Tax Information for Reservists

- Chapter 36: How To Treat Foreign Earned Income

- 36.1 Claiming the Foreign Earned Income Exclusion

- 36.2 What Is Foreign Earned Income?

- 36.3 Qualifying for the Foreign Earned Income Exclusion

- 36.4 How To Treat Housing Costs

- 36.5 Meeting the Foreign Residence or Physical Presence Test

- 36.6 Claiming Deductions

- 36.7 Exclusion Not Established When Your Return Is Due

- 36.8 Tax-Free Meals and Lodging for Workers in Camps

- 36.9 Virgin Islands, Samoa, Guam, and Northern Marianas

- 36.10 Earnings in Puerto Rico

- 36.11 Tax Treaties With Foreign Countries

- 36.12 Exchange Rates and Blocked Currency

- 36.13 Foreign Tax Credit

- Chapter 37: Planning Alimony and Marital Settlements

- 37.1 Planning Alimony Agreements

- 37.2 Decree or Agreement Required

- 37.3 Cash Payments Required

- 37.4 Payments Must Stop at Death

- 37.5 Child Support Payments Are Not Alimony

- 37.6 No Minimum Payment Period for Alimony

- 37.7 3rd Year Recapture If Alimony Drops by More Than $15,000

- 37.8 Legal Fees of Marital Settlements

- Chapter 38: Household Employment Taxes (“Nanny Tax”)

- Chapter 39: Gift and Estate Tax Planning Basics

- 39.1 Gifts of Appreciated Property

- 39.2 Gift Tax Basics

- 39.3 Filing a Gift Tax Return

- 39.4 Gift Tax Credit

- 39.5 Custodial Accounts for Minors

- 39.6 Trusts in Family Planning

- 39.7 What is the Estate Tax?

- 39.8 Take Inventory and Estimate the Value of Your Potential Estate

- 39.9 Estate Tax for 2012

- 39.10 Planning for a Potential Estate Tax

- Part 6: Business Tax Planning

- Chapter 40: Income or Loss From Your Business or Profession

- 40.1 Forms of Doing Business

- 40.2 Reporting Self-Employed Income

- 40.3 Accounting Methods for Reporting Business Income

- 40.4 Tax Reporting Year for Self-Employed

- 40.5 Reporting Certain Payments and Receipts to the IRS

- 40.6 Filing Schedule C

- 40.7 Deductions for Professionals

- 40.8 Nondeductible Expense Items

- 40.9 How Authors and Artists May Write Off Expenses

- 40.10 Deducting Expenses of a Sideline Business or Hobby

- 40.11 Deducting Expenses of Looking for a New Business

- 40.12 Home Office Deduction

- 40.13 What Home Office Expenses Are Deductible?

- 40.14 Allocating Expenses to Business Use

- 40.15 Business Income May Limit Home Office Deductions

- 40.16 Home Office for Sideline Business

- 40.17 Depreciation of Office in Cooperative Apartment

- 40.18 Net Operating Losses (NOLs)

- 40.19 Your Net Operating Loss

- 40.20 How To Report a Net Operating Loss

- 40.21 How To Carry Back Your Net Operating Loss

- 40.22 Election To Carry Forward Losses

- 40.23 Overview of the Domestic Production Activities Deduction

- 40.24 Qualified Production Activities

- 40.25 Figuring the Deduction

- 40.26 Business Credits

- 40.27 Filing Schedule F

- 40.28 Farming Expenses

- Chapter 41: Retirement and Medical Plans for Self-Employed

- 41.1 Overview of Retirement and Medical Plans

- 41.2 Choosing a Keogh Plan

- 41.3 Choosing a SEP

- 41.4 Deductible Keogh or SEP Contributions

- 41.5 How To Claim the Keogh or SEP Deduction

- 41.6 How To Qualify a Keogh Plan or SEP Plan

- 41.7 Annual Keogh Plan Return

- 41.8 How Keogh Plan Distributions Are Taxed

- 41.9 SIMPLE IRA Plans

- 41.10 Health Savings Account (HSA) Basics

- 41.11 Limits on Deductible HSA Contributions

- 41.12 Distributions From HSAs

- 41.13 Archer MSAs

- 41.14 Small Business Health Tax Credit

- Chapter 42: Claiming Depreciation Deductions

- 42.1 What Property May Be Depreciated?

- 42.2 Claiming Depreciation on Your Tax Return

- 42.3 First-Year Expensing Deduction

- 42.4 MACRS Recovery Periods

- 42.5 MACRS Rates

- 42.6 Half-Year Convention for MACRS

- 42.7 Last Quarter Placements—Mid-Quarter Convention

- 42.8 150% Rate Election

- 42.9 Straight-Line Depreciation

- 42.10 Computers and Other Listed Property

- 42.11 Assets in Service Before 1987

- 42.12 MACRS for Real Estate Placed in Service After 1986

- 42.13 Demolishing a Building

- 42.14 Leasehold Improvements

- 42.15 Depreciating Real Estate Placed in Service After 1980 and Before 1987

- 42.16 When MACRS Is Not Allowed

- 42.17 Amortizing Goodwill and Other Intangibles (Section 197)

