Chapter 4

Paying with the Right Payment Options

IN THIS CHAPTER

![]() Taking credit cards

Taking credit cards

![]() Obtaining a merchant account

Obtaining a merchant account

![]() Setting up your gateway and payment processor

Setting up your gateway and payment processor

![]() Offering payment options beyond credit cards

Offering payment options beyond credit cards

![]() Avoiding fraudulent charges and other online credit risks

Avoiding fraudulent charges and other online credit risks

One indisputable fact about running an online business is that you can’t very well sell products over the Internet if you don’t have a way to accept money from customers. Fortunately, you have a bevy of options.

One common solution is to accept credit cards, just as any bricks-and-mortar store does. With credit and debit cards most commonly used for online shopping, customers expect to be able to pay this way. Fortunately, the acceptance and growth of e-commerce have simplified the process for online merchants. In less than a week (and sometimes within 48 hours), you can be ready to accept your first online credit card order.

Then again, not all customers have credit cards ready at their fingertips. Or perhaps they don’t want to use credit cards online for security reasons. As an e-commerce merchant, you should provide those customers with an alternative payment solution.

In this chapter, we tell you about all the payment options available to your online business, and we show you how to start setting them up on your site.

Accepting Credit Card Payments

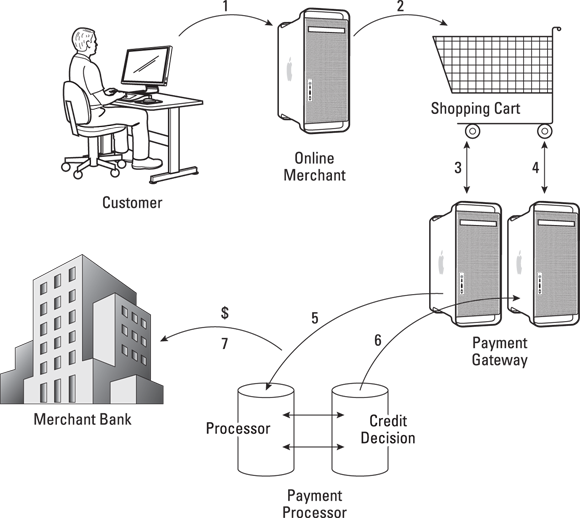

Enabling a website to accept credit cards is one of the most misunderstood functions of e-commerce. A shopper understands that she has to type her credit card number into a box on her computer screen and then click the Purchase button. And she knows that, after a few seconds, she receives an approval (or not) for her purchase. Although everything that happens between these two points comes across as a mystical unknown occurrence, not a drop of magic is involved in this simple process (see Figure 4-1).

FIGURE 4-1: Processing credit cards online.

Here’s how it works:

-

A customer goes shopping on your site and puts products into a virtual cart.

Shopping cart software that you add to your site allows customers to select products for purchase. When customers are ready to check out, the shopping cart starts the process of ringing up the sale.

-

The customer pays for the product by using a credit card.

Your shopping cart program should provide an online form for the customer to complete, including personal information, shipping details, and a credit card number with expiration date and, possibly, a verification code from the back of the card. (An expedited checkout process may be used for returning customers.)

-

Your site sends that credit card information to a payment gateway.

The gateway is a virtual gate through which information is transmitted, or passed between your site and a credit card processing site. The gateway, like the little box you use to swipe your card when you’re shopping in a traditional store, is a tool for communicating information between the store and the credit card company.

-

A payment processor receives and verifies your customer’s information.

The processor’s job is to talk with the company or bank that issues the credit card. The processor ensures that the card is valid and that it has enough credit to cover the purchase.

-

The processor sends a credit decision back to the gateway.

The processor finds out whether your customer is approved or declined for the purchase and transmits that data right back to the payment gateway.

-

Your gateway passes along the approval decision (approval or denial) to your shopping cart and finalizes the shopping transaction.

Your customer sees a final message saying that the purchase is approved (or not). From there, your shopping cart program can provide a receipt, shipping details, and an invitation to shop again.

Steps 2–6 take only a few seconds, and then your customer’s purchase is complete.

-

While your customer is receiving an approval message, the processor is sending the money to your bank account.

After the credit card issuer says that credit is available, the processor makes sure that money is sent to your bank and deposited into your merchant account.

Although this process is happening within milliseconds of the approval process, you might not see the money in your account for two to three business days.

