8.13 Mandatory Distributions From a Traditional IRA After Age 70½

The tax law requires that by April 1 of the year following the year in which you reach age 70½, you have to start receiving on an annual basis minimum distributions from your traditional IRAs under a schedule that meets IRS tests. The distributions will be fully taxable unless some of your IRA contributions were nondeductible (8.8). You cannot avoid tax on a required minimum distribution (RMD) by rolling it over to another account.

If you do not receive the required minimum amount, a penalty tax of 50% applies (unless the IRS waives it) to the difference between the amount that should have been received and the amount you did receive. For example, if you reach age 70½ in 2012, you may receive your first required minimum distribution (RMD) during 2012 or you may delay it until April 1, 2013, which is your “required beginning date.” Assume that, under the rules discussed below, your RMD for 2012 is $3,818, but you received only $3,000. Unless the IRS waives the penalty, you would have to pay a penalty of $409, 50% of the $818 shortfall.

If you are subject to a penalty, you should figure it on Form 5329, which must be attached to Form 1040. You can request a waiver of the penalty on Form 5329 if the failure to receive the proper amount was due to a reasonable error and you have or have or will make up for the shortfall; follow the Form 5329 instructions.

IRA owners and beneficiaries figure required minimum distributions (RMDs) differently.

The RMD rules for account owners of traditional IRAs are discussed in this section (8.13). Beneficiaries of traditional IRAs also must receive annual RMDs unless their entire share of the account is received by the end of the year after the year of the owner’s death. However, beneficiaries must use different rules to figure their RMDs (8.14).

Roth IRA owners (8.19) are not subject to RMD rules, but beneficiaries of Roth IRAs are (8.24).

Deadline for receiving your first required minimum distribution (RMD).

If you reach age 70½ in 2012, you must take your first RMD from your traditional IRA (the RMD for 2012) by April 1, 2013, your required beginning date, unless you received it during 2012. Your RMD for 2013 will have to be received by December 31, 2013, so if you delay your first RMD until early 2013 (but no later than April 1), you will have to take two distributions in 2013, one by April 1 and the other by December 31. This could substantially increase your 2013 taxable income. The RMD for 2014 and later years must be received by December 31 of that year.

If you reach age 70½ in 2013, you can take your first RMD (the RMD for 2013) during 2013 or delay it until April 1, 2014, your required beginning date. Your RMD for 2014 will have to be received by December 31, 2014.

Figuring Your Required Minimum Distribution (RMD)

The trustee or custodian of your traditional IRA must calculate the amount of your required minimum distribution or offer to do so. If you are required to receive a required minimum distribution (RMD) for 2012, the trustee or custodian should have reported the amount to you by January 31, 2012, or offered to calculate it upon your request. The calculation is based on final IRS regulations.

If you are required to receive an RMD for 2013, the IRA trustee or custodian must tell you by January 31, 2013 what your RMD is, or offer to calculate it for you upon your request.

To calculate the RMD for yourself, you can use Steps 1–3 below, which are based on the final IRS regulations.

If the IRA trustee or custodian calculates the RMD, the calculation may be based on the Uniform Lifetime Table (Table 8-3 below), which assumes that your beneficiary is 10 years younger than you are. However, if your sole beneficiary is your spouse who is more than 10 years younger than you, your RMD can be reduced by using the Joint Life and Last Survivor Expectancy Table (see Table 8-4). If this more-than-10-years-younger spousal exception applies and your IRA trustee or custodian does not use the Joint Life and Last Survivor Expectancy Table in calculating your RMD, you can do so yourself by calculating the RMD under Steps 1–3 below.

Table 8-3 Uniform Lifetime Table*

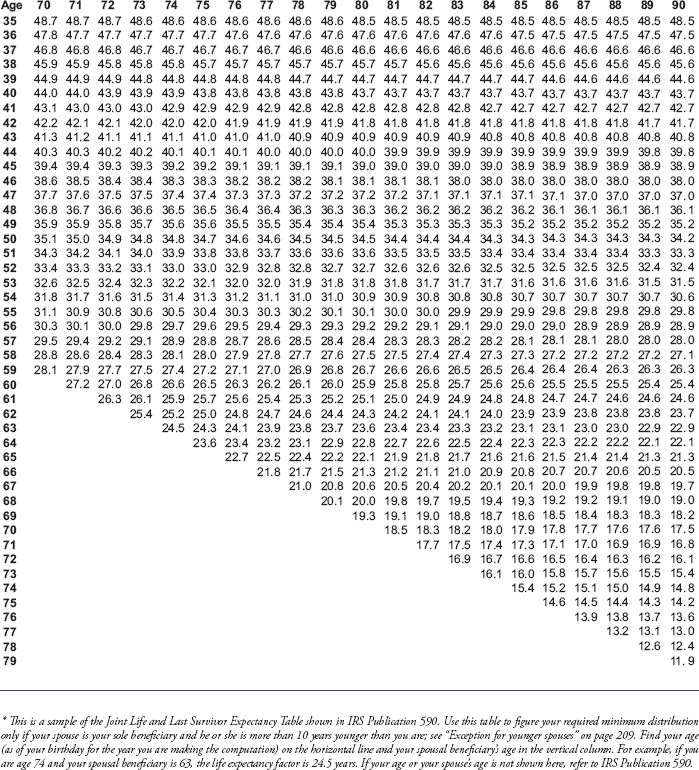

Table 8-4 Joint Life and Last Survivor Expectancy Table (for use by owners whose spouses are more than 10 years younger)*

Steps for figuring your required minimum distribution (RMD).

