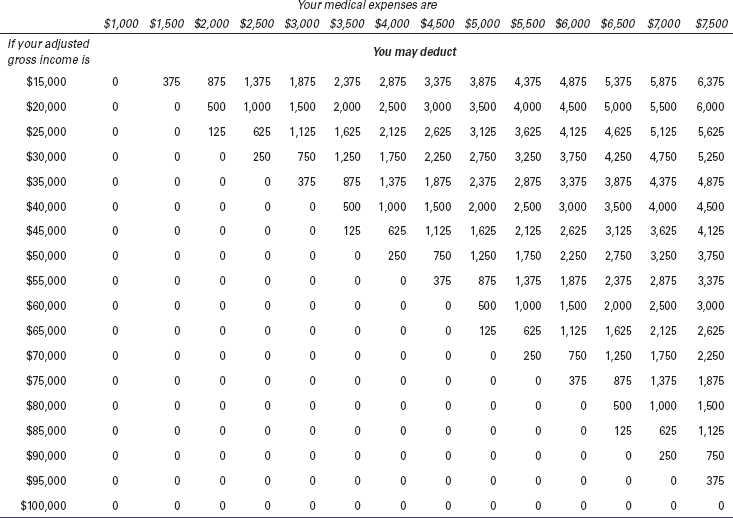

17.2 Allowable Medical Care Costs

In determining whether you have paid deductible medical expenses exceeding the 7.5% AGI floor (17.1), include the cost of diagnosis, cure, mitigation, treatment, or prevention of disease, or any treatment that affects a part or function of your body (Table 17-1). Also include qualifying costs you paid for your spouse (17.6) and your dependents (17.7).

Expenses that are solely for cosmetic reasons are not deductible. Also, expenses incurred to benefit your general health are not deductible even if recommended by a physician (17.3).

Medicine and drugs.

To be deductible, medicines and drugs other than insulin must be obtainable solely through a prescription by a doctor. Insulin is deductible even though a prescription may not be required. You may not deduct the cost of over-the-counter medicines and drugs, such as aspirin and other cold remedies, even if you have a doctor’s prescription.

Marijuana is not deductible even if prescribed by a doctor in a state allowing the prescription.

A prescribed drug brought in or shipped into the U.S. from another country is not deductible unless the FDA (Food and Drug Administration) allows that drug to be legally imported by individuals.

Diagnostic tests.

The IRS treats unreimbursed diagnostic procedures as deductible medical expenses (subject to the 7.5% of AGI floor), even if you had no symptoms of illness and you underwent the test without a physician’s recommendation. For example, the cost of an annual physical performed by a doctor and related laboratory tests is a medical expense, whether or not you were feeling ill. Similarly, a full body scan is a deductible diagnostic procedure, whether or not a physician recommended it. Where a procedure does not have a nonmedical function, a physician’s recommendation is not necessary. It also does not matter if a less expensive alternative to the full body scan is available. Finally, a home pregnancy test qualifies as a medical expense even though its purpose is not to detect disease but to test for the healthy functioning of the body.

Vitamins and nutritional or herbal supplements.

The IRS does not allow a deduction for the cost of vitamins, nutritional or herbal supplements, or “natural” medicines unless a medical practitioner recommends them as treatment for a specific medical condition diagnosed by a physician. Otherwise, they are considered to be for maintaining your general health rather than for medical care.

Stop-smoking programs.

The cost of smoking cessation programs is a deductible medical expense, as well as nicotine withdrawal drugs that require a physician’s prescription. Over-the-counter nicotine patches and gums are not deductible.

Exercise and weight-reduction programs.

If you incur costs for such programs to improve your general health, the costs are not deductible even if your doctor has recommended them. However, if your doctor has recommended a program as treatment for a specific condition, such as heart disease or hypertension, the IRS allows a deduction for the cost.

The IRS considers obesity a disease. If a physician has made a diagnosis of obesity, the costs of joining a weight-loss program and additional fees for meetings are eligible medical expenses. However, reduced-calorie diet foods that are substitutes for foods normally consumed are not deductible even if they are part of the program; see “Special foods” below.

Special foods.

The IRS position on deducting the cost of “special foods” is unclear. The IRS has long taken the position in Publication 502 that the excess cost of special foods or beverages over a regular diet is not a deductible medical expense if the special foods “satisfy normal nutritional needs”, even if a physician substantiates that a special diet is needed to alleviate or treat an illness. This IRS position not only bars a deduction for low-calorie foods, on the grounds that they substitute for a “normal” diet, but it could also block a deduction for diets required to deal with conditions such as Celiac disease. Although gluten-free foods may have a clear medical purpose as diagnosed by a physician, such foods obviously “satisfy normal nutritional needs” and so for that reason the IRS could deny a deduction for the excess cost.

In response to public pressure, the IRS informally suggested that it might change the language of Publication 502 and follow the standard used by the Tax Court, which allows a deduction for the excess cost of a special diet over ordinary food provided the medical need for it is established by a physician; see the Examples below. However, when this book went to press, the IRS had not eliminated its “normal nutritional needs” restriction.

Table 17-3 Nondeductible Medical Expenses

Infant formula.

Applying its “nutritional needs” test, the IRS in a private ruling denied a mother’s deduction for the cost of infant formula for her healthy child. Although the mother had a medical reason for buying the formula—she was unable to breastfeed her baby following a double mastectomy—the formula was food satisfying the child’s ordinary nutritional needs, and therefore was a nondeductible personal expense.

Portion of monthly service fees paid to retirement community.

The portion of the monthly fees that is allocable to medical care is a deductible medical expense (34.10).

Advance payment for lifetime care in retirement community.

If you pay a life-care fee or “founder’s fee” either monthly or in a lump sum to a retirement community, the portion allocable to future medical care may be included as a current medical expense (34.10).

Advance payments for lifetime care of disabled dependent.

You can treat as a current medical expense a nonrefundable advance payment to a private institution for the lifetime care and treatment of your physically or mentally impaired child upon your death or when you become unable to provide care. The nonrefundable payment must be a condition for the institution’s future acceptance of your child.