Although this process is happening within milliseconds of the approval process, you might not see the money in your account for two to three business days.

Securing a merchant account

Now that you better understand the process, you’re ready to get it set up on your site. The first step is to secure a merchant account. You can choose from several resources:

- Bank: You can turn to your local bank to set up a merchant account. After all, your business checking account resides there. Most banks now offer e-commerce merchant services as part of their standard small-business service packages. However, be aware of a few issues. Banks often

- Have a more rigid approval process for online businesses because they’re still considered high-risk ventures

- Pass your application to a third-party company for approval (as opposed to processing and managing it internally)

- Increase your costs for a merchant account because the bank is essentially a middleman and receives a commission on the referral of your account

- Direct provider: You can access many of the same direct merchant account providers that your local bank might use. By going directly to a processor to set up a merchant account, you can cut out some of the initial costs. You can set up a merchant account with one of these processors:

- Chase J.P. Morgan Paymentech:

www.chasepaymentech.com - Flagship Merchant Services:

www.flagshipmerchantservices.com - Cayan:

www.cayan.com/payment-processing - National Bankcard:

www.nationalbankcard.com

- Chase J.P. Morgan Paymentech:

- Third-party processor: This type of company or independent agent offers the following types of merchant account services:

- Broker: This person is usually an independent sales rep who makes a commission from brokering or signing up new customers. A broker who represents more than one company can help you compare and find the best rates available. (Brokers are not as common as they once were, given the increased access to so many online options.)

- Online service: Companies that once offered a primary service, such as a shopping cart program, are now including bundled access to multiple companion services. Setting up merchant accounts is among those services. Network Solutions, originally best known as a domain registrar, is an example of an online company expanding its e-commerce service offerings to include merchant services (

www.networksolutions.com/e-commerce). Similarly, storefronts or e-commerce solutions, such as Shopify (www.shopify.com), act as a third-party processor for their customers, so all your back-end operational and processing functions are tied with your online store — in one place. - Online specialist: Possibly considered an online service provider, PayPal (

www.paypal.com) is slightly different because the company specializes in online payments. Through its PayPal Payments Pro program, it offers e-retailers a complete solution that includes a merchant account and payment gateway for a low monthly fee, plus credit card transaction fees. Alternative or nontraditional services include Square (www.squareup.com) and Stripe (www.stripe.com). These hybrid online specialists are similar to PayPal, but the setup to start accepting credit card payments takes just minutes and does not require the setup of a separate merchant account. Stripe is unusual, in that it bypasses the payment gateway — to accept payments with Stripe, all you need is a Stripe account. These alternative online specialists also allow you to accept credit card transactions on mobile devices. Stripe also allows you to accept other payment options including Bitcoin (the Internet currency), Apple Pay, Android Pay (mobile phone payments), and Alipay (from China).

If you deal with one of the larger online services or online specialists, you can take advantage of their economies of scale and find a better deal on some items. For example, these sites may have inexpensive flat monthly service fees and no set-up fees or application fees. They also tend to have lower rates as well as higher approval and acceptance rates for online businesses because they target that customer base.

If you deal with one of the larger online services or online specialists, you can take advantage of their economies of scale and find a better deal on some items. For example, these sites may have inexpensive flat monthly service fees and no set-up fees or application fees. They also tend to have lower rates as well as higher approval and acceptance rates for online businesses because they target that customer base.

If you reside outside the United States or you expect to have a larger international customer base, make sure the merchant account can meet your needs. European countries in particular have different regulatory concerns than the United States, and your merchant account provider should understand and meet those requirements.

Choosing a payment gateway

As soon as you receive the go-ahead to accept credit cards, your next action is typically to choose a payment gateway, unless you’re using an alternative online specialist that doesn’t require a gateway.

The gateway talks to the credit card companies, your banks, and your website. Needless to say, the gateway plays an important role in your e-commerce equation.

If you’re receiving bundled services from one source, your merchant account provider might already have a designated gateway for you to use. That’s good news because it indicates that a relationship is already established. Both ends know how to successfully come together in the middle, so to speak. Alternatively, the provider might have partnerships set up with several gateways. They simply let you select the one you want to use. Or you might be left to search for a payment gateway on your own.

