The ex-ante Sharpe ratio (SR) compares the portfolio's expected excess portfolio to the volatility of this excess return, measured by its standard deviation. It measures the compensation as the average excess return per unit of risk taken:

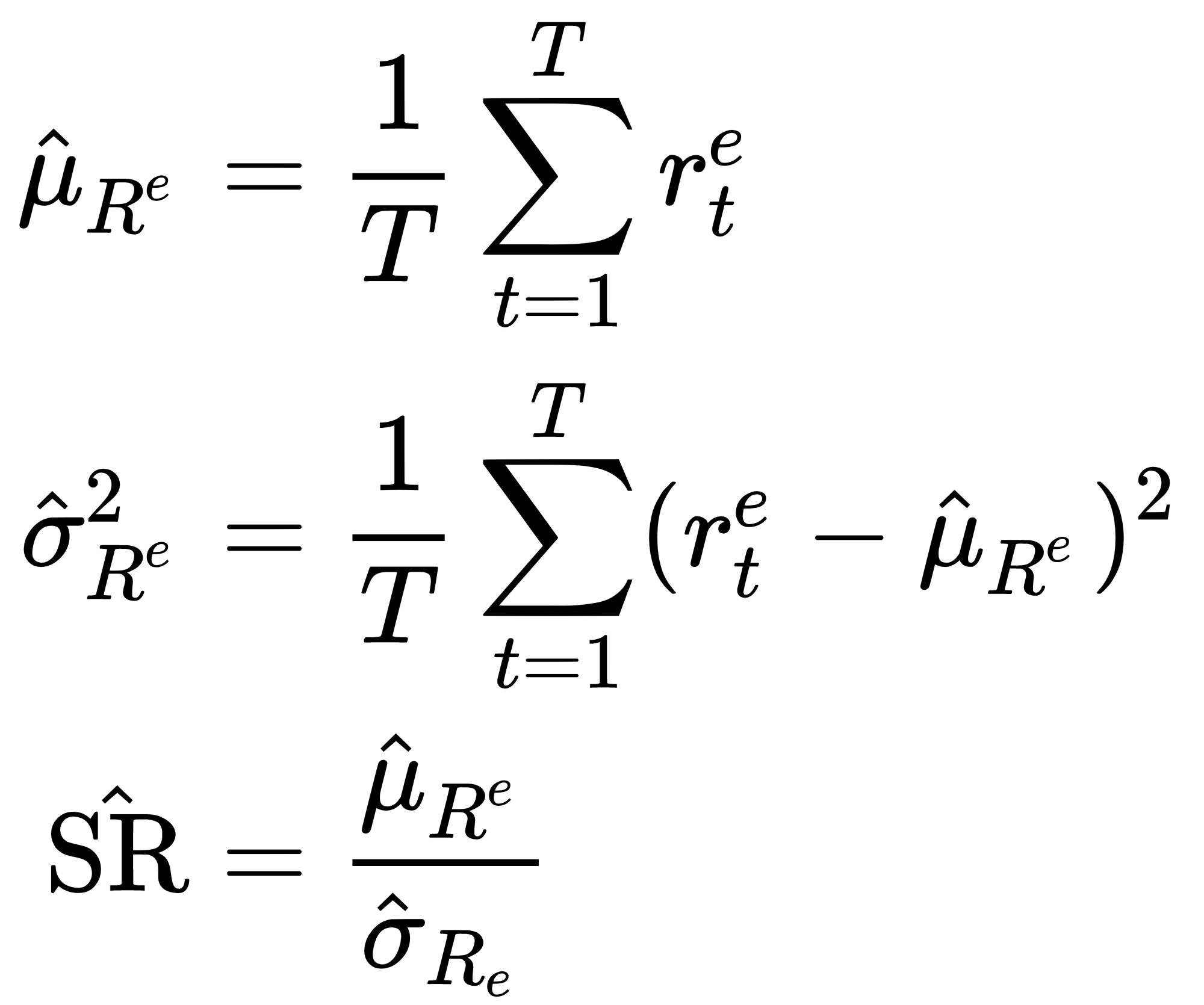

Expected returns and volatilities are not observable, but can be estimated as follows using historical data:

Unless the risk-free rate is volatile (as in emerging markets), the standard deviation of excess and raw returns will be similar. When the SR is used with a benchmark other than the risk-free rate, for example, the S&P 500, it is called the information ratio. In this case, it measures the excess return of the portfolio, also called alpha, relative to the tracking error, which is the deviation of the portfolio returns from the benchmark returns.

For independently and identically-distributed (iid) returns, the derivation of the distribution of the estimator of the SR for tests of statistical significance follows from the application of the Central Limit Theorem, according to large-sample statistical theory, to μ̂ and σ̂2.

However, financial returns often violate the iid assumptions. Andrew Lo has derived the necessary adjustments to the distribution and the time aggregation for returns that are stationary but autocorrelated returns. This is important because the time-series properties of investment strategies (for example, mean reversion, momentum, and other forms of serial correlation) can have a non-trivial impact on the SR estimator itself, especially when annualizing the SR from higher-frequency data (Lo 2002).