CHAPTER 16

Trading the Turn: 1993

SYNOPSIS

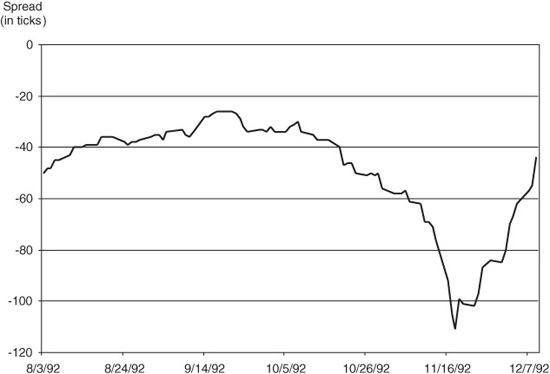

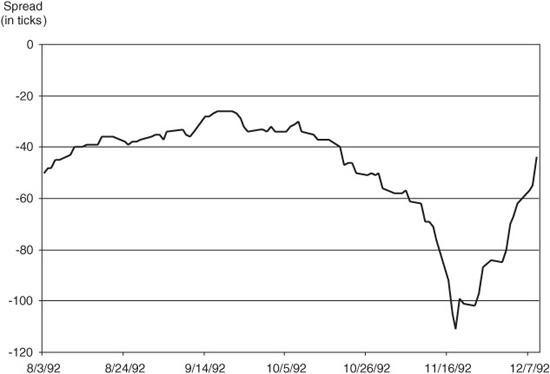

The last time there was any serious pressure on year-end financing rates was 1986. Even so, the memory lives on, and “the turn” still has an effect on people’s thinking about the way they finance positions over year end. Exhibit 16.1, for example, shows a huge change last November in the spread between the December ′92 and January ′93 LIBOR contracts. Given the rules of thumb developed in this note, the 60-tick drop in the spread suggests that the market briefly expected a 500-basis-point increase in the turn premium.

EXHIBIT 16.1

LIBOR Futures Calendar Spread December 1992/January 1993

“The turn” is a 2-, 3-, or 4-day period from the last business day of one year through the first business day of the next. Just how many days the turn contains depends on where the New Year’s holiday falls and how it is treated. This year (i.e., 1993), the turn will be unusual because it will be 3 days for some banks and 4 days for others. In the United States, for example, the turn is just like any other weekend for most U.S. banks. The Fed wire is open on both Friday, December 31, and on Monday, January 3, so that any financing done over year end will be done for 3 days. In the United Kingdom on the other hand, Monday the 3rd is a holiday so that London banks will have to choose between financing their positions for 4 days and arranging for their U.S. branches (for those that have them) to do their financing for 3 days over the turn and then for 1 day at the overnight rate.

The effect of all this on the December LIBOR and Eurodollar contracts will depend on how banks reconcile these differences. The final settlement prices of these two contracts will depend on the December 13 values of 1-month and 3-month LIBOR, which will be quoted by London banks for whom the turn is a 4-day event. As things now stand, many banks are quoting both 3-day and 4-day turn rates, and as the distinction between the two becomes clear to all market participants, competitive forces should cause the 4-day turn rate to be nothing more than a simple weighted average of the 3-day turn rate and a regular 1-day overnight rate. In this note, therefore, we treat the turn as if it is a 3-day event. This seems compatible with the way banks that are aware of the different holiday schedules are treating year-end financing.

In any case, people’s understanding of the turn has been sufficiently clouded by misunderstandings about year-end holiday schedules that everyone with an interest in the event should take special care when quoting turn rates and arranging year-end financing.

WHAT IS “THE TURN”?

“The turn” is the period of time between the last business day of the current calendar year and the first business day of the new year. Because New Year’s Day is a holiday, the number of days in the turn is at least 2 calendar days and can be 3 or 4.

Two-Day Turns

The turn lasts 2 days if December 31 falls on a Monday, Tuesday, or Wednesday. In each of these cases, the next calendar day is a holiday so that money borrowed on Monday would be paid back on Wednesday, 2 days later. Money borrowed Tuesday is paid back Thursday, and money borrowed Wednesday is paid back Friday.

Three-Day Turns

This year, the turn lasts 3 days because December 31 falls on a Friday and the Fed wire is open on both Friday and on the following Monday, January 3. Similarly, if December 31 fell on a Saturday so that January 1 is on Sunday, the turn likely would last 3 days as well, although the Fed wire might be closed on Monday. If it were, the turn would last 4 days.

