CHAPTER 3

The Eurodollar Futures Contract

Eurodollar futures contracts were first listed by the Chicago Mercantile Exchange (a.k.a. CME or “Merc”) in December 1981. They were followed in 1982 by the London International Financial Futures Exchange (now the London International Financial Futures and Options Exchange, LIFFE) and in 1984 by the Singapore International Monetary Exchange (SIMEX; now the Singapore Exchange, SGX).1

Today, only the CME and SGX are major players in Eurodollar futures. The contract is traded via open outcry at the CME and SGX and electronically via the CME’s GLOBEX system. With the exception of trading hours, the contracts traded at the CME and SGX are identical.

The purpose of this chapter is to introduce Eurodollar futures by covering:

• Contract specifications

• Performance bonds

• Volume and open interest

We also highlight several non-dollar 3-month money market futures.

CONTRACT SPECIFICATIONS2

The Eurodollar futures contract specifications are described below and summarized in Exhibit 3.1.

EXHIBIT 3.1

Eurodollar Futures Contract Specifications

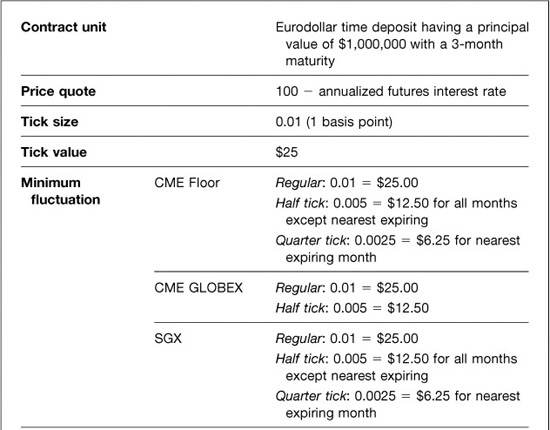

Contract Unit

The contract unit is $1,000,000 3-month Eurodollar time deposits.

Price Quote

Bids and offers are quoted in terms of the IMM (International Monetary Market) index, or 100.00 minus the yield on an annual basis for a 360-day year. For example, a deposit rate of 3.25 will be quoted as 96.75 [= 100.00 − 3.25].

Tick Size

The basic tick size is 0.01 (or 1 basis point, often represented by bp). The dollar value of a tick is $25, which accords with the change in the value of a 90-day $1,000,000 instrument.

Minimum Fluctuation

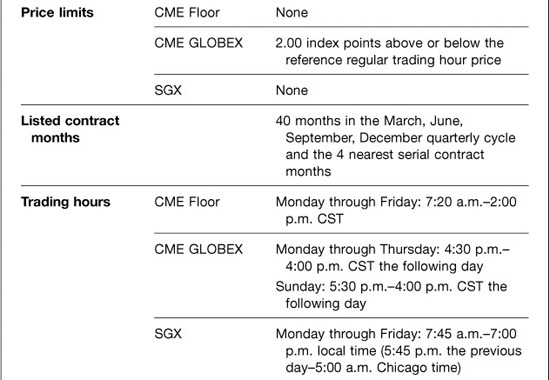

The nearest expiring contract month trades in quarter ticks or 0.0025 ($6.25). The minimum price fluctuation for all other contracts is a half tick or 0.005 ($12.50).

Listed Contract Months

Each Eurodollar futures contract represents a 3-month deposit rate beginning some time in the future. Eurodollar futures contracts trade out 10 years in the quarterly cycle and have expirations in March, June, September, and December. Four serial contracts with expirations outside of the quarterly cycle also trade. Serial contract months include January, February, April, May, July, August, October, and November. For example, during June, the 44 listed contracts include the 40 quarterly contracts plus the 4 serial contracts in July, August, October and November.

March, June, September, and December. Four serial contracts with expirations outside of the quarterly cycle also trade. Serial contract months include January, February, April, May, July, August, October, and November. For example, during June, the 44 listed contracts include the 40 quarterly contracts plus the 4 serial contracts in July, August, October and November.