- 42.18 Deducting the Cost of Computer Software

- 42.19 Amortizing Song Rights

- 42.20 Bonus Depreciation

- Chapter 43: Deducting Car and Truck Expenses

- 43.1 Standard Mileage Rate

- 43.2 Expense Allocations

- 43.3 Depreciation Restrictions on Cars, Trucks, and Vans

- 43.4 Annual Ceilings on Depreciation

- 43.5 MACRS Rates for Cars, Trucks, and Vans

- 43.6 Straight-Line Method

- 43.7 Depreciation for Year Vehicle Is Disposed Of

- 43.8 Depreciation After Recovery Period Ends

- 43.9 Trade-in of Business Vehicle

- 43.10 Recapture of Deductions on Business Car, Truck, or Van

- 43.11 Keeping Records of Business Use

- 43.12 Leased Business Vehicles: Deductions and Income

- Chapter 44: Sales of Business Property

- 44.1 Depreciation Recaptured as Ordinary Income on Sale of Personal Property

- 44.2 Depreciation Recaptured as Ordinary Income on Sale of Real Estate

- 44.3 Recapture of First-Year Expensing

- 44.4 Gifts and Inheritances of Depreciable Property

- 44.5 Involuntary Conversions and Tax-Free Exchanges

- 44.6 Installment Sale of Depreciable Property

- 44.7 Sale of a Proprietorship

- 44.8 Property Used in a Business (Section 1231 Assets)

- 44.9 Sale of Property Used for Business and Personal Purposes

- 44.10 Should You Trade in Business Equipment?

- 44.11 Corporate Liquidation

- Chapter 45: Figuring Self-Employment Tax

- Chapter 40: Income or Loss From Your Business or Profession

- Part 7: Filing Your Return and What Happens After You File

- Chapter 46: Filing Your Return

- Chapter 47: Filing Refund Claims, and Amended Returns

- Chapter 48: If the IRS Examines Your Return

- 48.1 Odds of Being Audited

- 48.2 When the IRS Can Assess Additional Taxes

- 48.3 Audit Overview

- 48.4 Preparing for the Audit

- 48.5 Handling the Audit

- 48.6 Tax Penalties for Inaccurate Returns

- 48.7 Penalties for Not Reporting Foreign Financial Accounts

- 48.8 Agreeing to the Audit Changes

- 48.9 Disputing the Audit Changes

- 48.10 Offer in Compromise

- 48.11 Recovering Costs of a Tax Dispute

- 48.12 Suing the IRS for Unauthorized Collection

- Glossary

- Index

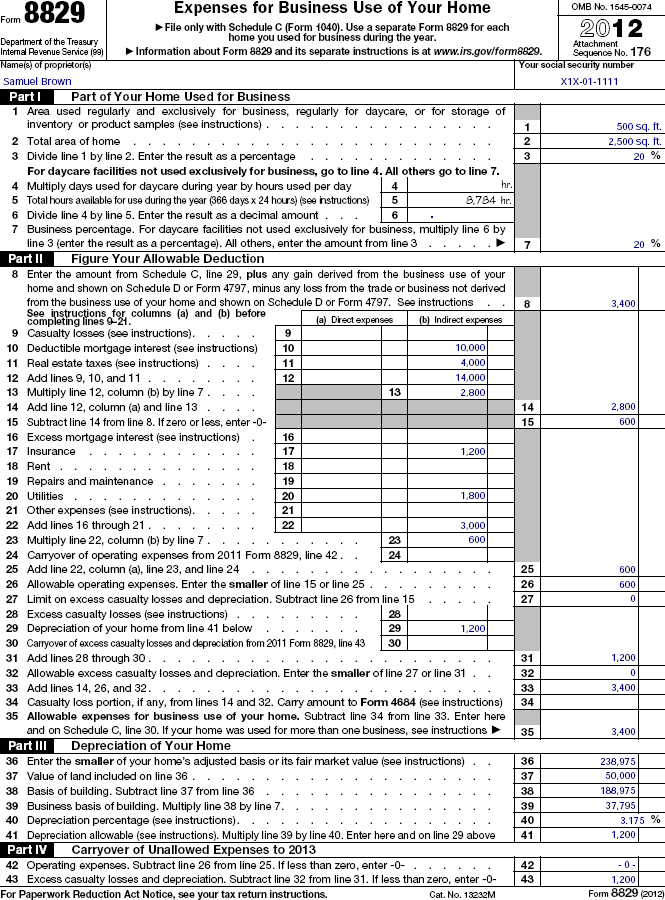

40.16 Home Office for Sideline Business

You may have an occupation and also run a sideline business from an office in your home. The home office expenses are deductible on Form 8829 if the office is a principal place of operating the sideline business or a place to meet with clients, customers, or patients. See the deduction tests (40.12) and the income limit computation (40.15) for home office deductions. Managing rental property may qualify as a business.

Managing your own securities portfolio.

Investors managing their own securities portfolios may find it difficult to convince a court that investment management is a business activity. According to Congressional committee reports, a home office deduction should be denied to an investor who uses a home office to read financial periodicals and reports, clip bond coupons, and perform similar activities. In one case, the Claims Court allowed a deduction to Moller, who spent about 40 hours a week at a home office managing a substantial stock portfolio. The Claims Court held these activities amounted to a business. However, an appeals court reversed the decision. According to the appeals court, the test is whether or not a person is a trader. A trader is in a business; an investor is not. A trader buys and sells frequently to catch daily market swings. An investor buys securities for capital appreciation and income without regard to daily market developments. Therefore, to be a trader, one’s activities must be directed to short-term trading, not the long-term holding of investments. Here, Moller was an investor; he was primarily interested in the long-term growth potential of stock. He did not earn his income from the short-term turnovers of stocks. He had no significant trading profits. His interest and dividend income was 98% of his income. See the discussion of trader expenses in 30.16.

-

No Comment