Four-Day Turns

The turn lasts 4 days if December 31 falls on either a Thursday or a Sunday. In either of these cases, any money borrowed on the last business day of the year must be kept for 4 days. For example, if December 31 is on Thursday, money borrowed then is paid back on Monday, the 4th, or 4 days later. Similarly, if December 31 is on Sunday, money borrowed on Friday the 29th is paid back on Tuesday the 2nd.

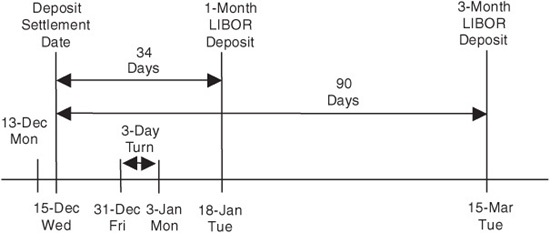

Exhibit 16.2 shows a time line of the turn for the end of 1993. The last business day is Friday, the 31st. A bank looking to borrow overnight funds on Friday would normally repay those funds the following Monday, which is the next business day. In this respect, this year’s turn is just like a normal weekend. New Year’s Day falls on Saturday, and the Fed wire is open for business as usual on Monday, the 3rd.

EXHIBIT 16.2

Time Line for the 1993 Turn

Turn financing rates can be obtained both in the forward deposit market and in the FRA (forward rate agreement) market. At this writing, the markets are still thin and rate indications seem to depend heavily on the nationality of the counterparty. For U.S. banks, the turn premium is very small, while for European and Japanese banks, turn financing rates are offered around 9 to 10 percent, which implies turn premiums in the neighborhood of 5 to 6 percent.

RATE BEHAVIOR AROUND THE TURN

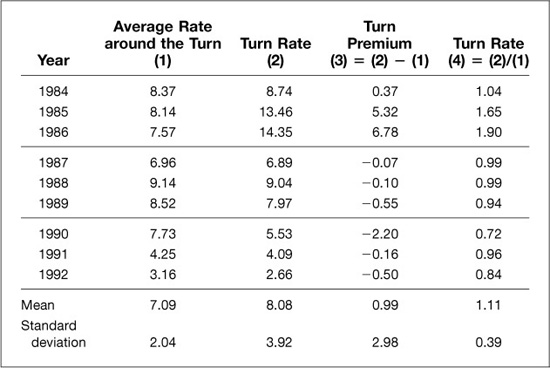

The turn has gained notoriety among bankers because of the pressures that have, in years past, been brought to bear on year-end financing rates. The source of this pressure is said to be the demand by banks for cash that can be used to dress up their balance sheets at the end of the calendar year. Although the Federal Reserve does what it can to accommodate this year-end increase in demand for liquid balances, and does an excellent job most of the time, it appears to have misjudged the size of the shift at least twice since 1984.

As shown in Exhibit 16.3, the turn rate and the average rate around the turn appear to have been fairly close to one another in most of the past 8 years. In 1984, for example, normal financing rates during the 5 days before and after the turn were around 8.37 percent. For the turn between 1984 and 1985, the turn rate increased to 8.74 percent, for a turn premium of 0.37 percent. The “turn ratio,” which is simply the ratio of the turn rate to the non-turn rate and which we will use later when we examine the effect of the turn on rate volatility, was only 1.04.

EXHIBIT 16.3

Fed Funds Behavior around Year-End

At the end of 1985, however, the turn premium was more than 5 percentage points, and at the end of 1986 the turn premium was nearly 7 percentage points. The effect of such large turn premiums on year-end financing costs must have had a riveting effect on bankers at the time. The effect of a 7-percentage-point turn premium on the cost of funding $1 billion over year end, even for a turn period as short as 2 days, is $389 thousand. This is serious money in anybody’s book.

Since 1986, realized rate behavior around the turn has been unremarkable. Even so, the possibility of a large premium still looms large, and wide swings in the market’s expectations about turn financing rates can have dramatic effects on forward deposit rates. In late November 1990, for example, fear of extreme pressure on year-end financing rates greatly depressed both December LIBOR and Eurodollar futures prices for about a week.

