European currency options grant the holder the right to buy (call option) or sell (put option) currency at a predetermined exchange rate (strike price or exercise price, X), on a specified date (maturity, T). These financial assets are also called foreign exchange options (or FX options), but to avoid confusion with the term "exchange option", we prefer the "currency option" terminology.

A basic assumption of the original Black-Scholes model (Black and Sholes, 1973, see also Merton, 1973) is that the underlying is a stock that pays no dividend. More generally, the results of the model are held only if the underlying does not grant any kind of yield and does not generate any kind of cost either. However, this assumption might be relaxed easily, and an extended version of the Black-Scholes formula is valid for currency options as well, while all the logic and argumentation of the model is unchanged.

The closed form formula for the price of a European currency call option (c0) is the following:

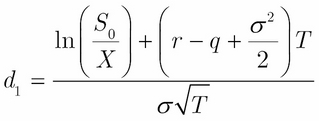

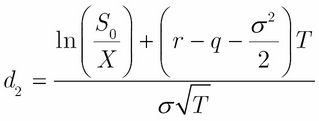

In the preceding formula, the values of d1 and d2 are as follows:

and

and  .

.

In the preceding formulas, S0 is the spot FX rate (the price of one unit of the base currency, expressed in the variable currency), X is the strike price, T is the time to maturity of the option (in years), σ is the volatility of the FX-rate, r and q are the risk-free log returns of the variable and the base currency respectively, and N denotes the cumulative distribution function of the standard normal distribution. It is easy to see from put-call parity that the price of a European currency put option (p0) with the same parameters is as follows:

The Black-Scholes formula and other option pricing models are available in the fOptions package. We can use the BlackScholesOption or the GBSOption function, both of which are practically the same, and the latter is a shorthand alias for the prior function.

BlackScholesOption(TypeFlag, S, X, Time, r, b, sigma,...)

Here, TypeFlag is either the character c, which stands for call or p (put). S is the current price and sigma is the volatility of the underlying. X is the strike price and Time is the time to maturity.

The other two parameters are a bit tricky because r and b are the risk-free rates, but the second one is meaningless when pricing options for stocks with the original BS model. This indicates that we must set b = r to get the BS stock option model, and set b = r-q to get the currency option model or the stock option model with continuous dividend yield. The other parameters of the function are optional and we do not need them.

To see how it works, let's say we have an option for EUR with five years' maturity, and the strike price is 0.7. The USD risk-free rate is r = 3% and the EUR risk-free rate is q = 2%. 1 USD is currently 0.7450 EUR, so this is the spot price of the underlying. Let the EUR volatility be 20 percent. If we call the BlackSholesOption function with the given parameters, we will get the following result:

BlackScholesOption ("c", 0.7450, 0.7, 5, 0.03, 0.01, 0.2) Title: Black Scholes Option Valuation Call: GBSOption(TypeFlag = "c", S = 0.745, X = 0.7, Time = 5, r = 0.03, b = 0.01, sigma = 0.2) Parameters: Value: TypeFlag c S 0.745 X 0.7 Time 5 r 0.03 b 0.01 sigma 0.2 Option Price: 0.152222 Description: Thu Aug 07 20:13:28 2014

We can also check out the price of the put option:

BlackScholesOption("p", 0.7450, 0.7, 5, 0.03, 0.01, 0.2) Title: Black Scholes Option Valuation Call: GBSOption(TypeFlag = "p", S = 0.745, X = 0.7, Time = 5, r = 0.03, b = 0.01, sigma = 0.2) Parameters: Value: TypeFlag p S 0.745 X 0.7 Time 5 r 0.03 b 0.01 sigma 0.2 Option Price: 0.08061367 Description: Thu Aug 07 20:15:11 2014

Then, we can also check the consistency with the put-call parity, which takes the following form for the currency options:

c - p = S*exp(-r*T)–X*exp(-q*T)

Substituting the data, on the left hand-side we have:

c - p = 0.152222 - 0.08061367 = 0.07160833,

On the right-hand side, we have:

0.745*exp(-0.02*5)-0.7*exp(-0.03*5) = 0.07160829.

It is important to mention that pricing a currency option is equivalent to pricing an option with any kind of underlying asset that grants continuous yield. For example, if the underlying is a stock or stock index with dividend yield q per annum, then the pricing formulas are the same as mentioned earlier.