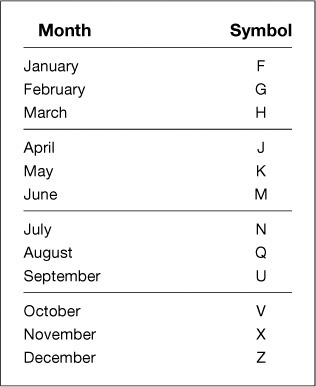

Contract Month Symbols

Each Eurodollar futures contract is identified by its month and year. The futures market has created symbols to represent each month (see Exhibit 3.2).

EXHIBIT 3.2

Contract Month Symbols

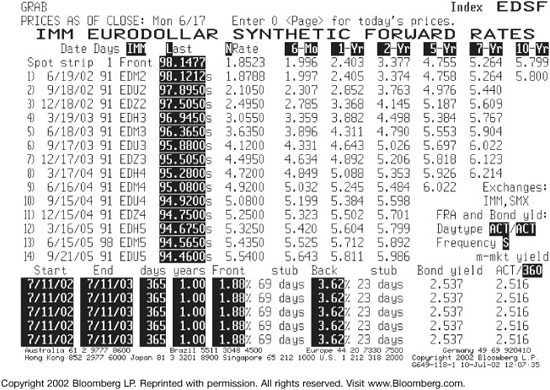

For example, the contract that expires in September 2003 is often represented as EDU3, where ED represents Eurodollar futures, U represents September, and 3 represents the last digit of the year. Bloomberg makes use of the contract month symbols in its EDSF function, which displays Eurodollar futures prices for each of the 40 quarterly expirations. (Exhibit 3.3 shows the first EDSF screen, with 14 Eurodollar futures contracts.)

EXHIBIT 3.3

Bloomberg EDSF Function Prices for June 17, 2002

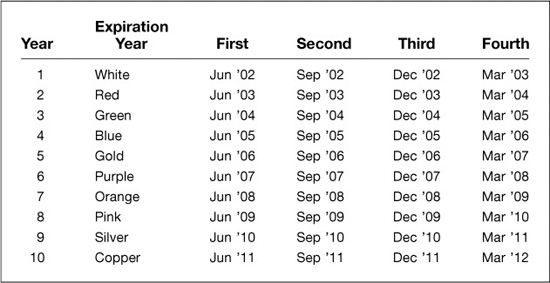

Color-Coded Grid

With 10 years of contracts, the market has also come up with creative ways to indicate groups of contracts. The CME defines expiration years in terms of a color-coded grid, with 4 quarterly cycle contract expirations per color (see Exhibit 3.4). For example, the first 4 quarterly contracts make up the “whites.” As of June 12, 2002, this would be the June 2002, September 2002, December 2002, and March 2003 contracts. The next 4 quarterly contracts make up the “reds.” The next 4 contracts make up the “greens” and so on.

EXHIBIT 3.4

Contract Year Color Grid As of June 12, 2002

This color-coded grid also allows traders to describe a specific part of the yield curve. For example, the “third red,” as shown in Exhibit 3.4, represents a 3-month deposit rate between 1-1/2 to 1-3/4 years in the future, depending on how soon the lead contract expires.

Expiring versus Lead Contract

Market terminology can be confusing at times. For example, people often use the phrases “expiring contract” and “lead contract” interchangeably. This is not correct. The expiring contract is the one that is nearest to futures expiration. The lead contract is the most active contract and is designated as the lead contract by its location on the floor of the exchange. The expiring contract and the lead contract may or may not be the same.

Trading Hours and Mutual Offset

Since 1984, the Chicago Mercantile Exchange and the Singapore Exchange have used a mutual offset system (MOS) to create a trade linkage between the two exchanges. The mutual offset system allows a trade executed at the CME to be transferred to SGX or a trade executed at SGX to be transferred to the CME. This offset is possible because the Eurodollar futures contracts on the two exchanges are fungible.