EFFECTS ON EURODOLLAR AND LIBOR FUTURES PRICES

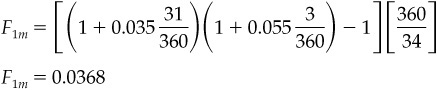

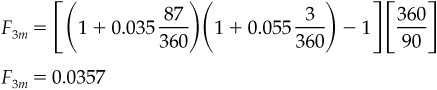

Because the 1-month LIBOR and 3-month Eurodollar futures contracts that expire in December settle to deposit rates that span the end of the year, changes in the turn rate affect the final settlement value of these two contracts. This year, for example, the December LIBOR and Eurodollar contracts expire on December 13. The final settlement price of the 1-month LIBOR contract on that day will be 100 − R1m, where R1m is the 1-month deposit rate on December 13 for the 34-day deposit period that runs from Wednesday, December 15, through Tuesday, January 18. (See Exhibit 16.4.) The final settlement price of the 3-month Eurodollar contract will be 100 − R3m, where R3m is the 3-month deposit rate on December 13 for the 90-day period that runs from December 15 through Tuesday, March 15.

EXHIBIT 16.4

How the Turn Fits In

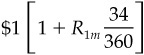

The relationship between the turn rate and the deposit rates to which the LIBOR and Eurodollar futures contracts will settle can be determined by comparing two borrowing transactions. In the first, money is borrowed for the full term at a term lending rate. In the second, money is borrowed in three legs—one that runs from December 15 through December 30, one that runs from December 31 through January 3, and one that runs from January 4 through the end of the term. Under the first strategy for borrowing 1-month money, one dollar borrowed on December 15 would call for

to be repaid on January 18. Under the second strategy, one dollar borrowed on December 15 would require a repayment of

where Rb, Rt, and Ra are the rates that apply to the days before, during, and after the turn and where Db, Dt, and Da are the actual number of days in the periods before, during, and after the turn. For a bank financing a position over this period to be indifferent between the two strategies, the two amounts of money must be the same. If we collapse the rates before and after the turn into a single, non-turn deposit rate, the two strategies cost the same if

The 3-month term deposit rate can be expressed the same way. The only difference is that the non-turn rate for the 90-day period would be different from the non-turn rate for the 34-day period.

To get a sense of how large an effect the turn can have on December LIBOR and Eurodollar futures prices, suppose first that the turn and non-turn rates are the same, say 3.50 percent. In this case, both 1-month and 3-month deposit rates would be (except for a trivial amount of compounding) 3.50 percent. December LIBOR and Eurodollar futures prices would both be 96.50 [= 100.00 − 3.50].

Suppose now that the turn rate increases 200 basis points to 5.50 percent, while the non-turn rate stays at 3.50 percent. At these rates, and given the day counts shown in Exhibit 16.4, the 1-month forward deposit rate for December 13 would be

which is 18 basis points higher than the 1-month forward rate with the turn rate at 3.50 percent. The 3-month or 90-day forward deposit rate would be

which is 7 basis points higher than the 3-month forward rate with the turn at 3.50. At these rates, the fair value of the December LIBOR contract would be 96.32 [= 100.00 − 3.68], and the fair value of the December Eurodollar contract would be 96.43 [= 100.00 − 3.57]. Thus, the effect of a 200 basis point spread between the turn and non-turn rates is to decrease the fair value of the December LIBOR contract by 18 basis points and the fair value of the December Eurodollar contract by 7 basis points.

Although the effect of any given turn/non-turn rate spread on the fair value of the December LIBOR and Eurodollar futures contracts depends to some extent on the actual number of days in the forward periods and on the level of rates, we have what we need for excellent working rules of thumb.

Rule of Thumb for a 4-Day Turn

With a 4-day turn, the effect of each 100-basis-point increase in the spread between the turn and non-turn forward deposit rates is a 12-tick decrease in the fair value of the December LIBOR contract and just over a 4-tick decrease in the fair value of the December Eurodollar contract.

Rule of Thumb for a 3-Day Turn

With a 3-day turn, the effect of each 100-basis-point increase in the spread between the turn and non-turn forward deposit rates is a 9-tick decrease in the fair value of the December LIBOR contract and just over a 3-tick decrease in the fair value of the December Eurodollar contract.