You can choose from hundreds of payment gateways, and hooking up with the wrong one can bring your sales to a halt (sometimes before they get started). Don’t worry, though: You should have no trouble finding the right match. Look for a payment gateway that has these characteristics:

- Diversity: To be effective, your gateway needs to work with all major credit cards, including MasterCard, Visa, and American Express.

-

Compatibility: One of the most important requirements is that the gateway integrates with your shopping cart software. Although major gateways are already set up to talk with the majority of off-the-shelf shopping carts, it never hurts to verify that your gateway is compatible.

If your shopping cart is custom designed or is a lesser-known software, you might have to do a little programming to make your gateway communicate with your site. - Timely payments: Each gateway has its own rules for when and how to make payment to your bank. Choose a gateway that deposits your money within a few days at most (as opposed to once a month or so).

- Support: As with any service provider, make sure that your payment gateway has customer service support, including tech support available at any time of the day or night.

- Accessibility: You should be able to view the status of your transactions in an online report, along with other management tools.

- Feature-rich: Payment gateways have a surprising number of features you can use (or add for a fee). Allowing for recurring billing and additional payment options on your customer accounts and fraud-protection tools for you are desirable features. Even though these options might not be a big deal now, you want them available as your site grows.

With the increasing demand for mobile payments, look for payment gateways that offer secure payment processing from mobile devices.

Today, you can choose from dozens, if not hundreds, of payment gateways. When you’re ready to get started, here’s a list of some better-known payment gateways you can contact:

- Authorize:

www.authorize.net - Cardstream:

www.cardstream.com(based in the United Kingdom) - Chase Paymentech:

www.chasepaymentech.com - Cayan:

www.cayan.com/payment-gateway-services - 2Checkout:

www.2checkout.com

When you’re comparing the cost of payment gateways, be sure to look at gateway resellers, too. Some offer a limited number of transactions for free when you sign up. In some cases, you don’t have to pay additional fees on your first 1,000 transactions.

Reading the fine print: Fees

When you’re applying to become an authorized credit card merchant, be sure to compare service providers. Although base rates might remain similar, other unexpected fees could swing the pendulum in favor of one over another. To compare apples to apples, you need to understand the different types of fees you might encounter:

- Application: Some agents charge a nominal fee for processing your application. Expect to pay at least $100.

- Setup: This fee covers the cost of establishing your merchant account and can range from $200 to $1,000 or more. A typical fee is $200 or $300.

-

Discount rate: Each time one of your customers make a purchase with a credit card, your merchant account provider takes a cut of the sale. The amount varies based on the type of card that’s used but is usually between 2 and 4 percent.

Your account should specify Internet, mail order, or telephone sales. Because you can’t swipe an actual credit card, rates for these types of transactions are typically higher (sometimes by as much as a full point) than those for offline retailers. - Terminal cost: When you’re swiping credit cards or manually punching in account numbers, you need a small electric terminal or box. You might have to lease or purchase this equipment, which can add several hundred dollars to your annual costs. For e-commerce sales, a terminal usually isn’t required. In some cases, you can use a phone app to swipe credit cards.

-

Statement: This monthly fee covers the merchant account provider’s cost of compiling, printing, and mailing a monthly statement of your account. The fee can be several dollars.

You might be able to eliminate this fee by choosing to access your reports online rather than on paper statements you receive by postal mail. When you ask your provider whether you have this option, also confirm how long online statements are available for viewing. (You print your own copies to serve as a permanent record, if needed.) - Transaction: You pay a small processing fee for each credit card transaction. This nominal amount is usually less than 25 cents per transaction. And yes, it’s in addition to your discount rate.

- Monthly minimum: If you expect to have a limited number of sales (maybe your business is new or you just don’t expect a lot of traffic early on), your merchant account provider might establish a minimum charge level. If your sales, number of transactions, or combined discount rate and transaction fees don’t exceed that minimum, the company tacks on an additional charge. In other words, the company is counting on you to process lots of orders so that it makes more money. You pay for it either way, though.

- Charge back: Whenever a customer disputes a purchase with the credit card company, the dollar amount of that purchase is taken from your bank account. Your merchant account provider might also charge you an additional fee for processing this transaction. Online orders that don’t require signatures (or the physical cards to process) are especially susceptible to charge backs.

- Termination: Whether you’re switching merchant providers or closing up shop, your original contract might contain a termination fee. Sometimes this fee can be as much as $1,000 or more.