For each of your traditional IRAs, figure the required minimum distribution (RMD) you must receive using the following steps. Keep in mind that once you have separately determined the RMD for each IRA, the IRS allows you to withdraw the total RMD for the year from any of the accounts in any combination you choose.

Step 1: Find the account balance of your IRA as of the previous December 31.

If you reach age 70½ during 2012, the account balance to be used for figuring your first required minimum distribution (RMD) is the account balance for December 31, 2011, even if the actual distribution for 2012 is not made until the first quarter of 2013 (January 1–April 1).

The year-end account balance must be adjusted if toward the end of the year there is an outstanding rollover. For example, if in December of 2011 you withdrew funds from your IRA and you rolled the funds back to the same IRA or a different one within 60 days but not until early in 2012, the rollover amount must be included as part of the December 31, 2011 account balance of the receiving IRA, even though it was not actually in any account on that date.

Step 2: Divide the account balance (Step 1) by the applicable life expectancy.

Your life expectancy under the IRS rules is taken from the Uniform Lifetime Table unless your sole beneficiary is your spouse who is more than 10 years younger than you are. The Uniform Lifetime Table (Table 8-3) provides a joint life expectancy for you and a “deemed” beneficiary who is exactly 10 years younger than you are. Your beneficiary’s actual age does not matter. The life expectancy period from the uniform table applies even if you have not named a beneficiary as of your required beginning date (April 1 of the year after the year you reach age 70½). Furthermore, you continue to use the Uniform Lifetime Table even if you change your beneficiary or beneficiaries after starting to receive RMDs, unless the change results in the naming of your spouse as sole beneficiary for the entire year and you qualify to use the Joint Life and Last Survivor Expectancy Table (Table 8-4) because your spouse is more than 10 years younger than you are.

Your “deemed” life expectancy from the Uniform Lifetime Table is the number of years listed next to your age on your birthday in the year for which you are making the computation. For example, if you are figuring your RMD for 2012, and you are age 71 on your birthday in 2012, your life expectancy from the table, based on age 71, is 26.5 years. When you figure your RMD for 2013, you will use a life expectancy of 25.6 years, the life expectancy from the Uniform Lifetime Table for someone age 72.

Exception for younger spouses.

If the sole beneficiary of your IRA is your spouse and he or she is more than 10 years younger than you are, do not use the Uniform Lifetime Table to get your life expectancy for Step 2. Use the actual joint life expectancy of you and your spouse, which will allow you to spread out RMDs over an even longer period. See Table 8-4, which has a sample section of the Joint Life and Last Survivor Expectancy Table from IRS Publication 590.

This rule applies only if your spouse meets the age test and is the sole beneficiary of your entire interest in the IRA at all times during the calendar year for which the RMD is being figured. If your spouse is named beneficiary during the year or he or she is one of several beneficiaries on the account, the Uniform Lifetime Table must be used for that year. Your spouse would not meet the sole beneficiary test. However, if you are married on January 1 of a year and during the year you divorce or your spouse dies, you are considered married for the entire year and may use the spousal exception to figure that year’s RMD using the joint life table(Table 8-4).

If the exception for spousal beneficiaries applies, find your joint life expectancy from the IRS table corresponding to both of your ages on your birthdays for the year of the computation. For example, if you are age 71 on your birthday in 2012 and your spouse on his or her birthday is age 58, use a joint life expectancy of 28.6 years (see Table 8-4) to figure your RMD for 2012. This is longer than the 26.5-year distribution period provided by the Uniform Lifetime Table for a 71-year-old, which means that your RMD will be somewhat lower.

Step 3: If you have more than one IRA, total the required minimum distributions (RMDs) for all the accounts.

After separately figuring the required minimum distribution (RMD) for each of your IRAs under Step 2, total the amounts. This is the minimum you must receive for the year; you are, of course, free to withdraw more than that. Although you must calculate the RMD separately for each account, you do not have to make withdrawals from each of them. The total RMD from all accounts may be taken from any one account, or more than one account if you prefer. For example, if you have five bank IRAs, you may take the entire RMD from the bank where you have the largest balance, or from any other combination of banks; see Example 3 below. The entire distribution is taxable unless part is allocable to nondeductible IRA contributions (8.9).

| Step 1. | Account balance of $200,000 as of December 31, 2011. |

| Step 2. | Based on Joe’s age of 71 (as of his birthday in 2012), the life expectancy from the Uniform Lifetime Table (Table 8-3) is 26.5 years. The table assumes that Joe has a beneficiary who is age 61 (10 years younger than he is). The fact that his wife is age 63 does not matter. |

| Step 3. | Divide Step 1 by Step 2. |

| IRA-1: | The RMD is $3,774. This is the account balance of $100,000 divided by 26.5, the life expectancy from the Uniform Lifetime Table for a person age 71 (Cynthia’s age on her birthday in 2012). |

| IRA-2: | The RMD is $377, the account balance of $10,000 divided by 26.5, the life expectancy from the Uniform Lifetime Table, using age 71. |