Rule of Thumb for a 2-Day Turn

With a 2-day turn, each 100-basis-point increase in the spread between the turn and non-turn forward deposit rates reduces the fair value of the December LIBOR contract by about 6 ticks and the fair value of the December Eurodollar contract by just over 2 ticks.

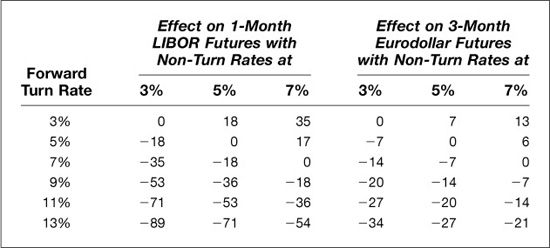

These rules of thumb are borne out by Exhibit 16.5, which shows the effect of various rate spreads on the fair value of both the December LIBOR and Eurodollar futures contracts given a 3-day turn. For example, if the non-turn forward deposit rate were 3 percent and the turn rate were 9 percent, the effect of the 600-basis-point spread would be a 53-tick reduction in the fair value of the December ′93 LIBOR futures contract. The same spread would produce a 20-tick reduction in the fair value of the December ′93 Eurodollar futures contract. Because the effect of the turn rate is roughly proportional to the length of the turn, the effects of these rate spreads on the fair values of the LIBOR and Eurodollar futures contracts given 2-day and 4-day turns can be determined easily enough from the figures shown in Exhibit 16.5.

EXHIBIT 16.5

Effect of Turn Rate on the Fair Values of Dec ′93 LIBOR and Eurodollar Futures Prices (3-Day Turn)

Implied Turn Rates

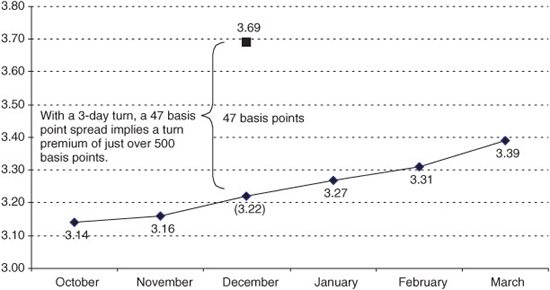

With these rules of thumb, it is easy to get a reading on the spread between turn and non-turn rates by looking at the pattern of rates implied by the 1-month LIBOR contracts, which have serial expirations extending out 6 months at any one time. On September 13, for example, there were 1-month LIBOR futures with expirations ranging from October 1993 through March 1994, not counting the expiring September 1993 contract. Exhibit 16.6 shows the strip of 1-month forward deposit rates implied by their September 13 settlement prices. The effect of the turn on the pattern of rates stands out clearly in this exhibit. The 1-month deposit rate for the November contract, which spans the period from mid-November to mid-December, was 3.16 percent. The 1-month deposit rate for the January contract, which spans the period from mid-January to mid-February, was 3.27 percent. In between, the 1-month deposit rate for the December contract was 3.69 percent, which was about 47 basis points higher than the 3.22 percent that the surrounding rates would suggest for a 1-month December deposit rate.

EXHIBIT 16.6

Implied 1-Month Forward Deposit Rates September 13, 1993

From this 47-basis-point differential, we can determine the spread between turn and non-turn financing rates that is implied by the LIBOR futures contract. Using the rule of thumb that each 100 basis points in the spread reduces the fair value of the December LIBOR contract by about 9 basis points, the 47-basis-point differential that we see in the December contract implied a spread of just over 500 basis points between the turn and non-turn rates.

This implied rate spread can be compared easily with the spreads quoted in the forward deposit market as a way of comparing the pricing of the turn in the two markets. If you find, for example, that the implied turn rate differential is larger than the actual, then you know that the December LIBOR contract is cheap relative to cash.

IMPLICATIONS FOR FUTURES SPREADS

Because the turn rate affects both the December LIBOR and Euro-dollar futures contracts, it affects the values of several key futures spreads including the:

December LED Spread

In this spread, you are long the LIBOR contract and short the Eurodollar contract. Given the rule of thumb for a 3-day turn, each 100-basis-point increase in the turn premium translates roughly into a 6-tick decrease in the value of this spread. Thus, the December LED spread is about 30 ticks lower than it would be if the turn premium were zero.

