CHAPTER 10

Convexity Bias: An Update

Chapters 7, 8, and 9 reproduce 3 research notes:

• The Convexity Bias in Eurodollar Futures (1994)

• Convexity Bias Report Card (1997)

• New Convexity Bias Series (2002)

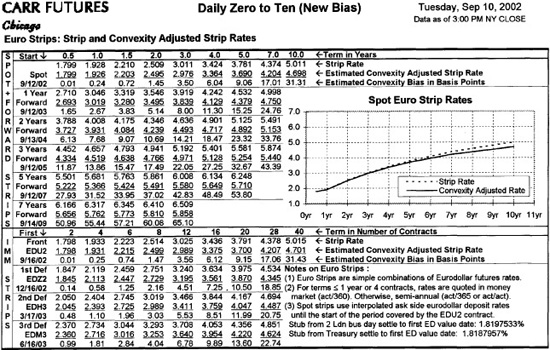

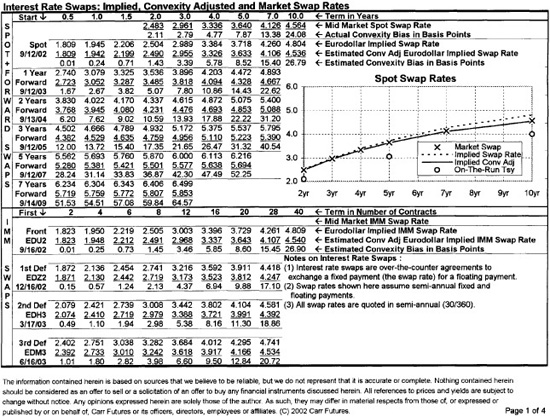

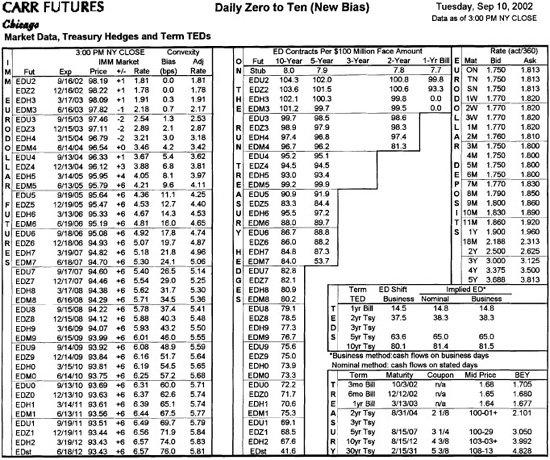

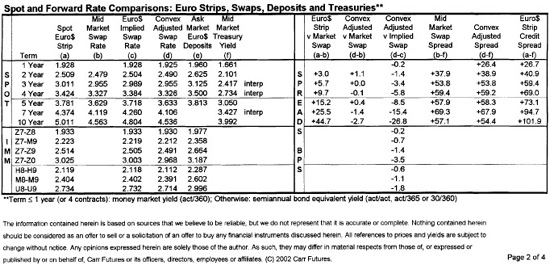

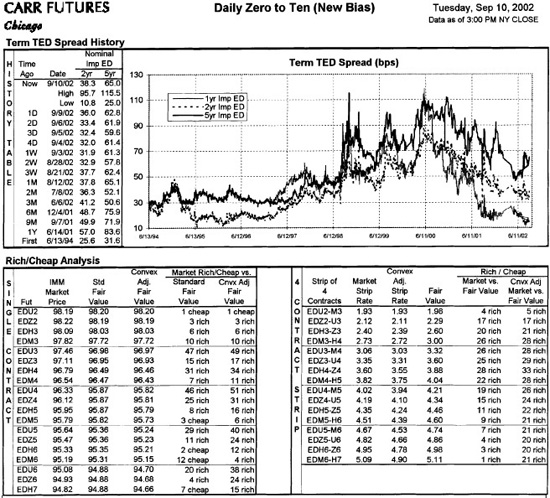

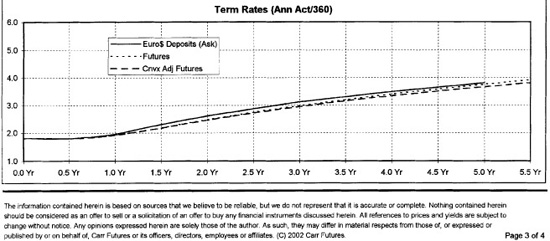

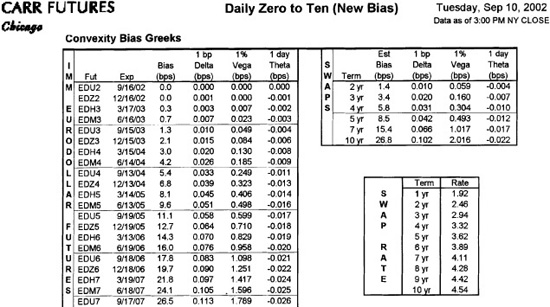

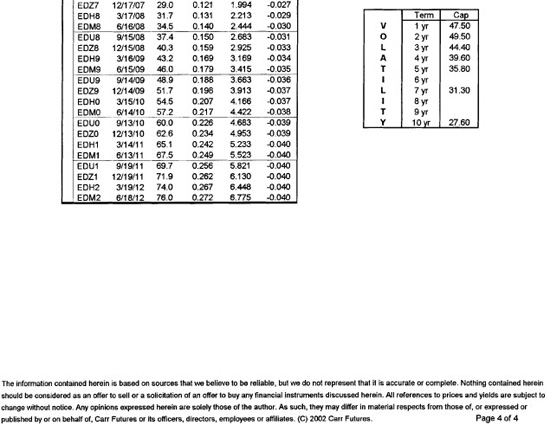

These three notes describe the work we have done to gain an understanding of the relationship between Eurodollar futures rates and the forward rates that one would use to price interest rate swaps. The “Daily Zero to Ten,” a four-page daily report produced by Carr Futures, is the working tool that has emerged from these notes. We reproduce a copy of this report, taken from the close of business September 10, 2002, in Exhibit 10.1.

For swap traders, the two most important pages are the first and fourth. The first page compares swap rates derived from three sources: the market; raw, unadjusted Eurodollar futures rates; and convexity-adjusted futures rates. For swap traders, the upper part of the lower panel is most relevant day to day. There you will find mid-market swap rates as reported by Reuters, a Eurodollar implied swap rate (as calculated from unadjusted futures rates) and an estimated convexity-adjusted Eurodollar implied swap rate (from convexity-adjusted rates). For example, the mid-market 5-year swap rate in the attached report was 3.640%. The Eurodollar implied swap rate was 3.718%, and the convexity-adjusted Eurodollar implied swap rate was 3.633%. The actual convexity bias was then 7.87 basis points [≈ 3.718% − 3.640%], while the estimated or theoretical convexity bias was 8.52 basis points [≈ 3.718% − 3.633%].

The fourth page is especially useful to risk managers, who often need convexity bias estimates from a disinterested source. Carr Futures can be this source, since it is a specialist futures firm and has, as a result, no swap book to value. This page is also useful to those who want to know what assumptions have gone into our calculations and how sensitive the estimates are to changes in rate levels and rate volatilities.