CHAPTER 18

The Eurodollar Option Contract

Eurodollar option contracts were listed by the Chicago Mercantile Exchange in March 1985. The first options had quarterly expirations and expired on the same date as their underlying futures contract. Over time, the CME has added serial options, mid-curve options, and options on the 5-year bundle. Eurodollar options trade on the Exchange floor and electronically through GLOBEX.

The purpose of this chapter is to introduce Eurodollar options by covering the:

• Grid of available option expirations and underlyings

• Contract specifications

OPTION EXPIRATIONS AND UNDERLYING FUTURES

The owner of a Eurodollar call option has the right, but not the obligation, to buy the underlying Eurodollar futures contract at the option’s strike price on or before option expiration. Similarly, the owner of a Eurodollar put option has the right, but not the obligation, to sell the underlying Eurodollar futures contract at the option’s strike price on or before option expiration. Because Eurodollar options can be exercised prior to or at expiration, they are American-style options.

We further distinguish Eurodollar options based on their underlying futures contract. This provides us with four types of options:

• Standard quarterly options

• Serial options

• Mid-curve options

• Five-year bundle options

Standard Quarterly Options

Eight standard quarterly options are available for trading at any given time. These options expire in the March, June, September, and December cycle. The underlying futures contract has the same expiration date as the option. So, for example, the standard Sep ′02 option is on the Sep ′02 futures contract.

Exhibit 18.1 shows a grid of available options along with their underlying futures contracts as of the close on June 17, 2002. The standard quarterly options are shown on the diagonal from the Sep ′02/Sep ′02 box to the Jun ′04/Jun ′04 box.

EXHIBIT 18.1

Grid of Available Options June 17, 2002, Close of Trading

Serial Options

Two standard serial options are listed, also. Serial contract months are those that fall outside of the March, June, September, and December cycle. Serial options have expirations in January, February, April, May, July, August, October, and November. The underlying futures for these options are the following quarterly futures contract. For example, Exhibit 18.1 shows that the Jul ′02 and Aug ′02 serial options are on the Sep ′02 futures contract.

Mid-Curve Options

Traders use mid-curve options to trade short-dated options on longer-dated futures. The four quarterly 1-year mid-curve options expire 1 year before their associated futures. For example, as shown in Exhibit 18.1, the 1-year mid-curve option that expires in Dec ′02 is on the Dec ′03 futures contract.

There are two serial 1-year mid-curve options. The underlying futures contract for each option is 1 year away from the quarterly futures contract that follows the option expiration. So, the Aug ′02 1-year mid-curve option is on the Sep ′03 futures contract (see Exhibit 18.1).

Two-year mid-curve options also allow traders to trade short-term options on longer-term futures. There are four quarterly 2-year mid-curve options. The associated futures contract expires 2 years after the option expiration.

Five-Year Bundle Options

There are two quarterly and two serial 5-year bundle options. These options give their owners the right to buy, if a call, or sell, if a put, the 5-year futures bundle beginning with the first available quarterly futures contract. Five-year bundle options trade only on the Exchange floor, not electronically.

OPTION CONTRACT SPECIFICATIONS1

The Eurodollar option contract specifications are described below and summarized in Exhibit 18.2.

EXHIBIT 18.2

Eurodollar Option Contract Specifications

Contract Unit

An option to buy, in the case of a call, or an option to sell, in the case of a put,

• One Eurodollar futures contract—for standard, serial, and mid-curve options

• One 5-year futures bundle—for 5-year bundle options

Price Quote

Bids and offers are quoted in IMM (International Monetary Market) index points. For example, a quote of 0.35 represents an option price of $875 [= 35 basis points × $25/basis point].

Tick Size

The basic tick size is 0.01 (or 1 basis point, often represented by bp). The dollar value of a tick is $25. The dollar value of a tick on the 5-year bundle option is $500 [= $25 × 20 contracts].

Minimum Fluctuation

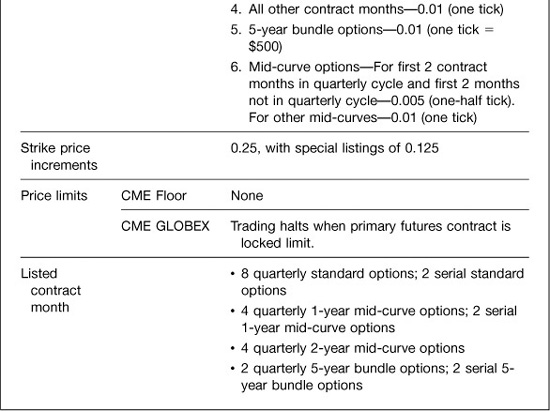

The minimum fluctuation for an option depends on its type (standard, 1-year mid-curve, 2-year mid-curve, or 5-year bundle); on whether it is a quarterly or serial option; and on where the option falls in the quarterly or serial cycle. The minimum fluctuation varies from 0.0025 (one-quarter tick) to 0.01 (one tick) based on these factors. See Exhibit 18.2 for details.