December/January LIBOR Spread

In this spread, you are long the December and short the January LIBOR contracts. Because the turn premium affects only the December contract, each 100-basis-point increase in the turn premium is worth about 9 ticks in this spread. As shown in Exhibit 16.6, this spread is 47 or so ticks lower than it would be if there were no turn premium.

December/March Eurodollar Spread

Here you are long the December and short the March Eurodollar contracts, and with a 3-day turn, each 100-basis-point increase in the turn premium decreases the value of this spread by about 3 ticks.

December TED Spread

In this spread, you are long the 3-month December Treasury bill contract and short the December Eurodollar contract. Because you are short the Eurodollar contract, each 100-basis-point increase in the turn premium increases the value of this spread by about 3 ticks.

One can work out similar implications for the Nov/Dec/Jan LIBOR butterfly and for the December/March TED tandem as well.

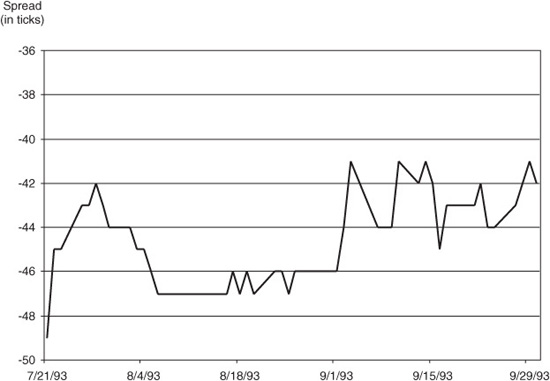

Of the various spreads, the December/January LIBOR spread is one of the better vehicles for trading the turn because the effect of the turn premium on the December contract price is both large and fairly direct, and the calendar risk in the trade is about as small as it can be without actually trading the cash deposits themselves. If the turn premium falls to zero by the time the December LIBOR contract expires on the 13th, a long position in the spread would gain 47 ticks, or $1,175 per spread. Exhibit 16.7 shows how this spread behaved last year, and Exhibit 16.8 shows how the spread has performed so far this year.

EXHIBIT 16.7

LIBOR Futures Calendar Spread December 1992/January 1993

EXHIBIT 16.8

LIBOR Futures Calendar Spread December 1993/January 1994

The dangers in this spread are three. One is that the turn rate is not realized until 2 or 3 weeks after the December contract expires. A second is that there is considerable fluctuation in the market’s perception of the turn premium throughout the months leading up to the end of the year. A third is that you are exposed to a flattening of the near-term yield curve.

The other spreads may be less attractive for trading the turn premium, but the effect of the turn on these spreads certainly cannot be ignored when evaluating trades that involve them. The December TED spread, for example, as well as the December/March TED tandem, are greatly influenced by the turn premium. With an implied turn premium of around 500 basis points, December Eurodollar futures trade 15 ticks or so lower than they would without the turn. Thus, we know that about 15 ticks of the current December TED spread can be attributed to the turn.

By the same token, the December/March Eurodollar calendar spread is 15 ticks lower than it would be without the turn.

EFFECT OF THE TURN ON LIBOR AND EURODOLLAR VOLATILITIES

Uncertainty about financing rates over the turn is an additional source of volatility for the 1-month and 3-month deposit rates to which the December LIBOR and Eurodollar futures contracts will settle. The focus of this section is on how best to determine the effect of turn-rate volatility on the volatilities for options on December LIBOR and Eurodollar futures.

The biggest hurdle to reckoning the effect of turn-rate volatility on LIBOR and Eurodollar volatilities is the problem of how to represent turn-rate volatility. The few observations that we have on the turn, which are shown in Exhibit 16.3, suggest fairly strongly that turn rates are not lognormally distributed. With so few observations, however, we only have what we think are two reasonable guides to choosing an alternative distribution. The first is that the size of the turn rate premium should be related to the level of interest rates. The second is that the chance of getting a huge turn premium should be fairly large even though most turn premiums will be close to zero.

One way to satisfy the first reasonableness check is to allow the ratio of the turn rate to the non-turn rate to be the random variable so that the turn premium is directly proportional to the level of rates. For example, a turn/non-turn ratio of 1.5 would produce a turn rate of 9 percent if base rates were 6 percent. If the base rate were 3 percent, the turn rate would be 4.5 percent. The turn premium in the first case would be 3 percent, while the turn premium in the second case would be 1.5 percent.

