APPENDIX B

Calculating Eurodollar Strip Rates and Implied Swap Rates

EURODOLLAR STRIP RATES

A Eurodollar strip is a position that contains one each of the contracts in a sequence of contract months. For example, a 1-year strip might contain one each of the June ′94, September ′94, December ′94, and March ′95 contracts. A 2-year strip would contain these plus one each of the June ′95, September ′95, December ′95, and March ′96 contracts. The rates implied by a strip of Eurodollar futures prices together with an initial spot rate can be used to calculate the terminal value of $1 invested today. For example,

where

TWT is the terminal value (i.e., terminal wealth) of $1 invested today for T years

R0 is spot LIBOR to the first futures expiration

F1 is the lead futures rate [= 100 − lead futures price]

Fn is the futures rate for the last contract in the strip

Di is the actual number of days in each period, i = 0,…, n

From this value of terminal wealth, we can calculate Eurodollar strip rates in several forms including money market, semiannual bond equivalent, and continuously compounded. All three are zero-coupon bond rates implied by a strip of Eurodollar futures prices.

MONEY MARKET STRIP YIELD

The money market strip yield is the value of RMM that satisfies

where N is the whole number of years in the strip and Df is the number of days in a partial year at the end of the strip.

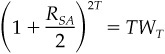

SEMIANNUAL BOND EQUIVALENT YIELD

The semiannual bond equivalent strip yield is the value of RSA that satisfies

which provides RSA as

![]()

CONTINUOUSLY COMPOUNDED YIELD

For computing returns on zero-coupon bonds, continuously compounded yields are the most convenient because the duration of a zero-coupon bond is equal to its maturity when yield changes are continuously compounded. The continuously compounded yield is the value of RCC for which

eT×RCC = TMT

where e is the base for natural logarithms. This can be solved as

![]()

where ln () is the natural log.

ZERO-COUPON BOND PRICE

The price of a $1 par value zero-coupon bond that matures at T is:

![]()

IMPLIED SWAP RATES

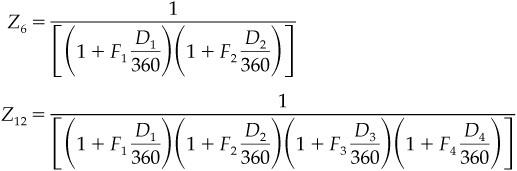

A conventional fixed/floating interest rate swap typically is priced as if it contains a long position in a floating rate note and a short position in a fixed rate note. At the time of the transaction, the fixed and floating rates are set so that the net present value of the swap is zero. If the initial floating rate is set equal to the market rate for the term of the floater—for example, equal to 3-month LIBOR if the swap has 3-month reset dates—then one can assume the hypothetical floater would trade at par. As a result, one can assume that the fixed rate on the swap must be set so that the hypothetical fixed rate note would also trade at par. The swap yield is simply the coupon rate that would accomplish this. For example, the swap yield for a 1-year swap with semiannual reset dates would be the value of C that satisfied the following

where Z6 is the price of a zero-coupon bond that matures in 6 months, and Z12 is the price of a zero-coupon bond that matures in 12 months. If one happens to be pricing a swap on a futures expiration date, the zero-coupon prices would be calculated as

and so forth. Note that F1 and F2 appear both in Z6 and Z12 while F3 and F4 appear only in Z12. From this, one can see that the swap yield implied by a sequence of Eurodollar futures rates is a weighted average of these rates that gives greater weight to the nearby rates than to the more distant rates.