Strike Price Increments

Option strike or exercise prices are usually in increments of 0.25, although strikes of 0.125 are possible for options that are near expiration. For the nearest options in the March quarterly cycle and the two nearest options not in the March quarterly cycle having the same underlying futures contract, 0.125 strikes shall be listed beginning on the Exchange business day following the expiration of the spot month options in the March quarterly cycle. For the nearest options in the March quarterly cycle and the two nearest options not in the quarterly cycle 1-year mid-curve options, and the nearest options in the March quarterly cycle 2-year mid-curve options, 0.125 strike prices shall be listed beginning on the Exchange business day following the expiration of the last contract month in the same listing cycle.

When an option begins to trade, the Exchange establishes the strike range of available options. The Exchange adds additional exercise prices up or down as the futures market rises or falls. For options on 5-year bundles, the strike prices are based on the average price of the futures contracts in the bundle.

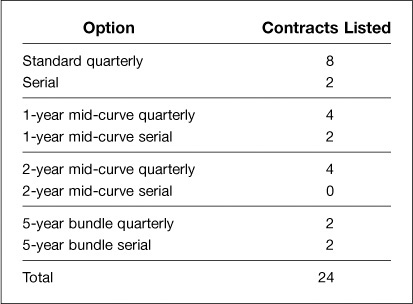

Listed Contract Months

All option types, with the exception of the 2-year mid-curve option, trade both quarterly and serial expirations. Two-year mid-curves have quarterly expirations only. The breakdown is shown in Exhibit 18.3.

EXHIBIT 18.3

Number of Standard, Serial, Mid-Curve, and Bundle Option Contracts

Contract Type and Month Symbols

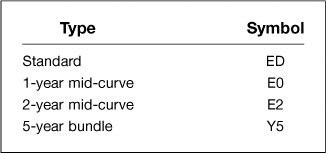

Each Eurodollar option contract is identified by type and by the month and year of expiration. Exhibit 18.4 shows the symbols used by the CME for each option type and Exhibit 18.5 shows the symbols for each contract month. For example, the 2-year mid-curve option that expires in December 2002 would be designated by E2Z2. The 1-year serial mid-curve option that expires in August 2002 would be designated by E0Q2.

EXHIBIT 18.4

Option Type Symbols

EXHIBIT 18.5

Contract Month Symbols

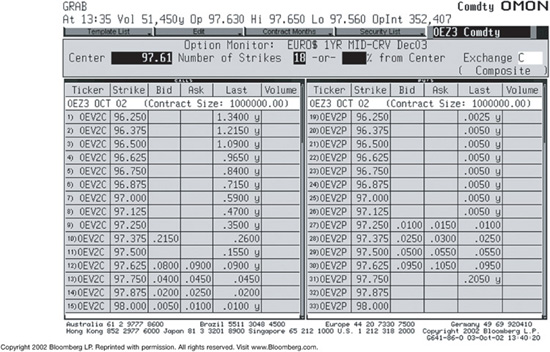

Sample Option Quotes

Bloomberg makes use of the contract month symbols in its option quote screen. For example, in Exhibit 18.6, October 2002 call and put prices are displayed next to the symbols 0EV2C and 0EV2P. Note that Bloomberg uses 0E, rather than E0, to designate the 1-year mid-curve contract. Bloomberg also uses 2E, rather than E2, to designate the 2-year mid-curve.

EXHIBIT 18.6

October ′02 1-Year Mid-Curve Option Prices

Trading Hours

Eurodollar options trade on the floor of the CME from 7:00 a.m. to 2:00 p.m. Chicago time. Standard and mid-curve options trade on GLOBEX Monday through Thursday, 2:13 p.m. to 7:04 a.m. the following day and Sunday from 5:30 p.m. to 7:04 a.m. the following day. Five-year bundle options do not trade on GLOBEX.

Last Trading Day

Standard quarterly options terminate trading at the same date and time as their underlying futures contracts. This means that the options stop trading at 11:00 a.m. London time on the second London bank business day immediately preceding the third Wednesday of the contract month. This is 5:00 a.m. Chicago time, except when daylight savings time is in effect in either, but not both, London or Chicago.

Serial options, mid-curve options, and 5-year bundle options all terminate at the close of trading on the Friday preceding the third Wednesday of the contract month.

Exercise of Option

The owner of a call or put may exercise the option on any business day that the option is traded. An option that is in the money at the termination of trading, and has not been liquidated or exercised prior to the termination of trading, is exercised automatically at 7:00 p.m., unless the Clearing House receives instructions to the contrary.

Assignment

After long options have been exercised, parties who are short the options are “assigned.” This assignment is done by random selection of clearing members with short positions in the appropriate options. The clearing member assigned an exercise notice shall be assigned a short futures position, in the case of a call, and a long futures position, in the case of a put. Assignment of the futures position is done at the option’s strike price; the futures position is then marked to market.