We can satisfy the second reasonableness check by allowing the behavior of the ratio of turn to non-turn rates to be described by the gamma distribution, which has fat enough tails to allow for a comparatively high number of very large outcomes.

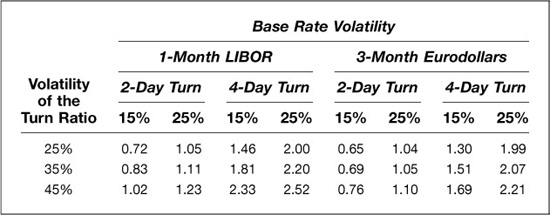

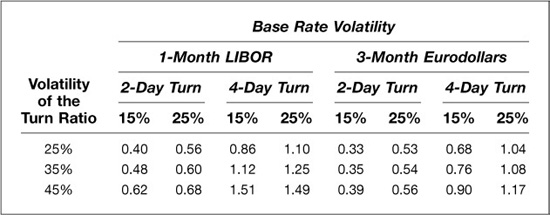

Using this approach, we can simulate the distribution of the 1-month and 3-month deposit rates that span the turn using various levels of volatility for non-turn rates and for the turn/non-turn ratio. From these simulated distributions, we can determine the effect that turn-rate volatility should have on the volatility of the December 1-month LIBOR and 3-month Eurodollar futures contracts. The results of these simulations are shown in Exhibits 16.9 and 16.10.

EXHIBIT 16.9

Add-on Turn Volatility Premium 3 Percent Forward Rate

EXHIBIT 16.10

Add-On Turn Volatility Premium 6 Percent Forward Rate

Theoretical Turn Volatility Premiums

How much is turn-rate volatility worth for options on December LIBOR and Eurodollar futures? The results shown in Exhibits 16.9 and 16.10 suggest that it should be fairly small. Consider the case in which

• The volatility (i.e., standard deviation) of the turn/non-turn ratio is 45 percent

• Forward deposit rates are around 3 percent

• The base rate volatilities of 1-month LIBOR and 3-month Eurodollar rates are 25 percent

• The turn period lasts 4 days

As shown in Exhibit 16.9, the contribution of volatility in the turn rate would add 1.49 percent to the volatility of the December LIBOR futures contract, and 1.17 percent to the volatility of the December Eurodollar futures contract. The contribution is smaller for lower levels of volatility. And, at any given set of volatilities, the contribution is smaller for a 2-day turn than for a 4-day turn.

The effect of turn-rate volatility is higher if the level of non-turn interest rates is higher. This is shown in Exhibit 16.10, where everything is the same as in Exhibit 16.9 except that the level of non-turn rates is 6 percent rather than 3 percent. At this level of rates, we reckon that the effect of 45 percent volatility in the turn/non-turn ratio combined with 25 percent base rate volatility is an increase of 2.52 percent in December LIBOR and 2.21 percent in December Eurodollar volatility for a 4-day turn.

SO WHAT?

These results may not seem very exciting at first glance because they cannot shed much light on whether December LIBOR or Eurodollar options are rich or cheap. They can be a powerful tool, however, in evaluating spread trades between December LIBOR and Eurodollar options.

For instance, even in the extreme case with rates at 6 percent, turn ratio volatility at 45 percent, base rate volatility at 25 percent, and a 4-day turn, the effect of turn-rate volatility on the difference between LIBOR and Eurodollar volatilities would only be about 0.3 percent (the difference between 2.52 and 2.21 as shown in Exhibit 16.10). In less extreme cases, and with a 3-day turn, the effect would be smaller.

