CHAPTER 17

The Turn: An Update

Chapter 16 reproduces the research note:

• Trading the Turn (1993)

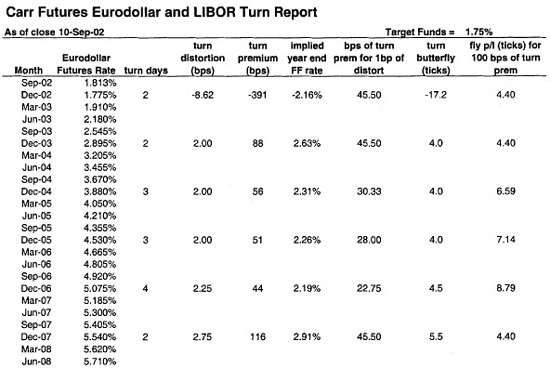

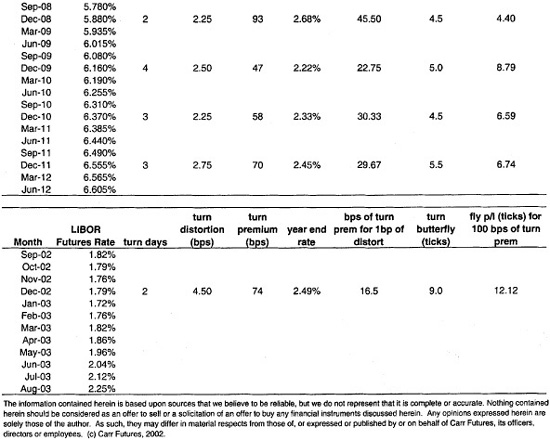

To help traders keep an eye on the market’s view about the turn, we created the “Eurodollar and LIBOR Turn Report,” shown in Exhibit 17.1. This report shows by year how much the December contract is out of line, how many days there are in each year’s turn, and what the distortion implied for a turn premium in the year-end Fed funds rate.

EXHIBIT 17.1

Eurodollar and LIBOR Turn Report

In the particular example shown here, the turn distortions are comparatively small by historical standards, and so are the turn premiums. For that matter, on September 10, 2002, the distortion for the Dec ′02 contract appeared to be negative. For the rest of the December contracts, the futures rate distortions are all 2+ basis points, implying Fed funds premiums of anywhere from 44 basis points (Dec ′06) to 116 basis points (Dec ′07).

HEDGING THE STUB

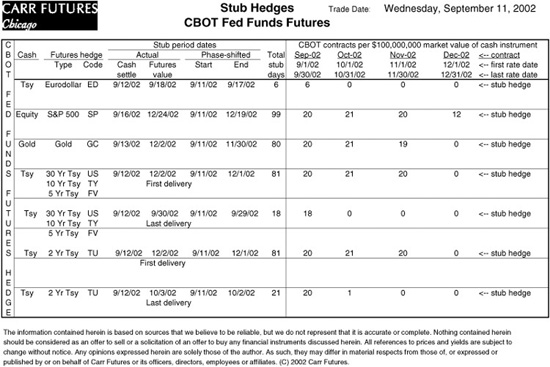

The period between today and the first available futures contract’s expiration has become known as the stub, and the term financing rate that covers this period is called the stub rate. Any trade or hedge that combines spot commodities with futures is exposed to stub rate risk. One way to offset this risk is to borrow or lend in the term money market to create offsetting interest rate exposure. The best available futures solution employs the Fed funds futures that are traded at the Chicago Board of Trade. These contracts are especially well suited to hedging very short-term money market risk—first, because Fed funds rates track term repo rates well, and second, because the contracts settle to averages of realized Fed funds rates, so there is very little slippage.

The “Stub Hedges” report, shown in Exhibit 17.2, was designed for clients who want to use futures rather than term repo to hedge their stub rate exposure. In the example provided here for the close of business on September 10, 2002 (trade date of September 11, 2002), you can see examples of various spot commodities traded against different futures. For example, the stub for a Treasury bond or note hedged with Eurodollar futures was 6 days, and the appropriate hedge for this risk would be 6 Sep ′02 Fed funds futures. For a spot equity position hedged with S&P equity futures, the stub period was 99 days, and the stub hedge would comprise 20 Sep ′02 contracts, 21 Oct ′02 contracts, 20 Nov ′02 contracts, and 12 Dec ′02 contracts.

EXHIBIT 17.2

Stub Hedges

Using CBOT Fed Funds Futures