CHAPTER 20

Caps, Floors, and Eurodollar Options

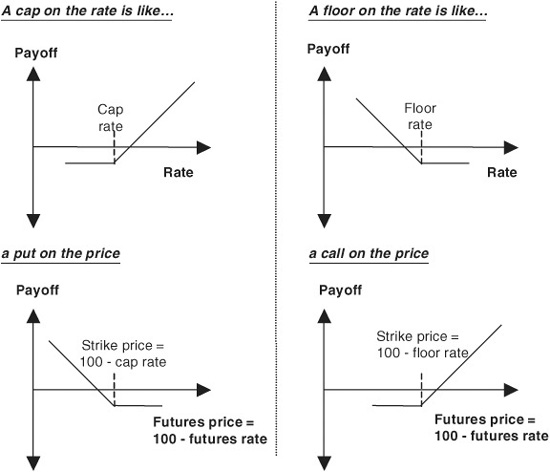

Eurodollar options are the exchange-traded counterparts to interest rate caps and floors, which are traded over the counter. An interest rate cap, which pays the holder if LIBOR is above the cap rate at the rate setting date, is akin to a Eurodollar put, and an interest rate floor, which pays if the reference rate is below the floor rate, is like a Eurodollar call. Exhibit 20.1 shows the comparison between the exchange-traded and over-the-counter products.

EXHIBIT 20.1

Cap and Eurodollar Put; Floor and Eurodollar Call

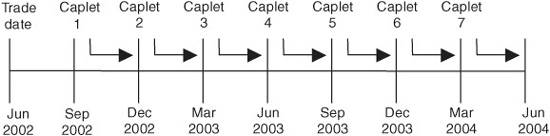

The usual cap or floor comprises a sequence of “caplets” or “floorlets.” That is, a cap is a sequence of single options whose payoff cover periods shorter than the life of the cap. For example, a 2-year cap with quarterly resets would comprise a sequence of 7 options, each of which depends on the value of 3-month LIBOR on the day the option expires. Thus, the first caplet in a 2-year cap traded in June 2002 would expire in September and would pay off or not depending on whether 3-month LIBOR on the rate setting date was greater than the cap rate. The seventh caplet would expire in March 2004 and would depend on the value of 3-month LIBOR then. Exhibit 20.2 illustrates this 2-year cap.

EXHIBIT 20.2

Rate Setting on a 2-Year Cap

From a pricing standpoint, there are three main differences between over-the-counter caps and floors and exchange-traded Eurodollar options. First, caps and floors tend to be European-style options, while Eurodollar futures options are American-style options. Second, the nominal payoff to a cap or floor depends on the days in the interest calculation period, while the nominal payoff to a Eurodollar futures option is a fixed $25 per basis point. Third, the holder of a cap or floor usually is paid in arrears—that is, at the end of the interest calculation period—while the holder of a Eurodollar option collects at option expiration.

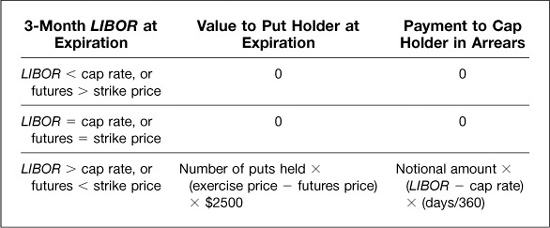

The differences and similarities in payoffs for a cap and a Eurodollar put are illustrated in Exhibit 20.3. The conditions under which the two pay off are identical as long as the strike price on the Eurodollar put is set equal to 100 less the cap rate and as long as the reference rate for the cap is 3-month LIBOR. If LIBOR is less than or equal to the cap rate at expiration, the futures price will be greater than or equal to its strike price, and both instruments will pay nothing.

EXHIBIT 20.3

An Interest Rate Cap is Like a Eurodollar Put Put Strike Price = 100 − Cap Rate

On the other hand, if LIBOR exceeds the cap rate at expiration, the holder of the cap collects an amount equal to

![]()

at the end of the interest calculation period. The holder of the Eurodollar put would receive

$2500[Exercise price ≫ Futures price]

on the day the option expires.

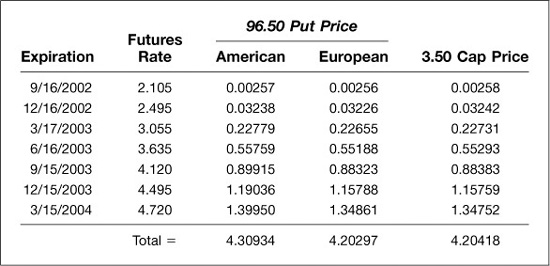

Exhibit 20.4 provides a comparison of the prices of Eurodollar puts and the component legs of a 2-year interest rate cap struck on June 17, 2002. The futures rates used in this exhibit were the implied Eurodollar futures rates at the close of business on June 17, and the implied volatilities (not shown) were market implieds. The cap rate was set at 3.50, which was roughly in the middle of the futures rate curve, and the Eurodollar put strike was set at 96.50 [= 100.00 − 3.50]. For simplicity, the caplets have been arranged so that their rate-setting dates fall on Eurodollar futures expiration dates, and all caplet periods in this example contain 91 days. All option prices are expressed in Eurodollar option terms. To find the dollar value of any one option, simply multiply its value by $2,500.

EXHIBIT 20.4

Comparing Eurodollar Puts to an Interest Rate Cap

June 17, 2002

The Eurodollar put prices are shown under the column labeled “American.” We also have valued the options as European style. For the full strip of puts, the value of early exercise that goes with the American-style options was 0.10637 [= 4.30934 − 4.20297]. The cap prices are simply the European put prices scaled by (91/90)/(1 + Rate (91/360)), which increases the payoff to reflect the 91 days in the caplet periods and decreases the payoff to reflect the fact that the cap holder gets the money at the end of the 91 days rather than on the expiration or rate setting date. A close comparison of the caplet prices with the European-style put prices shows that the day-count influence is greater for the shorter-dated caplets, while the discounting influence is greater for the longer-dated caplets.

The cap prices in Exhibit 20.4 are expressed in IMM, or Eurodollar futures options, terms for the sake of comparison. The convention for interest rate caps, however, is to quote the premium as a total dollar value or as a percentage of the notional amount if the structure is non-amortizing.