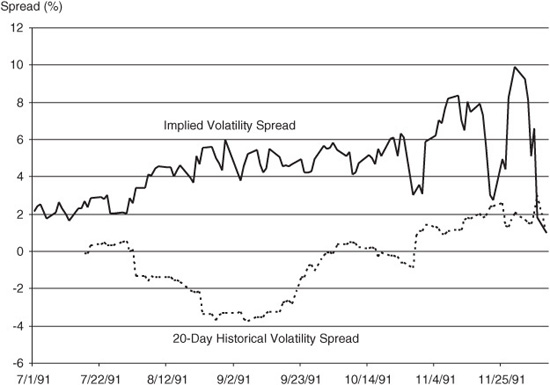

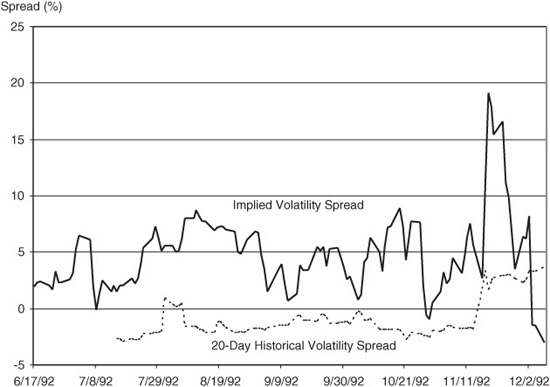

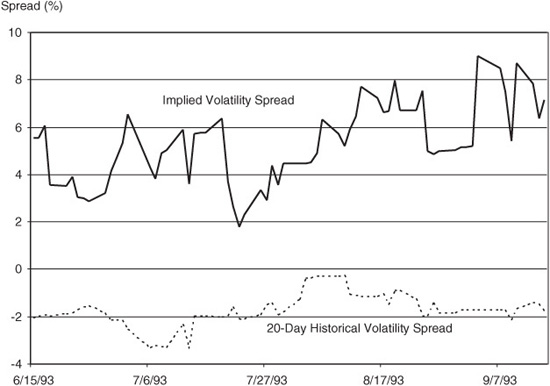

Also, we find that the spread between the historical volatilities of the December LIBOR and Eurodollar contracts over the past 2 years has actually been around zero to slightly negative. The dotted lines in Exhibits 16.11 and 16.12 show historical volatility spreads for 1991 and 1992. Exhibit 16.13 shows that the historical LED volatility spread has been below zero for the December 1993 contracts as well.

EXHIBIT 16.11

LED Volatility Spreads December 1991 Contracts

EXHIBIT 16.12

LED Volatility Spreads December 1992 Contracts

EXHIBIT 16.13

LED Volatility Spreads December 1993 Contracts

Now contrast the theory and the evidence, both of which point to a small volatility spread, with the spread between the implied volatilities for LIBOR and Eurodollar options. In 1991 and 1992, and again in 1993, the options market has paid a hefty premium for the LED volatility spread. The average implied volatility spread in 1992, for example, was about 4.5 percent. At this writing, the LED volatility spread for the December 1993 contracts is trading around 7 percent, which is far more than is warranted by either the theory or the evidence.

We view this as an opportunity to take advantage of an apparent mispricing. For example, to sell December 1993 LIBOR volatility and buy December 1993 Eurodollar volatility, on September 20, 1993, one could have:

• Sold 100 December 96.25 LIBOR straddles at 37 ticks per straddle, and sold 3 December LIBOR futures to make the position delta neutral.

• Bought 106 December 96.50 Eurodollar straddles at 25 ticks per straddle, and bought 4 December Eurodollar futures to make the position delta neutral.

Thus, the spread position could have been established for a net credit of about 12 ticks per straddle or 1,050 ticks for the position.

A position like this would have some interesting and desirable characteristics. First, because the spread is long the low-volatility options and short the high-volatility options, the net position provides a rare opportunity to be long gamma and to have time decay work in your favor at the same time.

The Risks in the Trade

As shown in both Exhibits 16.11 and 16.12, the implied LED volatility spread is highly variable. Thus, even though the additional premium paid for LIBOR volatility seems not to be justified by either the theory or the evidence, a position that is short LIBOR volatility and long Eurodollar volatility can produce large swings in a trader’s P/L from day to day. Also, a sharp increase in the turn rate can be costly for anyone who is short LIBOR volatility. In late November 1990, for example, such a spike in the turn rate increased the 20-day historical volatility spread to around 14 percent.

Even so, there are two ways the trader can make money on the trade. The first is a collapse in the implied volatility spread so that it accords more closely with what it should be. This is far and away the most satisfactory outcome because it avoids the need to actually work for a living by managing the position until the December expiration of the options.

If the implied volatility spread does not collapse, the trader can still make money if the realized difference between December LIBOR and Eurodollar volatilities proves to be less than 7 percent. In this case, if the position is properly managed, the trader can profit from the relatively higher time decay that would be taken in on the LIBOR options than would be paid out on the Eurodollar options.