Before signing any agreement, seek out the clause that details the steps you have to take to cancel the agreement. If early termination is expensive, make sure that a companion clause specifies that you can upgrade when new features are released. Today’s version of the latest and greatest feature can be quickly usurped in a few months. You don’t want to get stuck paying big bucks for features that don’t keep pace with your growing business. Some competitive providers don’t lock you into long-term contracts, so take the time to compare the pros and cons of each provider.

Offering Alternative Payment Options

You might think that credit cards have a hold on the online shopping market. Indeed, the majority of customers prefer paying that way. Yet online security concerns and the demand for flexibility are driving the need for alternative options.

You receive a definite benefit when you expand your customers’ payment choices. Online stores that offer only credit cards as a payment source can still get a substantial number of their visitors to purchase something. But by adding PayPal or e-checks (or electronic checks), you can sometimes boost that conversion rate by nearly 25 percent, according to research by PayPal.

Gaining more customers by being flexible is a no-brainer, as they say. As luck would have it, you can offer customers more than a handful of alternative payment solutions:

- PayPal: One of the most popular alternatives is allowing customers to pay by using a PayPal account. As we mentioned when discussing merchant accounts, PayPal specializes in online payment processing. It offers many options, is a one-stop shop for all your e-commerce payment needs, and is widely recognized. To start using this option, go to

www.paypal.com. - Electronic checks: This service, also called Automated Clearing House (ACH) processing, allows a customer to use funds taken directly from a personal or business bank account. The funds are then deposited directly into your bank account. For you, this service represents lower processing fees per transaction than with credit cards. Fees can range from 30 cents per transaction to more than a dollar for each check. Increasingly, payment gateways are making electronic check processing available for your website. Or you can use a third-party e-check provider, such as

- iChex:

www.ichex.com - Forte:

www.forte.net/echeck - PaySimple:

www.paysimple.com

- iChex:

- Gift cards: Offering gift certificates or gift cards on your site is an easy way to extend payment options while increasing your sales.

- Instant credit: If your customers could buy now and pay later, don’t you think that it would help prevent shopping cart abandonment? Well, companies are now providing online retailers a way to do just that. At the time of checkout, your customer essentially receives approval for the dollar amount of the purchase. This process usually takes no more than 15 seconds. Then the customer has a set amount of time to make the payment. Don’t worry: You receive the funds immediately, as you would with any other type of payment. A third-party company handles everything for you. PayPal Credit (

www.paypalcredit.com), formerly known as Bill Me Later, offers one such solution. - Offline payments: An option that’s sometimes overlooked is allowing customers to send in payments by using a less technically advanced method. Although only a small percentage of shoppers are likely to use these options, it could be worthwhile. After all, it’s certainly not cost prohibitive to extend these options:

- Send payment through Western Union.

- Mail checks through the U.S. Postal Service.

- Pay by phone (requires a credit card, but some customers feel safer this way).

Managing the Payment Process to Protect Your Income

Believe it or not, one day you will receive a fraudulent charge back from a customer. You lose the money, plus handling fees charged by the credit card company. Of course, a charge back is only one type of online fraud you have to worry about. Dealing with stolen credit cards is another common headache.

Don’t despair yet. Credit card companies, payment gateways, and processors are working diligently to help protect your online business from thieves. All you have to do is choose to implement their protective services. To help minimize your risks, search out these standard security features from your payment gateway provider:

- Address verification service (AVS): Each time an order is placed, the physical street address on file with the credit card issuer is compared to the billing address the customer gives you with an order.

- Card code verification (CCV): Customers must enter both a credit card account number and a special three- or four-digit code called the CCV. The code is usually on the back of the credit card.

- Filtering: You can use several security filtering tools. One type allows you to set a monetary limit for additional security checks on orders that exceed that amount. Other filters screen for suspicious orders and identify IP addresses that have excessive amounts of purchases within a short period.

- Address blocking: By using this tool, you can block IP addresses from your site. In this case, the addresses are known sources of earlier fraudulent orders.

- Authorized AIM IP: When you submit Advanced Integration Method (AIM) transactions, you can designate a server’s specific IP addresses that are allowed to transmit transactions.

As a smaller online business (generating less than $5 million in annual sales), you typically have a lower fraud rate than large online retailers. That’s because smaller businesses process fewer transactions, validate orders manually (usually), and fight charge backs by calling customers personally.