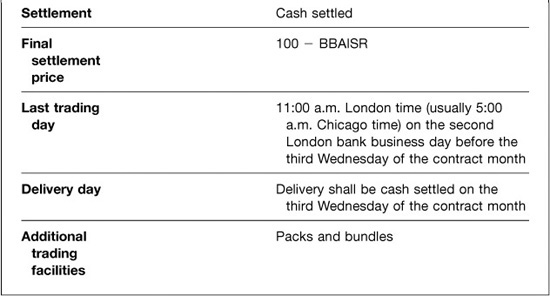

Final Settlement Price

The Eurodollar futures contract is cash settled to a final settlement price that is tied to spot 3-month LIBOR. The final settlement price is 100 minus the British Bankers’ Association Interest Settlement Rate (BBAISR) for 3-month Eurodollar interbank time deposits, rounded to the nearest 1/10,000th of a percentage point, on the second London bank business day immediately preceding the third Wednesday of the contract month.

In order to calculate the BBAISR, the British Bankers’ Association selects 16 reference banks, all of whom are major participants in the London Eurodollar market, and asks them to provide rates at which they could borrow U.S. dollars through the interbank market. The quotes are rank ordered and the middle two quartiles are arithmetically averaged for the fixing. The fixing is conducted at 11 a.m. London time.

Last Trading Day

The Eurodollar futures contract terminates trading at 11:00 a.m. London time on the second London bank business day immediately preceding the third Wednesday of the contract month. This is 5:00 a.m. Chicago time, except when daylight savings time is in effect in either, but not both, London or Chicago.

From a practical perspective, the last day of trading on the CME floor is the third business day immediately preceding the third Wednesday of the contract month. Barring holidays, this is the Friday preceding expiration. The contract is last traded on GLOBEX at 11:00 a.m. London time (usually 5:00 a.m. Chicago time) on the day of Eurodollar futures expiration.

Value Dates

The value dates for Eurodollar futures fall 2 London business days after contract expiration. This is because the contract is settled to 3-month LIBOR, which has a 2-day settlement period. Eurodollar futures value dates always fall on the third Wednesday of the contract month.

Additional Trading Facilities

Market participants often want to execute a series of Eurodollar futures contracts in order to target specific segments of the yield curve. Rather than execute each contract month individually and incur execution risk, packs and bundles can be used to execute all of the desired contract months in a single transaction.

Packs are the simultaneous purchase or sale of an equally weighted, consecutive series of 4 Eurodollar futures, quoted on an average net change basis from the previous day’s close. All packs trade in quarter ticks.

Bundles also involve the simultaneous purchase or sale of a consecutive series of Eurodollar futures contracts, but bundles have maturities of 1, 2, 3, 4, 5, 6, 7, 8, 9, and 10 years. The first contract in a bundle is generally the first quarterly contract. An exception to this is the 5-year forward bundle, which covers years 5 through 10 of the Eurodollar futures strip. All bundles trade in quarter ticks.

“Rolling” packs and bundles allow market participants to execute packs and bundles with “non-standard” start dates. Consequently, market players can trade packs and bundles that start with any quarterly contract. For additional information on packs and bundles, see “Hedging and Trading with Eurodollar Stacks, Packs, and Bundles,” chapter 13.

INITIAL AND MAINTENANCE PERFORMANCE BONDS

The financial integrity of a futures exchange is ensured by its clearing house. The clearing house is responsible for settling trading accounts, clearing trades, collecting and maintaining performance bond funds, requiring delivery, and reporting trade data. Clearing firms stand between the customers and the clearing house. A customer who wishes to trade Eurodollar futures, or any other futures for that matter, is required to deposit funds known as initial performance bond (or initial margin) with his or her clearing firm.

On a daily basis, the customer’s position is marked to market and gains or losses are posted to the customer’s performance bond account. If the customer’s funds drop below the maintenance performance bond level, the clearing firm will demand additional funds from the customer to bring the level back to the initial performance bond amount. This call for additional funds is known as a performance bond call (previously, a margin call). Exhibit 3.5 shows a summary of how Eurodollar futures work.

EXHIBIT 3.5

How Eurodollar Futures Work

VOLUME AND OPEN INTEREST

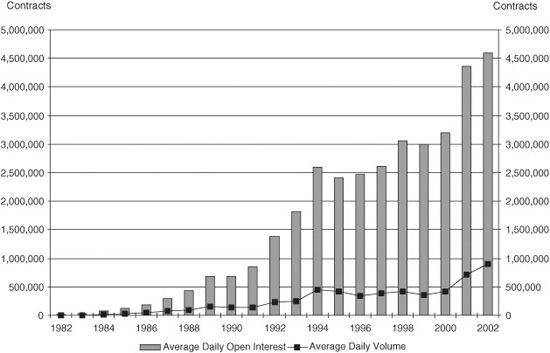

The growth of trading and open interest in Eurodollar futures at the CME is chronicled in Exhibit 3.6. What began as a contract trading in the shadows of Treasury bill and CD futures has grown to gigantic proportions. At this writing (June 2002), open interest in all contract months combined was over 4.5 million. At $1 million notional amount per contract, this translates into open positions on the books of traders and hedgers that are the equivalent of more than 4.5 trillion of 3-month deposits. This is big money.

EXHIBIT 3.6

Eurodollar Futures Volume and Open Interest 1982 through June 2002

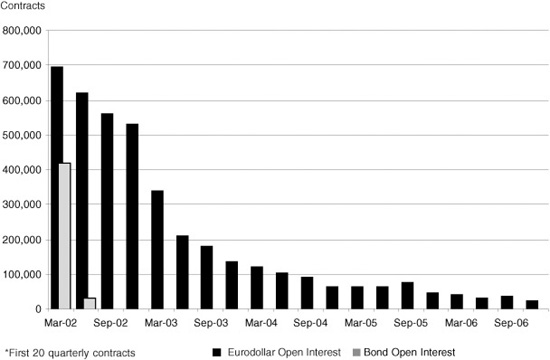

Part of the reason for the success of the contract is illustrated in Exhibit 3.7, which compares the open interest across contract months in Eurodollar and Treasury bond futures. Nearly all of the open interest in bond futures is concentrated in the first 2 months. In contrast, there is substantial open interest in back-month Eurodollar futures.

EXHIBIT 3.7

Bond and Eurodollar* Futures Open Interest by Contract Year-End 2001

Eurodollar futures differ from bond futures in one other key respect. The ratio of daily trading volume to open interest in bond futures is often more than one-to-one. In contrast, the ratio of daily trading volume to open interest in Eurodollar futures is much lower, around one-to-five. Stated differently, the open interest in bonds turns over once a day on average. The open interest in Eurodollars turns over only once a week.

What this suggests is that Eurodollar futures are a hedger’s contract, while Treasury bond futures are much more akin to a trader’s contract. This fits what we already know about Eurodollar futures. The growth in the contract has been driven by the flexibility it affords in shaping and hedging interest rate exposure at the short end of the yield curve. It is no accident that the market for back-month Eurodollar futures has kept pace with the burgeoning interest rate swap market.

OTHER 3-MONTH MONEY MARKET FUTURES CONTRACTS

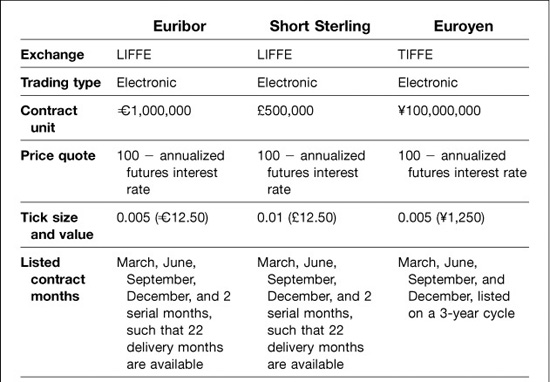

The success of the CME’s Eurodollar futures contract led other exchanges to create 3-month deposit futures. There were PIBOR futures on French deposit rates; Euro lira futures on Italian deposit rates; EuroDM futures on German deposit rates; and MIBOR futures on Spanish rates. With the introduction of the Euro (=€) as the currency of the European Economic and Monetary Union, these money market contracts were superseded by Euribor futures. Other active 3-month deposit futures include Short Sterling futures on British deposit rates and Euroyen futures on Japanese rates. Exhibit 3.8 shows the contract specifications for some of these actively traded contracts.

EXHIBIT 3.8

Other 3-Month Money Market Futures Contract Specifications